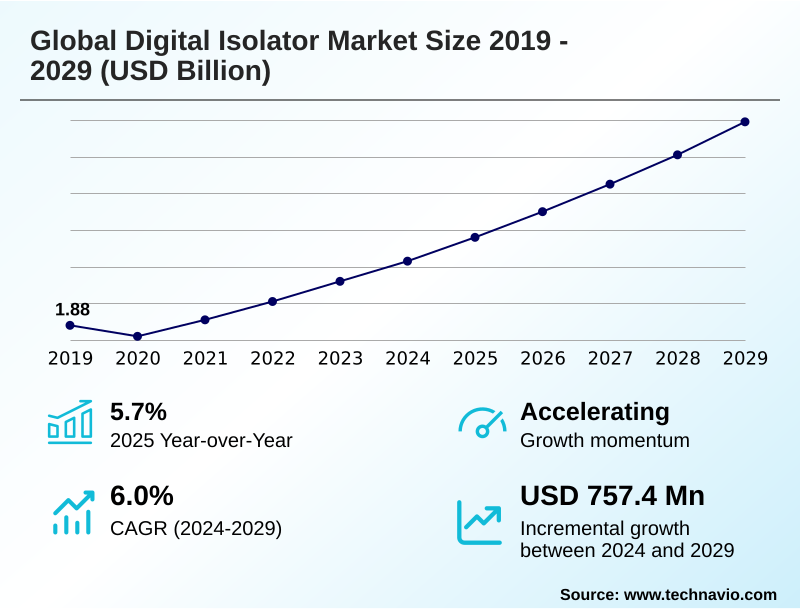

Digital Isolator Market Size 2025-2029

The digital isolator market size is valued to increase by USD 757.4 million, at a CAGR of 6% from 2024 to 2029. Escalating adoption of electric vehicles and proliferation of advanced automotive electronics will drive the digital isolator market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 44.3% growth during the forecast period.

