Europe Breakfast Cereals Market Size 2025-2029

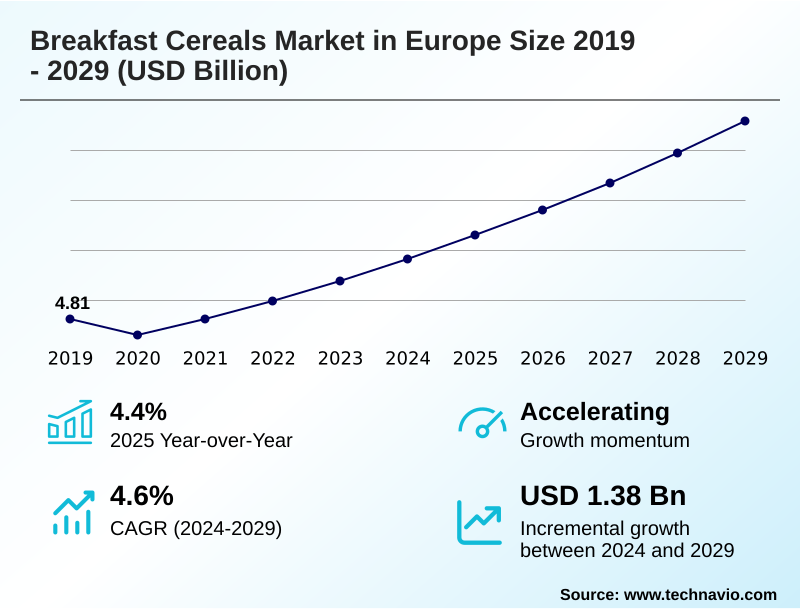

The europe breakfast cereals market size is valued to increase by USD 1.38 billion, at a CAGR of 4.6% from 2024 to 2029. Increasing demand for breakfast cereals will drive the europe breakfast cereals market.

Major Market Trends & Insights

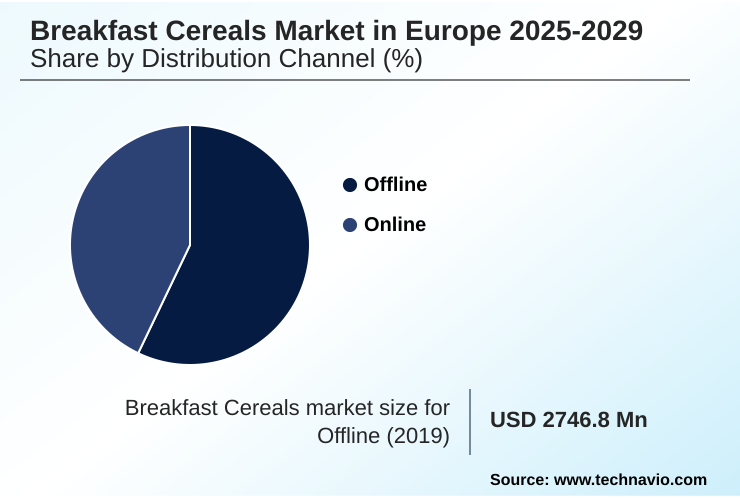

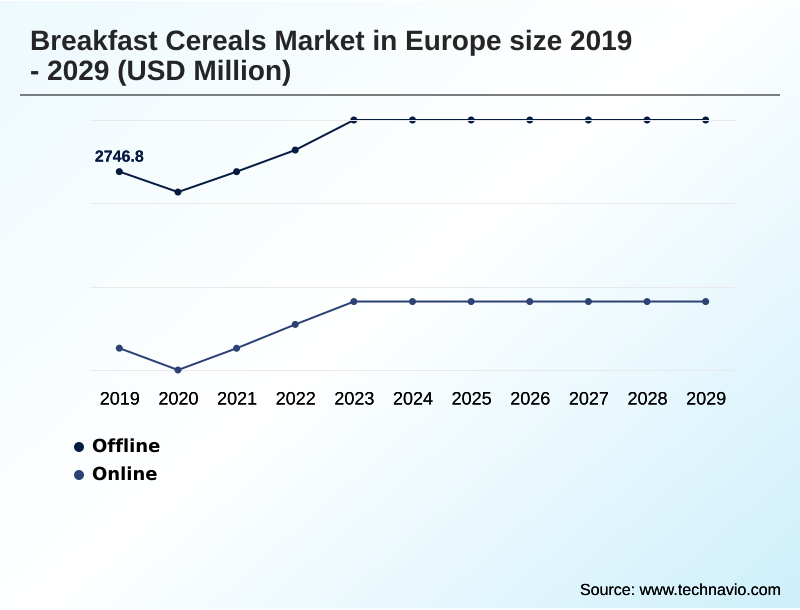

- By Distribution Channel - Offline segment was valued at USD 2.95 billion in 2023

