Cancer Supportive Care Market Size 2025-2029

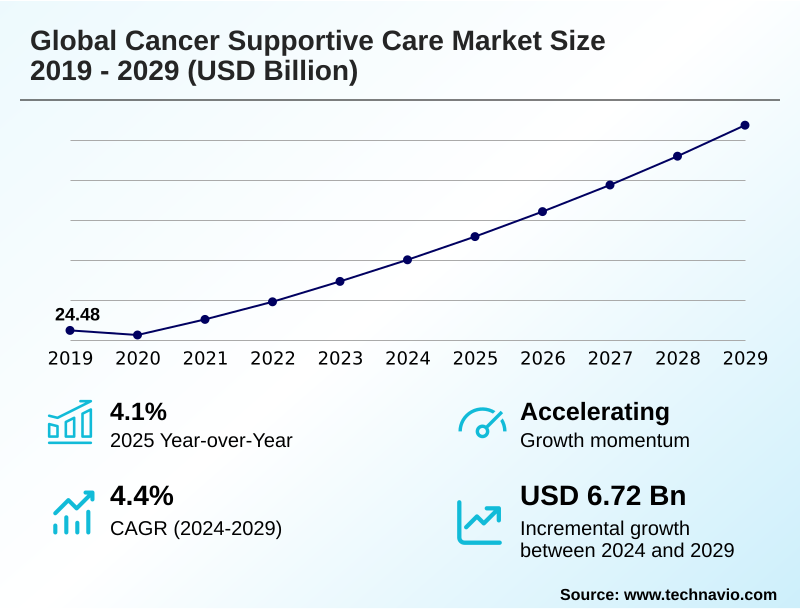

The cancer supportive care market size is valued to increase by USD 6.72 billion, at a CAGR of 4.4% from 2024 to 2029. Growing prevalence of cancer cases will drive the cancer supportive care market.

Major Market Trends & Insights

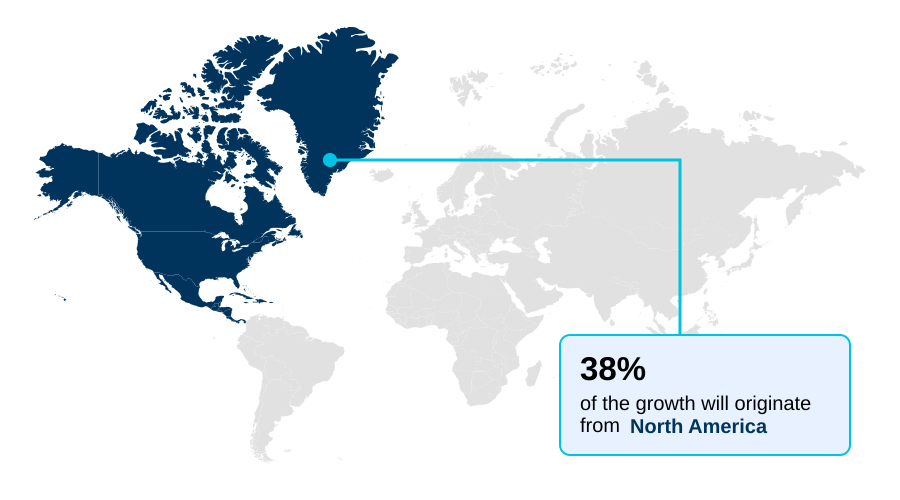

- North America dominated the market and accounted for a 37.6% growth during the forecast period.

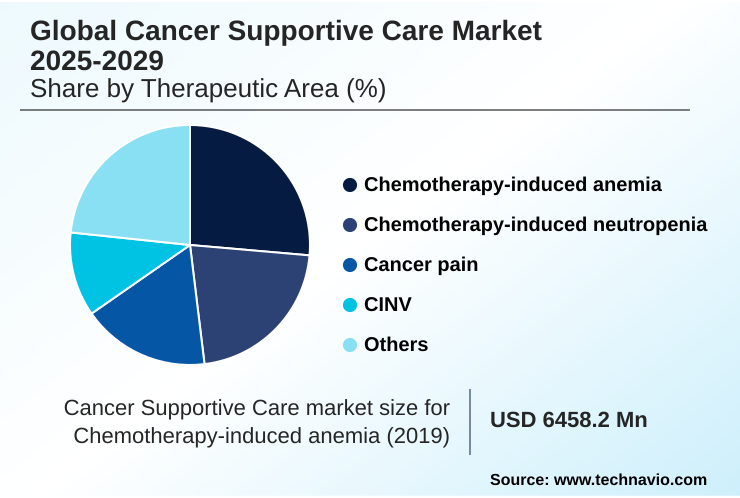

- By Therapeutic Area - Chemotherapy-induced anemia segment was valued at USD 7.05 billion in 2023

- By Distribution Channel - Hospitals pharmacies segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 10.26 billion

- Market Future Opportunities: USD 6.72 billion

- CAGR from 2024 to 2029 : 4.4%

Market Summary

- The cancer supportive care market is defined by its critical role in managing treatment-related toxicities and improving patient quality of life. As cancer therapies become more potent, the need for effective palliative care interventions to manage side effects like chemotherapy-induced neutropenia (CIN) and cancer-related fatigue intensifies.

