Ball Bearings Market Size 2025-2029

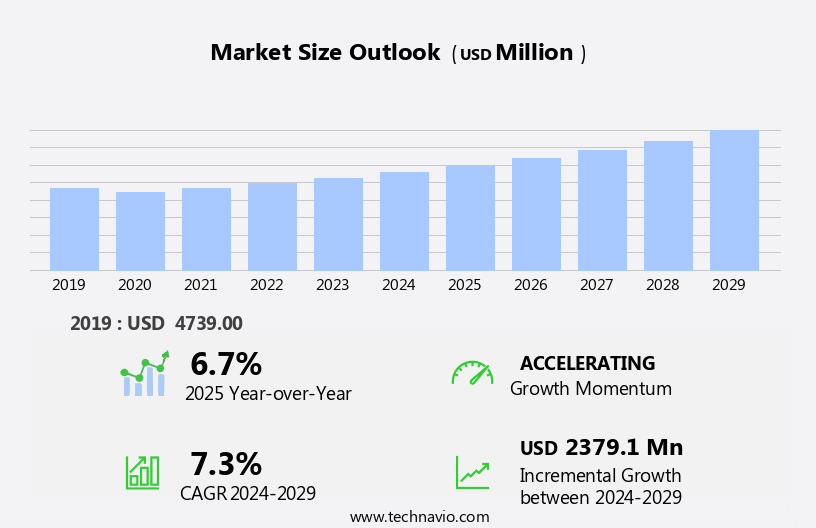

The ball bearings market size is forecast to increase by USD 2.38 billion, at a CAGR of 7.3% between 2024 and 2029.

- The rising demand for ball bearings from the automotive sector will be one of the key factors impelling the market's growth. This sector's increasing demand for efficient and durable components is fueling the market's expansion. Additionally, the introduction of new ball bearing products, such as ceramic and magnetic bearings, is broadening the market's scope and catering to various industries' specific requirements. However, the market faces challenges from fluctuating raw material prices, which can impact the cost structure and profitability of manufacturers.

- Navigating these price fluctuations through effective supply chain management and exploring alternative raw material sources will be crucial for companies seeking to capitalize on market opportunities and maintain competitiveness. Further, the complex designs of the roller bearing can be further leveraged by adding more rolling elements to enhance wear and tear resistance as well as strength.

What will be the Size of the Ball Bearings Market during the forecast period?

- The market encompasses various aspects, including bearing installation, temperature management, vibration analysis, seals, assembly, and disassembly. These bearings are essential for various systems in a car, including air conditioning, automatic transmission, electric power steering, and rear-wheel drive driveline setups. Advanced bearing manufacturing technology has led to automation and robotics in bearing production, ensuring precision and consistency. Bearing fatigue, wear, and failure analysis are crucial for predicting and mitigating potential issues, while alignment and torque management are essential for optimal performance. Linear ball bearings, spherical ball bearings, needle roller bearings, and roller bearings each offer unique advantages, with their selection depending on the specific application requirements. Bearing raceways, cages, and housings play vital roles in enhancing the overall efficiency and longevity of the bearings.

- Bearing temperature and lubrication analysis are integral to maintaining optimal operating conditions. Performance simulation, design optimization, life prediction, and lubrication systems are essential tools for engineers to ensure the highest possible bearing efficiency and reliability. Bearing vibration levels and noise analysis are essential for monitoring the health of machinery, enabling preventive maintenance and minimizing downtime. Further, the complex designs of the roller bearing can be further leveraged by adding more rolling elements to enhance wear and tear resistance as well as strength. By focusing on these aspects, businesses can improve their overall productivity and competitiveness in the market.

How is this Ball Bearings Industry segmented?

