Clinical Chemistry Analyzers Market Size 2026-2030

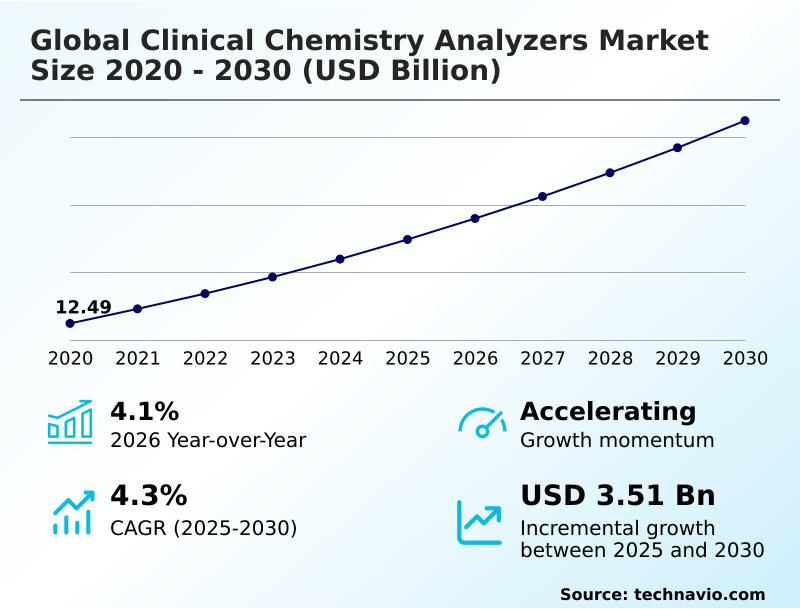

The clinical chemistry analyzers market size is valued to increase by USD 3.51 billion, at a CAGR of 4.3% from 2025 to 2030. Increasing global prevalence of chronic diseases and expanding geriatric population will drive the clinical chemistry analyzers market.

Major Market Trends & Insights

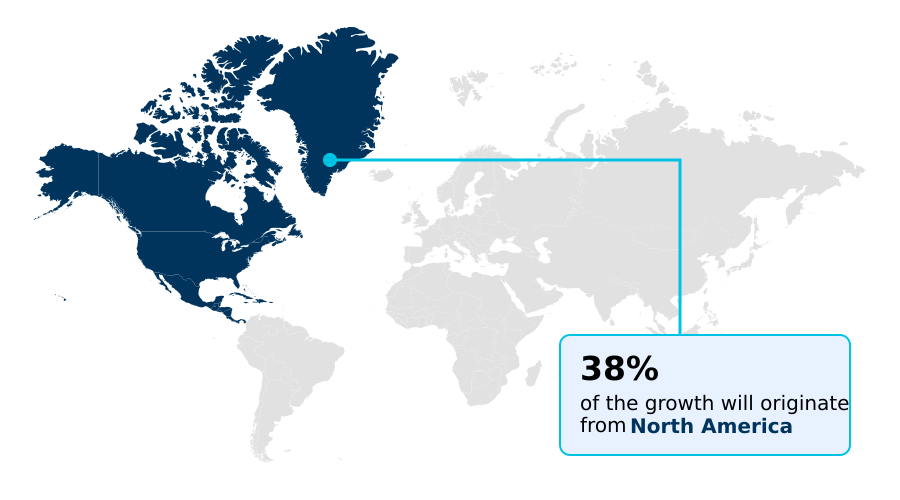

- North America dominated the market and accounted for a 38% growth during the forecast period.