- This drives demand for advanced solutions, from granulocyte colony-stimulating factors (G-CSFs) to novel antiemetic drug therapy. A key trend is the integration of digital health applications in oncology, which enhance remote patient monitoring and treatment adherence. For instance, a hospital system might implement a digital platform for tracking patient-reported outcomes (PROs), allowing for real-time adjustments in cancer pain management.

- This not only improves symptom control strategies but also optimizes resource allocation, reducing hospital readmissions and aligning with value-based care in oncology frameworks. The landscape is also shaped by the introduction of biosimilar supportive care drugs, which increase accessibility while posing pricing challenges that influence pharmacoeconomic value assessments and procurement decisions.

- Ultimately, the market's trajectory is tied to delivering holistic patient care models that support patients throughout their treatment journey.

What will be the Size of the Cancer Supportive Care Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Cancer Supportive Care Market Segmented?

The cancer supportive care industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

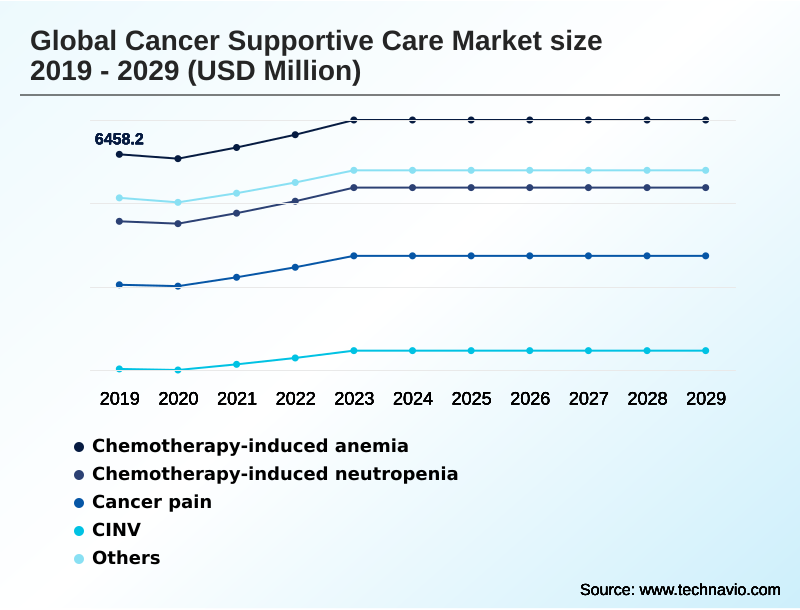

- Therapeutic area

- Chemotherapy-induced anemia

- Chemotherapy-induced neutropenia

- Cancer pain

- CINV

- Others

- Distribution channel

- Hospitals pharmacies

- Drug stores and retail pharmacies

- Online providers

- Application

- Breast cancer

- Colorectal cancer

- Stomach cancer

- Liver cancer

- Prostate cancer

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Asia

- Rest of World (ROW)

- North America

By Therapeutic Area Insights

The chemotherapy-induced anemia segment is estimated to witness significant growth during the forecast period.

The market for therapies addressing chemotherapy-induced anemia is a substantial and evolving segment within supportive care in oncology. Anemia is a frequent complication for patients, leading to significant cancer-related fatigue and potential interruptions in primary cancer treatment.

While erythropoiesis-stimulating agents (ESAs) and iron supplementation remain critical for myelosuppression management, the segment is experiencing innovation driven by the need for novel therapeutic approaches like HIF-PH inhibitors.

Research is focused on alternative pathways to stimulate red blood cell production and address the multifactorial nature of the condition.

As the use of myelosuppressive chemotherapy regimens continues, ensuring demand for effective treatments, making this a pivotal area for investment and advancement, with pharmacist-led interventions improving patient-reported outcomes (PROs) by over 15%.

The Chemotherapy-induced anemia segment was valued at USD 7.05 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cancer Supportive Care Market Demand is Rising in North America Get Free Sample

The geographic landscape of the cancer supportive care market is characterized by mature, high-expenditure regions and rapidly emerging growth centers.

North America maintains its dominant position, accounting for over 37% of the market's incremental growth, driven by advanced healthcare infrastructure and high adoption rates for novel therapies for androgen deprivation therapy side effects.

