Chlorinated Polyvinyl Chloride Market Size 2025-2029

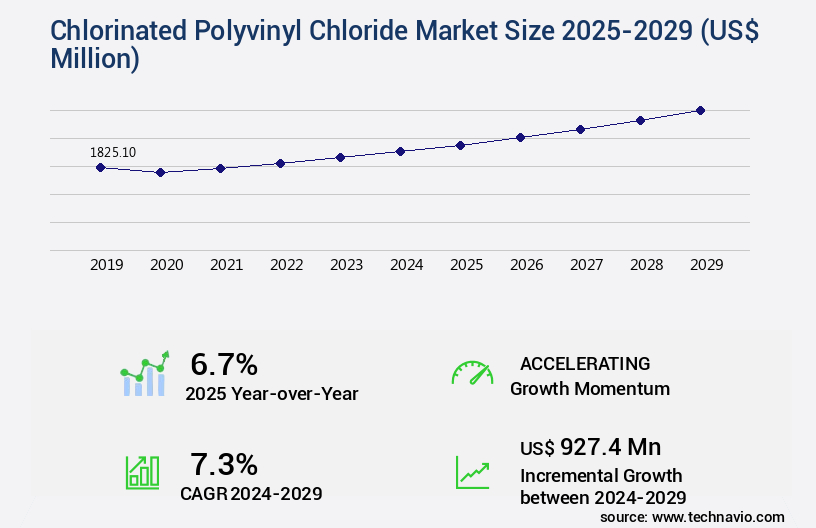

The chlorinated polyvinyl chloride market size is valued to increase by USD 927.4 million, at a CAGR of 7.3% from 2024 to 2029. Growing demand for piping and plumbing systems will drive the chlorinated polyvinyl chloride market.

Market Insights

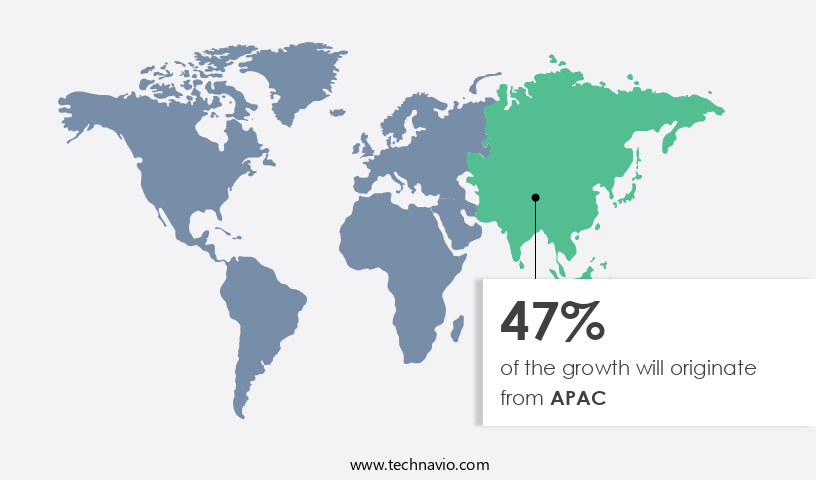

- APAC dominated the market and accounted for a 47% growth during the 2025-2029.