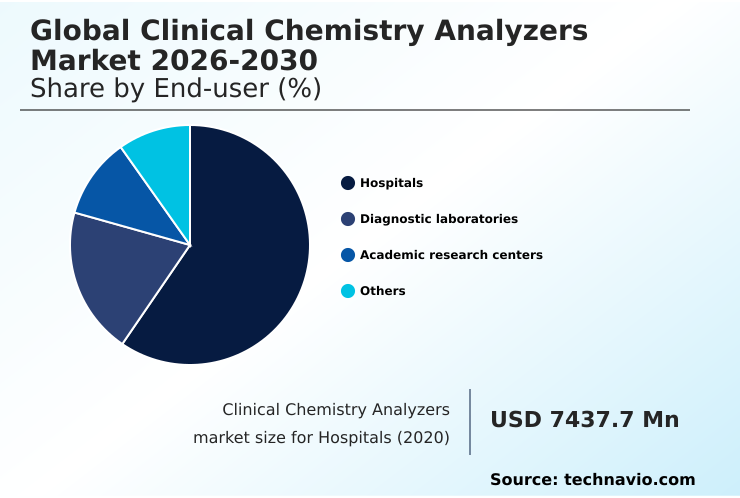

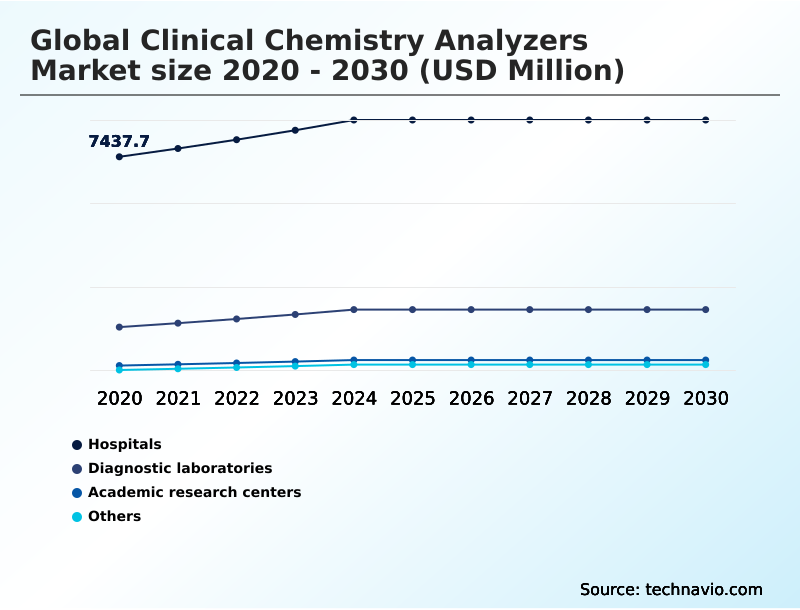

- By End-user - Hospitals segment was valued at USD 8.51 billion in 2024

- By Type - Fully automated clinical chemical analyzers segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 5.99 billion

- Market Future Opportunities: USD 3.51 billion

- CAGR from 2025 to 2030 : 4.3%

Market Summary

- The Clinical Chemistry Analyzers Market is foundational to modern healthcare, providing essential data for disease diagnosis and management. Growth is sustained by the rising global incidence of chronic conditions and an aging population, which together escalate the demand for routine biochemical monitoring.

- Technological innovation is a primary catalyst, with a clear industry shift towards total laboratory automation (TLA) and integrated systems combining clinical chemistry and immunoassay testing. These advancements address persistent challenges such as the critical shortage of skilled laboratory professionals and downward pressure on test reimbursement.

- For example, a large hospital network can implement a fully automated platform to consolidate testing from multiple departments, which reduces the cost-per-test and allows for the reallocation of staff to higher-value interpretive tasks. This drive for efficiency is balanced by the expansion of decentralized point-of-care testing (POCT), creating demand for compact, user-friendly devices in outpatient settings.

- The market's trajectory is defined by this dual focus: maximizing efficiency in centralized labs while expanding access to diagnostics at the point of need.

What will be the Size of the Clinical Chemistry Analyzers Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Clinical Chemistry Analyzers Market Segmented?

The clinical chemistry analyzers industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Hospitals

- Diagnostic laboratories

- Academic research centers

- Others

- Type

- Fully automated clinical chemical analyzers

- Semi automated clinical chemical analyzers

- Product type

- Reagents

- Analyzers

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By End-user Insights

The hospitals segment is estimated to witness significant growth during the forecast period.

Hospitals are the primary end-user segment, driven by the critical need for high-throughput diagnostic operations supporting emergency, intensive care, and surgical units.

These facilities predominantly invest in modular, integrated systems that perform both clinical chemistry and immunoassay testing, often connected to total laboratory automation tracks. The main requirements are uncompromising reliability and rapid turnaround times to manage immense daily sample volumes.

Purchasing decisions are complex, typically involving multi-year contracts that factor in the total cost of ownership, the breadth of the test menu, and system efficiency.

The adoption of these advanced platforms, which feature automated quality control and intelligent sample routing, has been shown to reduce analytical errors by more than 20%, directly enhancing patient safety and operational effectiveness in demanding 24/7 environments.

The Hospitals segment was valued at USD 8.51 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Clinical Chemistry Analyzers Market Demand is Rising in North America Request Free Sample

The geographic landscape of the market is defined by a dichotomy between mature and emerging regions.

North America represents the largest and most developed market, projected to contribute 38% of the incremental growth, driven by a focus on laboratory automation to counter workforce shortages and reimbursement pressures.

In this region, adoption of Total Laboratory Automation (TLA) systems can reduce pre-analytical errors by over 50%. Europe mirrors this maturity, with an emphasis on consolidating laboratory services and navigating the stringent IVDR regulatory framework.

In contrast, Asia is the fastest-growing region, fueled by significant healthcare infrastructure investment in countries like China and India.