The ball bearings industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Automotive industry

- Heavy industry

- Aerospace and railway industry

- Others

- Product

- Deep groove

- Angular contact

- Self-aligning

- Others

- Product Type

- Grease-lubricated bearings

- Oil-lubricated bearings

- Dry bearings

- Type

- Conventional bearings

- Smart bearings

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By End-user Insights

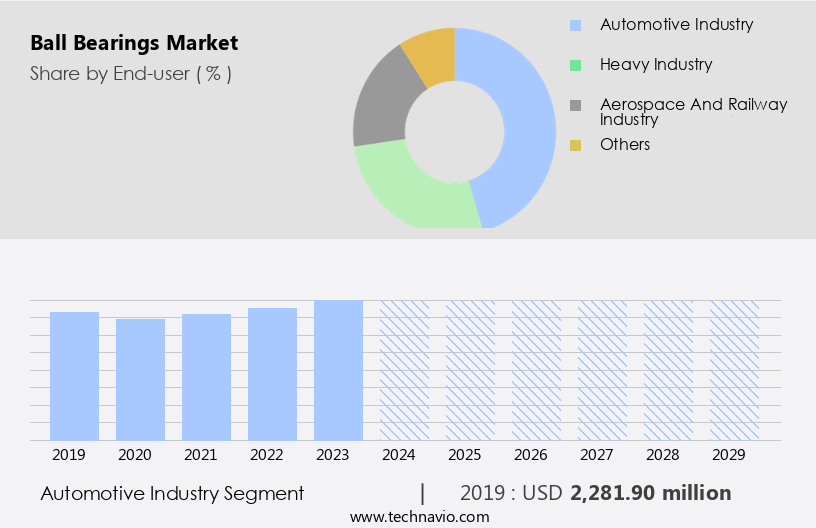

The automotive industry segment is estimated to witness significant growth during the forecast period. As the automotive manufacturers use miniature ball bearings in their throttle bodies, fan motors, and anti-lock braking applications, the surging demand for these components will have a direct impact on the demand for miniature ball bearings. The market encompasses a range of products, including industrial ball bearings, which are integral to various industries for reducing friction and enhancing mechanical efficiency. Radial ball bearings and low-noise ball bearings are key types, with the former supporting radial loads and the latter designed for quiet operation. Ball bearing failures can occur due to various reasons, such as lubrication failure or dynamic overloading. Grease lubrication and oil lubrication are common methods for maintaining ball bearings, with ISO standards providing guidelines for their manufacturing and certification. High-precision ball bearings, such as those used in aerospace and medical applications, demand stringent quality control.

Ball bearings are also used in automotive applications, including automotive ball bearing replacement in wheel hub assemblies and transmission systems, contributing to vehicle stability, ride comfort, and energy efficiency. Ball bearing materials, such as steel and ceramics, impact their cost, durability, and performance. Ball bearing inspection and testing ensure their quality and reliability, while innovations in ball bearing design, such as self-aligning and hybrid ball bearings, expand their applications. Ball bearing manufacturing processes, including dynamic load rating and friction reduction techniques, influence their efficiency and lifespan. Ultra-precision ball bearings and vibration analysis are essential for high-speed applications, while agricultural and miniature ball bearings cater to specific industries. Ball bearing maintenance practices, such as cleaning and lubrication, are crucial for ensuring their longevity and optimal performance. The market is also experiencing growth, driven primarily by the surging demand for high-quality bearings in various industries, including manufacturing, and renewable energy.

The Automotive industry segment was valued at USD 2.28 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

