Electronic Warfare (Ew) Market Size and Growth Forecast 2026-2030

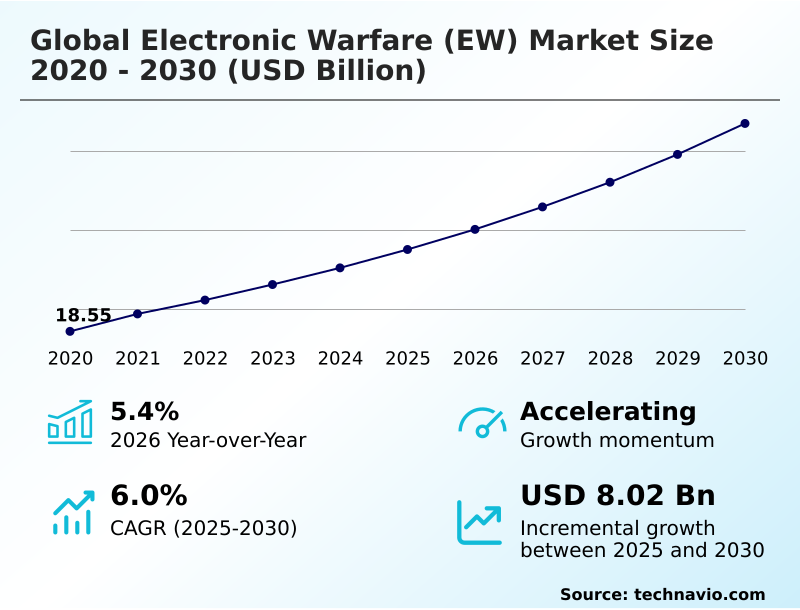

The Electronic Warfare (Ew) Market size was valued at USD 23.76 billion in 2025 growing at a CAGR of 6% during the forecast period 2026-2030.

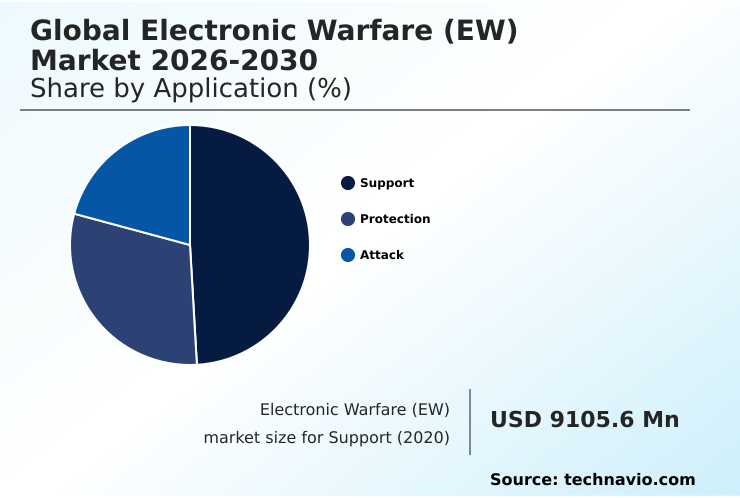

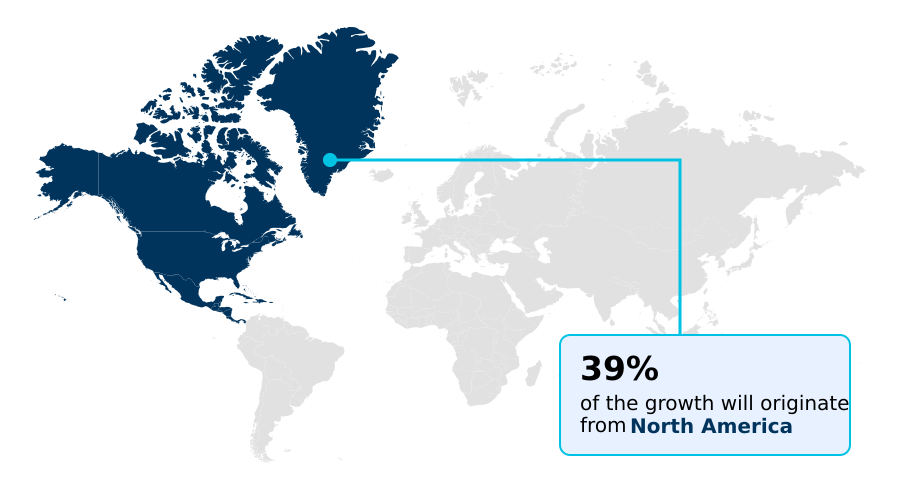

North America accounts for 39% of incremental growth during the forecast period. The Support segment by Application was valued at USD 11.11 billion in 2024, while the Airborne segment holds the largest revenue share by Platform.

