Additive Manufacturing Market Size 2025-2029

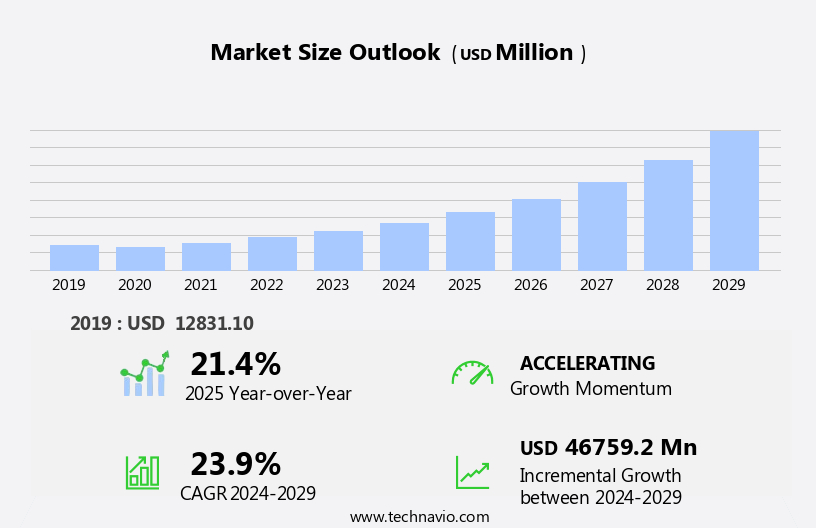

The additive manufacturing market size is forecast to increase by USD 46.76 billion at a CAGR of 23.9% between 2024 and 2029.

- The market is experiencing significant growth, driven primarily by the high demand in the medical device sector for customized and complex components. This trend is further fueled by increasing consumer interest in personalized, 3D-printed products across various industries. However, the market growth is not without challenges. The high initial cost of setting up additive manufacturing facilities remains a significant barrier for entry, limiting the number of players and potentially hindering market penetration. Moreover, the technology's limited material options and the need for specialized expertise pose additional challenges.

- To capitalize on the market opportunities and navigate these challenges effectively, companies must focus on collaborations, strategic partnerships, and continuous innovation to reduce costs, expand material offerings, and improve production efficiency. By staying abreast of the latest industry developments and trends, businesses can position themselves to succeed in this dynamic and evolving market.

What will be the Size of the Additive Manufacturing Market during the forecast period?

- The market continues to experience significant growth and innovation, driven by the increasing adoption of industrial 3d printing technologies in various industries. The market's size is projected to expand at a robust rate, with the automotive and industrial segments leading the charge. Technologies such as fuse deposition modeling, stereolithography, and selective laser sintering are gaining popularity due to their ability to produce complex geometries and reduce production expenses. The market is also witnessing increased regulatory scrutiny, leading to the development of certification standards and quality assurance protocols. The integration of advanced scanning software and design software capabilities is enabling more precise and efficient manufacturing processes.

- Mergers & acquisitions and collaboration agreements are common as companies seek to expand their offerings and enhance their competitive positions. Despite the advancements, challenges remain, including the need for installation services, addressing the skills gap, and ensuring compatibility with traditional manufacturing methods. Desktop additive manufacturing and desktop 3d printers are also gaining traction for prototyping and educational purposes. The market's future direction lies in the continued development of more advanced technologies, improved design software, and the expansion of applications beyond prototyping to production. The shift from subtractive manufacturing methods to additive manufacturing is transforming industries, offering new opportunities for innovation and cost savings.

- The market's dynamics are shaped by ongoing technological advancements, regulatory developments, and industry 4.0 trends.

How is this Additive Manufacturing Industry segmented?

