Supply Chain Management (SCM) Software Market Size 2026-2030

The supply chain management (scm) software market size is valued to increase by USD 29.63 billion, at a CAGR of 15.2% from 2025 to 2030. Strategic mainstreaming of agentic AI and autonomous decision-support systems will drive the supply chain management (scm) software market.

Major Market Trends & Insights

- North America dominated the market and accounted for a 35.8% growth during the forecast period.

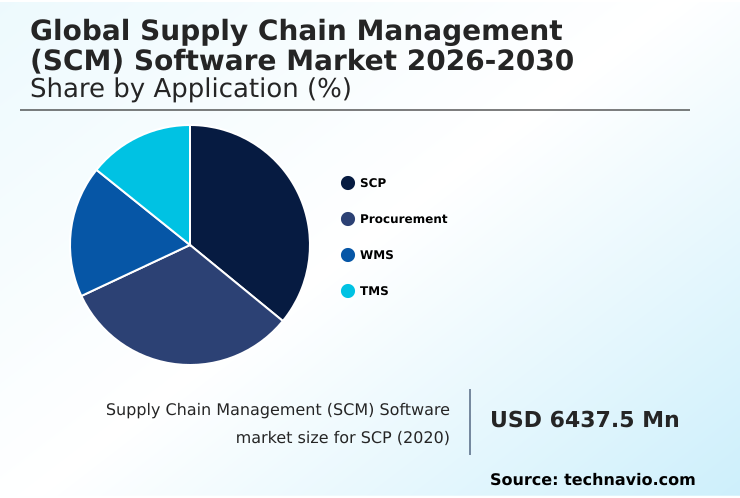

- By Application - SCP segment was valued at USD 9.26 billion in 2024

- By Deployment - On-premises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 40.55 billion

- Market Future Opportunities: USD 29.63 billion

- CAGR from 2025 to 2030 : 15.2%

Market Summary

- The supply chain management (SCM) software market is undergoing a significant transformation, moving beyond traditional data reporting to embrace autonomous orchestration and agentic intelligence. This evolution is driven by the need for enterprises to build resilient, self-healing supply chains capable of navigating persistent global trade volatility.

- Core to this shift is the adoption of unified, cloud-native platforms that integrate advanced technologies like artificial intelligence, digital twins, and generative AI. For instance, a global manufacturer can now leverage a digital twin of its entire network to simulate the impact of a potential port strike, allowing it to proactively reroute shipments and adjust inventory levels before disruptions occur.

- The market is also heavily influenced by the mandatory digitalization of sustainability and ESG compliance, compelling firms to invest in solutions that provide end-to-end visibility into multi-tier supplier ethics and Scope 3 emissions.

- However, this progress is tempered by challenges such as the technical complexity of integrating modern software with legacy systems and the escalating threat of cybersecurity risks in highly interconnected digital ecosystems. The democratization of technology through low-code/no-code platforms is a key trend, empowering business users to develop custom applications and accelerate digital adoption across the organization.

What will be the Size of the Supply Chain Management (SCM) Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Supply Chain Management (SCM) Software Market Segmented?

The supply chain management (scm) software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- SCP

- Procurement

- WMS

- TMS

- Deployment

- On-premises

- Cloud-based

- Component

- Software

- Services

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- China

- Japan

- South Korea

- Middle East and Africa

- Saudi Arabia

- South Africa

- Turkey

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Application Insights

The scp segment is estimated to witness significant growth during the forecast period.

The supply chain planning (SCP) segment is shifting from periodic planning cycles toward continuous, event-driven models powered by predictive demand sensing and autonomous orchestration. Modern platforms now use digital twin technology for real-time disruption simulation, allowing for proactive strategy testing.

A key development is the integration of agentic AI, with software agents now capable of independently identifying supply-demand imbalances and executing corrective actions, a transition that has improved forecast accuracy by over 15% in early adoption cases.

This move toward self-healing networks, which also incorporate prescriptive analytics and ethical sourcing metrics, minimizes reliance on manual forecasting. The evolution of low-code/no-code platforms and cloud-native orchestration further democratizes access to advanced optimization tools, enhancing overall system resilience and performance.

The SCP segment was valued at USD 9.26 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Supply Chain Management (SCM) Software Market Demand is Rising in North America Get Free Sample

The global supply chain management (SCM) software market is geographically led by North America, which accounts for over 35% of the incremental growth, driven by its sophisticated technological ecosystem and rapid adoption of predictive demand sensing and warehouse automation.

Europe follows closely, with its market heavily influenced by stringent regulatory frameworks like the Corporate Sustainability Reporting Directive, which mandates deep multi-tier supplier transparency and Scope 3 emissions tracking.

The APAC region is the fastest-growing market, with a CAGR of 15.7%, propelled by massive industrialization and the expansion of the digital economy in countries like China and India.

