Dental Insurance Market Size 2026-2030

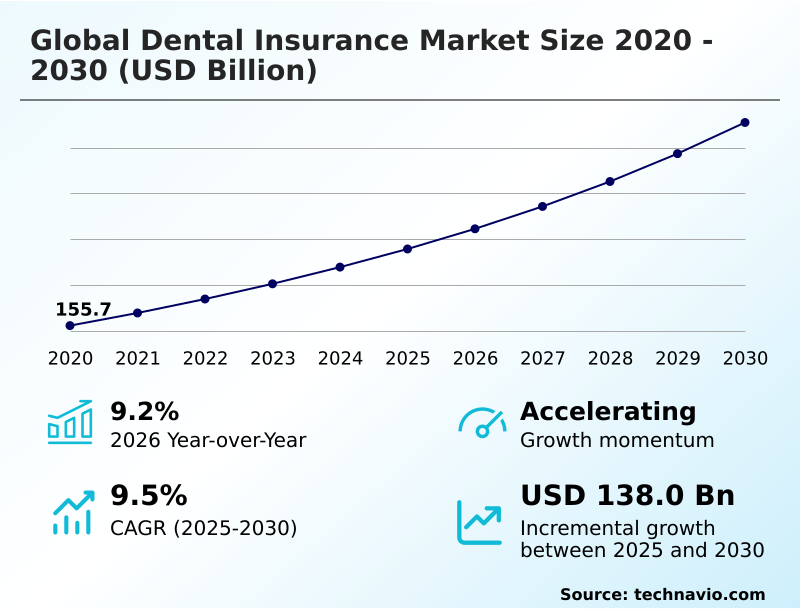

The dental insurance market size is valued to increase by USD 138 billion, at a CAGR of 9.5% from 2025 to 2030. Integration of oral and systemic healthcare models will drive the dental insurance market.

Major Market Trends & Insights

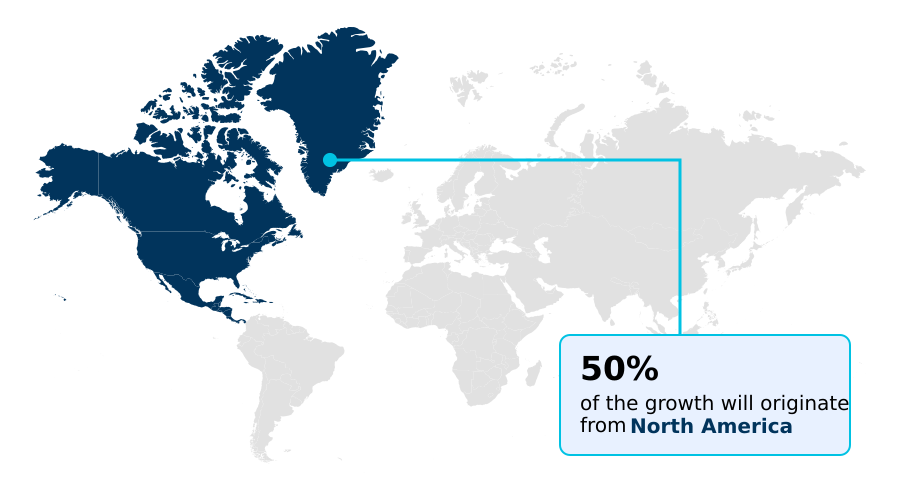

- North America dominated the market and accounted for a 49.6% growth during the forecast period.

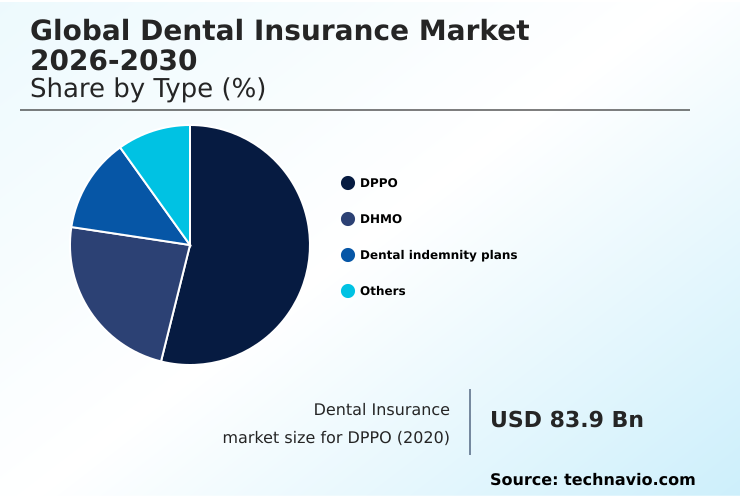

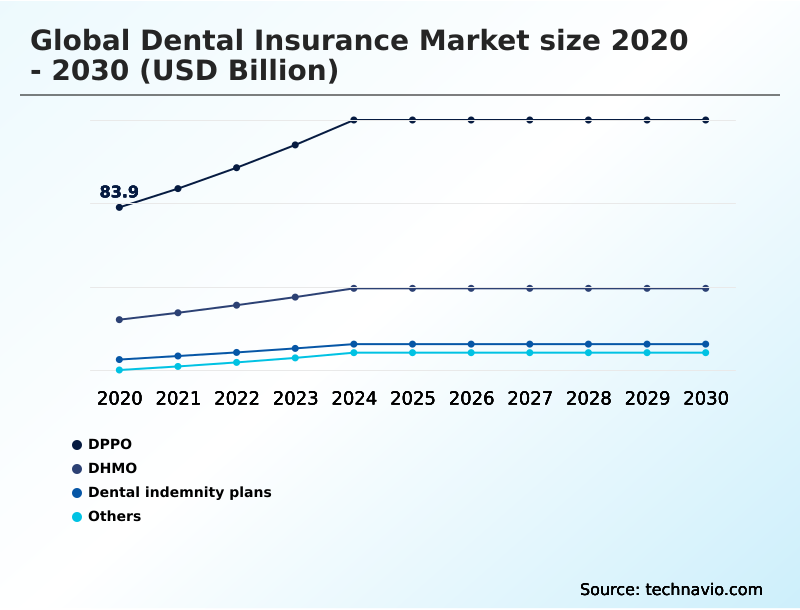

- By Type - DPPO segment was valued at USD 120.7 billion in 2024

- By Service Type - Basic segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 221.6 billion

- Market Future Opportunities: USD 138 billion

- CAGR from 2025 to 2030 : 9.5%

Market Summary

- The dental insurance market is undergoing a significant transformation, driven by a shift toward value-based care models and the integration of advanced digital technologies. Payers are moving beyond traditional reimbursement structures to prioritize preventive services and measurable patient outcomes, compelling investment in robust data analytics.

- This evolution addresses the need for greater operational efficiency in provider network management and claims adjudication automation. For instance, a business scenario involves leveraging AI-powered utilization review to analyze treatment patterns, flagging potential over-treatment and reducing costs by over 15% without compromising care quality. This approach not only contains expenses but also strengthens payer-provider collaboration models.

- Challenges remain, including navigating complex dental insurance regulatory compliance and addressing the dental workforce shortage impact, which strains network adequacy. However, the focus on teledentistry platforms and member engagement portals continues to enhance access and improve the policyholder experience, defining the industry's forward trajectory.

What will be the Size of the Dental Insurance Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Dental Insurance Market Segmented?

The dental insurance industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- DPPO

- DHMO

- Dental indemnity plans

- Others

- Service type

- Basic

- Preventive

- Major

- End-user

- Corporates

- Individuals

- Families

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- Japan

- China

- Australia

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The dppo segment is estimated to witness significant growth during the forecast period.

The global dental insurance market is segmented by plan types, with the Dental Preferred Provider Organization (DPPO) model representing a dominant structure.

This framework operates on a network-based system where carriers contract with a wide range of dental professionals to offer services at negotiated rates.

A core appeal of the DPPO is its flexibility, allowing policyholders to seek care from out-of-network providers, albeit with a different coinsurance structure. The design balances cost-containment for employers with the freedom of choice consumers demand.

This model is integral to corporate dental benefit design, especially for entities focused on provider network management and delivering value-based care models.

Effective claims adjudication automation and integrated dental-medical benefits are key to optimizing these plans and delivering effective orthodontic solutions and fee-for-service options within a Dental Health Maintenance Organization.

The DPPO segment was valued at USD 120.7 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 49.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Dental Insurance Market Demand is Rising in North America Get Free Sample

The geographic landscape of the dental insurance market is diverse, with North America accounting for 49.6% of the opportunity, driven by mature employer-sponsored markets in the United States and Canada.

Europe follows with 25.2%, where statutory health systems in countries like Germany and France are increasingly supplemented by private plans. The APAC region is the fastest-growing frontier, fueled by rising incomes in China and India.

Key operational elements like prosthodontics coverage and periodontal disease management are universal, but their implementation varies. For instance, teledentistry platforms are crucial for expanding access in markets like Australia.