The additive manufacturing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

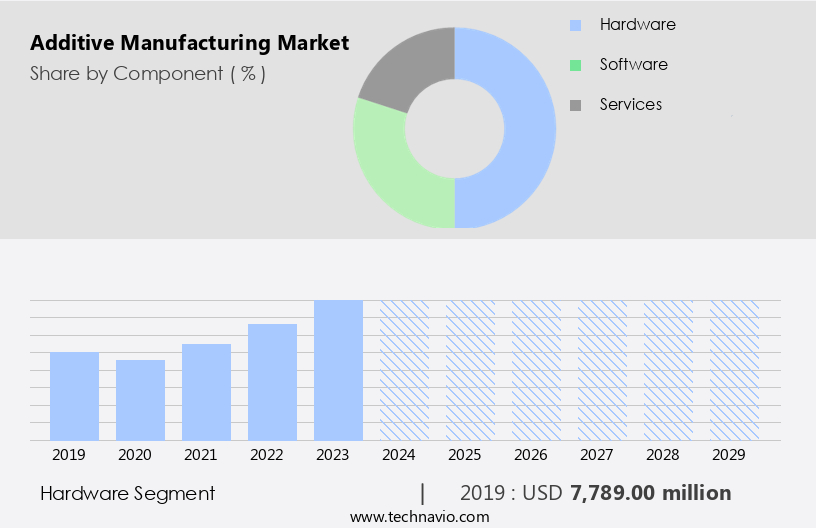

- Component

- Hardware

- Software

- Services

- End-user

- Automotive

- Aerospace

- Industrial

- Healthcare

- Defense

- Consumer Goods

- Education/Research

- Others

- Material

- Plastics

- Metals

- Ceramics

- Others

- Technology

- Stereolithography

- Polyjet printing

- Binder jetting

- Laser sintering

- Fused Deposition Modeling (FDM)

- Direct Metal Laser Sintering (DMLS)

- Electron Beam Melting (EBM)

- Directed Energy Deposition (DED)

- Others

- Binder jetting

- Geography

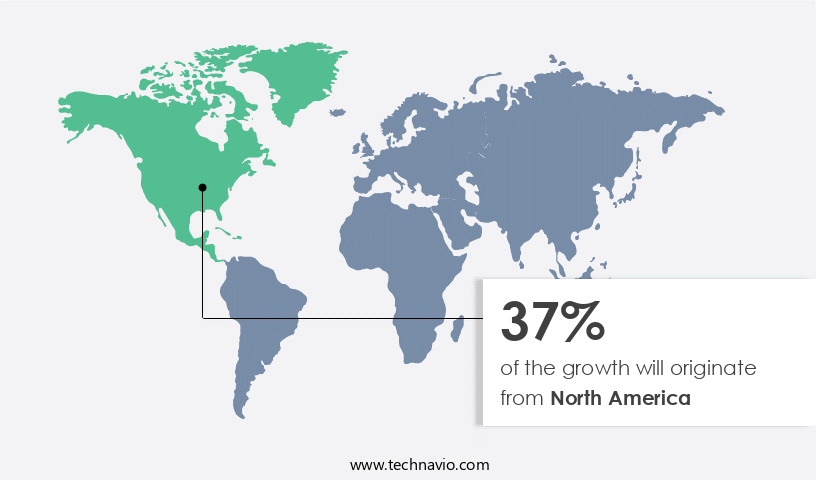

- North America

- US

- Canada

- Europe

- France

- Germany

- Spain

- UK

- APAC

- China

- India

- Japan

- South America

- Brazil

- Middle East and Africa

- UAE

- Rest of World

- North America

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

Additive manufacturing, also known as 3D printing, is revolutionizing industrial production by enabling the creation of complex parts layer-by-layer. The market for this technology is in a high-growth stage, driven by the increasing adoption in industries such as aerospace, automotive, healthcare, and manufacturing. Industrial 3D printers, which use technologies like Fused Deposition Modeling (FDM), Stereolithography, Selective Laser Sintering (SLS), and Digital Light Processing (DLP), are at the heart of this process. These printers offer advantages such as enhanced material usage, functional parts precision, and reduced production expenses. The dental industry and education sector are witnessing significant growth in the utilization of additive manufacturing for patient-specific healthcare products and educational purposes, respectively.