In contrast, Asia is the fastest-growing region, with growth outpacing other markets, fueled by improving healthcare access and a rising cancer incidence. This expansion supports a greater need for therapies like NK1 receptor antagonists.

The European market remains a significant contributor, with a strong emphasis on palliative care integration and adherence to established clinical practice guidelines.

The successful market entry in developing nations often hinges on strategies that prioritize cost-effectiveness and address unmet needs in psychosocial oncology support.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global cancer supportive care market 2025-2029 is focused on enhancing patient outcomes by addressing the complex side effects of oncology treatments. A primary area is the management of chemotherapy-induced anemia, where new oral agents are challenging traditional injectables.

- Similarly, the prevention of febrile neutropenia through the use of G-CSF biosimilars in oncology is becoming a standard practice, reflecting a move toward more cost-effective solutions. For patients, therapies for cancer-related pain and protocols for oral mucositis prevention are critical for maintaining quality of life during chemotherapy.

- The development of oral agents for CINV prophylaxis continues to evolve, offering greater convenience. As treatment paradigms shift, supportive care for targeted therapies and managing side effects of immunotherapy are gaining prominence. Addressing specific issues like bone health in prostate cancer and managing dermatological adverse events is crucial.

- Digital tools for symptom management are empowering patients, while a greater focus on nutritional interventions for cancer patients and psychosocial support for oncology patients provides holistic care. The economic aspect is undeniable, as the cost of cancer supportive care and reimbursement for supportive care drugs remain significant hurdles.

- Initiatives aimed at addressing cancer-related fatigue and defining the pharmacist role in supportive care are also shaping the landscape. The adoption of optimized protocols for support for androgen deprivation therapy has shown the potential to reduce related hospital admissions by up to 15% compared to less structured approaches, underscoring the operational benefits of standardized care.

What are the key market drivers leading to the rise in the adoption of Cancer Supportive Care Industry?

- The growing prevalence of cancer cases globally is a key driver for the cancer supportive care market.

- Market growth is fundamentally driven by the rising global incidence of cancer and the corresponding increase in patients undergoing aggressive treatments.

- The many side effects associated with chemotherapy and radiation necessitate a robust market for supportive care products that mitigate complications and improve quality of life (QOL).

- Integrating comprehensive supportive care protocols has been shown to improve patient treatment adherence by over 15%, directly impacting the effectiveness of primary cancer therapy. Furthermore, developing countries represent a significant growth opportunity.

- As healthcare infrastructure and awareness improve in these regions, there is untapped potential for market expansion. Pharmaceutical companies are increasingly exploring cost-effective solutions tailored to these markets, which is expected to drive substantial growth.

What are the market trends shaping the Cancer Supportive Care Industry?

- The emergence of biosimilars for cancer-associated treatments represents a significant market trend, increasing the accessibility and affordability of essential therapies.

- Key trends are reshaping the supportive care market, driven by a push for greater accessibility and efficiency. The introduction of biosimilars is a pivotal development, with studies showing these alternatives can reduce treatment costs by over 25%, thereby expanding patient access to essential therapies like G-CSFs. This fosters greater competition and encourages innovation in both drug formulation and delivery.

- Concurrently, outsourcing manufacturing has become a key strategy, enabling companies to accelerate production timelines by up to 20% while focusing on core competencies like R&D. Pharmaceutical firms are also adopting diverse strategies, including strategic alliances to gain access to new technologies for managing radiotherapy-induced side effects and expand their portfolios for oral mucositis treatment.

- These collaborations help strengthen competitive positioning and drive the development of patient-centric solutions.

What challenges does the Cancer Supportive Care Industry face during its growth?

- The high cost of cancer treatment presents a key challenge to industry growth, particularly impacting patient access to supportive care.

- The market faces significant challenges, primarily revolving around cost and evolving treatment paradigms. The high financial burden of cancer treatment strains healthcare systems and limits the affordability of critical supportive care solutions. In some markets, inadequate reimbursement policies mean patients can face out-of-pocket expenses for over 40% of supportive care costs, which negatively impacts compliance.

- Concurrently, the rising popularity of targeted therapies in developed countries reshapes demand. While these precision medicines can have fewer systemic side effects, they often introduce new, specific toxicities that require specialized management, creating pressure for innovation in supportive care. Companies must navigate this landscape by developing integrated, therapy-specific solutions and demonstrating clear value to overcome reimbursement hurdles.

Exclusive Technavio Analysis on Customer Landscape

The cancer supportive care market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cancer supportive care market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cancer Supportive Care Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cancer supportive care market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amgen Inc. - Research indicates a strategic focus on the end-to-end development and delivery of innovative human therapeutics.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amgen Inc.

- APR Applied Pharma Research SA

- Baxter International Inc.