These regions are prioritizing cloud-native orchestration and dynamic freight optimization to manage complex, high-volume trade corridors, underscoring the global demand for agile, intelligent, and compliant supply chain solutions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Enterprises are increasingly focusing on strategic SCM initiatives to gain a competitive edge. A primary area of investment is in AI-driven procurement automation benefits, where machine learning algorithms optimize sourcing decisions and automate routine purchasing tasks, leading to significant cost reductions and improved supplier performance.

- Simultaneously, the adoption of cloud-native SCM for SMEs is democratizing access to advanced capabilities, allowing smaller businesses to compete with larger corporations on agility and efficiency.

- This trend is complemented by the growing importance of ESG compliance reporting software, which provides the necessary tools to track and report on sustainability metrics across the entire value chain, meeting both regulatory requirements and consumer expectations. To manage increasing complexity and risk, companies are turning to a digital twin for supply chain risk simulation.

- This technology allows them to model various disruption scenarios and develop robust contingency plans. Furthermore, the integration of generative AI in demand forecasting is revolutionizing how businesses predict market trends, with natural language queries enabling more intuitive and accurate analysis.

- This shift toward intelligent, interconnected, and sustainable supply chains is redefining operational excellence, with companies leveraging advanced software reporting double-digit improvements in operational efficiency compared to those relying on legacy systems.

What are the key market drivers leading to the rise in the adoption of Supply Chain Management (SCM) Software Industry?

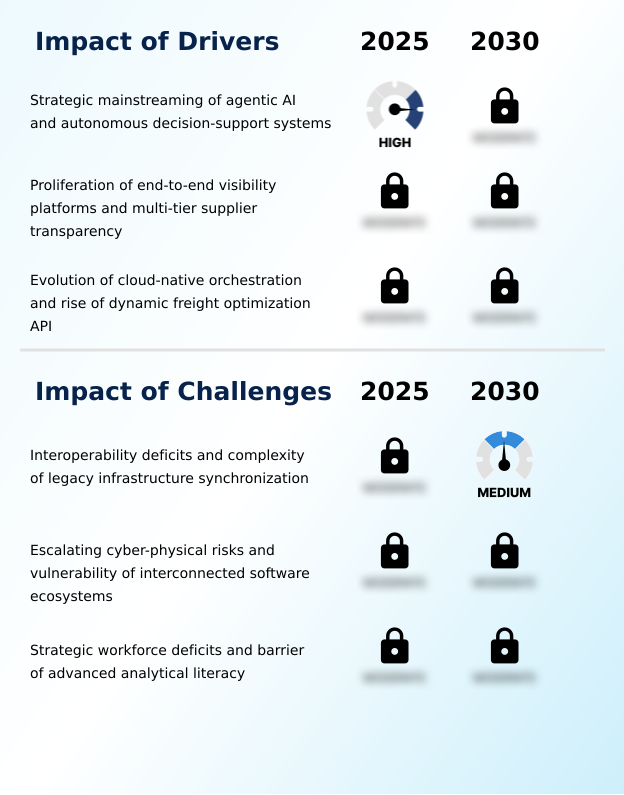

- The strategic mainstreaming of agentic AI and autonomous decision-support systems is a key driver of market growth.

- Market growth is propelled by the strategic mainstreaming of agentic AI for autonomous decision-making across logistics networks. This shift addresses the need to shorten disruption response times, with software agents now capable of automatically rerouting shipments based on predictive analytics.

- A second major driver is the proliferation of end-to-end visibility platforms, which provide transparency into multi-tier supplier networks to identify hidden risks and ensure regulatory compliance.

- Supply chain concerns have doubled year-over-year, leading to a sevenfold increase in exploration of technologies like digital twins for traceability.

- Finally, the evolution of cloud-native orchestration and dynamic freight optimization APIs provides the real-time modal flexibility needed to navigate fluctuating costs and capacity constraints, making advanced demand forecasting accessible to more businesses.

What are the market trends shaping the Supply Chain Management (SCM) Software Industry?

- The digitalization of mandatory sustainability and Environmental, Social, and Governance (ESG) compliance is an increasingly vital market trend.

- Key market trends are centered on sustainability, circularity, and democratization. The transition toward mandatory ESG compliance is compelling companies to adopt auditable, real-time data platforms for tracking Scope 3 emissions and ethical sourcing metrics. This is creating significant demand for digital product passports.

- Concurrently, the rise of circular supply chain platforms, a sector projected to grow at 13.7%, is enabling robust material recovery tracking and reverse logistics. This trend is crucial for managing cradle-to-cradle product lifecycles. Furthermore, the democratization of development through low-code/no-code platforms is accelerating digital transformation, with forecasts indicating that 70% of new SCM applications will use these technologies.