Material optimization and design software utilization are also crucial components, enabling the creation of cost-effective manufacturing solutions. The rapid prototyping benefits and sustainability advantages of additive manufacturing further contribute to its popularity. The market for additive manufacturing is witnessing significant software growth potential, with demand for scanning software, design software, and consultation solutions increasing. The automotive industry is a significant segment, with automotive prototyping being a major application. The proliferation of additive manufacturing technology is transforming traditional manufacturing methods, making it an essential tool for businesses seeking to remain competitive. Installation services are also becoming increasingly important to ensure the smooth implementation of additive manufacturing solutions.

Additive manufacturing, through its various components, is transforming the manufacturing landscape by offering rapid manufacturing processes, improved material usage, and cost savings. The technology's continued growth is expected to bring about significant advancements in various industries.

Get a glance at the market report of share of various segments Request Free Sample

The Hardware segment was valued at USD 7.79 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

Additive manufacturing, also known as 3D printing, is revolutionizing industrial production by enabling the creation of complex, functional parts through layer-by-layer addition. This technology offers several advantages over traditional manufacturing methods, including enhanced material usage, reduced production expenses, and increased precision. Industrial 3D printers, such as Fuse Deposition Modeling and Stereolithography, are increasingly being adopted for manufacturing functional parts, particularly in industries like automotive and dental. The automotive industry's growing demand for lightweight components and customized designs is driving the adoption of additive manufacturing. Companies like General Motors (GM) and Ford Motor Company are investing in this technology to improve fuel efficiency, reduce emissions, and cater to evolving consumer preferences and regulatory standards.

The dental industry is also experiencing significant growth due to the production of patient-specific healthcare products. Additive manufacturing also offers sustainability advantages, as it minimizes material waste and reduces the need for transportation and inventory. The technology's proliferation is further fueled by the growth potential of design software and scanning software, which enable efficient production and optimization of materials. Despite the advantages, the market is still in its high growth stage, with significant potential for further expansion. The technology's capabilities continue to evolve, with advancements in metal material dominance, rapid manufacturing processes, and consultation solutions. The education sector is also utilizing additive manufacturing for educational purposes, further expanding its reach and impact.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Additive Manufacturing Industry?

- High demand in medical device sector is the key driver of the market.

- 3D printing is revolutionizing the medical field by enabling the creation of customized implants and prosthetics, tailored to the unique requirements of individual patients. This customization leads to improved fit and functionality, resulting in better patient outcomes. Medical professionals utilize 3D printing technology to create anatomical models, offering a hands-on understanding of complex surgeries and techniques. These models reduce operation time and risks by providing a more comprehensive visualization of patient anatomy and pathology, aiding in the planning of intricate medical and surgical procedures.

- The adoption of 3D printing in the medical sector is on the rise due to its numerous advantages, making it an essential tool for medical professionals in clinical and research applications.

What are the market trends shaping the Additive Manufacturing Industry?

- Increase in consumer interest in 3D customized products is the upcoming market trend.

- Customization in additive manufacturing, or 3D printing, is gaining popularity among consumers due to the ability to create unique, tailor-made products. This trend is driven by the increasing affordability of desktop 3D printers, enabling individuals to produce customized items at home. However, the high cost of these printers limits their accessibility to a select group of consumers with a significant disposable income. As a result, many consumers opt for online services that offer customized 3D-printed products. The market for customized 3D-printed goods is expanding, with various industries, such as healthcare, automotive, and aerospace, adopting this technology to create complex and intricate parts.

- Despite the high cost, consumers are willing to invest in customized 3D-printed products due to their unique value proposition. This trend is expected to continue, with advancements in technology and increasing affordability leading to wider adoption.

What challenges does the Additive Manufacturing Industry face during its growth?

- High initial cost incurred in setting up additive manufacturing facilities is a key challenge affecting the industry growth.

