Digital Shipyard Market Size 2026-2030

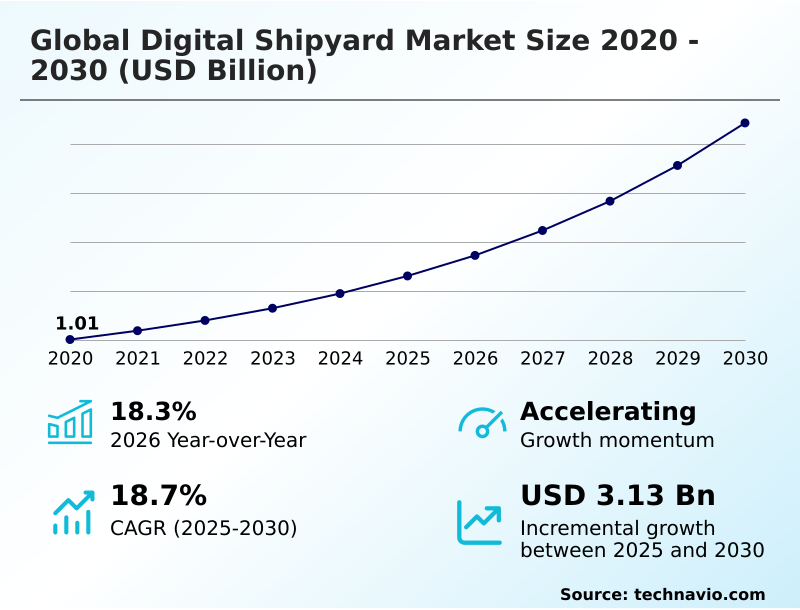

The digital shipyard market size is valued to increase by USD 3.13 billion, at a CAGR of 18.7% from 2025 to 2030. High initial investment and uncertain return on investment will drive the digital shipyard market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 34.8% growth during the forecast period.

