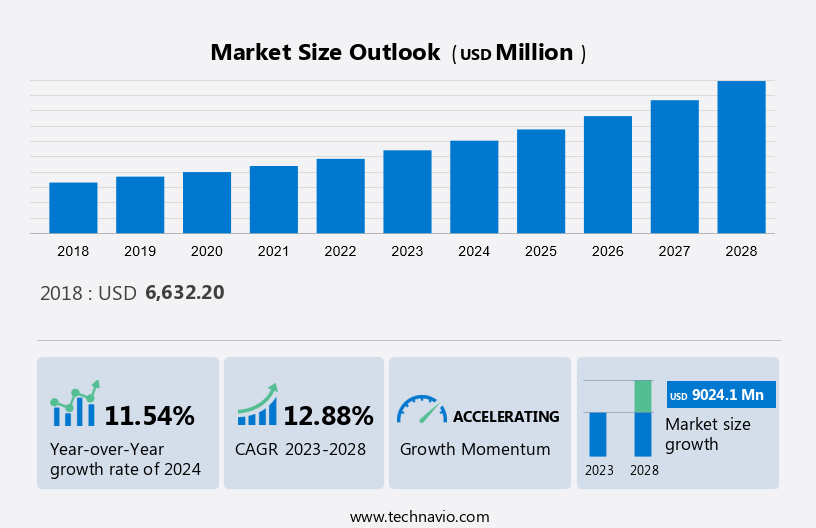

Cardiac Biomarker Market Size 2024-2028

The Global Cardiac Biomarkers Market size is estimated to grow by USD 9.02 billion at a CAGR of 12.88% between 2023 and 2028. The growth of the cardiac biomarkers market depends on several factors, including the increasing prevalence of CVDs, the growing geriatric population, and the rising number of M&A and new product launches. However, the market growth may be restrained due to market challenges such as the high cost of diagnostic products. However, market players are working on opportunities such as the use of digital health in rapid diagnostics for POC and technological advancement to cut down cost, which will boost the growth of the market. It also includes an in-depth analysis of drivers, trends, and challenges.

What will be the size of the Market During the Forecast Period?

To learn more about this report, Request Free Sample!

Market Dynamics and Customer Landscape

The market encompasses substances or molecules that are indicative of heart conditions, including chronic disorders and acute coronary syndromes such as heart attack and failure. The market is driven by the need for early detection of cardiovascular conditions and abnormality in cardiac functioning. Biomarkers such as enzymes and hormones play a crucial role in diagnosing critical cardiac conditions like Atherosclerosis. Healthcare providers rely on hospital laboratories and point-of-care testing facilities for accurate diagnostic results. The market is influenced by the growing elderly population, prompting increased focus on clinical research studies and epidemiological studies to identify new biomarkers. Access to biological samples from a diverse patient base is essential for developing effective diagnostic tools and treatments for cardiac diseases.

Key Market Drivers

The Increasing prevalence of CVDs is notably driving the market growth. The market has experienced significant growth due to the increasing prevalence of cardiovascular diseases, particularly in countries like the US. Approximately 6.5 million individuals aged 40 and above in the US are affected by Peripheral Arterial Disease (PAD), with equal prevalence among men and women. Factors contributing to this trend include low awareness, smoking, high prevalence of obesity, diabetes, high cholesterol, and high blood pressure.

In hospital laboratories, cardiac biomarkers such as myoglobin, natriuretic peptides, ischemia-modified albumin, and novel substances are used to identify myocardial infarction, microvascular dysfunction, and ischemia. These markers are essential for patient care on a patient-specific basis, enabling personalized medicine and improving the standard of care. Quality control, sensitivity, specificity, and regulatory issues are crucial considerations in the collection, detection, and storage of these biomarkers, which have storage limits and require specific conditions to maintain accuracy. Hence, these factors are expected to drive market growth during the forecast period.