- Additive manufacturing, a revolutionary technology in the manufacturing industry, is characterized by its layer-by-layer production process. While the market for this technology is growing, the high costs associated with it remain a significant challenge. The primary drivers of these costs are the specialized equipment and advanced software required for additive manufacturing. The cost of entry-level FDM or SLA machines is relatively low, ranging from under USD5,000. However, high-end additive manufacturing printers, such as SLS, material jetting, and metal printing, can cost anywhere from USD200,000 to USD850,000, and even several millions of dollars. Moreover, the need for proprietary raw materials sold by 3D printer manufacturers at high profit margins further contributes to the high costs.

- End-users also face the additional expense of training or hiring skilled personnel to ensure the production of high-quality devices. Despite these challenges, the benefits of additive manufacturing, including reduced material waste, increased design freedom, and faster production times, make it an attractive option for various industries.

Exclusive Customer Landscape

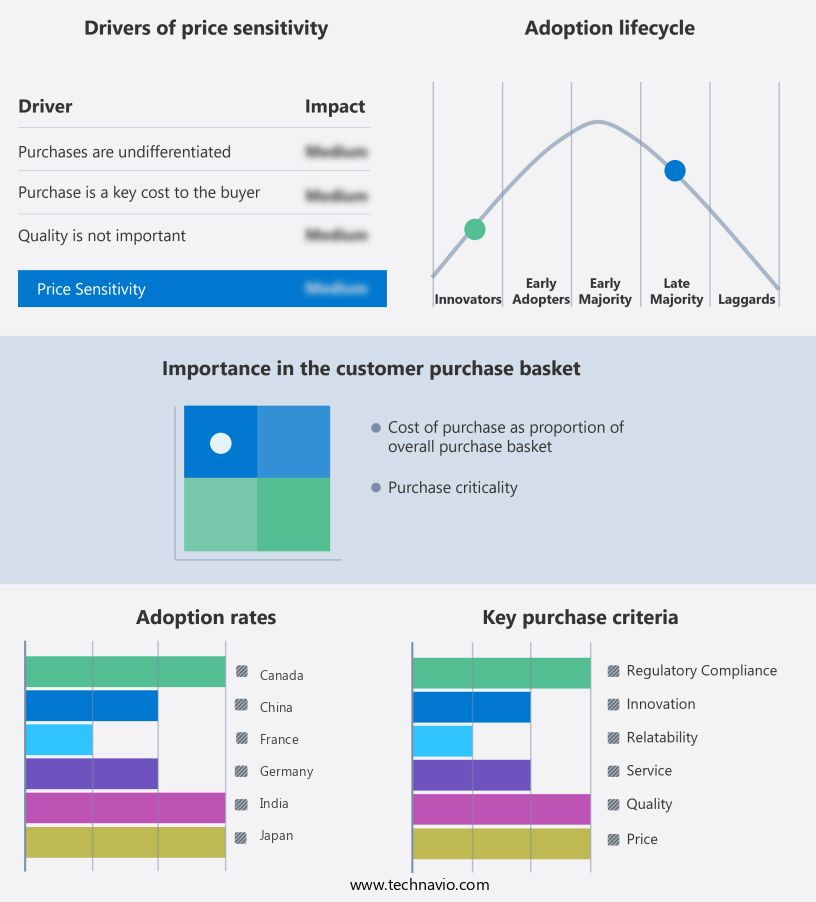

The additive manufacturing market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the additive manufacturing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, additive manufacturing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3D Systems Corp. - The company specializes in additive manufacturing solutions, providing advanced 3D printers, print materials, and accompanying software. Our offerings cater to various industries, enabling efficient production and innovation through cutting-edge technology.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3D Systems Corp.

- 3DEO Inc.

- Additive Industries BV

- Autodesk Inc.

- BICO Group AB

- Canon Inc.

- Carbon Inc.

- CINCINNATI Inc.

- ColVisTec AG

- DMG MORI Co. Ltd.

- dsm-firmenich

- ENVISIONTEC US LLC

- EOS GmbH

- Formlabs Inc.

