Cloud Storage Services Market Size 2026-2030

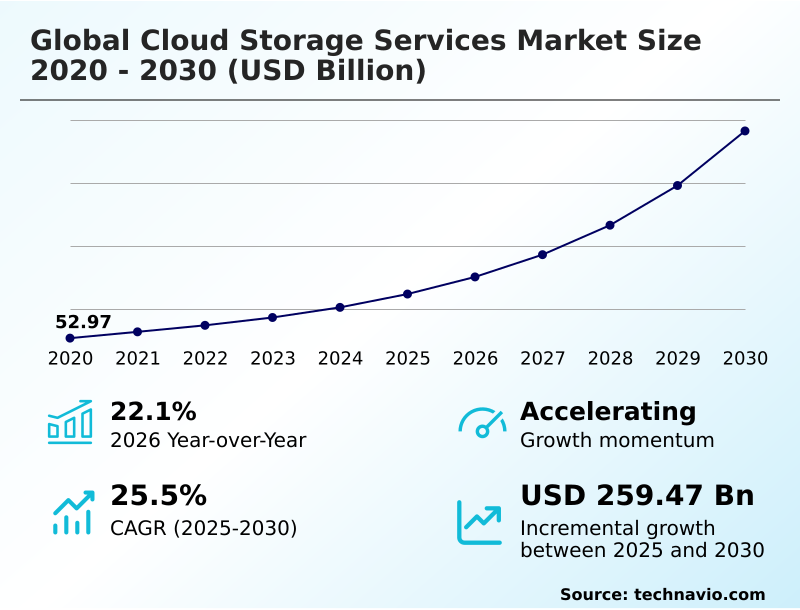

The cloud storage services market size is valued to increase by USD 259.47 billion, at a CAGR of 25.5% from 2025 to 2030. Proliferation of AI and ML workloads will drive the cloud storage services market.

Major Market Trends & Insights

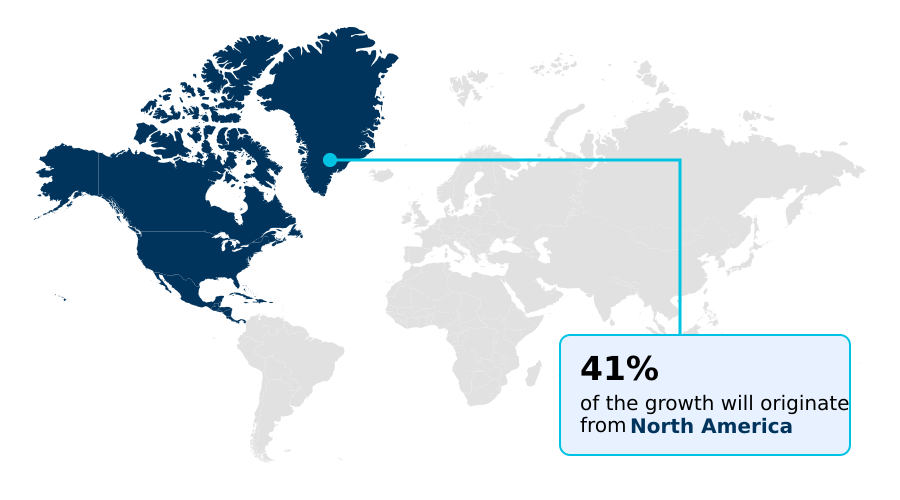

- North America dominated the market and accounted for a 41.1% growth during the forecast period.