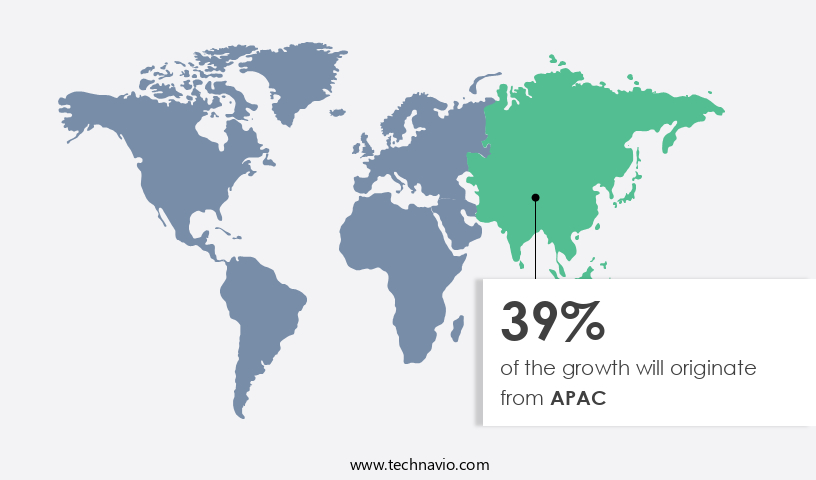

APAC is estimated to contribute 39% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market is experiencing significant growth in the Asia-Pacific (APAC) region due to the rapid industrial evolution, driven by advancements in electric vehicles, renewable energy, shipbuilding, aerospace, and mining. China, in particular, is a major growth engine, accounting for over 70% of global electric vehicle (EV) production and 80% of domestic EV sales in 2024. This pivotal role in the global automotive supply chain necessitates the use of specialized ball bearings for electric motors, drivetrains, and wheel assemblies. Ball bearings are essential components for ensuring smooth, efficient, and durable operation in machinery and equipment.

The market encompasses various types, including radial ball bearings, self-aligning ball bearings, thrust ball bearings, miniature ball bearings, and high-precision ball bearings, among others. Ball bearings are manufactured using different materials, such as steel, ceramic, and hybrid, to cater to diverse applications and requirements. ISO standards and ABEC standards govern the quality and performance of ball bearings. Proper lubrication, either oil or grease, is crucial for their longevity and efficiency. Ball bearing failures can result from various factors, including lubrication failure, static load rating, and dynamic load rating. Regular inspection, testing, and maintenance are essential to prevent premature failure and ensure optimal performance.

Ball bearings are used extensively in various industries, including automotive, agriculture, aerospace, and medical, among others. The demand for energy efficiency and reliability is driving innovation in ball bearing design and manufacturing. Ultra-precision ball bearings, hybrid ball bearings, and ceramic ball bearings are some of the recent innovations in the market. The market is witnessing robust growth in the APAC region due to the transformative industrial evolution. The demand for specialized ball bearings, particularly in the electric vehicle industry, is driving consumption and innovation in the market. Proper maintenance, lubrication, and adherence to standards are essential to ensure the longevity and efficiency of ball bearings.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Ball Bearings market drivers leading to the rise in the adoption of Industry?

- The automotive industry's growth serves as the primary catalyst for market expansion. The automotive industry's expansion, driven primarily by the increasing adoption of electric vehicles (EVs), significantly impacts the demand for ball bearings. Ball bearings are essential components in automotive systems, facilitating rotational motion and minimizing friction in various applications, including wheel hubs, transmissions, electric motors, and auxiliary systems. In 2024, global EV sales reached over 17 million units, representing a substantial 25% increase from the previous year. This growth underscores the automotive sector's transition towards electrification, fueled by regulatory requirements, technological innovations, and consumer preference for eco-friendly mobility solutions.

What are the Ball Bearings market trends shaping the Industry?

- The introduction of new products is a current market trend. Professionals in the industry are expected to stay informed about the latest innovations. The global market is experiencing significant innovation, particularly in the development of advanced bearing solutions for electric vehicle (EV) applications. Manufacturers are focusing on creating products that meet the demands of high-speed performance, energy efficiency, and compact design. In March 2025, NSK Ltd. introduced a deep groove ball bearing, which is compact and lightweight, designed specifically for EV drive units. This new bearing achieves a reduction in outer diameter and weight of approximately 10 percent and 51 percent, respectively, compared to conventional models. The bearing's newly engineered narrow-width combined plastic cage contributes to lower friction and supports rotational speeds surpassing a dmn value of 2.

- This shift towards advanced bearing solutions underscores the importance of oil lubrication and grease lubrication in ensuring optimal performance and longevity. Additionally, the market is witnessing a growing emphasis on iso standards, high-precision ball bearings, and low-noise ball bearings to meet the evolving needs of various industries. Ball bearing failures continue to be a concern, necessitating regular inspection and testing to maintain productivity and minimize downtime. Overall, the ball bearing market is witnessing a dynamic landscape, driven by technological advancements and evolving industry demands.

How does Ball Bearings market face challenges during its growth?