Significant Market Trends

The increased focus on personalized medicine is the primary trend in the market. The market is expanding due to the rising prevalence of conditions such as high blood pressure, high cholesterol, obesity, and physical inactivity. These factors increase the risk of heart diseases, including myocardial infarction and ischemia. Hospital laboratories utilize various markers, such as C-reactive protein (CRP), myoglobin, natriuretic peptides, ischemia-modified albumin (IMA), and novel cardiac biomarkers, for diagnosing and monitoring heart conditions. These markers provide valuable information on an individual patient's profile, enabling personalized medicine and patient-specific treatment plans.

Further, protein detection, sensitivity, specificity, and quality control are essential aspects of cardiac biomarker testing. Regulatory issues and storage conditions, including sample collection and storage limits, also play a significant role in ensuring accurate and reliable results. Smoking and other substances or molecules can influence the levels of these biomarkers, making it crucial for the standard of care to consider these factors in patient care. Hence, these factors are expected to drive demand for cardiac biomarkers in the forecast period.

Major Market Challenges

The shortage of skilled clinicians is a major challenge impeding market growth. The global shortage of cardiologists, including various specialties, persists in both developed and underdeveloped countries. In the US, for instance, there was a deficit of around 4,500 cardiologists in 2021 to fill private practice and academic positions, with this number projected to reach approximately 6,000 by 2025. This shortage can be attributed to several factors, such as consolidation among healthcare organizations, new maintenance of certification requirements, funding cuts for Graduate Medical Education and research, and declining physician reimbursements. Meanwhile, the market continues to expand due to the increasing prevalence of conditions like high blood pressure, high cholesterol, obesity, physical inactivity, and smoking. These conditions can lead to complications such as myocardial infarction, ischemia modified albumin, myoglobin, natriuretic peptides, microvascular dysfunction, and other cardiac issues.

Further, hospital laboratories rely on these markers for patient care on a patient-specific basis, utilizing novel cardiac biomarkers for personalized medicine. Protein detection, sensitivity, and specificity are crucial for accurate diagnosis and quality control. Regulatory issues and sample collection procedures must also be addressed, along with storage conditions and storage limits to ensure the integrity of these substances or molecules. Hence, these factors may impede market growth due to the low adoption of these costly diagnostic products.

Key Market Customer Landscape

The market report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Market Customer Landscape

Who are the Major Market Companies?

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Abbott Laboratories - The company offers cardiac biomarker solutions such as BNP, CK-MB, Galectin 3, Myoglobin, and Troponin I.

The cardiac biomarker market report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

- Abbott Laboratories

- Advanced ImmunoChemical Inc.

- BG Medicine Inc.

- Bio Rad Laboratories Inc.

- bioMerieux SA

- Boditech Med Inc.

- Creative Diagnostics

- Danaher Corp.

- Diazyme Laboratories Inc.

- F. Hoffmann La Roche Ltd.

- Lepu Medical Technology Beijing Co. Ltd.

- LifeSign LLC

- LSI Medience Corp.

- Noavaran Payesh Aani Salamat. Co.

- Oy Medix Biochemica Ab

- Randox Laboratories Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Segmentation