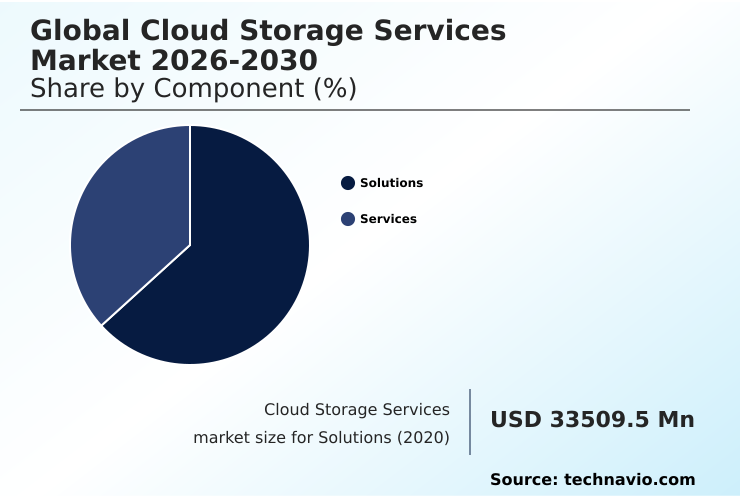

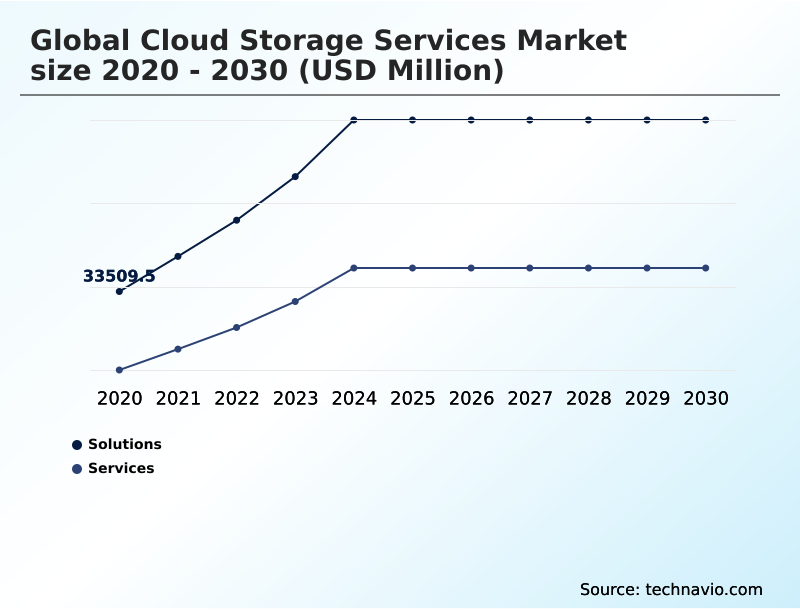

- By Component - Solutions segment was valued at USD 64.21 billion in 2024

- By Type - Public segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 329.63 billion

- Market Future Opportunities: USD 259.47 billion

- CAGR from 2025 to 2030 : 25.5%

Market Summary

- The cloud storage services market forms the foundational backbone of the modern digital economy, evolving far beyond simple data preservation. Growth is propelled by the transition toward data-driven decision-making, where organizations require high-performance repositories for AI and machine learning applications. This has shifted focus from passive archival to active data lakes supporting high-velocity processing.

- Consequently, hybrid and multi-cloud architectures are becoming standard, allowing enterprises to optimize costs and avoid vendor lock-in. For instance, a global manufacturing firm might use a private cloud for sensitive intellectual property and operational data while leveraging a public cloud’s elastic compute power for supply chain analytics and predictive maintenance modeling. This strategic data placement balances security with agility.

- However, this complex environment introduces challenges related to navigating divergent global data sovereignty mandates and mitigating sophisticated cybersecurity threats, demanding robust governance and zero-trust security frameworks to ensure data integrity and compliance across jurisdictions.

What will be the Size of the Cloud Storage Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Cloud Storage Services Market Segmented?

The cloud storage services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Solutions

- Services

- Type

- Public

- Private

- Hybrid

- End-user

- IT and telecom

- BFSI

- Government and public sector

- Healthcare

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Component Insights

The solutions segment is estimated to witness significant growth during the forecast period.

The solutions sub-segment is central to the market, providing the architectural frameworks for storing and securing digital information. This includes primary storage for active workloads, as well as essential backup and disaster recovery solutions.

Demand for object storage is expanding due to the growth of unstructured data from IoT devices and multimedia content. This technology manages data via metadata, offering superior scalability.

Innovations like autonomous tiering, which uses machine learning for intelligent data placement, are becoming critical. This approach enhances operational efficiency, as evidenced by a 40% reduction in data retrieval latency for some international research enterprises using AI-optimized tiers.

Furthermore, container-native storage supports modern application development, making the solutions segment the core of the cloud ecosystem's efficiency.

The Solutions segment was valued at USD 64.21 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cloud Storage Services Market Demand is Rising in North America Get Free Sample

The geographic distribution of the cloud storage services market is characterized by a mature North American sector and a rapidly accelerating APAC region.

While North America holds a substantial market share, driven by its extensive hyperscale infrastructure, the APAC region is projected to have the fastest growth, with a CAGR of 28.4%, fueled by widespread digitalization and mobile-first economies.