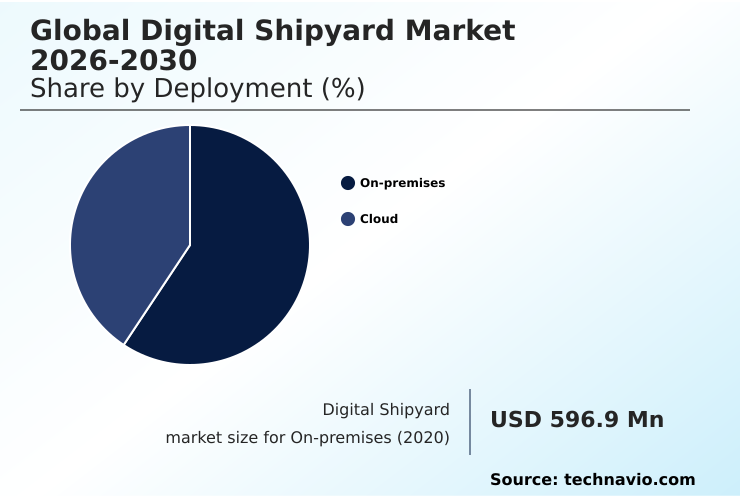

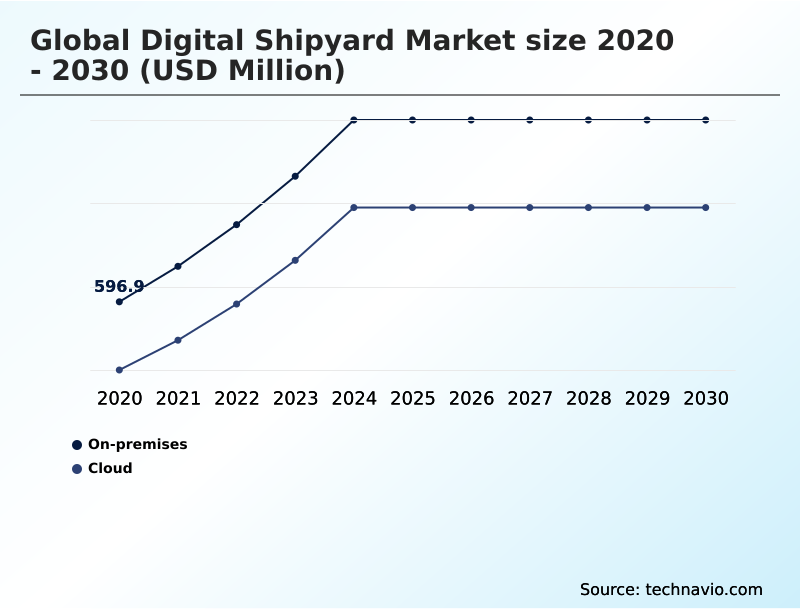

- By Deployment - On-premises segment was valued at USD 1.10 billion in 2024

- By Type - Commercial shipyards segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 4.43 billion

- Market Future Opportunities: USD 3.13 billion

- CAGR from 2025 to 2030 : 18.7%

Market Summary

- The digital shipyard market is undergoing a fundamental transformation, shifting from traditional, labor-intensive practices to integrated, data-centric operations. This evolution is driven by the urgent need to manage the increasing complexity of modern vessels, enhance productivity, and mitigate persistent skilled labor shortages.

- Technologies such as the industrial internet of things (iiot), artificial intelligence, and digital twins are no longer aspirational but are becoming core to a shipyard's competitive strategy.

- For instance, in the construction of a next-generation naval destroyer, a fully integrated digital thread connects every stage, from initial design simulations to real-time production monitoring on the shop floor and eventual through-life support. This creates a single source of truth, enabling predictive maintenance analytics and significantly reducing the costly rework that arises from data silos.

- However, the high initial investment for enterprise resource planning (erp) and the challenge of upskilling the existing workforce to leverage these advanced manufacturing processes remain significant considerations for many operators. The market's trajectory is toward creating smart, autonomous ecosystems that improve both efficiency and safety.

What will be the Size of the Digital Shipyard Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Digital Shipyard Market Segmented?

The digital shipyard industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- On-premises

- Cloud

- Type

- Commercial shipyards

- Naval and defense shipyards

- Specialized shipyards

- Application

- Medium shipyards

- Large shipyards

- Small shipyards

- Geography

- APAC

- China

- Japan

- South Korea

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Deployment Insights

The on-premises segment is estimated to witness significant growth during the forecast period.

The on-premises deployment model remains a critical component of the digital shipyard market, especially for naval and defense applications where data sovereignty and security are non-negotiable.

This approach, which involves hosting all digital infrastructure within the shipyard's physical perimeter, provides absolute control over sensitive assets like proprietary designs and national security data, enabling the use of air-gapped networks.

For mission-critical engineering tasks requiring high-performance computing, such as advanced simulation tools for computational fluid dynamics, an on-premise setup ensures minimal latency.

While requiring significant upfront capital, this model is the most reliable foundation for organizations with strict security obligations and a need for deep integration with legacy systems, ensuring data integrity in over 99% of operations for asset performance management and through-life support optimization.

The On-premises segment was valued at USD 1.10 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 34.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Digital Shipyard Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the digital shipyard market is characterized by distinct regional drivers and adoption patterns.

APAC, which accounts for 34.8% of the market's incremental growth, is defined by large-scale, state-supported initiatives aimed at creating fully autonomous production systems and smart shipyard technologies.

Countries in this region are aggressively pursuing supply chain digitalization to maintain their dominance in commercial shipbuilding. In contrast, North America and Europe are largely driven by strategic national security interests and naval fleet modernization.

Here, the focus is on deploying advanced solutions for naval vessel lifecycle management and through-life support optimization, leveraging model-based systems engineering (mbse) to manage the immense complexity of modern warships and secure the maritime industrial base.

These varied approaches reflect a global industry adapting to unique economic and geopolitical pressures.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The modern shipbuilding process is a digitally orchestrated journey, beginning with generative ai for hull form optimization and sustainable ship design using cfd analysis to meet stringent environmental targets. In the naval sector, this progresses to the use of a plm system for warship design integration and mbse for complex naval systems integration, ensuring all systems function seamlessly.