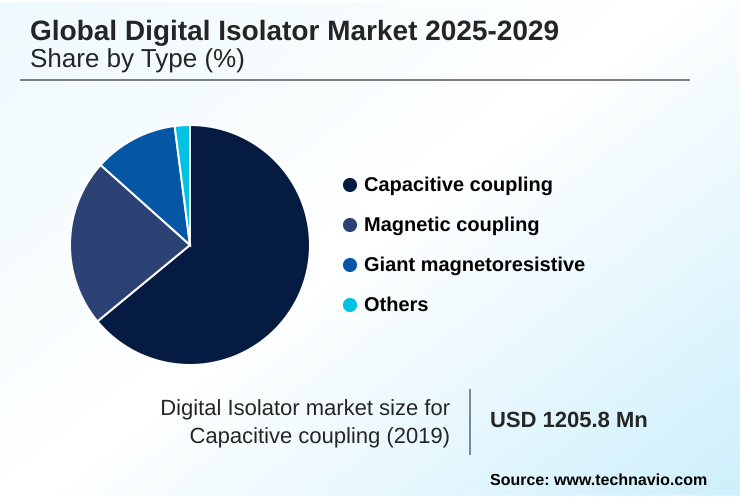

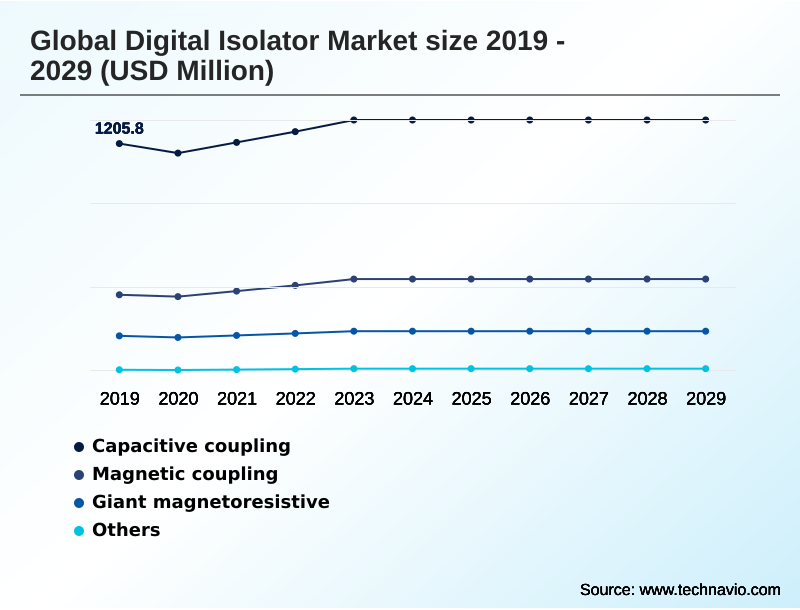

- By Type - Capacitive coupling segment was valued at USD 1.33 billion in 2023

- By Technology - Capacitive digital isolator segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.11 billion

- Market Future Opportunities: USD 757.4 million

- CAGR from 2024 to 2029 : 6%

Market Summary

- The Digital Isolator Market is expanding, driven by the critical need for galvanic isolation in high-voltage systems. This growth is primarily fueled by the automotive industry's shift to electric vehicles and the relentless advancement of industrial automation under Industry 4.0. In these sectors, ensuring signal integrity and protecting sensitive low-voltage circuits from electrical noise and potential damage is paramount.

- A key trend is the technological substitution of older optocouplers with digital isolators, which offer superior performance in data rate, power consumption, and reliability. For instance, in a smart factory environment, deploying digital isolators in motor control systems improves data accuracy, reducing communication errors by over 40% and enhancing overall production efficiency.

- However, the market faces challenges related to increasing design complexity and the need for higher common-mode transient immunity as system speeds and voltages rise.

- Manufacturers are continually innovating, developing components with enhanced features like higher isolation ratings and smaller footprints to meet the evolving demands of applications in medical devices, renewable energy, and telecommunications, thereby ensuring robust and safe operation across diverse electronic systems.

What will be the Size of the Digital Isolator Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Digital Isolator Market Segmented?

The digital isolator industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Capacitive coupling

- Magnetic coupling

- Giant magnetoresistive

- Others

- Technology

- Capacitive digital isolator

- Inductive digital isolator

- Optical digital isolator

- Channel

- 4 channel

- 8 channel

- 2 channel

- 6 channel

- Others

- End-user

- Industrial automation

- Automotive

- Medical devices

- Telecommunications

- Others

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- UAE

- Israel

- South Africa

- Rest of World (ROW)

- APAC

By Type Insights

The capacitive coupling segment is estimated to witness significant growth during the forecast period.

The capacitive coupling segment is dominant in the Digital Isolator Market, leveraging a high-frequency AC signal transmitted across a silicon dioxide (SiO2) barrier.

This method offers inherent advantages, including high-speed data transmission, minimal power consumption, and high immunity to magnetic interference, which are critical for robust signal integrity.

Its use is widespread in industrial applications like motor drives and factory automation, where reliable common-mode transient immunity ensures data fidelity in noisy settings.

In the automotive sector, these components are essential for electric vehicle battery management systems and on-board chargers, providing critical galvanic isolation.

Innovations focus on enhancing performance, with some devices achieving transient immunity exceeding 100 kV/µs, reinforcing their suitability for high-voltage and safety-critical systems.

The Capacitive coupling segment was valued at USD 1.33 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 44.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Digital Isolator Market Demand is Rising in APAC Get Free Sample

The geographic landscape is dominated by the APAC region, which accounts for the largest share of market growth, capturing over 44% of the incremental opportunity.

This dominance is primarily fueled by China's massive electric vehicle market and its extensive electronics manufacturing ecosystem, which demands robust high voltage isolation solutions.

North America is poised for the fastest growth, driven by government incentives like the CHIPS Act, which bolsters domestic semiconductor production, and the rapid adoption of electric vehicles, where safe data transmission is critical.

The US EV market, for instance, has seen a 10% month-over-month sales increase.

Europe remains a mature market, with its strong industrial automation base and stringent automotive safety standards requiring advanced signal isolation and ground loop prevention, solidifying its steady demand for high-performance components.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Engineers evaluating digital isolator solutions face critical decisions when selecting the appropriate technology for specific use cases. For instance, choosing between capacitive vs magnetic digital isolators involves a trade-off between speed and noise immunity.