- This allows for greater innovation and customization using tools for procurement automation and inventory optimization.

What challenges does the Supply Chain Management (SCM) Software Industry face during its growth?

- Interoperability deficits and the complexity of synchronizing with legacy infrastructure are key challenges affecting industry growth.

- The market faces significant structural challenges, led by interoperability deficits between modern cloud platforms and legacy infrastructure, a problem cited by 83% of supply chain professionals as a primary decelerator for digital transformation. This technical debt creates data silos that inhibit end-to-end visibility and agile decision-making. Another critical challenge is the escalation of cyber-physical risks within interconnected software ecosystems.

- The expanded attack surface of cloud-based models requires a move toward zero-trust architecture to protect against sophisticated threats. Finally, a strategic workforce deficit and a lack of advanced analytical literacy hinder the effective use of sophisticated tools for prescriptive analytics and warehouse automation, leading to underutilization and poor returns on investment for many organizations.

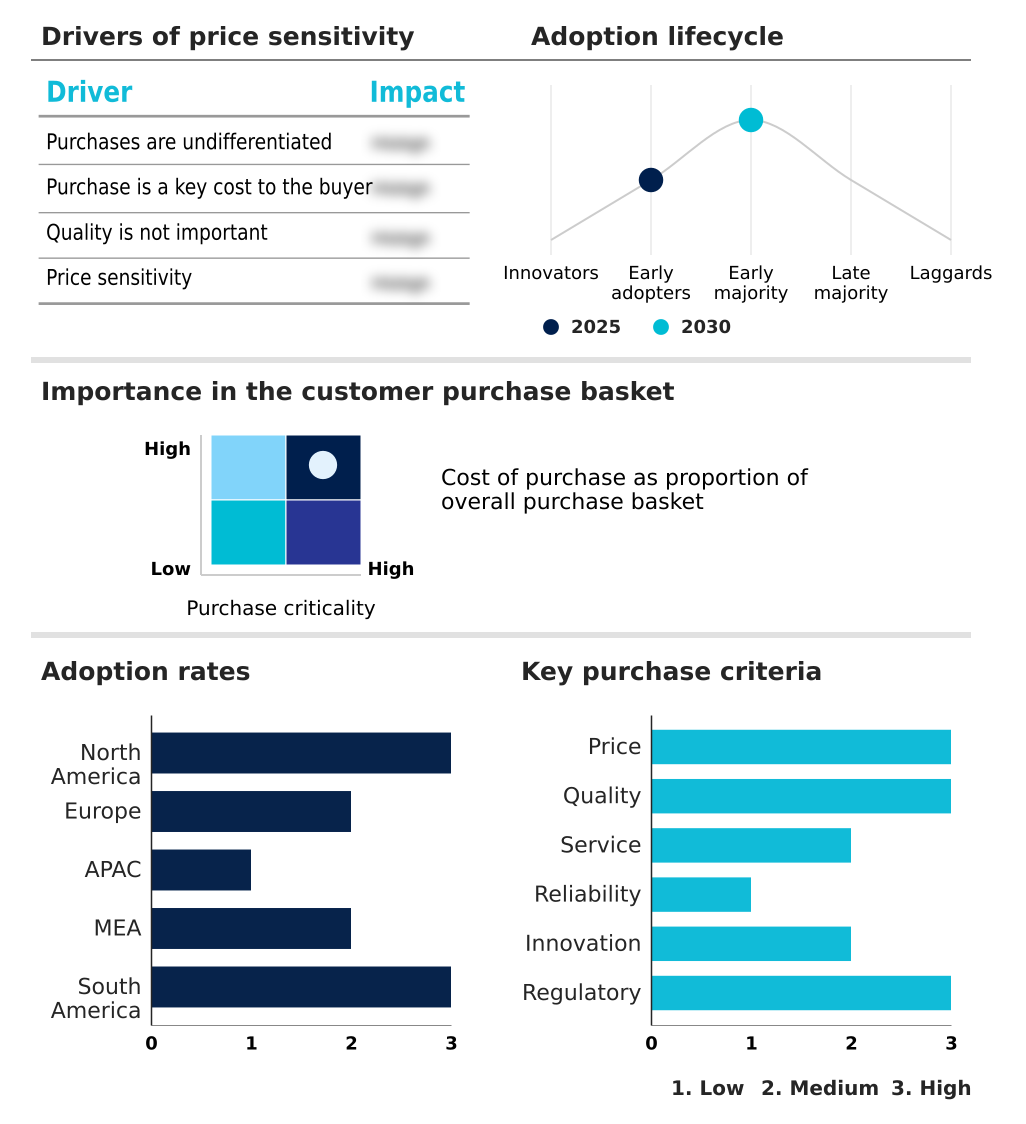

Exclusive Technavio Analysis on Customer Landscape

The supply chain management (scm) software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the supply chain management (scm) software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Supply Chain Management (SCM) Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, supply chain management (scm) software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Blue Yonder Group Inc. - Offerings center on AI-driven demand planning, inventory optimization, and comprehensive logistics solutions that facilitate autonomous, resilient, and transparent end-to-end supply chain operations.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Blue Yonder Group Inc.