Data sovereignty and residency regulations significantly influence regional strategies, particularly in Europe, where compliance with GDPR is paramount. This has driven demand for localized data centers and sovereign cloud solutions.

In contrast, emerging markets in South America and the Middle East and Africa are increasingly adopting cloud-native approaches, often bypassing legacy on-premises systems.

This diverse global landscape necessitates flexible, geo-specific strategies from service providers to address varying regulatory, economic, and technological conditions.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Enterprises are increasingly adopting a multi-faceted approach to their data strategies to balance performance, cost, and compliance. The need for cost-effective archival storage solutions for retaining vast amounts of historical data is a primary consideration, often forming the foundational layer of an organization's storage architecture.

- However, the real challenge lies in managing unstructured data at scale, which now constitutes the bulk of enterprise information. This has spurred the adoption of AI-powered data classification and tiering, allowing for automated and intelligent data placement. As businesses harness analytics and machine learning, the demand for high-throughput object storage for analytics becomes critical, enabling rapid insights from massive datasets.

- To secure these distributed environments, implementing zero-trust security for cloud data is non-negotiable. This strategy is complemented by hybrid cloud storage orchestration tools that provide a unified management plane across on-premises and public cloud resources. Furthermore, reducing data retrieval latency for AI is essential for real-time applications and model training.

- Central to this entire ecosystem is a strict adherence to data sovereignty and residency compliance, which dictates architectural choices and deployment models. Organizations that successfully integrate these elements can achieve a storage cost reduction of over 30% compared to traditional, unmanaged approaches, directly impacting IT budget efficiency and overall business agility.

What are the key market drivers leading to the rise in the adoption of Cloud Storage Services Industry?

- The proliferation of AI and machine learning workloads serves as a key driver for the market's growth.

- The market is primarily driven by the exponential growth of AI and machine learning workloads, which demand massive, high-performance storage repositories.

- The transition toward generative AI has fundamentally altered infrastructure requirements, favoring active data lakes that support high-velocity processing over traditional archival systems.

- In response, providers have introduced specialized AI-optimized object storage tiers that can reduce data retrieval latency by as much as 40%. A second major driver is the escalating complexity of global data security and regulatory compliance.

- Stringent mandates like GDPR necessitate solutions with granular access controls and localized data hosting.

- This regulatory pressure is accelerating the migration from legacy on-premises systems to more secure and compliant cloud environments that feature zero-trust architectures and immutable storage to protect against ransomware and unauthorized access.

What are the market trends shaping the Cloud Storage Services Industry?

- The integration of generative AI is fundamentally reshaping cloud infrastructure, leading to the emergence of autonomous storage management as a defining market trend.

- Key market trends are converging around intelligence and distribution. The integration of generative AI is transforming passive repositories into active, intelligent data platforms, with autonomous storage management systems using machine learning to optimize data placement and automate lifecycle tasks. This shift toward AI-native infrastructure has led to the direct embedding of vector database capabilities into object storage services.

- Concurrently, a move from centralized data centers to distributed edge storage and decentralized architectures is underway, driven by the need to reduce latency for real-time applications. The expansion of 5G networks and IoT devices accelerates this trend, making localized data processing a critical component of modern strategies.

- In some deployments, edge storage has been shown to reduce application latency by up to 70%, enhancing user experience and enabling new use cases in industrial automation and smart city infrastructure.

What challenges does the Cloud Storage Services Industry face during its growth?

- The persistent complexity of data egress fees and the challenge of company lock-in present significant hurdles to industry growth.

- Primary market challenges stem from financial friction and security vulnerabilities. Data egress fees and vendor lock-in remain significant barriers, creating unpredictable costs and limiting multi-cloud strategies; this issue is a primary concern for 94% of IT leaders. The complexity and expense of moving data between platforms often force organizations to remain with suboptimal providers.

- Simultaneously, the threat landscape is escalating, with a documented 154% year-over-year surge in cloud security incidents, many resulting from customer-side misconfigurations and mismanaged credentials. The fragmentation of global data regulations further complicates operations, forcing organizations to deploy duplicate infrastructure to meet disparate data residency laws, thereby increasing costs and reducing the inherent scalability benefits of the cloud.