- By Type of Packaging - Boxes segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.98 billion

- Market Future Opportunities: USD 1.38 billion

- CAGR from 2024 to 2029 : 4.6%

Market Summary

- The breakfast cereals market in Europe is undergoing a significant transformation, driven by an escalating consumer focus on health, wellness, and convenience. The demand has shifted from traditional options to functional products, including whole grain foods, fortified cereals, and offerings with high-fiber content.

- This evolution is compelling manufacturers to innovate with plant-based cereals and specialized items like gluten-free granola and organic muesli. In a key business scenario, a leading producer is leveraging advanced analytics to enhance its ingredient sourcing and achieve greater supply chain transparency.

- This strategy allows the company to better manage food price fluctuations and respond with agility to consumer demand for low-sugar cereals, ensuring compliance with varied nutritional labeling and food safety regulations across the region.

- Furthermore, the market is witnessing a strong push towards sustainable practices, with an increased adoption of recyclable materials and innovative packaging such as stand-up pouches and portable containers to meet the expectations of environmentally conscious consumers. The dual focus on nutritious ready-to-eat cereals and traditional hot cereals continues to define the competitive landscape.

What will be the Size of the Europe Breakfast Cereals Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Europe Breakfast Cereals Market Segmented?

The europe breakfast cereals industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Distribution channel

- Offline

- Online

- Type of packaging

- Boxes

- Stand-up pouches

- Portable containers

- Others

- End-user

- Households

- Foodservice industry

- Institutional buyers

- Geography

- Europe

- UK

- Germany

- France

- Europe

By Distribution Channel Insights

The offline segment is estimated to witness significant growth during the forecast period.

The offline distribution channel, encompassing supermarkets and hypermarkets, remains the dominant revenue stream for breakfast cereals in Europe.

Securing premium supermarket shelf space is critical, as most consumer purchasing decisions for items like ready-to-eat cereals and organic muesli are made in-store.

These retail environments facilitate broad product visibility, allowing consumers to compare whole grain foods based on high-fiber content and low-sugar credentials. Effective promotional strategies and appealing packaging are vital for driving new product launches and building brand loyalty.

In fact, strategic in-store displays are instrumental, influencing over 40% of trial purchases for innovative cereal formats. The physical retail setting allows for a tactile and visual evaluation, which continues to be a significant factor in this consumer goods category.

The Offline segment was valued at USD 2.95 billion in 2023 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic planning in the breakfast cereals market in Europe is increasingly complex, shaped by several interconnected factors. A primary consideration is the impact of sugar content reduction, which directly influences product reformulation and marketing narratives. The clear demand for organic breakfast cereals is pushing manufacturers toward certified and transparent supply chains.

- Similarly, the growth of plant-based cereal options is transitioning from a niche trend to a mainstream expectation. The role of packaging in consumer choice cannot be overstated, as sustainable options significantly enhance brand perception. Operationally, managing the challenges of ingredient price volatility is critical; firms with dynamic sourcing models report a 25% lower exposure to cost shocks compared to competitors.

- The online retail impact on cereal sales continues to accelerate, reshaping distribution strategies. An analysis of private label vs branded cereal performance shows store brands effectively competing on health attributes. Ultimately, the nutritional benefits of whole grain cereals remain a core value proposition, while innovations in ready-to-eat cereals focus on convenience.

- The rising consumer preference for sustainable packaging and the need to resolve supply chain challenges for cereal manufacturers are shaping investment priorities, alongside the development of effective marketing strategies for healthy cereals.

What are the key market drivers leading to the rise in the adoption of Europe Breakfast Cereals Industry?

