Enjoy complimentary customisation on priority with our Enterprise License!

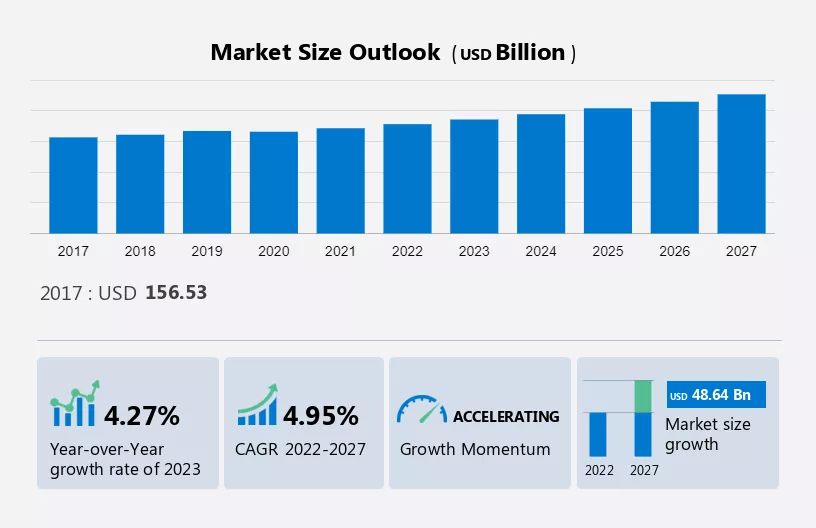

The Condiments Market is projected to increase by USD 48.64 billion from 2022 to 2027. The market is estimated to grow at a CAGR of 4.95% between 2022 and 2027.

This report extensively covers market segmentation by product (table sauces, cooking ingredients, mustard, and others), distribution channel (offline and online), and geography (APAC, Europe, North America, Middle East and Africa, and South America). It also includes an in-depth analysis of drivers, trends, and challenges. Furthermore, the report includes historic market data from 2017 to 2021.

The growth of the global condiments market is being invigorated by the frequent number of product launches in categories such as sauces, pickles, dressings, and mustard. Vendors operating in the global condiments market focus on innovation in terms of flavors and ingredients. The recent product launches in the global condiments market include the following.

To get additional information about the market, Buy Report

Our researchers analyzed the data with 2022 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers, trends, and challenges will help stakeholders in the value chain refine their marketing strategies to gain a competitive advantage.

Trends

Retail stores and online shops have been creating their own food and beverage products, including condiments. Major vendors such as Amazon, El Corte, Shufersal, and Sainsbury's offer private-label condiments, giving consumers more options. In Japan, the availability of private-label options has increased the consumption of cooking and table sauces among nearly two-thirds of consumers. Private-label condiments have been launched by many retailers, such as Amazon's Solimo salsa and Happy Belly mustard product lines. The growth of private-label condiments is expected to boost the global condiments market during the forecast period.

Challenge

The global condiments market faces distribution challenges, posing serious difficulties for vendors. Retailers are expected to come up with innovative merchandising solutions, like movable shelves, to minimize replenishment costs. To reduce warehousing expenses, there is a growing preference for more frequent, smaller product deliveries. Retail stores operate at lower profit margins, putting manufacturers under price and margin pressure. Changing consumer preferences towards convenience stores has prompted vendors to balance volume and price while developing new category management skills.

Customer Landscape

The report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their growth strategies.

Global Condiments Market Customer Landscape

Vendors are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The report also includes detailed analyses of the competitive landscape of the market and information about 15 market vendors, including:

Qualitative and quantitative analysis of vendors has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize vendors as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize vendors as dominant, leading, strong, tentative, and weak.

The table sauces segment was valued at USD 55.12 billion in 2017 and continued to grow until 2021. The sub-categories barbecue sauces and hot sauces have been the major variants of table sauces, which have witnessed significant growth in many countries. Currently, salad dressings are the most common type of dressings available in the market, which include mayonnaise, ranch dressing, Italian dressing, coconut cream dressing, zesty lemon dressing, agrodolce dressing, and balsamic vinaigrette dressing. The growth of dressings-based table sauces in the market is further invigorated by frequent product launches.

For a detailed summary of the market segments BUY REPORT

The change in shopping preferences propels the sales of condiments through the online channel, which is expected to grow at a rapid pace during the forecast period. Presently, most consumers make their purchase decisions based on online research on websites, blogs, and social media. This shift is mostly led by the penetration and geographical reach of e-retailers. Some of the key e-retailers offering condiments are Amazon, Rakuten Inc., Alibaba Group Holding Ltd., and JD.com Inc. Retailers such as Walmart, Costco, and Sears, which sell canned food, have also introduced their e-commerce portals. As per The World Bank Group, internet penetration in the US reached 92% in 2022 from 87% in 2020. This helped a large section of consumers gain access to online retail platforms. Internet penetration and smartphone use enable consumers to shop online. They also allow manufacturers to expand their distribution networks by partnering with third-party e-retailers and raising their sales and expanding their geographical presence.