- The volatile pricing of raw materials poses a significant challenge to the industry's growth trajectory. The market faces ongoing volatility due to fluctuations in raw material prices, particularly for steel, a key component in bearing manufacturing. Steel's pricing is influenced by external pressures such as rising costs for raw materials like iron ore and coal. For example, iron ore prices outside China increased from USD 105 per tonne in August 2023 to USD 135 per tonne in December 2023. This price instability can impact production economics and supply chain stability. Ball bearings are precision-engineered components with high demands for quality, making the use of high-grade materials essential.

- Other factors affecting the market include static load rating, ABEC standards, high-speed ball bearings, ball bearing pricing, premature failure, ball bearing maintenance, and certification. Ensuring compliance with standards like ABEC and maintaining ball bearings properly can help mitigate risks and improve overall performance. Despite these challenges, the market is expected to continue its growth trajectory, driven by the increasing demand for fuel-efficient and high-performance vehicles, along with advancements in automation that streamline production and enhance product quality.

Exclusive Customer Landscape

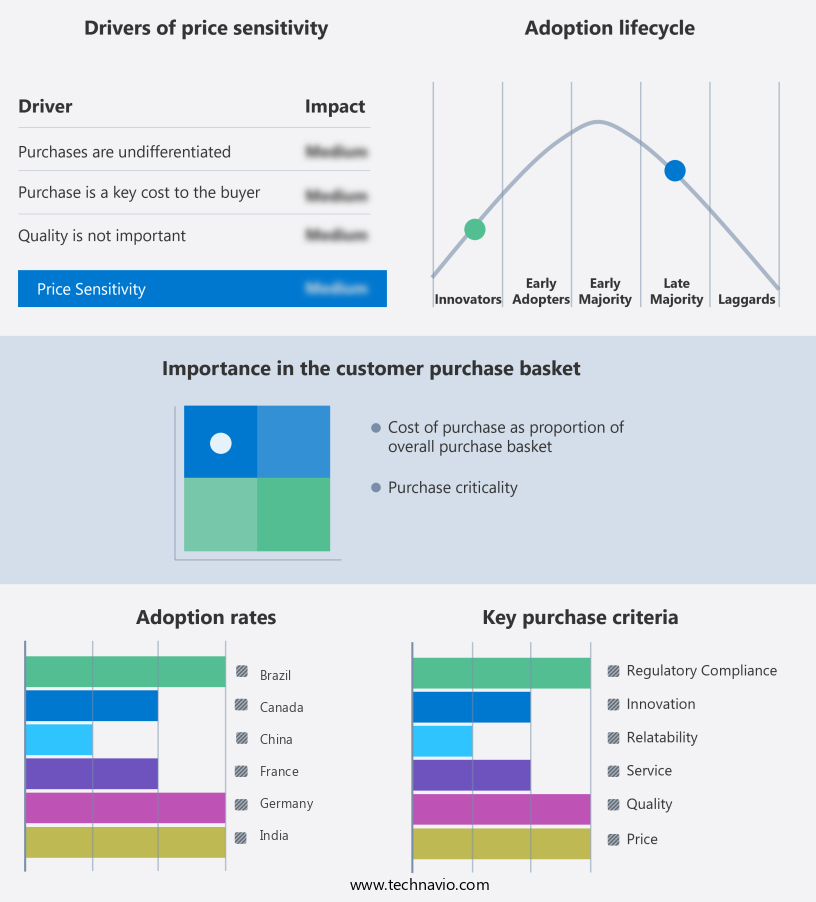

The ball bearings market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ball bearings market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, ball bearings market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AB SKF - This company specializes in providing a range of ball bearings, including single and double row angular contact, four-point contact, and deep groove types.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AB SKF

- ASAHI SEIKO Co. Ltd.

- C and U Group

- Grupo NBI

- Harbin Bearing Manufacturing Co. Ltd.

- HKT BEARINGS Ltd.

- JTEKT Corp.

- LYC Bearing Corp.

- MinebeaMitsumi Inc.

- NACHI FUJIKOSHI Corp.

- NSK Ltd.

- NTN Corp.

- RBC Bearings Inc.

- Regal Rexnord Corp.

- Schaeffler AG

- Sriji Gopalji Foundries Pvt. Ltd

- The Timken Co.