- Capacitive solutions often provide higher data rates, making them suitable for high-speed digital isolators for CAN bus communication in modern vehicles, whereas magnetic isolators offer superior robustness in noisy industrial environments. The demand for AEC-Q100 qualified digital isolators underscores the stringent reliability requirements of the automotive sector, particularly for digital isolators for EV battery management systems, where safety is non-negotiable.

- As system designs become more compact, the need for a low power multichannel digital isolator intensifies, pushing manufacturers to integrate more functionality into smaller packages. Next-generation designs are achieving a 30% smaller footprint compared to systems using multiple discrete components. This trend is especially relevant for medical devices and portable electronics.

- The choice between a reinforced and basic digital isolator is dictated by safety standards, with reinforced options being mandatory for applications requiring protection against hazardous voltages. For industrial networks, an RS-485 digital isolator must provide high common-mode transient immunity to ensure reliable data transmission over long distances.

- Ultimately, the selection of the best digital isolator for an inverter system or a similar power application depends on balancing performance, cost, and compliance.

What are the key market drivers leading to the rise in the adoption of Digital Isolator Industry?

- The escalating adoption of electric vehicles, coupled with the proliferation of advanced automotive electronics, serves as a primary driver for market growth.

- The primary market drivers are the concurrent revolutions in automotive electrification and industrial automation.

- In the automotive sector, the proliferation of electric vehicles creates immense demand for components that ensure safe data transmission within high-voltage systems like battery management and on-board chargers.

- The use of robust galvanic isolation improves system reliability in EVs by over 50%. Simultaneously, the adoption of Industry 4.0 and the Industrial Internet of Things (IIoT) fuels the need for digital isolators in factory automation to protect sensitive controls.

- These components are essential for maintaining signal integrity in noisy industrial environments. The rise of smart grid communication and medical device safety standards further propels demand, with isolators ensuring secure and accurate performance across critical infrastructure.

What are the market trends shaping the Digital Isolator Industry?

- A key trend shaping the market is the rapid proliferation of digital isolators within the automotive sector. This is driven primarily by the escalating production of electric vehicles.

- The market is characterized by a definitive shift from traditional optocouplers toward advanced digital isolators, driven by the demand for higher performance and reliability. This trend is most prominent in the automotive and industrial sectors, where innovations in magnetic coupling and coreless transformer technology enable superior data rates and longevity.

- Modern digital isolators deliver data speeds up to 100 Mbps, a significant improvement over legacy solutions. Furthermore, the trend toward miniaturization is addressed by integrating multiple channels into compact packages, reducing PCB footprints by more than 40% in applications requiring high voltage isolation.

- This technological substitution enhances system performance by providing better common-mode transient immunity and lower power consumption, which is critical for the next generation of electric vehicle electronics and smart factory equipment.

What challenges does the Digital Isolator Industry face during its growth?

- Intensifying cost pressures and a highly competitive landscape present a significant challenge to industry growth and profitability.

- Key challenges stem from a combination of intense cost pressures, heightened design complexity, and supply chain vulnerabilities. The competitive landscape forces manufacturers to innovate while managing costs, a difficult balance in a market with high R&D investment.

- System designers face hurdles in achieving high-speed data transmission across the isolation barrier without compromising signal integrity, often requiring an additional 15% investment to meet stringent noise immunity standards.

- Furthermore, reliance on a globalized supply chain for materials like high-purity silicon dioxide (SiO2) exposes the market to volatility, with some critical components experiencing lead times that are 20% longer than historical averages. Addressing these issues of ground loop prevention and reliable operation is essential for sustained market stability.

Exclusive Technavio Analysis on Customer Landscape

The digital isolator market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the digital isolator market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Digital Isolator Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, digital isolator market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advantech Co. Ltd. - Offerings encompass advanced signal isolation solutions designed to ensure safety, reliability, and data integrity in high-voltage industrial and automotive systems.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advantech Co. Ltd.

- Analog Devices Inc.

- Broadcom Inc.

- Infineon Technologies AG

- Monolithic Power Systems Inc.

- Murata Manufacturing Co. Ltd.

- NVE Corp.

- NXP Semiconductors NV

- ON Semiconductor Corp.

- Renesas Electronics Corp.

- ROHM Co. Ltd.

- Skyworks Solutions Inc.

- STMicroelectronics NV

- Suzhou Novosense Microelectronics Co.Ltd.