The market is projected to grow by USD 13.23 billion from 2020 to 2030, with USD 8.02 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Electronic Warfare (Ew) Market Overview

The electronic warfare (EW) market is defined by a strategic imperative for electromagnetic spectrum dominance, with a year-over-year growth of 5.4% reflecting extensive defense modernization programs. This landscape is increasingly shaped by multi-domain operations, compelling a shift from legacy platforms to integrated, software-defined radio (SDR) in EW solutions. A key focus is the development of cognitive electronic warfare, where systems autonomously adapt to novel threats. For instance, in a contested airspace scenario, an airborne platform's electronic attack systems might leverage real-time spectrum analysis to dynamically counter an adversary’s adaptive radar, a process that relies on advanced AI and ML in EW threat detection. This capability enhancement is crucial as North America, which accounts for 39% of the incremental growth, continues to drive technological advancements. However, procurement decisions are complicated by the high development and integration costs associated with these sophisticated systems, pushing for the adoption of open systems architecture for EW to mitigate long-term expenses and ensure interoperability.

Drivers, Trends, and Challenges in the Electronic Warfare (Ew) Market

The strategic landscape of the electronic warfare (EW) market is increasingly shaped by complex regulatory and technical hurdles, with frameworks like the International Traffic in Arms Regulations (ITAR) governing the export of sensitive technologies. This creates significant challenges for multi-domain operations EW integration, as collaboration between allied nations on ew systems for unmanned aerial vehicles requires navigating stringent compliance protocols.

The cost of developing cognitive EW systems is a major barrier, pushing prime contractors to explore software-defined EW system architecture and open architecture EW system upgrades to manage expenses. In practice, a defense firm developing next generation jammer mid band capabilities for a naval platform must balance performance with the high costs of integrating gallium nitride based EW components.

These open standards can reduce development timelines by up to 30% compared to proprietary systems. Furthermore, the focus on ew training and simulation platforms highlights the need for realistic environments to prepare for countering hypersonic missile threats with EW.

Specialized applications, such as miniaturized ew systems for ground forces and EW protection for naval vessels, demand unique solutions, while integrating EW with cyber warfare becomes critical for addressing threats in anti-access area denial (A2AD) environments and securing GPS signals against jamming.

This complexity extends to developing EW countermeasures for drone swarms and systems for urban warfare scenarios, demanding adaptive and resilient technologies.

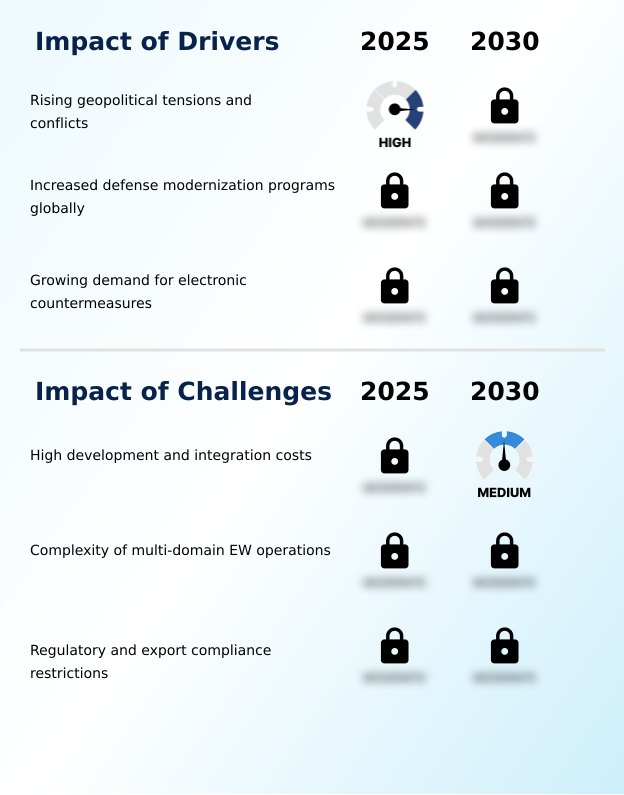

Primary Growth Driver: Rising geopolitical tensions and conflicts are a key driver for the market, compelling nations to invest in advanced electronic warfare capabilities to maintain strategic superiority.