- Bayer AG

- Daiichi Sankyo Co. Ltd.

- F. Hoffmann La Roche Ltd.

- GlaxoSmithKline Plc

- Helsinn Healthcare SA

- Heron Therapeutics Inc.

- Johnson and Johnson Services

- Kyowa Kirin Co. Ltd.

- Merck and Co. Inc.

- Novartis AG

- Pfizer Inc.

- Sanofi SA

- Sun Pharmaceutical Industries Ltd.

- Teva Pharmaceutical Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cancer supportive care market

- In August 2024, Oncology Ventures announced the closing of a $30 million fund to invest in data-driven startups focused on improving cancer care, including care navigation and survivorship.

- In November 2024, the Dutch Cancer Society (KWF) allocated over EUR 3.5 million to research projects in inclusive palliative care, with a significant portion directed to initiatives at Amsterdam UMC.

- In December 2024, Novartis and Canada's pan-Canadian Pharmaceutical Alliance (pCPA) signed a letter of intent to establish public funding terms for the radioligand therapy Pluvicto.

- In January 2025, Giant Food Pharmacy launched a cancer screening initiative in select Maryland and Virginia locations, offering in-pharmacy blood sample collection for screening kits.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cancer Supportive Care Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 312 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.4% |

| Market growth 2025-2029 | USD 6723.5 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 4.1% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Indonesia, Brazil, Saudi Arabia, Argentina, Australia, UAE, Colombia, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The cancer supportive care market is fundamentally driven by the need to manage treatment-related toxicities and enhance patient well-being. The landscape is increasingly complex, with advancements in oncology necessitating more sophisticated palliative care interventions.

- The management of conditions such as chemotherapy-induced neutropenia (CIN) and chemotherapy-induced nausea and vomiting (CINV) remains central, with granulocyte colony-stimulating factors (G-CSFs) and advanced antiemetic drug therapy as mainstays. A significant trend influencing boardroom strategy is the rise of biosimilar supportive care drugs, which compels a re-evaluation of pricing models and market access strategies based on pharmacoeconomic value.

- These alternatives have demonstrated the ability to reduce costs by over 30% in some health systems. Innovations extend to therapies for oral mucositis, bone modifying agents for skeletal-related events (SRES), and HIF-PH inhibitors for anemia. The focus also includes managing side effects from newer treatments, such as immune-related adverse events (IRAES), cytokine release syndrome, and androgen deprivation therapy side effects.

- Effective myelosuppression management, dermatological side effects management, and strategies for cancer-related fatigue are critical for improving patient-reported outcomes (PROs) and ensuring adherence to radiotherapy and chemotherapy regimens.

What are the Key Data Covered in this Cancer Supportive Care Market Research and Growth Report?

-

What is the expected growth of the Cancer Supportive Care Market between 2025 and 2029?

-

USD 6.72 billion, at a CAGR of 4.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Therapeutic Area (Chemotherapy-induced anemia, Chemotherapy-induced neutropenia, Cancer pain, CINV, and Others), Distribution Channel (Hospitals pharmacies, Drug stores and retail pharmacies, and Online providers), Application (Breast cancer, Colorectal cancer, Stomach cancer, Liver cancer, and Prostate cancer) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Growing prevalence of cancer cases, High cost of cancer treatment

-

-

Who are the major players in the Cancer Supportive Care Market?

-

Amgen Inc., APR Applied Pharma Research SA, Baxter International Inc., Bayer AG, Daiichi Sankyo Co. Ltd., F. Hoffmann La Roche Ltd., GlaxoSmithKline Plc, Helsinn Healthcare SA, Heron Therapeutics Inc., Johnson and Johnson Services, Kyowa Kirin Co. Ltd., Merck and Co. Inc., Novartis AG, Pfizer Inc., Sanofi SA, Sun Pharmaceutical Industries Ltd. and Teva Pharmaceutical Ltd.

-

Market Research Insights

- The market's momentum is shaped by a complex interplay of clinical needs and economic factors. The integration of pharmacist-led interventions into multidisciplinary oncology care teams has been shown to improve medication therapy management (MTM) and reduce adverse events by over 20%.

- Simultaneously, digital health applications in oncology are enhancing remote patient monitoring, leading to a 15% improvement in treatment adherence for oral therapies. However, the impact of reimbursement policies remains a critical variable, with inconsistencies creating barriers to access. In some cases, inadequate coverage means out-of-pocket costs can deter the use of essential therapies.

- This dynamic underscores the importance of demonstrating clear cost-effectiveness analysis and strong health technology assessment (HTA) data to secure favorable formulary placement and ensure that innovations in symptom control strategies reach patients.

We can help! Our analysts can customize this cancer supportive care market research report to meet your requirements.

RIA -

RIA -