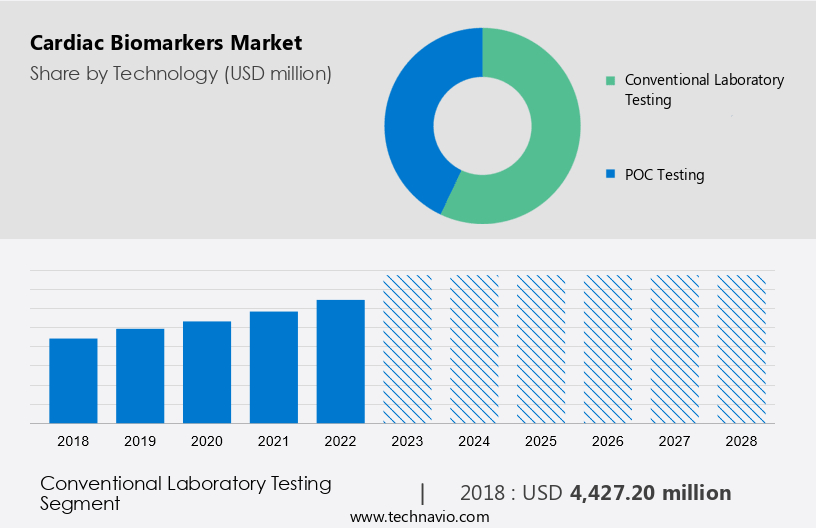

By Technology

The market share growth of the conventional laboratory testing segment will be significant during the forecast period. In conventional laboratory or lab-based testing, a clinician takes a sample of bodily fluids or tissues from the patient and then ensures its packaging and safe transport. These samples are then shipped to a central laboratory to be analyzed by a skilled laboratory professional. Depending on the complexity of the laboratory test, the results take approximately 1-2 days to be processed, and it is then sent back to the clinician. These test results are shared with patients in person, by phone, by email, or via a patient portal.

Get a glance at the market contribution of various segments Request a PDF Sample

The conventional laboratory testing segment was valued at USD 4.43 billion in 2018. The process of lab-based testing takes up to a week, right from when the patient provides the sample until the results are delivered; the long time taken is mainly attributed to the need for proper packaging and shipping, lab capacity, test processing, and data sharing. Such factors are major factors for the declining growth of the conventional laboratory testing segment in the market in focus during the forecast period.

By Region

For more insights on the market share of various regions Request PDF Sample now!

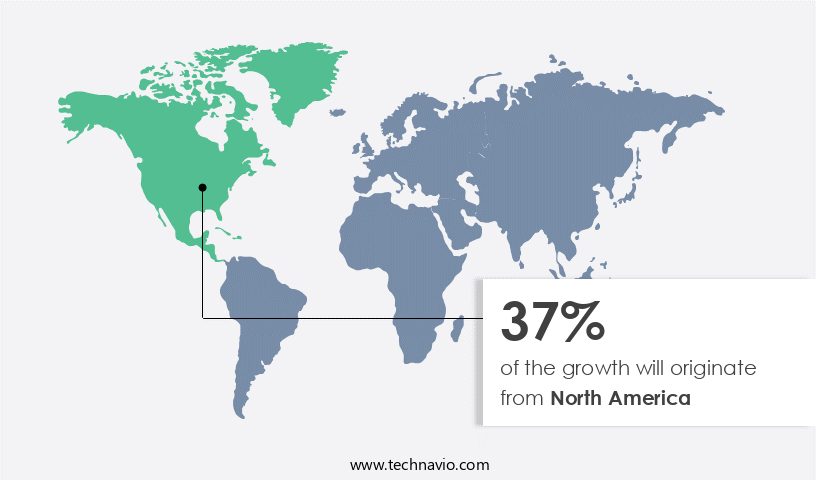

North America is estimated to contribute 37% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. The market in North America is experiencing significant growth due to the high prevalence of cardiovascular diseases (CVDs), particularly in the context of acute coronary syndrome and chronic heart conditions. Factors driving market expansion include increasing healthcare expenditure on cardiac conditions, the aging population, and rising diagnostic procedures. Cardiac biomarkers, such as Cardiac troponin, CK-MB, and CRP, are essential components of cardiovascular medicine for early detection and disease management. These biomarkers, found in blood, play a crucial role in cardiac diagnostics, particularly in the context of heart attacks and heart failure. Archived specimens and advanced technologies are also contributing to market growth. The field of cardiology is witnessing numerous clinical research efforts to improve cardiovascular diagnostics and reduce heart-related deaths. Healthcare systems and technologies are increasingly adopting cardiac test kits and diagnostic solutions to enhance disease management and improve patient outcomes.