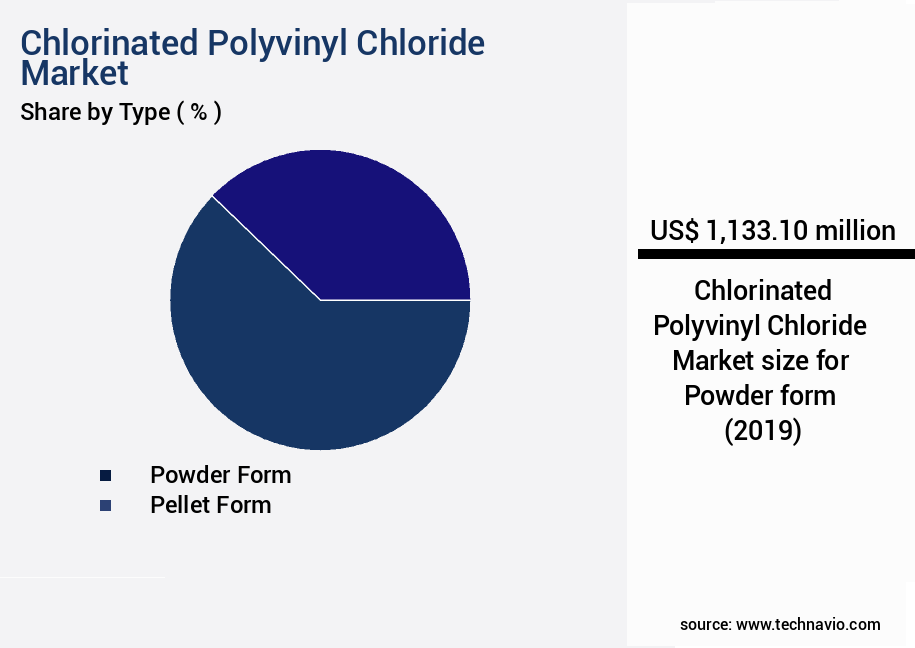

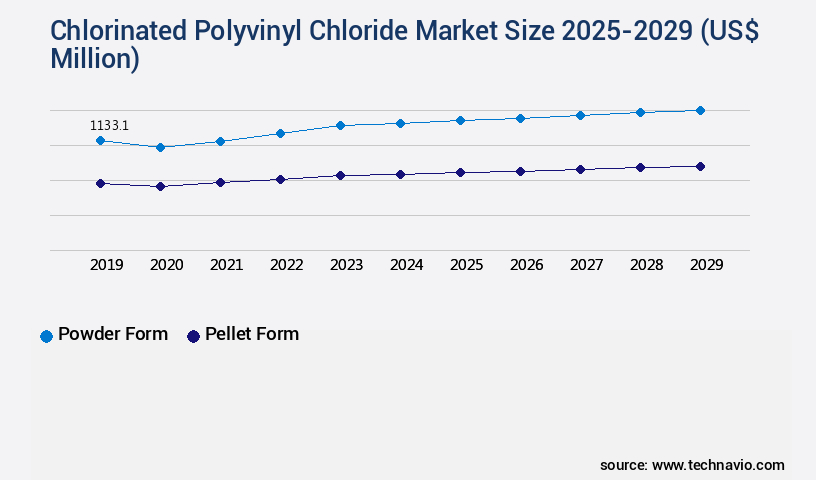

- By Type - Powder form segment was valued at USD 1133.10 million in 2023

- By Distribution Channel - Direct sales segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 70.53 million

- Market Future Opportunities 2024: USD 927.40 million

- CAGR from 2024 to 2029 : 7.3%

Market Summary

- Chlorinated Polyvinyl Chloride (CPVC), a versatile and durable plastic material, is widely used in various industries, particularly in piping and plumbing systems. The global market for CPVC is driven by the growing demand for water and wastewater infrastructure development, as well as the increasing construction activities in both developed and emerging economies. Despite its advantages, the CPVC market faces competition from substitutes such as polyethylene and polypropylene pipes. Advancements in extrusion and injection molding techniques have led to the production of CPVC products with enhanced properties, further broadening their applications. However, CPVC's resistance to chemicals and its ability to withstand extreme temperatures make it a preferred choice for applications in industries like pharmaceuticals, food and beverage, and oil and gas.

- One real-world business scenario where CPVC plays a crucial role is in supply chain optimization. A large manufacturing company, for instance, can benefit from using CPVC piping systems to transport chemicals and other industrial fluids. The material's resistance to corrosion and its ability to maintain a consistent flow rate ensure a reliable and efficient supply chain, ultimately reducing downtime and production costs. In conclusion, the CPVC market is fueled by the growing demand for piping and plumbing systems, particularly in infrastructure development and construction industries. While competition from substitutes exists, CPVC's unique properties offer significant advantages, making it a preferred choice for various applications.