For further insights about regional markets,Request PDF Sample now!

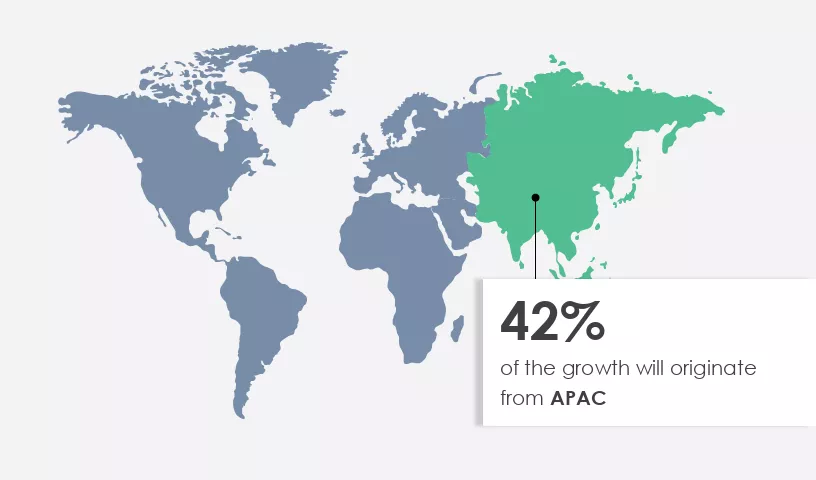

APAC is estimated to contribute 42% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The condiments market in APAC is highly fragmented due to the presence of many regional and global vendors. Kraft Heinz, NutriAsia Inc. (NutriAsia), Three Threes Condiments Pty Ltd. (Three Condiments), Nestle, Kewpie, and Unilever are among the major players operating in the market in APAC. Japan, China, India, Vietnam, Australia, Indonesia, the Philippines, South Korea, Singapore, Bangladesh, Pakistan, and Taiwan are the major markets with considerable demand for condiments in APAC. Moreover, the rapid emergence of the catering industry in China has been supporting the adoption of condiments in China as food items served through catering channels use considerable amounts of condiments.

The rising outbreak of respiratory and infectious diseases in the region was expected to further increase the growth of the market in the region. However, in condiments for retail, food, and beverage, restaurant vendors focused on establishing a supply system to meet the strong demand as part of their recovery strategy. This, in turn, will drive the growth of the global condiments market during the forecast period.

This report forecasts the contribution of all the segments to the growth of the market. In addition, we have included the COVID-19 impact and the recovery strategies for each segment. In 2021, owing to the mass vaccination drive and other government initiatives resulted in the removal of the lockdown and the resumption of business operations in the condiments market. In condiments for retail, foods and beverage, and restaurants establishing a supply system to meet the strong demand as part of their recovery strategy. This, in turn, will drive the growth of the global condiments market during the forecast period.

The report forecasts market growth by revenue at global, regional & country levels and provides an analysis of the latest trends and growth opportunities from 2017 to 2027.

|

Condiments Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

172 |

|

Base year |

2022 |

|

Historic period |

2017-2021 |

|

Forecast period |

2023-2027 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.95% |

|

Market growth 2023-2027 |

USD 48.64 billion |

|

Market structure |

USD Fragmented |

|

YoY growth 2022-2023(%) |

4.27 |

|

Regional analysis |

APAC, Europe, North America, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 42% |

|

Key countries |

US, China, Japan, India, and Germany |

|

Competitive landscape |

Leading Vendors, Market Positioning of Vendors, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

ADF Foods Ltd., Ajinomoto Co. Inc., Conagra Brands Inc., Cremica Food Industries Ltd., Dabur India Ltd., Dr. August Oetker KG, General Mills Inc., Halcyon Proteins Pty. Ltd., Hormel Foods Corp., Kerry Group Plc, Kewpie Corp., McCormick and Co. Inc., Midas Foods International, Nestle SA, NutriAsia Inc., Patanjali Ayurved Ltd., PepsiCo Inc., The Kraft Heinz Co., Three Threes Condiments Pty Ltd., and Unilever PLC |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

We can help! Our analysts can customize this report to meet your requirements. Get in touch

1 Executive Summary

2 Market Landscape

3 Market Sizing

4 Historic Market Size

5 Five Forces Analysis

6 Market Segmentation by Product

7 Market Segmentation by Distribution Channel

8 Customer Landscape

9 Geographic Landscape

10 Drivers, Challenges, and Trends

11 Vendor Landscape

12 Vendor Analysis

13 Appendix

Get lifetime access to our

Technavio Insights

Cookie Policy

The Site uses cookies to record users' preferences in relation to the functionality of accessibility. We, our Affiliates, and our Vendors may store and access cookies on a device, and process personal data including unique identifiers sent by a device, to personalise content, tailor, and report on advertising and to analyse our traffic. By clicking “I’m fine with this”, you are allowing the use of these cookies. Please refer to the help guide of your browser for further information on cookies, including how to disable them. Review our Privacy & Cookie Notice.