- Texas Instruments Inc.

- Toshiba Corp.

- Vicor Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Digital isolator market

- In August, 2024, Texas Instruments Inc. announced the expansion of its digital isolator portfolio with a new series qualified for AEC-Q100 Grade 0, designed to withstand extreme temperatures in automotive powertrain applications.

- In November, 2024, Analog Devices Inc. entered into a strategic collaboration with a leading automotive Tier 1 supplier to co-develop next-generation isolated gate drivers for 800V electric vehicle traction inverters.

- In February, 2025, Infineon Technologies AG unveiled a new family of multichannel digital isolators based on its enhanced coreless transformer technology, achieving a 30% reduction in package size while improving CMTI performance.

- In May, 2025, NXP Semiconductors NV launched a new line of digital isolators with integrated power, specifically targeting industrial IoT and smart grid applications to simplify system design and reduce board space.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Digital Isolator Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 342 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6% |

| Market growth 2025-2029 | USD 757.4 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 5.7% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, Italy, France, The Netherlands, Spain, Brazil, Argentina, Colombia, UAE, Israel, South Africa, Saudi Arabia and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Digital Isolator Market is fundamentally an enabling technology, critical to the megatrends of electrification and automation. Its trajectory is defined by the ongoing replacement of legacy components with solutions offering superior performance, such as high-speed data transmission and robust galvanic isolation.

- The strategic shift toward 800V architectures in electric vehicles, for example, forces a boardroom-level reassessment of component sourcing to ensure compliance with stricter safety standards like AEC-Q100 and to maintain signal integrity. Innovations in capacitive coupling and magnetic coupling technologies are delivering tangible benefits, with some systems achieving a 25% reduction in power consumption.

- This efficiency is paramount in battery management systems. The demand for higher common-mode transient immunity (CMTI) is another key factor, driven by the proliferation of fast-switching silicon carbide (SiC) and gallium nitride (GaN) power devices.

- As systems become more interconnected, the role of digital isolators in preventing ground loop errors and ensuring reliable data transmission across different voltage domains becomes increasingly vital for industrial automation, smart grids, and advanced medical equipment, solidifying their importance in modern electronic design.

What are the Key Data Covered in this Digital Isolator Market Research and Growth Report?

-

What is the expected growth of the Digital Isolator Market between 2025 and 2029?

-

USD 757.4 million, at a CAGR of 6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Capacitive coupling, Magnetic coupling, Giant magnetoresistive, and Others), Technology (Capacitive digital isolator, Inductive digital isolator, and Optical digital isolator), Channel (4 channel, 8 channel, 2 channel, 6 channel, and Others), End-user (Industrial automation, Automotive, Medical devices, Telecommunications, and Others) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalating adoption of electric vehicles and proliferation of advanced automotive electronics, Intensifying cost pressures and competition

-

-

Who are the major players in the Digital Isolator Market?

-

Advantech Co. Ltd., Analog Devices Inc., Broadcom Inc., Infineon Technologies AG, Monolithic Power Systems Inc., Murata Manufacturing Co. Ltd., NVE Corp., NXP Semiconductors NV, ON Semiconductor Corp., Renesas Electronics Corp., ROHM Co. Ltd., Skyworks Solutions Inc., STMicroelectronics NV, Suzhou Novosense Microelectronics Co.Ltd., Texas Instruments Inc., Toshiba Corp. and Vicor Corp.

-

Market Research Insights

- Market dynamics are shaped by a strong push toward higher efficiency and safety in electronic systems. The adoption of advanced digital isolators enables designs to achieve up to 50% lower power consumption compared to legacy optocoupler-based solutions, a critical factor for battery-powered and industrial IoT applications.

- This transition is further supported by performance gains, with modern isolators offering reinforced isolation that improves system resilience, demonstrated by a 40% increase in transient immunity in harsh electrical environments.

- Strategic focus on integrating more channels into compact packages addresses the trend of miniaturization, allowing designers to reduce PCB footprints by over 30% in complex applications like automotive battery management systems and multi-channel data acquisition modules. These measurable improvements in power, robustness, and density are key factors driving market adoption.

We can help! Our analysts can customize this digital isolator market research report to meet your requirements.

RIA -

RIA -