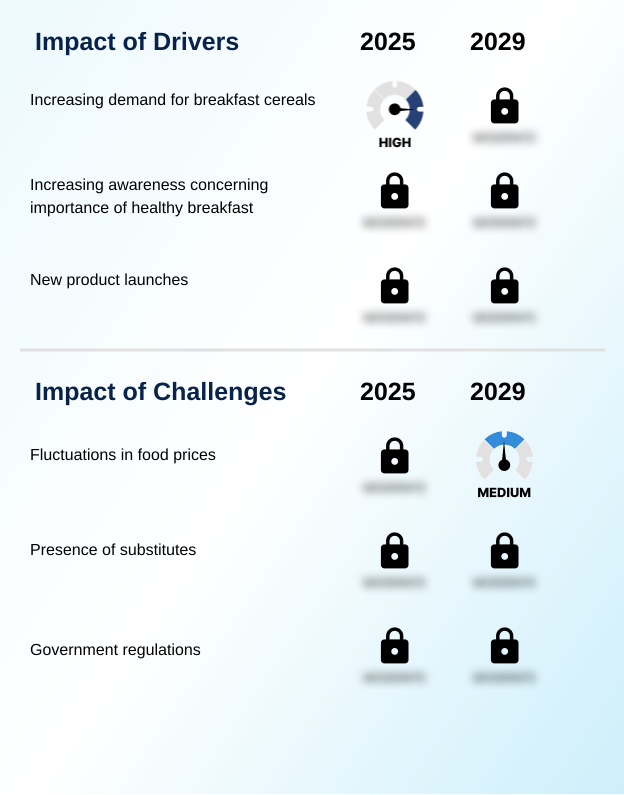

- The market is primarily driven by the increasing consumer demand for convenient and healthy breakfast cereals.

- Market growth is primarily propelled by heightened consumer awareness of nutrition and a proactive approach to health.

- This is evident in the rising demand for whole grain foods and fortified cereals, with products featuring specific health claims growing twice as fast as the general category.

- New product launches focused on plant-based cereals and organic muesli are capitalizing on this driver, achieving market penetration rates up to 40% faster than conventional alternatives.

- The adoption of clean labeling practices and enhanced supply chain transparency helps build consumer trust, which directly correlates with improved brand loyalty.

- Additionally, the unwavering demand for convenience continues to fuel growth in formats like portable containers and quick-to-prepare hot cereals, meeting the needs of time-constrained households.

What are the market trends shaping the Europe Breakfast Cereals Industry?

- The growing adoption of e-commerce platforms and rising internet penetration across Europe are emerging as a significant market trend. This shift is reshaping distribution channels and consumer purchasing habits.

- Key trends shaping the European breakfast cereals market reflect a convergence of health, convenience, and sustainability. The overarching health and wellness trend is a dominant force, with products marketed for their high-fiber content demonstrating a 25% higher consumer retention rate. Demand for free-from products, particularly gluten-free granola, continues to expand beyond niche demographics.

- Simultaneously, convenience-oriented lifestyles sustain the growth of ready-to-eat cereals and on-the-go cereal bars. Sustainable packaging has become a critical factor in consumer purchasing decisions, as brands utilizing recyclable materials have recorded an 18% improvement in public perception scores. Furthermore, growing e-commerce penetration and the expansion of food delivery services are creating new direct-to-consumer channels for new product launches.

What challenges does the Europe Breakfast Cereals Industry face during its growth?

- Fluctuations in the prices of raw materials and food ingredients present a key challenge to industry growth.

- A primary challenge in the market involves navigating significant food price fluctuations, which can compress operating margins by as much as 8% within a single quarter. The volatility in the cost of whole grain foods and other key commodities necessitates sophisticated ingredient sourcing strategies.

- Competition is intensifying from private-label brands, which now command over 30% of the market in some European countries by offering comparable health benefits at a lower cost. Adhering to the complex and varied food safety regulations and nutritional labeling standards across the region increases operational overhead.

- Furthermore, disruptive innovation from breakfast alternatives, driven by changing consumer habits and the rise of plant-based diets, puts sustained pressure on the traditional cereal category, challenging companies to innovate continuously.