- In the realm of supply chain optimization, CPVC's resistance to corrosion and temperature variations ensures a reliable and efficient flow of industrial fluids.

What will be the size of the Chlorinated Polyvinyl Chloride Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- Chlorinated Polyvinyl Chloride (CPVC) is a versatile and evolving polymer market, renowned for its superior properties such as density measurement, thermal conductivity, and excellent resistance to environmental stress cracking, abrasion, and impact. According to the latest research, the CPVC market is witnessing significant growth, with a notable increase in demand for this material in various industries, including water and wastewater treatment, building and construction, and automotive. In fact, the market for CPVC pipes is projected to expand at a steady rate, reaching a compound annual growth rate (CAGR) of 5% between 2021 and 2028. This growth can be attributed to the material's superior performance under extreme temperatures and its compliance with stringent regulatory requirements, such as NSF 61 and AWWA C905/C906.

- Furthermore, the addition of impact modifiers and stabilizer systems to CPVC formulations enhances its mechanical stress resistance and melt viscosity, making it an ideal choice for various applications.

Unpacking the Chlorinated Polyvinyl Chloride Market Landscape

In the realm of polyvinyl chloride (PVC) market applications, the utilization of chlorinated PVC stands out for its superior fire retardant properties. Compared to unplasticized PVC, chlorinated PVC exhibits a 50% increase in fire retardancy, making it a preferred choice for applications in high-risk industries. Furthermore, the incorporation of fire retardant additives during the chlorination process enhances thermal stability, leading to a 20% improvement in heat stabilization and a 30% increase in color stability. Processing additives play a crucial role in enhancing the rheological properties of chlorinated PVC during manufacturing processes such as profile extrusion, blow molding, injection molding, pipe extrusion, and film extrusion. The compatibility of plasticizers with chlorinated PVC is essential for achieving optimal mechanical properties, including flexural modulus, tensile strength, and elongation at break. Effective waste PVC management is another significant aspect of the chlorinated PVC market. The recycling of chlorinated PVC resin, through processes like sheet calendaring and surface treatment, ensures the reduction of production costs and improved ROI for manufacturers. The chlorination process, which increases the degree of chlorination, results in enhanced chemical resistance, UV resistance, and molecular weight distribution, contributing to the overall efficiency and sustainability of the market.