- General Electric Co.

- HP Inc.

- Markforged Holding Corp.

- MATERIALISE NV

- Stratasys Ltd.

- voxeljet AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Additive manufacturing, also known as 3D printing, is a revolutionary technology that enables the creation of three-dimensional objects by adding material layer-by-layer. This process offers several advantages over traditional manufacturing methods, making it an increasingly popular choice for various industries. One significant benefit of additive manufacturing is the enhanced material usage it provides. By building objects from the ground up, only the necessary material is used, reducing waste and production expenses. This feature is particularly appealing to industries that deal with complex geometries and intricate designs. Industrial 3D printers, which are designed for large-scale production, have gained traction in recent years.

These printers use various techniques such as Fuse Deposition Modeling (FDM) and Stereolithography (SLA) to create functional parts with high precision. The ability to produce precise parts is crucial for industries that require high-quality components, such as the aerospace and medical sectors. Desktop 3D printers, on the other hand, are more suitable for prototyping and educational purposes. These printers offer a cost-effective solution for individuals and small businesses, allowing them to create their designs quickly and easily. The growth of additive manufacturing has led to an increased demand for scanning software, which is essential for converting traditional designs into 3D models.

The software market is expected to grow significantly as more companies adopt additive manufacturing processes. Functional parts produced through additive manufacturing offer several advantages over those made using subtractive methods. These advantages include reduced material waste, faster production times, and the ability to create complex geometries that are difficult or impossible to achieve using traditional methods. The dental industry has seen significant growth in the adoption of additive manufacturing technology. Patient-specific healthcare products, such as dental implants and bridges, can be produced using 3D printing, leading to improved patient outcomes and reduced production costs. The education sector is also utilizing additive manufacturing for various purposes, including research and development, curriculum development, and student training.

The technology's ability to create complex models and prototypes makes it an invaluable tool for educational institutions. Material optimization is another area where additive manufacturing excels. By using advanced design software and material properties, manufacturers can optimize their designs for improved performance and reduced production costs. Stereolithography, a popular additive manufacturing technique, offers several advantages over traditional manufacturing methods. It allows for the production of parts with high resolution and intricate details, making it ideal for industries that require high-precision components. The automotive industry is another sector that has embraced additive manufacturing, particularly for prototyping and automotive design.

The technology's ability to create complex geometries and functional parts quickly and cost-effectively makes it an attractive option for automotive manufacturers. The growth potential of additive manufacturing software is significant, with the market expected to expand rapidly as more companies adopt the technology. The software market includes design software, scanning software, and consultation solutions, all of which are essential for optimizing the additive manufacturing process. Rapid prototyping is another area where additive manufacturing excels, offering significant benefits over traditional manufacturing methods. The technology's ability to produce functional parts quickly and cost-effectively makes it an attractive option for companies looking to bring their products to market faster.

Additive manufacturing also offers sustainability advantages, as it reduces material waste and production emissions compared to traditional manufacturing methods. The technology's high growth stage and continued technology proliferation make it an exciting area for innovation and development. Metal materials dominate the additive manufacturing landscape, with companies investing heavily in research and development to expand their offerings. Rapid manufacturing processes, such as metal 3D printing, are becoming increasingly common, offering significant benefits over traditional manufacturing methods. Installation services are also an essential part of the additive manufacturing ecosystem, ensuring that companies can effectively integrate the technology into their production processes.

These services include installation, training, and ongoing support, ensuring that companies can maximize the benefits of their additive manufacturing investments.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

242 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 23.9% |

|

Market growth 2025-2029 |

USD 46759.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

21.4 |

|

Key countries |

US, Germany, China, Canada, Japan, UK, France, India, Spain, South KoreaUAE, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Additive Manufacturing Market Research and Growth Report?

- CAGR of the Additive Manufacturing industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the additive manufacturing market growth of industry companies

We can help! Our analysts can customize this additive manufacturing market research report to meet your requirements.

RIA -

RIA -