Segment Overview

The market research report provides comprehensive data (region wise segment analysis), with forecasts and estimates in "USD Billion" for the period 2024 to 2028, as well as historical data from 2018 to 2022 for the following segments.

- Technology Outlook

- Conventional laboratory testing

- POC testing

- Product Outlook

- Troponin

- BNP and NT-proBNP

- CK-MB

- Myoglobin

- Others

- End-user Outlook

- Hospitals and clinics

- Diagnostic laboratories

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- The U.K.

- Germany

- France

- Rest of Europe

- Asia

- China

- India

- Rest of World (ROW)

- Brazil

- Argentina

- Rest of the Middle East & Africa

- North America

You may also interested in below market reports:

Market Analyst Overview

The market refers to the industry focused on the production, development, and distribution of various biomarkers used for the diagnosis and prognosis of cardiac diseases. These biomarkers include Cardiac Troponins (cTn), Brain Natriuretic Peptide (BNP), and Creatine Kinase-MB (CK-MB). Cardiac Troponins are proteins found in the heart that are released into the bloodstream when the heart muscle is damaged. BNP is a hormone produced by the heart in response to the stretching of the cardiac muscle fibers. CK-MB is an enzyme that is released into the bloodstream when there is damage to the heart or skeletal muscle. The use of these cardiac biomarkers in the diagnosis and treatment of cardiac diseases such as myocardial infarction, heart failure, and cardiomyopathy is increasing, driving the growth of the Cardiac Biomarkers market.

Additionally, the development of more sensitive and specific assays for these biomarkers is expected to further fuel market growth. (Cardiac Biomarkers, cTn, BNP, CK-MB, diagnosis, prognosis, heart disease, myocardial infarction, heart failure, cardiomyopathy, growth, sensitive, specific). The market is witnessing significant growth driven by the need for early diagnosis of cardiovascular disorders and Point of care testing facilities. With the emergence of the novel coronavirus, there's a heightened awareness of the high risks associated with conditions like congestive heart failure, myocarditis, and hypertension. Hospitals, especially in Spain, have reported a decline in the number of patients visiting emergency departments for cardiac issues. This trend has led to a reduction in admissions and a shift towards more lifestyle changes to manage cardiovascular health. The market is also seeing advancements in Point-of-Care Biomarker Tests, offering rapid and convenient diagnostics.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

185 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 12.88% |

|

Market growth 2024-2028 |

USD 9.02 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

11.54 |

|

Regional analysis |

North America, Europe, Asia, and Rest of World (ROW) |

|

Performing market contribution |

North America at 37% |

|

Key countries |

US, Germany, China, UK, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Abbott Laboratories, Advanced ImmunoChemical Inc., AgPlus Diagnostics Ltd., BG Medicine Inc., Bio Rad Laboratories Inc., bioMerieux SA, Boditech Med Inc., Creative Diagnostics, Danaher Corp., Diazyme Laboratories Inc., F. Hoffmann La Roche Ltd., Lepu Medical Technology Beijing Co. Ltd., LifeSign LLC, LSI Medience Corp., Noavaran Payesh Aani Salamat. Co., Oy Medix Biochemica Ab, Randox Laboratories Ltd., Response Biomedical Corp., Siemens Healthineers AG, Signosis Inc., and Tosoh Corp. |

|

Market dynamics |

Parent market analysis, Market forecast, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

Get access to Report Sample PDF !

What are the Key Data Covered in this Market Forecasting Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting of the market between 2023 and 2027

- Precise estimation of the size of the market size and its contribution to the parent market

- Accurate predictions about upcoming market trends and analysis and changes in consumer behavior

- Growth of the market industry across Europe, North America, APAC, South America, and Middle East and Africa

- Thorough market growth analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive market analysis and report on the factors that will challenge the market research and growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -