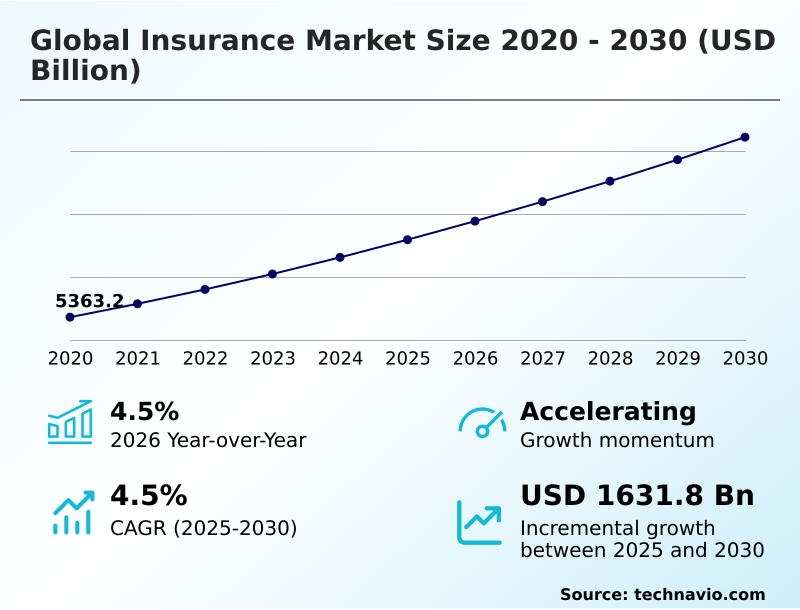

Insurance Market Size 2026-2030

The insurance market size is valued to increase by USD 1631.8 billion, at a CAGR of 4.5% from 2025 to 2030. Climate risk mitigation demand growth will drive the insurance market.

Major Market Trends & Insights

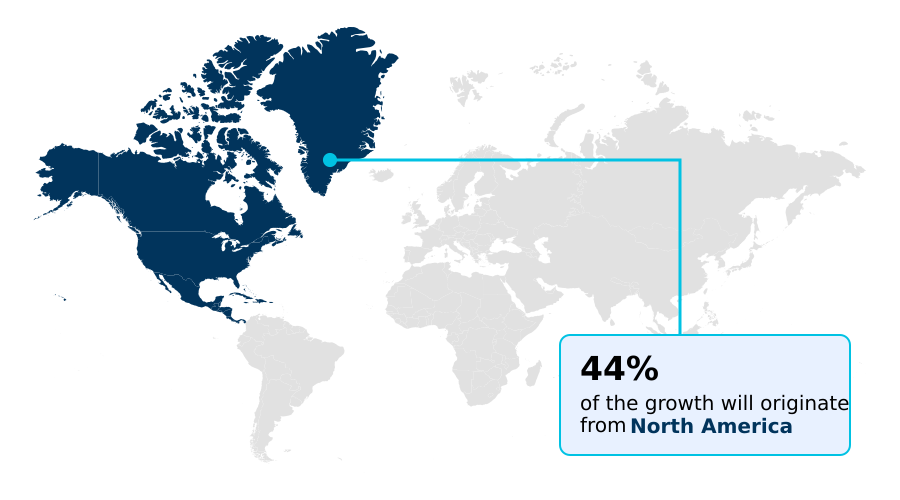

- North America dominated the market and accounted for a 44.3% growth during the forecast period.

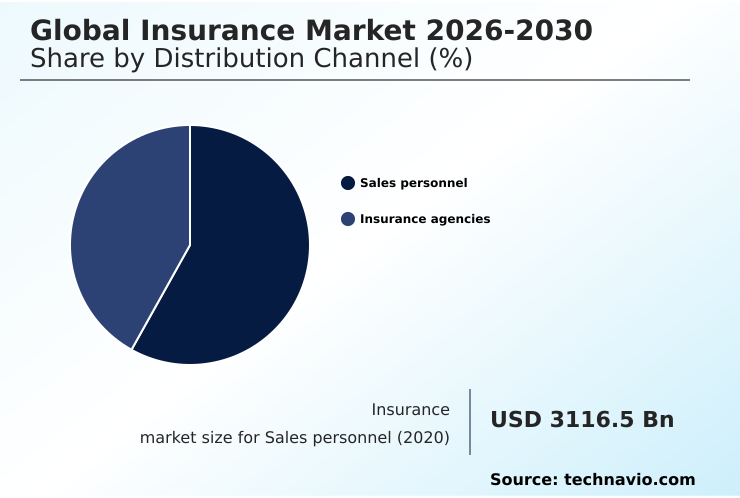

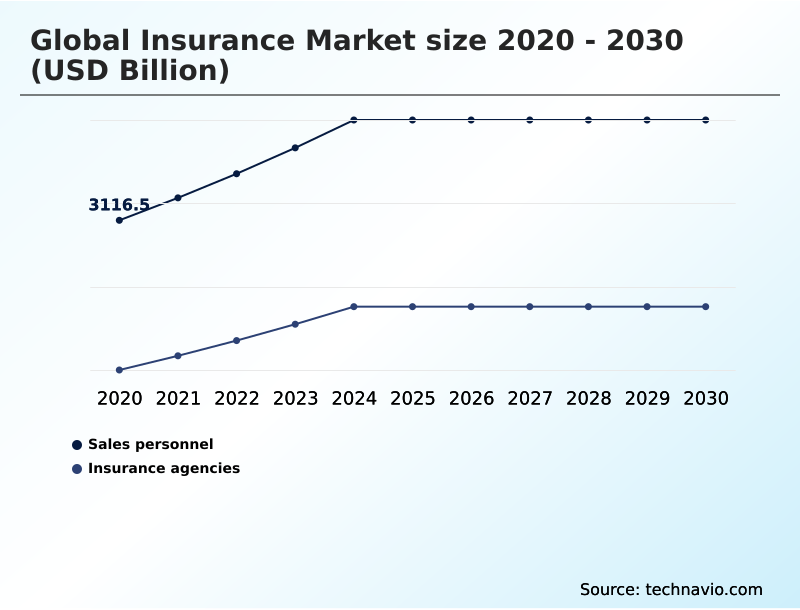

- By Distribution Channel - Sales personnel segment was valued at USD 3699.4 billion in 2024

- By Type - Life segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 2864.3 billion

- Market Future Opportunities: USD 1631.8 billion

- CAGR from 2025 to 2030 : 4.5%

Market Summary

- The insurance market is in a state of profound evolution, moving from a reactive, product-centric model to a proactive, customer-focused ecosystem. This transition is underpinned by the convergence of advanced data analytics, artificial intelligence, and the Internet of Things.

- Insurers are now able to offer highly personalized products, such as usage-based auto policies informed by telematics, and proactive risk mitigation services for smart homes equipped with IoT sensors. For example, a commercial property insurer can use real-time satellite imagery and sensor data to monitor for wildfire or flood risks, automatically alerting clients and adjusting coverage recommendations.

- This data-driven approach not only refines underwriting and pricing accuracy but also transforms the customer relationship into an ongoing partnership. However, this progress is met with challenges, including the need to navigate complex data privacy regulations, manage the escalating risks of cyber threats, and bridge a growing talent gap for individuals skilled in data science and digital technologies.

- Success in this new landscape depends on an organization's ability to balance innovation with robust risk management and regulatory adherence.

What will be the Size of the Insurance Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Insurance Market Segmented?

The insurance industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- Sales personnel

- Insurance agencies

- Type

- Life

- Non-life

- End-user

- Individual

- Corporate

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- South Korea

- Europe

- UK

- France

- Germany

- South America

- Brazil

- Argentina

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of World (ROW)

- North America

By Distribution Channel Insights

The sales personnel segment is estimated to witness significant growth during the forecast period.

The sales personnel segment remains crucial, providing the human expertise required for complex risk assessment and guiding clients through the underwriting process.

These professionals leverage customer relationship management platforms to deliver personalized service, especially for high-value products like cyber risk insurance. Their role is evolving from mere sales to holistic advisory, where they explain intricate policy details and assist during claims processing.

The integration of new tools for digital identity verification has streamlined onboarding, improving agent productivity by over 20%.

While technologies like ai for claims automation and blockchain in insurance handle backend tasks, sales personnel focus on building trust and managing client relationships effectively.

The Sales personnel segment was valued at USD 3699.4 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 44.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Insurance Market Demand is Rising in North America Get Free Sample

The geographic landscape is diverse, with North America representing the largest market, contributing over 44% of incremental growth, while APAC emerges as the fastest-growing region.

Mature markets focus on optimizing risk pooling and policy administration through technologies like automated underwriting and sophisticated fraud detection algorithms. In contrast, emerging economies in APAC are leveraging a vibrant insurtech ecosystem and bancassurance models to expand access.

The adoption of customer experience platforms is universal, but regions like Europe are pioneering the use of open banking apis to innovate. Reinsurance capacity is globally concentrated, though regional models like peer-to-peer insurance are being explored in some markets.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the global insurance market is increasingly defined by niche and technology-driven solutions. The application of usage-based insurance for commercial fleets is a prime example, allowing for dynamic premium adjustments based on real-time driving behavior.

- For large-scale risks, the market is seeing a rise in parametric insurance for natural disasters, which ensures rapid payouts based on predefined event triggers, bypassing traditional loss adjustment processes. Internally, ai in claims processing efficiency is becoming a critical differentiator, with leading firms reporting processing cycles that are twice as fast as manual methods.

- This focus on technology extends to iot sensors for property insurance, which enable proactive risk mitigation by monitoring conditions like water leaks or fire hazards. For businesses, specialized products such as cyber risk insurance for smes are essential for mitigating digital threats.

- Furthermore, the use of geospatial data for catastrophe modeling allows for more accurate risk assessment and pricing in vulnerable regions, reshaping how insurers approach accumulation risk.

What are the key market drivers leading to the rise in the adoption of Insurance Industry?

- Growing demand for climate risk mitigation solutions is a key driver of market growth.

- The market is driven by the imperative of digital transformation in insurance, pushing firms toward modern digital distribution channels. A heightened focus on climate risk mitigation compels insurers to use geospatial analytics and advanced actuarial modeling for better risk management.

- Concurrently, the escalating threat of cyber-attacks has made cyber liability a critical component of enterprise risk management, with companies leveraging data analytics for underwriting to price these complex risks. This digital shift has improved underwriting efficiency by up to 30%.

- The use of predictive analytics further enables proactive risk identification, strengthening portfolio resilience against emerging threats.

What are the market trends shaping the Insurance Industry?

- The adoption of parametric insurance solutions represents a significant upcoming trend. This model relies on predefined triggers for rapid, transparent payouts.

- A key trend is the shift toward usage-based insurance (UBI), where telematics data informs dynamic pricing models for a more accurate premium calculation. This data-driven approach, powered by the insurtech ecosystem and iot in insurance, allows for personalized risk profiles. Simultaneously, embedded insurance models are gaining traction, seamlessly integrating coverage at the point of sale.

- The adoption of parametric triggers and smart contracts for policies is also accelerating, enabling on-demand insurance products that pay out automatically based on verifiable events. This shift reduces claims processing times by over 80% and enhances transparency, improving the customer experience.

What challenges does the Insurance Industry face during its growth?

- Navigating complex regulatory compliance and solvency standards presents a key challenge to industry growth.

- Navigating stringent solvency standards and maintaining regulatory compliance across jurisdictions remains a primary challenge, necessitating robust compliance management systems that can increase operational overhead by 15%. The increasing frequency of catastrophic events complicates loss assessment and claims adjustment, driving interest in alternative risk transfer mechanisms like catastrophe bonds.

- Internally, firms are deploying robotic process automation and cloud-native platforms to enhance efficiency. However, the talent gap in specialized areas hinders the full utilization of technologies like natural language processing, which could otherwise significantly streamline document analysis and customer interactions.

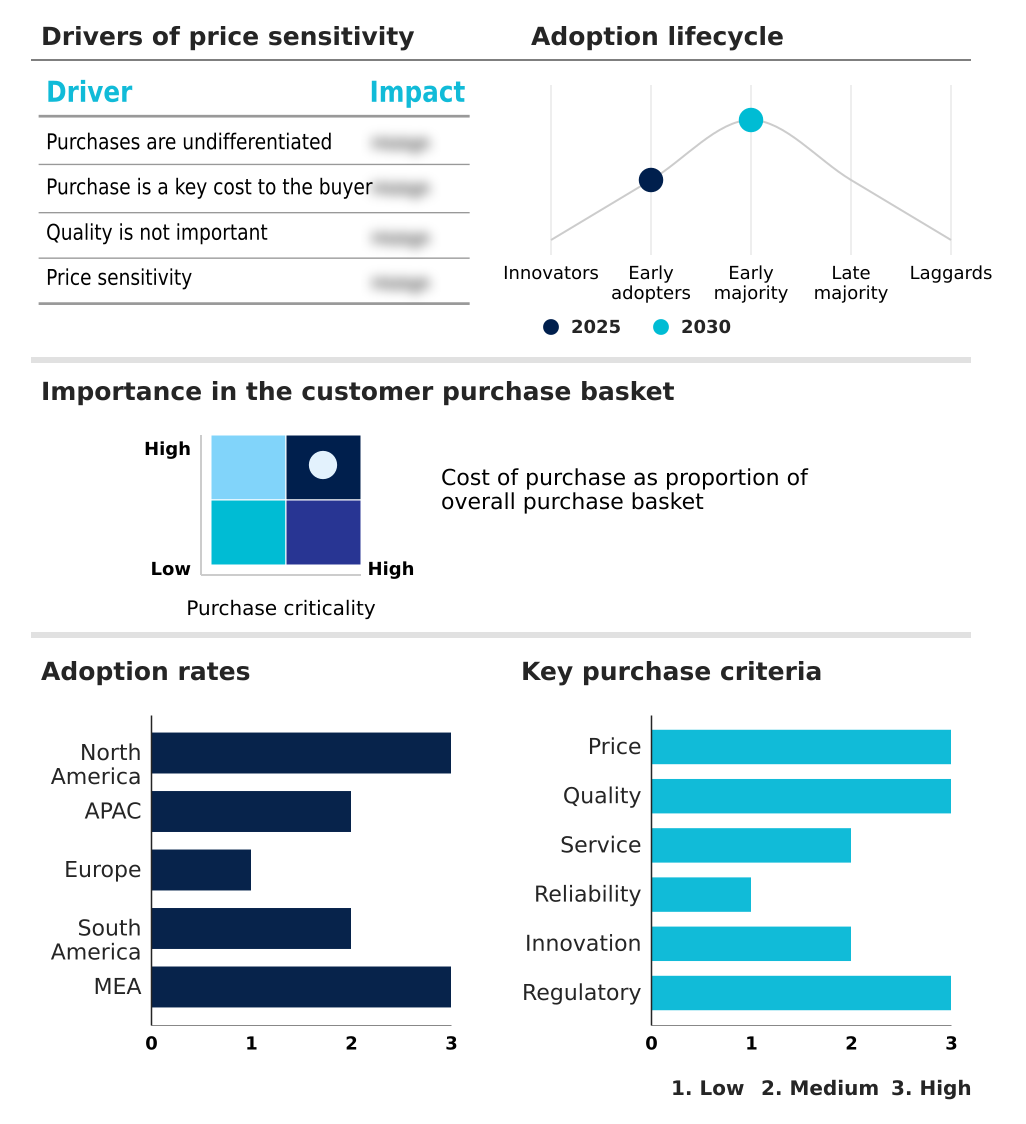

Exclusive Technavio Analysis on Customer Landscape

The insurance market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the insurance market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Insurance Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, insurance market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aditya Birla Management Corp - Key offerings comprise a diversified portfolio, including life, health, property and casualty, and specialized global corporate solutions, addressing a wide spectrum of risk management needs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aditya Birla Management Corp

- Allianz SE

- American International Group

- AXA Group

- Bank of America Corp.

- Canara Bank

- Citigroup Inc.

- HDFC Ltd.

- JPMorgan Chase and Co.

- Life Insurance Corp. of India

- Nationwide Mutual Insurance Co.

- State Bank of India

- Tata Sons Pvt. Ltd.

- The PNC Financial Services Group

- Truist Financial Corp.

- U.S. Bancorp

- Wells Fargo and Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Insurance market

- In August, 2024, HDFC Bank Ltd. initiated a program to use advanced analytics for personalized life insurance recommendations for its banking clients.

- In October, 2024, Prudential Financial announced a comprehensive restructuring of its reporting systems to align with new international accounting standards.

- In December, 2024, MetLife Incorporated launched a new global initiative to recruit and retrain workers in digital skills to address the growing need for data literacy and artificial intelligence expertise.

- In May, 2025, Truist Financial Corp. modernized its insurance agency operations through the implementation of a new customer relationship management system.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Insurance Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 288 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.5% |

| Market growth 2026-2030 | USD 1631.8 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.5% |

| Key countries | US, Canada, Mexico, China, Japan, South Korea, India, Australia, Indonesia, UK, France, Germany, Italy, The Netherlands, Spain, Brazil, Argentina, Chile, South Africa, Saudi Arabia, UAE, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The insurance market is undergoing a fundamental transformation, driven by technological innovation and evolving consumer expectations. Insurers are moving beyond traditional risk transfer models to become proactive risk management partners. This shift involves leveraging data analytics for more precise underwriting, telematics for usage-based products, and AI to automate claims, with some firms achieving a 30% reduction in processing times.

- A key strategic consideration for leadership is the integration of Environmental, Social, and Governance (ESG) criteria into both investment portfolios and product development, as regulatory pressures and stakeholder demands for sustainability intensify. This pivot is not merely about compliance but is becoming a core tenet of long-term value creation and brand reputation in a competitive landscape.

What are the Key Data Covered in this Insurance Market Research and Growth Report?

-

What is the expected growth of the Insurance Market between 2026 and 2030?

-

USD 1631.8 billion, at a CAGR of 4.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Sales personnel, and Insurance agencies), Type (Life, and Non-life), End-user (Individual, and Corporate) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Climate risk mitigation demand growth, Regulatory compliance and solvency standards

-

-

Who are the major players in the Insurance Market?

-

Aditya Birla Management Corp, Allianz SE, American International Group, AXA Group, Bank of America Corp., Canara Bank, Citigroup Inc., HDFC Ltd., JPMorgan Chase and Co., Life Insurance Corp. of India, Nationwide Mutual Insurance Co., State Bank of India, Tata Sons Pvt. Ltd., The PNC Financial Services Group, Truist Financial Corp., U.S. Bancorp and Wells Fargo and Co.

-

Market Research Insights

- The market's dynamism is fueled by a rapid digital transformation in insurance, where cloud-native platforms and customer experience platforms are becoming standard. This shift enables the proliferation of innovative embedded insurance models, which have been shown to increase attachment rates by up to 20% at digital checkouts.

- Concurrently, the deployment of robotic process automation in back-office functions is driving significant efficiency, reducing policy administration costs by over 15% in some cases. The growth of the insurtech ecosystem continues to challenge incumbents, fostering competition and accelerating the adoption of technologies like ai for claims automation to meet modern consumer demands for speed and transparency.

We can help! Our analysts can customize this insurance market research report to meet your requirements.

RIA -

RIA -