This expansion creates substantial demand for a wide range of analyzers, from high-throughput systems in new urban hospitals to cost-effective benchtop models for developing rural healthcare networks, reflecting a global push for enhanced diagnostic access.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the clinical chemistry analyzers market increasingly revolves around optimizing laboratory architecture and assay portfolio management. The total laboratory automation vs standalone analyzers debate is central to this, with integrated networks showing a distinct advantage.

- Facilities that adopt immunoassay and clinical chemistry integration on a single platform report up to a 20% faster turnaround time compared to those using separate systems, a critical factor for acute care diagnostics.

- Furthermore, the role of point of care clinical chemistry systems is expanding beyond emergency use to chronic disease management in outpatient clinics, directly competing with traditional centralized lab testing models. The economic viability of these choices is often determined by the clinical chemistry analyzer reagent rental model, which minimizes upfront capital expenditure.

- Vendor selection now heavily weighs the clinical chemistry analyzer software integration capabilities and the breadth of the specialty clinical chemistry assays menu, as these factors directly impact workflow efficiency and profitability. This is particularly true for labs looking to bring esoteric testing in-house, where the availability of specific therapeutic drug monitoring on chemistry analyzers can be a key differentiator.

- The evaluation of clinical chemistry analyzer cost per test remains paramount, especially when comparing semi-automated vs fully automated systems for smaller labs. The clinical chemistry analyzer test menu expansion strategy is a core competitive lever, alongside the development of sustainable clinical chemistry consumables and adherence to evolving clinical chemistry analyzer regulatory standards.

- A comprehensive clinical chemistry analyzer maintenance contract is also crucial for ensuring uptime and long-term performance.

What are the key market drivers leading to the rise in the adoption of Clinical Chemistry Analyzers Industry?

- The increasing global prevalence of chronic diseases, coupled with an expanding geriatric population, is a key driver for the market.

- Market growth is propelled by a convergence of clinical needs and technological advancements. The rising prevalence of chronic diseases necessitates continuous monitoring, driving demand for routine clinical chemistry testing and specialized photometric analysis.

- Technological innovation serves as a powerful catalyst, with advancements in total laboratory automation (TLA) and integrated systems being paramount. These platforms, which can reduce sample processing time by up to 30%, address the critical global shortage of skilled laboratory professionals.

- Furthermore, the paradigm shift toward preventative healthcare and the decentralization of diagnostics are creating robust demand for point-of-care testing (POCT) solutions. These compact, cartridge-based reagent systems can shorten diagnostic turnaround from hours to under 15 minutes, enabling immediate clinical decision-making.

What are the market trends shaping the Clinical Chemistry Analyzers Industry?

- A growing emphasis on sustainability and eco-friendly laboratory solutions is emerging as a key trend. This shift influences purchasing decisions by incorporating criteria focused on reducing the environmental footprint of instruments and consumables.

- Key trends are reshaping the market, moving beyond analytical performance to address operational and strategic goals. The dominance of the reagent rental model is a primary commercial trend, allowing laboratories to adopt state-of-the-art automated immunoassay systems and chemistry analyzers with minimal upfront capital. This model enhances profitability for manufacturers by ensuring long-term consumable sales.

- Another pivotal trend is the expansion of assay menus to include high-value specialty tests, enabling laboratories to consolidate esoteric testing and improve their service offerings. This strategy can increase a lab's revenue per sample by over 15%.

- Additionally, a growing emphasis on sustainability is influencing instrument design, with new systems engineered to reduce reagent consumption and waste, which can lower operational costs by 5-10% annually.

What challenges does the Clinical Chemistry Analyzers Industry face during its growth?

- The high initial capital investment required for advanced systems and a stringent regulatory landscape represent a key challenge affecting industry growth.

- The market faces significant financial and operational headwinds that temper growth. The high capital investment for automated clinical chemistry systems and the stringent regulatory landscape, including CE-IVDR certification and 510(k) clearance, create substantial barriers to adoption, especially for smaller facilities.

- Compounding this is the persistent downward pressure on reimbursement, which has reduced revenue-per-test by an average of 8% in some high-volume assay categories, forcing laboratories to prioritize cost-per-test metrics above all else. A critical operational challenge is the severe shortage of skilled laboratory professionals, with some regions reporting staff vacancy rates as high as 20%.

- This deficit limits the ability of labs to fully leverage the capabilities of advanced instrumentation and manage increasing test volumes effectively.

Exclusive Technavio Analysis on Customer Landscape

The clinical chemistry analyzers market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the clinical chemistry analyzers market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Clinical Chemistry Analyzers Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, clinical chemistry analyzers market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - Offerings center on integrated diagnostic platforms and comprehensive assay menus designed to enhance laboratory workflow efficiency and support critical clinical decision-making.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Arkray USA Inc.

- Balio Diagnostics

- Bio Rad Laboratories Inc.

- Cardinal Health Inc.

- Chengdu Seamaty Co. Ltd.