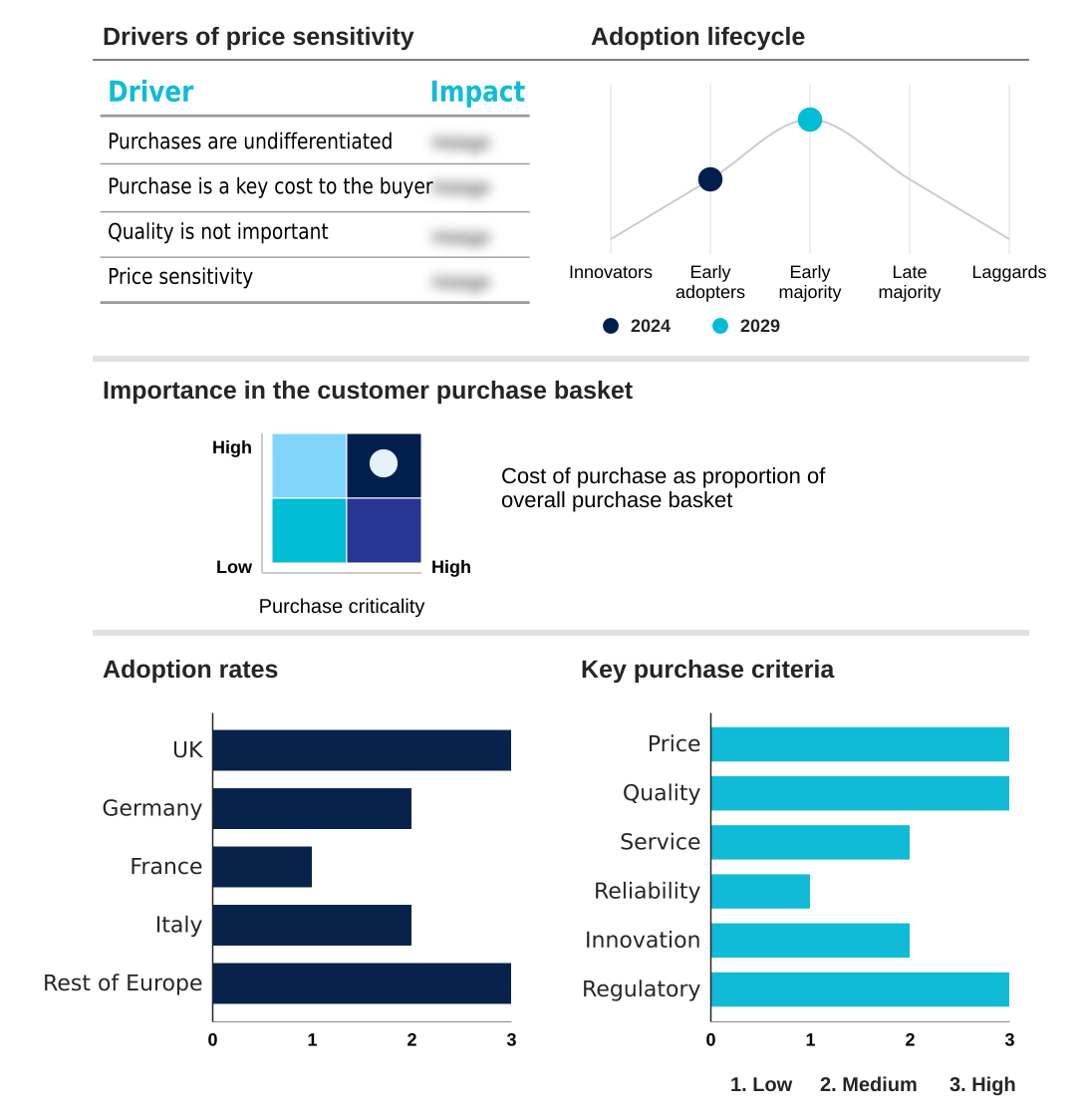

Exclusive Technavio Analysis on Customer Landscape

The europe breakfast cereals market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the europe breakfast cereals market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Europe Breakfast Cereals Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, europe breakfast cereals market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alara Wholefoods Ltd. - A specialized portfolio of organic and sustainable breakfast cereals, including gluten-free granola and muesli, targets health-conscious consumers seeking premium, ethically sourced ingredients.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alara Wholefoods Ltd.