- On the production floor, ai for shipyard production scheduling optimizes workflows, while automated welding for complex hull structures ensures precision and speed. The human element is enhanced through ar for shipyard technician training and digital work instructions for outfitting, which are proven to improve first-time quality significantly.

- Throughout the vessel's life, technologies like the digital twin for naval submarine maintenance and iot sensors for predictive vessel maintenance revolutionize upkeep, with some yards using 3d scanning for ship repair assessment to quote jobs faster.

- This holistic digital approach, which includes optimizing the supply chain with shipyard erp and using iiot for real-time production monitoring, achieves a level of coherence that reduces integration faults by over 60% compared to traditional, siloed methods, fundamentally changing how vessels are built and maintained.

What are the key market drivers leading to the rise in the adoption of Digital Shipyard Industry?

- The imperative to enhance operational efficiency and reduce production costs in a competitive, labor-constrained environment serves as a primary driver for market growth.

- The market is propelled by the dual drivers of increasing vessel complexity and the government-backed imperative for naval fleet modernization.

- The shift toward sustainable ship design, incorporating alternative fuels and advanced energy-saving devices, increases design and integration complexity by over 50% compared to conventional ships, making model-based systems engineering indispensable.

- Digital tools are essential for the safe integration of these novel systems. Concurrently, strategic government initiatives are funding the development of the maritime industrial base, mandating the use of technologies that support strategic national security objectives.

- The push for shipbuilding cost reduction is also a major factor, with robotic welding automation boosting productivity in key tasks by as much as 300% over manual methods, directly addressing both labor shortages and efficiency goals.

What are the market trends shaping the Digital Shipyard Industry?

- The proliferation of digital twin technology and the establishment of an end-to-end digital thread are dominant trends shaping the industry's evolution toward integrated, data-driven operations.

- A dominant trend in the digital shipyard market is the convergence of digital twin technology with AI-powered analytics, hosted on collaborative, cloud-based shipbuilding platforms. This synergy creates a dynamic virtual replica of a vessel that is continuously updated, enabling advanced lifecycle performance simulation.

- The proliferation of digital thread integration ensures that data from design, production, and operations flow seamlessly, which is critical for reducing vessel downtime. AI-driven predictive maintenance, a key application, has demonstrated the ability to reduce unexpected equipment failures by up to 40%.

- Concurrently, the adoption of augmented reality (ar) and virtual reality (vr) for design validation and technician training is accelerating, with some shipyards reporting a 20% reduction in design review cycles. This move toward an integrated digital ecosystem is redefining shipyard operational efficiency and enabling more complex vessel integration.

What challenges does the Digital Shipyard Industry face during its growth?

- The substantial initial capital expenditure required for a full-scale digital transformation represents a primary challenge affecting widespread market adoption.

- Significant challenges hinder the widespread adoption of digital shipyard technologies, led by the need for substantial upfront investment and a critical gap in workforce skills. A full-scale digital overhaul can require an investment representing 10-15% of a shipyard's annual revenue, a formidable barrier for many.

- This is compounded by a shortage of digitally proficient talent, with demand for roles that blend data science with shipbuilding expertise outstripping supply by a ratio of 3:1 in some regions.

- Furthermore, ensuring maritime cybersecurity solutions are robust enough to protect sensitive design data is a growing concern, as cyber-attacks against industrial targets have risen by over 20% in the last year. Achieving true system interoperability to create a seamless data environment remains a persistent technical hurdle, limiting the full potential of digitalization.