- Coupa Software Inc.

- Descartes Systems Group Inc.

- E2open Parent Holdings Inc.

- Epicor Software Corp.

- IBM Corp.

- Infor Inc.

- Jaggaer LLC

- Kinaxis Inc.

- Logility SCS Inc.

- Magaya Corp.

- Manhattan Associates Inc.

- Microsoft Corp.

- o9 Solutions Inc.

- Oracle Corp.

- Panasonic Holdings Corp.

- SAP SE

- Solvoyo Co.

- StockIQ Technologies Inc.

- Webgility Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Supply chain management (scm) software market

- In May, 2025, Oracle announced the launch of specialized AI agents within its Fusion Cloud Applications, designed to autonomously manage high-volume workflows like competitive bidding and the conversion of purchase orders.

- In March, 2025, a revised technology forecast from a leading research firm predicted that 70% of new enterprise applications in the supply chain sector will utilize low-code or no-code technologies by year-end.

- In December, 2024, a major global trade management platform launched a localized compliance engine designed to automate the classification of goods under new, highly complex tariff and environmental tax regimes.

- In September, 2024, a Thomson Reuters Global Trade Report revealed that supply chain concerns among trade professionals doubled year-over-year, leading to a sevenfold increase in the exploration of emerging technologies for traceability.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Supply Chain Management (SCM) Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 296 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 15.2% |

| Market growth 2026-2030 | USD 29629.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 13.5% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Spain, Italy, The Netherlands, China, Japan, South Korea, India, Australia, Indonesia, Saudi Arabia, South Africa, Turkey, UAE, Israel, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The supply chain management (SCM) software market is rapidly evolving from systems of record to intelligent engines of autonomous decision-making. The integration of agentic AI and digital twin technology is becoming standard, enabling a human-plus-agent framework where software executes corrective actions based on predictive demand sensing and real-time geopolitical risk signals.

- This shift toward continuous planning and low-touch planning is critical for navigating volatility. A major boardroom consideration is the mandatory implementation of scope 3 emissions tracking and ethical sourcing metrics, which necessitates platforms capable of ensuring multi-tier supplier transparency. While the benefits are clear, nearly 83% of professionals identify legacy infrastructure synchronization as a primary barrier.

- The move to cloud-native orchestration and the use of generative AI for natural language queries are helping to overcome these hurdles. Successful deployment requires a focus on zero-trust architecture to mitigate cyber-physical risks, alongside investments in circular supply chain modules for material recovery tracking and reverse logistics to achieve sustainability goals.

What are the Key Data Covered in this Supply Chain Management (SCM) Software Market Research and Growth Report?

-

What is the expected growth of the Supply Chain Management (SCM) Software Market between 2026 and 2030?

-

USD 29.63 billion, at a CAGR of 15.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (SCP, Procurement, WMS, and TMS), Deployment (On-premises, and Cloud-based), Component (Software, and Services) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Strategic mainstreaming of agentic AI and autonomous decision-support systems, Interoperability deficits and complexity of legacy infrastructure synchronization

-

-

Who are the major players in the Supply Chain Management (SCM) Software Market?

-

Blue Yonder Group Inc., Coupa Software Inc., Descartes Systems Group Inc., E2open Parent Holdings Inc., Epicor Software Corp., IBM Corp., Infor Inc., Jaggaer LLC, Kinaxis Inc., Logility SCS Inc., Magaya Corp., Manhattan Associates Inc., Microsoft Corp., o9 Solutions Inc., Oracle Corp., Panasonic Holdings Corp., SAP SE, Solvoyo Co., StockIQ Technologies Inc. and Webgility Inc.

-

Market Research Insights

- Market dynamics are increasingly shaped by the push for systemic resilience over pure cost optimization, a shift where 68% of trade professionals now cite supply chain reliability as their top strategic concern. The adoption of advanced software, particularly for spend management and global trade compliance, is accelerating.

- Organizations are leveraging supply chain orchestration platforms to manage complex supplier relationships and automate procurement processes. This has led to a sevenfold increase in the exploration of technologies like blockchain for traceability.

- Furthermore, the focus on omnichannel fulfillment and last-mile delivery modules is intensifying, driven by the need to meet heightened consumer expectations for speed and transparency in the final stages of the supply chain.

We can help! Our analysts can customize this supply chain management (scm) software market research report to meet your requirements.

RIA -

RIA -