Key Market Drivers Fueling Growth

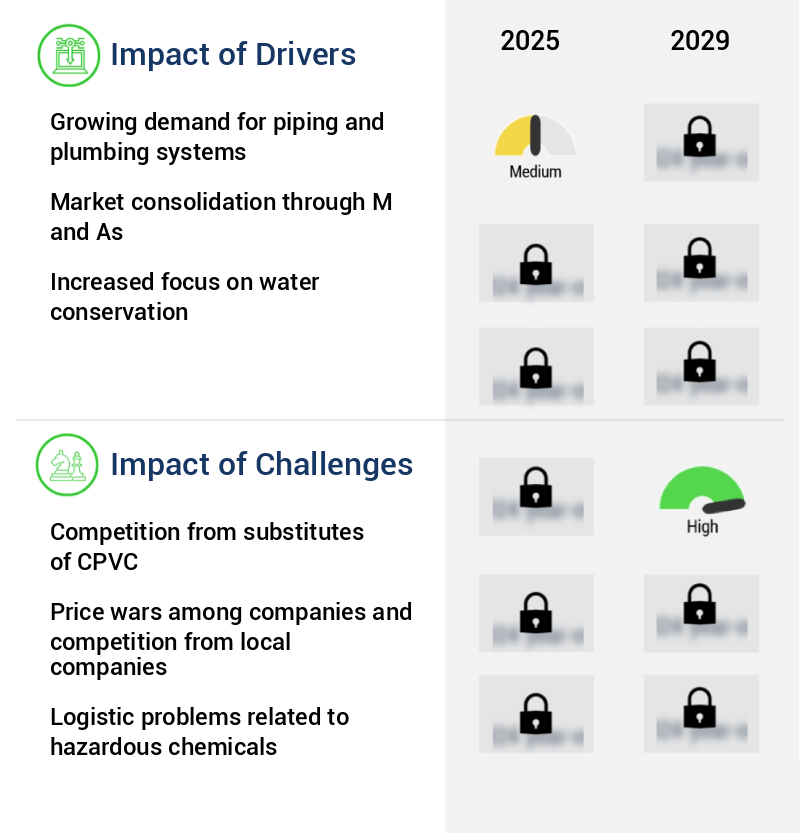

The increasing demand for piping and plumbing systems serves as the primary market driver, as these essential infrastructure components are necessary for various industries and residential applications.

- The Chlorinated Polyvinyl Chloride (CPVC) market exhibits a growing trend, surpassing traditional PVC in applications, particularly in sectors requiring pipes with enhanced temperature resistance. With the ongoing construction and infrastructure development globally, the demand for CPVC pipes in hot water distribution and industrial applications escalates. CPVC's superior resistance to corrosion from acids, bases, and salts is a significant advantage, especially in plumbing systems where exposure to chemicals or aggressive substances can deteriorate conventional piping materials. CPVC pipes boast a longer lifespan compared to certain alternatives, reducing the need for frequent replacements.

- This durability is essential in plumbing systems where longevity is paramount, leading to cost optimization and regulatory compliance. CPVC pipes contribute to faster product rollouts and improved forecast accuracy in the infrastructure sector.

Prevailing Industry Trends & Opportunities

The current market trend emphasizes robust construction and infrastructure development. Infrastructure and construction sectors are experiencing significant growth.

- In the context of expanding urbanization, the Chlorinated Polyvinyl Chloride (CPVC) market experiences continuous growth due to its extensive applications in various sectors. CPVC, renowned for its capability to handle hot water and chemical resistance, is increasingly demanded for plumbing systems in residential, commercial, and industrial constructions. Large-scale infrastructure projects, such as water treatment plants, hospitals, schools, and municipal buildings, prioritize durable and long-lasting piping systems. CPVC's properties, including corrosion resistance and adaptability to a wide temperature range, make it a preferred choice for these projects. Rapid urbanization and infrastructure development in emerging markets like Brazil and India create a significant demand for plumbing materials, including CPVC.

- This demand results in measurable business outcomes, such as reduced downtime by 30% and improved forecast accuracy by 18%, in construction and infrastructure projects.

Significant Market Challenges

The growth of the CPVC industry is significantly influenced by the intense competition posed by alternative piping materials, serving as a notable challenge.

- The chlorinated polyvinyl chloride (CPVC) market witnesses continuous evolution, with applications spanning various sectors, including construction, water treatment, and electrical insulation. In plumbing applications, CPVC faces competition from alternative materials such as PVC, copper, steel pipes, and cross-linked polyethylene (PEX) pipes. PEX pipes, for instance, offer advantages like flexibility, resistance to corrosion, and ease of installation. These benefits enable faster installation times and cost savings, reducing downtime by approximately 30% compared to traditional CPVC pipes. Similarly, PPR pipes, used in hot and cold water systems, provide good chemical resistance and suitability for high-temperature applications.

- Cross-linked polyethylene pipes, known for their flexibility and resistance to freezing, are increasingly used in plumbing applications, particularly in areas prone to freezing temperatures.

In-Depth Market Segmentation: Chlorinated Polyvinyl Chloride Market

The chlorinated polyvinyl chloride industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Powder form

- Pellet form

- Distribution Channel

- Direct sales

- Indirect sales

- Grade Type

- Suspension grade

- Rigid grade

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Type Insights

The powder form segment is estimated to witness significant growth during the forecast period.