- Danaher Corp.

- DiaSorin SpA

- Dirui Industrial Co. Ltd

- Erba Group

- F. Hoffmann La Roche Ltd.

- Hitachi Ltd.

- HORIBA Ltd.

- Meril Life Sciences Pvt. Ltd.

- Randox Laboratories Ltd.

- Shenzhen Mindray BioMedical

- Siemens AG

- Sysmex Corp.

- Thermo Fisher Scientific Inc.

- Werfenlife SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Clinical chemistry analyzers market

- In January 2025, QuidelOrtho announced it received 510(k) clearance from the US Food and Drug Administration for its Vitros Immunodiagnostic Products Fructosamine Reagent, enhancing chronic disease management capabilities on its integrated platforms.

- In October 2024, HORIBA Medical launched its Yumizen C100 CP, a compact clinical chemistry analyzer featuring a user-friendly interface and ready-to-use reagent cartridges specifically designed for point-of-care and smaller laboratory environments.

- In September 2024, Palantir Technologies expanded its partnership with the University of Colorado Anschutz Medical Campus to apply its Foundry platform for aggregating and analyzing large-scale data generated by clinical chemistry analyzers, aiming to improve research and operational insights.

- In March 2025, FUJIFILM Wako Diagnostics U.S.A. Corp. announced the commercial availability of its FDA-cleared beta-Hydroxybutyrate (BHB) assay for open clinical chemistry platforms, providing a critical tool for the rapid assessment of diabetic ketoacidosis.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Clinical Chemistry Analyzers Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 306 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.3% |

| Market growth 2026-2030 | USD 3506.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.1% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Thailand, Indonesia, Brazil, Saudi Arabia, South Africa, UAE, Turkey, Israel, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The clinical chemistry analyzers market is undergoing a significant operational and financial transformation. The foundational driver remains the high volume of routine testing, including metabolic panel testing and electrolyte analysis, fueled by an aging population. However, the competitive landscape is now shaped by advanced technological capabilities such as ion selective electrode technology and integrated immunoassay modules.

- A key strategic trend impacting boardroom-level budgeting is the shift away from capital purchases toward long-term operational agreements like the reagent rental model. This approach can reduce initial capital outlay by nearly 100%, converting a major capital expenditure into a predictable operational expense, which is highly attractive for budget-constrained healthcare systems.

- This model is sustained by the demand for proprietary consumables, including specialized calibrators and controls. Concurrently, innovation is focused on enhancing workflow through total laboratory automation (TLA) and the development of compact systems for point-of-care testing (POCT).

- The expansion of test menus to include high-value assays for therapeutic drug monitoring is another critical value driver, transforming analyzers into more versatile diagnostic hubs that improve laboratory workflow efficiency and clinical utility.

What are the Key Data Covered in this Clinical Chemistry Analyzers Market Research and Growth Report?

-

What is the expected growth of the Clinical Chemistry Analyzers Market between 2026 and 2030?

-

USD 3.51 billion, at a CAGR of 4.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Hospitals, Diagnostic laboratories, Academic research centers, and Others), Type (Fully automated clinical chemical analyzers, and Semi automated clinical chemical analyzers), Product Type (Reagents, Analyzers, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing global prevalence of chronic diseases and expanding geriatric population, High initial capital investment and stringent regulatory landscape

-

-

Who are the major players in the Clinical Chemistry Analyzers Market?

-

Abbott Laboratories, Arkray USA Inc., Balio Diagnostics, Bio Rad Laboratories Inc., Cardinal Health Inc., Chengdu Seamaty Co. Ltd., Danaher Corp., DiaSorin SpA, Dirui Industrial Co. Ltd, Erba Group, F. Hoffmann La Roche Ltd., Hitachi Ltd., HORIBA Ltd., Meril Life Sciences Pvt. Ltd., Randox Laboratories Ltd., Shenzhen Mindray BioMedical, Siemens AG, Sysmex Corp., Thermo Fisher Scientific Inc. and Werfenlife SA

-

Market Research Insights

- Market dynamics are shaped by the convergence of technological innovation and economic pressures. The adoption of integrated systems combining clinical chemistry and immunoassay testing has been shown to improve sample throughput by up to 25%, a critical gain for laboratories facing staff shortages.

- Simultaneously, the strategic shift toward reagent rental and managed service contracts helps healthcare facilities circumvent high initial capital costs, aligning with operational expenditure models. This business model is pivotal as laboratories grapple with reimbursement cuts that have reduced revenue-per-test by an average of 8% in certain high-volume assay categories.

- The decentralization of testing further influences the landscape, with point-of-care testing (POCT) platforms reducing diagnostic turnaround from hours to minutes, directly impacting clinical workflow and patient management in outpatient settings.

We can help! Our analysts can customize this clinical chemistry analyzers market research report to meet your requirements.