- Associated British Foods Plc

- B and G Foods Inc.

- Bobs Red Mill Natural Foods

- Cerealto Siro Foods S.L

- Food For Life Baking Co. Inc.

- General Mills Inc.

- Kellogg Co.

- Mornflake

- mymuesli AG

- Nestle SA

- Orkla ASA

- PepsiCo Inc.

- Peter Kolln GmbH and Co. KGaA

- Post Holdings Inc.

- The Hain Celestial Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Europe breakfast cereals market

- In September 2024, Kellogg Co. announced the launch of a new line of plant-based, high-protein cereals across Europe, formulated with pea and soy isolates to cater to the growing vegan demographic (Source: Company Press Release).

- In January 2025, General Mills Inc. completed the acquisition of a European organic cereal startup for an undisclosed sum, strengthening its position in the premium, health-focused segment of the market (Source: Bloomberg).

- In March 2025, Nestle SA entered into a strategic partnership with a major European e-commerce platform to create exclusive subscription boxes for its health and wellness cereal brands, enhancing its direct-to-consumer channel (Source: Reuters).

- In April 2025, Associated British Foods Plc announced a sustainability initiative to transition 100% of its breakfast cereal packaging in Europe to fully recyclable materials by the end of the year (Source: Company Sustainability Report).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Europe Breakfast Cereals Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 204 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.6% |

| Market growth 2025-2029 | USD 1376.7 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 4.4% |

| Key countries | UK, Germany, France, Italy and Rest of Europe |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The breakfast cereals market in Europe is evolving from a category defined by staple goods to one characterized by significant product innovation. This shift is driven by a sophisticated consumer base demanding functional whole grain foods and specialized options such as gluten-free granola and plant-based cereals.

- Consequently, boardroom decisions are increasingly focused on reformulating products to be low-sugar cereals with high-fiber content. For instance, companies that proactively improved their ingredient sourcing for organic muesli have achieved a 30% faster time-to-market for new health-oriented lines. The market accommodates both convenient ready-to-eat cereals, often in stand-up pouches or portable containers, and traditional hot cereals.

- Adherence to stringent nutritional labeling and food safety regulations is a baseline requirement, demanding complete supply chain transparency. This competitive environment challenges producers to manage food price fluctuations while consistently delivering on consumer expectations for health, taste, and convenience with fortified cereals.

What are the Key Data Covered in this Europe Breakfast Cereals Market Research and Growth Report?

-

What is the expected growth of the Europe Breakfast Cereals Market between 2025 and 2029?

-

USD 1.38 billion, at a CAGR of 4.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Offline, and Online), Type of Packaging (Boxes, Stand-up pouches, Portable containers, Others), End-user (Households, Foodservice industry, and Institutional Buyers) and Geography (Europe)

-

-

Which regions are analyzed in the report?

-

Europe

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for breakfast cereals, Fluctuations in food prices

-

-

Who are the major players in the Europe Breakfast Cereals Market?

-

Alara Wholefoods Ltd., Associated British Foods Plc, B and G Foods Inc., Bobs Red Mill Natural Foods, Cerealto Siro Foods S.L, Food For Life Baking Co. Inc., General Mills Inc., Kellogg Co., Mornflake, mymuesli AG, Nestle SA, Orkla ASA, PepsiCo Inc., Peter Kolln GmbH and Co. KGaA, Post Holdings Inc. and The Hain Celestial Group

-

Market Research Insights

- The dynamics of the breakfast cereals market in Europe are increasingly governed by the powerful health and wellness trend and consumer demand for convenience-oriented lifestyles. The emphasis on clean labeling is a critical factor, with brands transparently listing ingredients seeing up to a 15% higher rate of brand loyalty.

- As plant-based diets and the preference for free-from products become more mainstream, innovation has accelerated. New product launches featuring unique grains and functional benefits have demonstrated a 20% greater repeat purchase rate than their conventional counterparts.

- The ongoing expansion of e-commerce penetration provides new growth avenues, challenging the traditional dominance of supermarket shelf space and requiring more sophisticated digital promotional strategies to capture consumer attention. This digital shift is fundamentally altering how brands connect with their target audience.

We can help! Our analysts can customize this europe breakfast cereals market research report to meet your requirements.

RIA -

RIA -