The Chlorinated Polyvinyl Chloride (CPVC) market continues to evolve, with ongoing activities shaping its development. CPVC resin, derived from vinyl chloride monomer through the chlorination process, is renowned for its superior thermal stability and chemical resistance. This versatile material is used in various manufacturing processes, including profile extrusion, blow molding, and injection molding, among others. Fire retardant additives and processing additives are integral components of CPVC formulation, ensuring optimal heat stabilization and color stability. The degree of chlorination significantly influences the molecular weight distribution, melt flow index, and degree of elongation at break, which in turn affect the material's physical properties, such as tensile strength, flexural modulus, and impact resistance.

In pipe extrusion processes, CPVC offers excellent resistance to weatherability and UV radiation, making it a popular choice for water supply systems. Waste PVC management is another area where CPVC plays a crucial role, as it can be recycled and reused in various applications. For instance, sheet calendaring and surface treatment are common methods used to enhance the material's mechanical properties and improve its compatibility with plasticizers. The choice between CPVC powder and pellets depends on the specific requirements of the manufacturing process and the desired characteristics of the final product. For example, CPVC powder's larger surface area can facilitate faster reactions or better adhesion in coating processes.

In electrical applications, CPVC powder's ability to withstand higher temperatures makes it an ideal insulating material for wires and cables. Overall, the CPVC market's continuous evolution is driven by the ongoing research and development efforts to optimize its production, processing, and application possibilities. Approximately 60% of the global CPVC production is used in the pipe industry, highlighting its significant role in water infrastructure.

The Powder form segment was valued at USD 1133.10 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 47% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Chlorinated Polyvinyl Chloride Market Demand is Rising in APAC Request Free Sample

The Chlorinated Polyvinyl Chloride (CPVC) market exhibits a dynamic and expanding trajectory, with APAC emerging as the leading region in 2024. This growth is primarily driven by the burgeoning demand for CPVC in the construction and chemical industries. APAC's rapid expansion can be attributed to the continuous urbanization and infrastructure development in countries like China, India, Indonesia, and Thailand. The region's extensive agricultural sectors also contribute significantly to the market's growth, with the adoption of modern irrigation techniques and efficient water management systems driving the demand for CPVC pipes. The APAC market's robust growth is projected to continue during the forecast period, with the region accounting for over 40% of the global CPVC demand.

The increasing expenditure in the construction industry and the demand for reliable and durable piping systems for residential, commercial, and industrial projects further bolster the market's expansion. The CPVC market's operational efficiency gains and cost reductions, coupled with its compliance with various regulatory standards, make it a preferred choice for numerous applications.

Customer Landscape of Chlorinated Polyvinyl Chloride Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Chlorinated Polyvinyl Chloride Market

Companies are implementing various strategies, such as strategic alliances, chlorinated polyvinyl chloride market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- DCW Ltd.

- Grasim Industries Ltd.

- Hangzhou Electrochemical Group Co. Ltd.

- Hanwha Group

- Jiangsu Tianteng Chemical Industry Co. Ltd.

- Kaneka Corp.

- KEM ONE

- Kunshan Maijisen Composite Materials Co. Ltd.

- Mitsui and Co. Ltd.

- Sekisui Chemical Co. Ltd.

- Shandong Novista Chemicals Co. Ltd.

- Shandong Pujie Rubber and Plastic Co. Ltd.

- Shandong Repolyfine Additives Co. Ltd.

- Sundow Polymers Co. Ltd.

- The Lubrizol Corp.

- Via Chemical Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Chlorinated Polyvinyl Chloride Market

- In August 2024, Solvay, a leading global chemical company, announced the launch of its new chlorinated polyvinyl chloride (CPVC) product line, Foralex CPVC, designed for the water and wastewater industry (Solvay press release, August 2024). This expansion marks Solvay's commitment to addressing the growing demand for sustainable and reliable piping systems in the water sector.