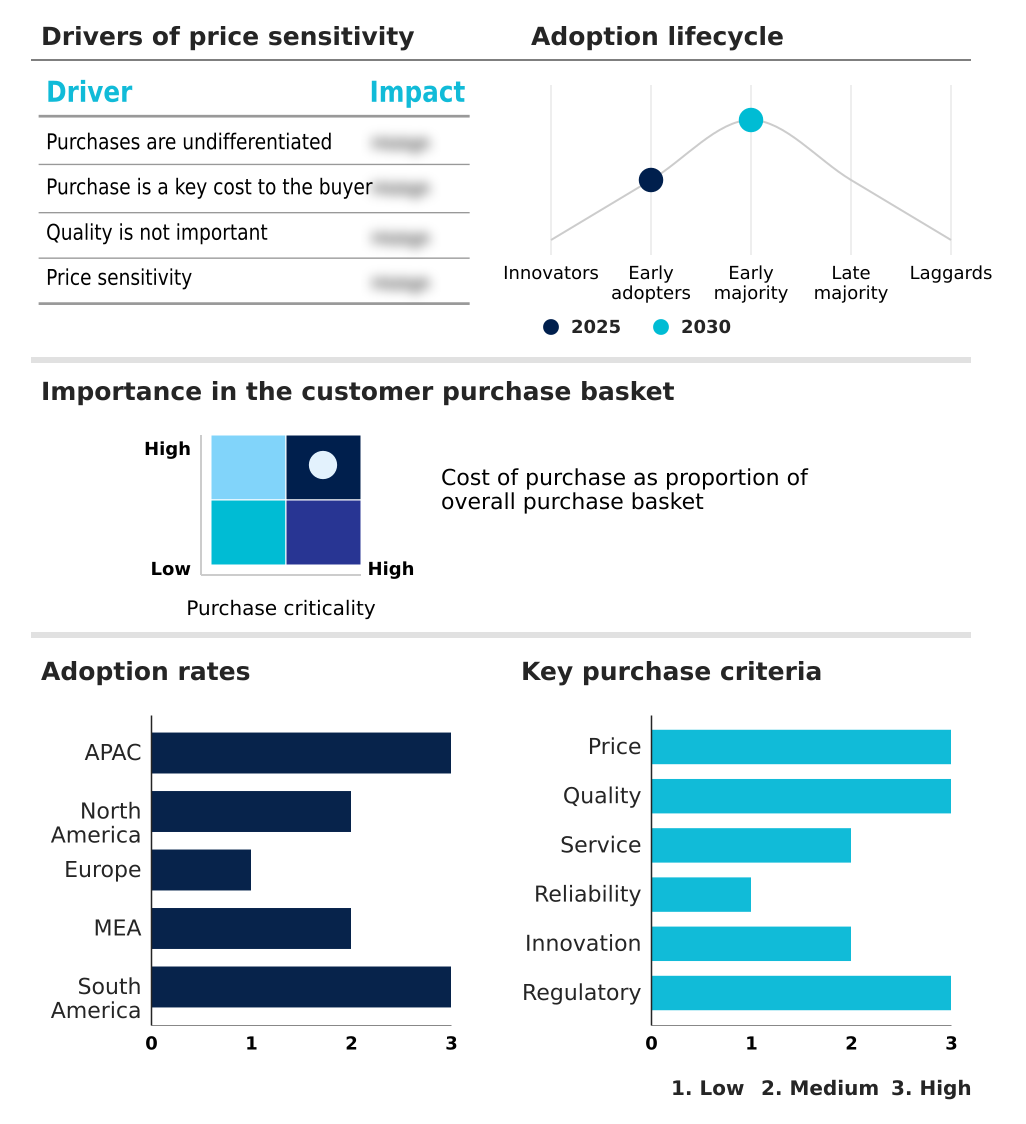

Exclusive Technavio Analysis on Customer Landscape

The digital shipyard market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the digital shipyard market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Digital Shipyard Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, digital shipyard market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - The company offers collaborative operations and marine software, enabling predictive maintenance and smart shipbuilding integration for enhanced efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Accenture PLC

- Altair Engineering Inc.

- Aras Corp.

- BAE Systems Plc

- Bentley Systems Inc.

- Damen Shipyards Group

- Dassault Systemes SE

- Emerson Electric Co.

- Hexagon AB

- Honeywell International Inc.