- ZWZ Bearing

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ball Bearings Market

- In March 2023, SKF, a leading ball bearing manufacturer, announced the launch of its new innovative deep groove ball bearing with increased load capacity. This new product is designed to cater to the growing demand for high-performance bearings in the wind energy sector (SKF Press Release, 2023).

- In August 2024, Schaeffler, another key player in the market, entered into a strategic partnership with Bosch Rexroth to develop and produce advanced bearing solutions for electric and hybrid vehicles. This collaboration aims to enhance Schaeffler's presence in the automotive industry and strengthen its product portfolio (Bosch Press Release, 2024).

- In November 2024, NSK Ltd, a major ball bearing manufacturer, acquired the bearing business of a leading European competitor, expanding its market share in Europe and enhancing its product offerings. The acquisition was valued at approximately USD 500 million (NSK Press Release, 2024).

- In January 2025, the European Union announced a new policy initiative to promote the use of energy-efficient ball bearings in various industries, including wind energy, automotive, and manufacturing. This policy change is expected to drive the demand for ball bearings in Europe and boost the market growth (European Commission Press Release, 2025).

Research Analyst Overview

The market continues to evolve, driven by the diverse demands of various sectors. Radial and thrust bearings, integral components in numerous industries, undergo constant development to meet the evolving needs of applications. Oil and grease lubrication methods persistently adapt to optimize performance and efficiency. ABEC standards, a critical aspect of ball bearing specifications, continue to advance, ensuring high-precision and reliability. Static and dynamic load ratings are meticulously engineered to accommodate increasing demands. High-speed ball bearings, a vital segment, are subject to continuous innovation to enhance friction reduction and energy efficiency. Ball bearing pricing remains a significant consideration, with manufacturers focusing on cost-effective solutions without compromising quality.

The Ball Bearings Market continues to expand with diverse ball bearing types, including specialized steel ball bearings for durability and precision. Effective ball bearing lubrication enhances performance and lifespan, while rigorous ball bearing testing ensures reliability across multiple ball bearing applications. Industries such as automotive ball bearings, aerospace ball bearings, agricultural ball bearings, and medical ball bearings drive demand for specialized solutions. Proper ball bearing cleaning helps reduce ball bearing noise and maintain ball bearing efficiency. Factors like ball bearing cost influence procurement decisions, while ongoing ball bearing innovations improve technology. Adherence to strict ball bearing standards ensures quality and consistency, supporting growth across various sectors.

The Ball Bearings Market continues to evolve with advancements in bearing seals and bearing housings, ensuring durability and protection. Efficient bearing lubrication systems optimize performance, while precise bearing assembly and bearing disassembly improve maintenance processes. Proper bearing alignment enhances functionality, minimizing bearing torque issues and reducing bearing noise levels. In-depth bearing lubrication analysis helps prevent wear, supporting effective bearing failure analysis for enhanced reliability. Innovations in bearing life prediction and bearing performance simulation drive efficiency, while bearing design optimization ensures adaptability across industries. The rise of bearing automation streamlines manufacturing, promoting consistent quality and improved operational workflow.

Premature failure, a persistent challenge, is addressed through rigorous testing, inspection, and certification processes. Ball bearing materials, including steel, ceramic, and hybrid composites, are continually refined to improve durability and reduce noise. Maintenance and cleaning techniques evolve to minimize downtime and extend ball bearing life expectancy. ISO standards and ball bearing design innovations ensure compliance with evolving industry regulations and requirements. Self-aligning ball bearings, ultra-precision bearings, and vibration analysis are among the many advancements shaping the ball bearing landscape. Ball bearings find applications in automotive, aerospace, agricultural, medical, and numerous other industries, underscoring their indispensable role in modern technology. The continuous dynamism of the market reflects the ongoing quest for enhanced performance, reliability, and efficiency.

Dive into Technavio's strong research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ball Bearings Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

252 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.3% |

|

Market growth 2025-2029 |

USD 2.38 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.7 |

|

Key countries |

China, US, Japan, India, Germany, Canada, UK, Brazil, South Korea, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Ball Bearings Market Research and Growth Report?

- CAGR of the Ball Bearings industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the ball bearings market growth of industry companies

We can help! Our analysts can customize this ball bearings market research report to meet your requirements.

RIA -

RIA -