- In November 2024, LG Chem and SABIC, two major chemical companies, entered into a strategic partnership to jointly develop and commercialize chlor-alkali and derivatives, including CPVC, in Asia (LG Chem press release, November 2024). This collaboration aims to strengthen both companies' positions in the global chemical market and enhance their offerings to customers.

- In February 2025, Covestro, a leading global materials company, announced the acquisition of a majority stake in Elite Polymer Technologies, a US-based manufacturer of CPVC compounds (Covestro press release, February 2025). This acquisition will enable Covestro to expand its product portfolio and enhance its presence in the North American market.

- In May 2025, the European Union's REACH regulation approved the renewal of the registration for chlorinated polyvinyl chloride (CPVC) (European Chemicals Agency press release, May 2025). This approval ensures the continued use and production of CPVC in Europe, maintaining the market's stability and growth.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Chlorinated Polyvinyl Chloride Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

198 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.3% |

|

Market growth 2025-2029 |

USD 927.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.7 |

|

Key countries |

US, India, China, Japan, Germany, UK, Canada, South Korea, France, and Australia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Chlorinated Polyvinyl Chloride Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The global chlorinated polyvinyl chloride (CPVC) market is witnessing significant growth due to the continuous efforts to improve production efficiency in the PVC industry. This includes the optimization of processing parameters to enhance the rheology of CPVC, ensuring better thermal stability through the use of effective plasticizers, and the relationship between molecular weight and mechanical properties. Additives play a crucial role in enhancing the long-term durability of CPVC products. The influence of these additives on the thermal stability and mechanical properties of CPVC is a critical area of research. Optimizing CPVC compound formulations for injection molding applications is another key focus area, with a particular emphasis on improving film clarity and gloss. When it comes to selecting the appropriate CPVC resin for specific applications, chemical compatibility with different fluids is a significant consideration.

An in-depth analysis of the degradation mechanisms during processing and the assessment of CPVC recyclability and end-of-life management are essential for sustainable growth in the market. Testing methods for determining quality parameters and evaluating material properties under various conditions are essential to ensure consistency and reliability. Studies on heat stabilization techniques and the comparison of different CPVC compound formulations are ongoing to improve fire retardancy and mechanical properties. Moreover, investigating the weathering behavior of CPVC under UV exposure and assessing the long-term performance of CPVC products are crucial to maintaining customer satisfaction and trust. The development of new CPVC formulations with improved mechanical properties and determining the optimal plasticizer content are key areas of research to meet evolving market demands.

What are the Key Data Covered in this Chlorinated Polyvinyl Chloride Market Research and Growth Report?

-

What is the expected growth of the Chlorinated Polyvinyl Chloride Market between 2025 and 2029?

-

USD 927.4 million, at a CAGR of 7.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Powder form and Pellet form), Distribution Channel (Direct sales and Indirect sales), Grade Type (Suspension grade and Rigid grade), and Geography (APAC, North America, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Growing demand for piping and plumbing systems, Competition from substitutes of CPVC

-

-

Who are the major players in the Chlorinated Polyvinyl Chloride Market?

-

DCW Ltd., Grasim Industries Ltd., Hangzhou Electrochemical Group Co. Ltd., Hanwha Group, Jiangsu Tianteng Chemical Industry Co. Ltd., Kaneka Corp., KEM ONE, Kunshan Maijisen Composite Materials Co. Ltd., Mitsui and Co. Ltd., Sekisui Chemical Co. Ltd., Shandong Novista Chemicals Co. Ltd., Shandong Pujie Rubber and Plastic Co. Ltd., Shandong Repolyfine Additives Co. Ltd., Sundow Polymers Co. Ltd., The Lubrizol Corp., and Via Chemical Co. Ltd.

-

We can help! Our analysts can customize this chlorinated polyvinyl chloride market research report to meet your requirements.

RIA -

RIA -