The adoption of specific orthodontic solutions, management of non-covered service fees, and navigating varied cybersecurity in dental insurance protocols define regional strategies. Moreover, dental insurance for seniors and effective dental insurance network optimization are global priorities shaped by local demographics.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the dental insurance landscape requires a clear understanding of its intricate components. Consumers are constantly comparing DPPO and DHMO plans to find the best fit for their needs, while also learning how to use FSAs for dental procedures and managing dental benefits with HSAs.

- A key concern is understanding your explanation of benefits and how to calculate out-of-pocket dental costs, which is often complicated by the dental insurance waiting period explained in policy documents. The rise of value-based care models in dentistry is changing how providers operate, with an increasing focus on medical necessity criteria for implants and negotiating reimbursement rates with payers.

- Simultaneously, the impact of DSO consolidation on premiums is a major topic, as is how AI streamlines dental claims. For patients, knowing how to find the best dental insurance for orthodontic work and filing appeals for denied dental claims are critical skills.

- The industry also faces internal and external pressures, including cybersecurity risks for dental payers and ongoing regulatory changes in dental insurance. These shifts affect everything from dental coverage in medicare advantage plans to the challenges of non-covered service fees and how medical loss ratio affects plans, creating a dynamic environment for both dental insurance options for retirees and corporate beneficiaries.

- Data shows that individuals with insurance are more than twice as likely to seek preventive care, underscoring its role in promoting health.

What are the key market drivers leading to the rise in the adoption of Dental Insurance Industry?

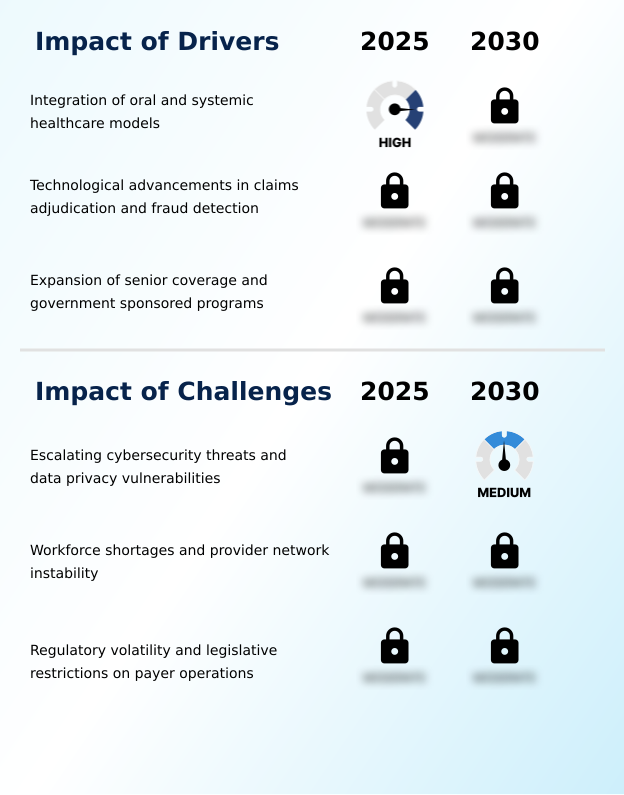

- The integration of oral and systemic healthcare models is a key driver propelling market growth and reshaping benefit plan designs.

- Market growth is propelled by the convergence of healthcare models and demographic shifts. The expansion of integrated dental-medical benefits is a primary driver, as evidence shows this approach improves outcomes for chronic conditions by over 15%.

- This has led to a re-evaluation of value-based dental reimbursement structures and dental insurance premium calculation methodologies. A significant catalyst is the growing demand for dental insurance for seniors, largely through Medicare Advantage Plans that include supplemental dental insurance.

- This demographic requires extensive prosthodontics coverage and periodontal disease management. The industry's response includes designing better self-funded dental administration options and enhancing cross-border dental coverage for retirees.

- The ongoing payer-provider collaboration models are crucial for managing costs and ensuring the viability of these expanding benefit packages, addressing a critical need in an aging global population.

What are the market trends shaping the Dental Insurance Industry?

- A significant market trend is the strategic integration of medical and oral health benefits, driven by the recognized link between oral health and systemic well-being.

- Key trends are reshaping the dental insurance sector, with a pronounced shift toward digital integration and consumer-centric products. The adoption of health savings accounts and flexible spending accounts for dental care is growing, with users reporting up to 30% more control over their healthcare spending.

- Insurers are focused on protected health information security and personally identifiable information privacy as they roll out teledentistry insurance coverage and member engagement portals. This digital shift is supported by the increasing use of automated claims review systems. Moreover, the formalization of dental implant insurance and cosmetic dentistry riders within plans addresses rising consumer demand.

- In a significant regulatory development, at least two states have enacted laws governing AI in dental claims processing, setting a precedent for industry-wide compliance. This push for transparency and efficiency is also evident in the expansion of pediatric dental benefits and orthodontia coverage plans.

What challenges does the Dental Insurance Industry face during its growth?

- Escalating cybersecurity threats and data privacy vulnerabilities present a key challenge affecting industry growth and operational stability.

- The dental insurance market faces significant structural and operational challenges that constrain growth. A primary issue is the acute dental workforce shortage impact, with over 60% of dental practices reporting difficulties in hiring, which compromises network adequacy standards and leads to care delays.

- This operational strain is compounded by escalating cybersecurity threats, as evidenced by a recent breach that exposed the data of 146,000 individuals, highlighting vulnerabilities in protecting PHI. Furthermore, navigating complex dental insurance regulatory compliance is a major hurdle. Payers must constantly adapt to new rules governing medical loss ratio and virtual credit card payments.

- The industry's reliance on electronic health record integration and the need for a stringent utilization review process create additional complexities, alongside managing the coordination of benefits and the grievance and appeals process effectively.

Exclusive Technavio Analysis on Customer Landscape

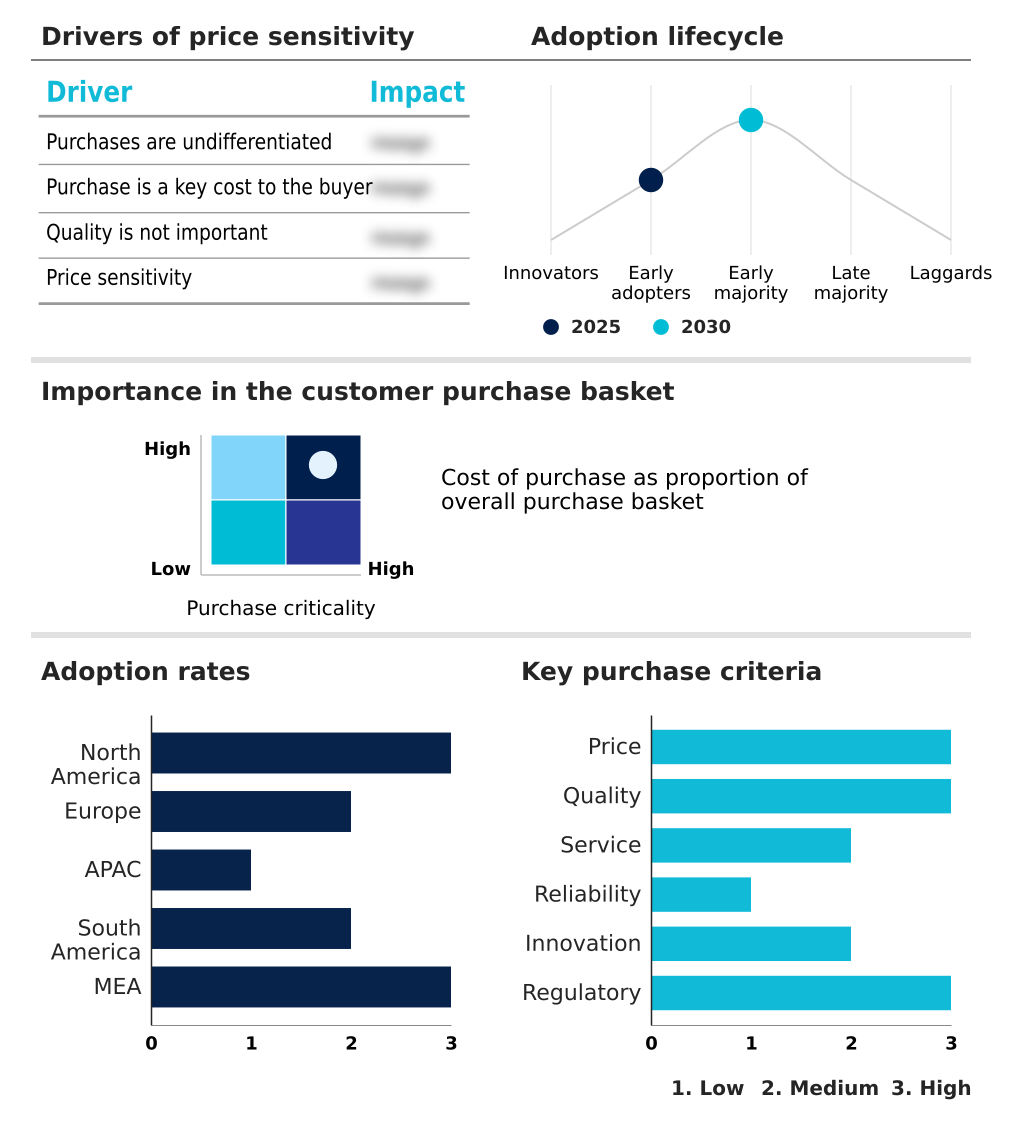

The dental insurance market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the dental insurance market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Dental Insurance Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, dental insurance market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aetna Inc. - Offers PPO and DMO dental insurance plans featuring extensive provider networks for comprehensive cleanings, fillings, crowns, and orthodontic treatments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aetna Inc.

- AFLAC Inc.

- Allianz SE

- Ameritas Mutual Holding Co.

- Anthem Inc.

- AXA Health

- Delta Dental Plans Association

- HDFC ERGO General Insurance Co.

- Humana Inc.

- Metlife Inc.

- Star Health and Allied Insurance

- Sun Life Financial Inc.

- The Cigna Group

- The Guardian Life Insurance Co

- United Concordia Companies Inc

- United HealthCare Services Inc

- Unum Group.

- Zurich Insurance Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Dental insurance market

- In August 2025, Cigna Healthcare released its 2025 Dental Trends Report, highlighting the necessity of whole-person health and detailing how integrated medical, dental, and behavioral treatments improve overall health outcomes.

- In October 2025, the states of Arizona and Maryland enacted legislation to regulate the use of artificial intelligence in insurance claim payment adjudication, establishing new legal boundaries for automated systems.

- In November 2025, Delta Dental of Virginia disclosed a significant data security incident in which an employee email compromise led to the exposure of personal and health information for approximately 146,000 individuals.

- In January 2025, the American Dental Association Health Policy Institute released a report indicating that over 60% of surveyed dentists identified staffing shortages as the most significant challenge facing their practices.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Dental Insurance Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 297 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.5% |

| Market growth 2026-2030 | USD 138.0 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.2% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, Japan, China, Australia, India, South Korea, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The dental insurance market is defined by a complex interplay of risk management and operational efficiency. Core plan structures like the Dental Preferred Provider Organization and Dental Health Maintenance Organization are evolving through technology. The industry is focused on adverse selection mitigation by refining its group underwriting and coordination of benefits protocols.

- A key boardroom-level decision area is the investment in claims adjudication automation and utilization review systems, which can reduce processing times by over 30%. This efficiency is critical for managing the high volume of transactions associated with capitation plans and direct reimbursement plans. Payers are also standardizing their pre-authorization process and explanation of benefits for clarity.

- The management of usual, customary, and reasonable rates remains a central operational task, directly impacting profitability. Adherence to network adequacy standards and a transparent grievance and appeals process are essential for regulatory compliance and maintaining member trust. These operational mechanics are fundamental to delivering sustainable and competitive dental coverage.

What are the Key Data Covered in this Dental Insurance Market Research and Growth Report?

-

What is the expected growth of the Dental Insurance Market between 2026 and 2030?

-

USD 138 billion, at a CAGR of 9.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (DPPO, DHMO, Dental indemnity plans, and Others), Service Type (Basic, Preventive, and Major), End-user (Corporates, Individuals, and Families) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Integration of oral and systemic healthcare models, Escalating cybersecurity threats and data privacy vulnerabilities

-

-

Who are the major players in the Dental Insurance Market?

-

Aetna Inc., AFLAC Inc., Allianz SE, Ameritas Mutual Holding Co., Anthem Inc., AXA Health, Delta Dental Plans Association, HDFC ERGO General Insurance Co., Humana Inc., Metlife Inc., Star Health and Allied Insurance, Sun Life Financial Inc., The Cigna Group, The Guardian Life Insurance Co, United Concordia Companies Inc, United HealthCare Services Inc, Unum Group. and Zurich Insurance Co. Ltd.

-

Market Research Insights

- The dental insurance market dynamics are increasingly shaped by a focus on value and efficiency. Payers are adopting sophisticated dental insurance cost-sharing models to manage expenses, while corporate dental benefit design is evolving to attract and retain talent. A critical area of focus is the individual dental insurance marketplace, where consumer choice is paramount.

- Statistics show that plans offering robust preventive care coverage mandates see up to 40% higher member retention compared to basic plans. Furthermore, the implementation of AI in dental claims processing has reduced adjudication errors by more than 25% for some carriers, demonstrating a clear return on investment.

- The dental workforce shortage impact continues to be a concern, with over 60% of practices reporting recruitment challenges, which directly affects dental insurance network optimization and member access to timely care.

We can help! Our analysts can customize this dental insurance market research report to meet your requirements.

RIA -

RIA -