Exclusive Technavio Analysis on Customer Landscape

The cloud storage services market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cloud storage services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cloud Storage Services Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cloud storage services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Akamai Technologies Inc. - The company offers cloud storage services such as object storage and edge-based storage through its cloud infrastructure platform.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Akamai Technologies Inc.

- Alibaba Cloud

- Amazon Web Services Inc.

- Apple Inc.

- Box Inc.

- DigitalOcean Holdings Inc.

- Dropbox Inc.

- Google LLC

- IBM Corp.

- Microsoft Corp.

- NetApp Inc.

- Oracle Corp.

- OVH Groupe SA

- pCloud International AG

- Proton AG

- Pure Storage Inc.

- Rackspace Technology Inc.

- Tencent Holdings Ltd.

- Tresorit AG

- Wasabi Holding Co. Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cloud storage services market

- In October 2024, Microsoft Corp. announced significant enhancements to its OneDrive consumer and enterprise cloud storage service, introducing a redesigned, photos-first mobile interface with enhanced editing capabilities and a new natural language search feature powered by Copilot AI.

- In November 2024, Box Inc. announced at its annual BoxWorks customer conference a comprehensive set of AI-powered innovations centered on transforming how enterprise organizations manage unstructured data, including the introduction of Box AI Studio, Box Apps, and a new Enterprise Advanced subscription plan.

- In February 2025, Wasabi Holding Co. Inc. published its 2025 Global Cloud Storage Index, a survey of 1,600 IT decision-makers across organizations with more than 100 employees globally.

- In April 2025, Box Inc. announced at Google Cloud Next 2025 a deepened partnership with Google Cloud, enabling AI-powered metadata extraction for enterprise content stored in Box by leveraging Google's Gemini 2.0 Flash model.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cloud Storage Services Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 312 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 25.5% |

| Market growth 2026-2030 | USD 259472.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 22.1% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is undergoing a significant architectural transformation, driven by the dual pressures of AI integration and complex data sovereignty requirements. The traditional model of passive, archival storage is being supplanted by active, intelligent data repositories designed for high-velocity processing and autonomous management.

- This shift necessitates a move toward AI-native storage architectures that embed capabilities like vector databases and automated data tiering directly into the infrastructure. Boardroom decisions now center on whether to invest in these advanced, purpose-built systems or attempt to retrofit legacy environments, a choice with long-term strategic implications.

- Implementing AI-optimized storage has demonstrated tangible performance gains, with some configurations reducing data model training times by over 30%. This evolution demands a sophisticated approach to hybrid and multi-cloud orchestration, where data mobility, security, and compliance are managed seamlessly across a distributed and increasingly complex digital estate, challenging enterprises to rethink their core data strategies.

What are the Key Data Covered in this Cloud Storage Services Market Research and Growth Report?

-

What is the expected growth of the Cloud Storage Services Market between 2026 and 2030?

-

USD 259.47 billion, at a CAGR of 25.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Solutions, and Services), Type (Public, Private, and Hybrid), End-user (IT and telecom, BFSI, Government and public sector, Healthcare, and Others) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Proliferation of AI and ML workloads, Persistent complexity of data egress fees and company lock-in

-

-

Who are the major players in the Cloud Storage Services Market?

-

Akamai Technologies Inc., Alibaba Cloud, Amazon Web Services Inc., Apple Inc., Box Inc., DigitalOcean Holdings Inc., Dropbox Inc., Google LLC, IBM Corp., Microsoft Corp., NetApp Inc., Oracle Corp., OVH Groupe SA, pCloud International AG, Proton AG, Pure Storage Inc., Rackspace Technology Inc., Tencent Holdings Ltd., Tresorit AG and Wasabi Holding Co. Inc.

-

Market Research Insights

- The market's dynamics are shaped by a strategic pivot toward architectures that enhance operational resilience and cost efficiency. The widespread adoption of multi-cloud data mobility allows enterprises to mitigate the risks of vendor dependency, a significant concern for 94% of IT leaders who cite company lock-in as a primary operational anxiety.

- This shift is supported by robust data governance frameworks that ensure compliance across various platforms. As organizations adopt AI-native workflows, the emphasis on high-performance object storage grows, with implementations demonstrating up to 40% reductions in data retrieval latency.

- These advancements in cloud data lifecycle management are critical for optimizing both performance and expenditure, enabling businesses to align their storage strategies with evolving technological and economic demands.

We can help! Our analysts can customize this cloud storage services market research report to meet your requirements.

RIA -

RIA -