- IFS World Operations AB

- Inmarsat Global Ltd.

- Navantia SA

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Wartsila Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Digital shipyard market

- In May, 2025, a major Japanese consortium involving leading shipbuilders and owners completed advanced pilot trials for a collaborative digital twin platform designed to enable the secure exchange of 3D design models and operational data.

- In August, 2025, major European shipbuilder Navantia commenced operations at a new highly automated workshop in its San Fernando facility, leveraging technologies like hybrid laser welding to significantly cut construction times and costs.

- In April, 2025, a leading global container line placed a landmark order for a new fleet of ammonia-ready vessels, with the contract stipulating that the shipyard must utilize a comprehensive digital twin for virtual prototyping and lifecycle simulation.

- In July, 2025, the US Department of the Navy allocated a new tranche of funding specifically for the digital modernization of its public shipyards, with a focus on implementing digital twin technologies to reduce maintenance periods for submarines and aircraft carriers.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Digital Shipyard Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 305 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 18.7% |

| Market growth 2026-2030 | USD 3129.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 18.3% |

| Key countries | China, Japan, South Korea, India, Australia, Indonesia, US, Canada, Mexico, Germany, France, UK, Italy, The Netherlands, Spain, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The digital shipyard market represents a paradigm shift from conventional manufacturing to a fully integrated, data-driven ecosystem. The adoption of digital twin technology, product lifecycle management (plm), and the internet of things (iot) is becoming a baseline requirement for competitiveness.

- This transition necessitates boardroom-level strategic decisions regarding capital expenditure on foundational technologies like high-performance computing, enterprise resource planning (erp), and robotic welding automation. The implementation of a comprehensive digital thread integration creates an unbroken data flow from concept to decommissioning.

- This facilitates the use of virtual reality (vr), augmented reality (ar), and advanced simulation tools for virtual prototyping, which has been shown to reduce physical rework and design-related errors by over 30%. Technologies such as additive manufacturing and 3d laser scanning are further transforming maintenance and repair.

- This evolution is not merely about adopting isolated smart shipyard technologies; it is about leveraging an entire suite of tools—from ai-powered foundation models to real-time data analysis—to achieve new levels of precision and productivity in a complex industry.

What are the Key Data Covered in this Digital Shipyard Market Research and Growth Report?

-

What is the expected growth of the Digital Shipyard Market between 2026 and 2030?

-

USD 3.13 billion, at a CAGR of 18.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (On-premises, and Cloud), Type (Commercial shipyards, Naval and defense shipyards, and Specialized shipyards), Application (Medium shipyards, Large shipyards, and Small shipyards) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

High initial investment and uncertain return on investment, Imperative for operational efficiency and cost reduction amid labor shortages

-

-

Who are the major players in the Digital Shipyard Market?

-

ABB Ltd., Accenture PLC, Altair Engineering Inc., Aras Corp., BAE Systems Plc, Bentley Systems Inc., Damen Shipyards Group, Dassault Systemes SE, Emerson Electric Co., Hexagon AB, Honeywell International Inc., IFS World Operations AB, Inmarsat Global Ltd., Navantia SA, Rockwell Automation Inc., Schneider Electric SE, Siemens AG and Wartsila Corp.

-

Market Research Insights

- The dynamics of the digital shipyard market are driven by a strategic push toward greater operational resilience and competitiveness. The imperative for shipbuilding cost reduction is compelling shipyards to adopt digital platform collaboration to streamline workflows, with early adopters reporting up to a 20% acceleration in project timelines.

- Concurrently, government-led naval fleet modernization programs are accelerating the integration of technologies for complex vessel integration, which are critical for national security. Advanced simulation tools for sustainable ship design have also demonstrated a capacity to reduce material waste by over 15%, aligning with green shipbuilding initiatives.

- This digital shift addresses the need for shipyard operational efficiency while also building a more resilient maritime industrial base capable of meeting future demands with enhanced productivity and quality.

We can help! Our analysts can customize this digital shipyard market research report to meet your requirements.

RIA -

RIA -