Market growth is primarily propelled by increased defense modernization programs globally, fueled by rising geopolitical tensions and conflicts. Nations are allocating significant budgets to upgrade legacy platforms and achieve electromagnetic spectrum dominance.

This modernization is particularly evident in the APAC region, which is expanding its capabilities at a faster rate than Europe, driven by the need to counter sophisticated regional threats.

The demand for advanced electronic countermeasures (ECM) suites is surging as military operations become more reliant on technology for asset protection in contested environments.

This includes the widespread procurement of new platform survivability equipment and systems designed for the suppression of integrated air defense systems (IADS), ensuring operational superiority in high-threat scenarios.

Emerging Market Trend: The integration of artificial intelligence and machine learning is a transformative market trend, driven by the need for faster, more adaptive threat responses in complex electromagnetic environments.

Key market trends are centered on the integration of artificial intelligence and the miniaturization of components. The development of cognitive electronic warfare, which leverages AI and ML in EW threat detection, is enabling systems to move beyond pre-programmed libraries and autonomously counter novel threats using adaptive signal processing. This is critical for real-time spectrum analysis in congested environments.

Concurrently, the trend toward miniaturized EW systems for ground forces and unmanned platforms is expanding operational flexibility. These compact, power-efficient modules facilitate the deployment of advanced electronic support measures and unmanned aerial system countermeasures at the tactical edge, enhancing force protection and situational awareness without relying on large, dedicated assets.

This convergence of intelligent software and compact hardware is reshaping both defensive and offensive capabilities across all operational domains.

Key Industry Challenge: High development and integration costs represent a significant challenge, constraining procurement budgets and slowing the pace of innovation across the electronic warfare market.

Significant market constraints stem from the high development and integration costs associated with sophisticated EW platforms and the complexity of multi-domain EW operations. The financial burden of creating advanced cognitive systems creates substantial barriers to entry and limits procurement for even well-funded defense ministries.

A primary technical hurdle is achieving seamless interoperability across air, land, sea, space, and cyber domains, a key challenge in multi-domain operations EW integration. Furthermore, regulatory and export compliance restrictions, such as the International Traffic in Arms Regulations (ITAR), add layers of administrative complexity and can impede international collaboration and technology transfer.

These factors collectively slow innovation and create uncertainty for global suppliers, impacting the overall competitiveness and growth trajectory of the market.

Explore Full Market Dynamics Analysis Request Free Sample

Electronic Warfare (Ew) Market Segmentation

The electronic warfare (ew) industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Application Segment Analysis

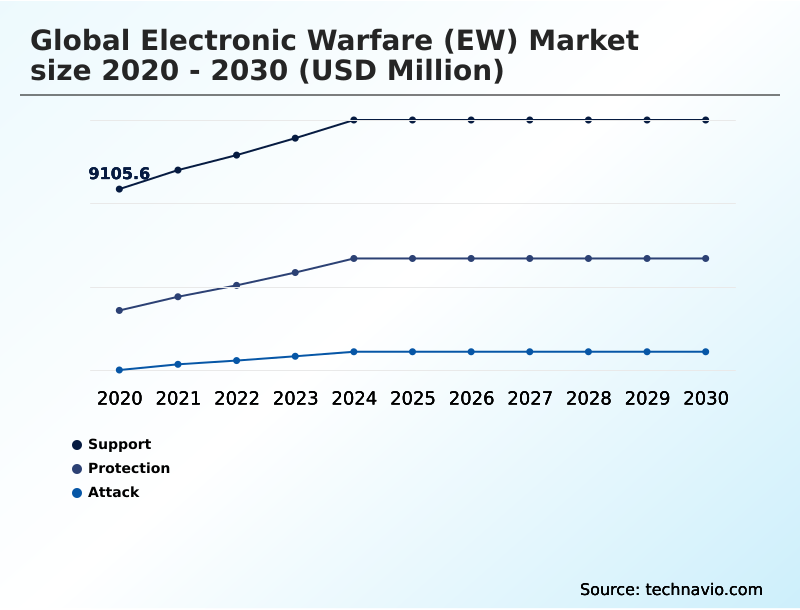

The support segment is estimated to witness significant growth during the forecast period.

The support segment is foundational to electromagnetic operations, primarily involving electronic support measures and signal intelligence (SIGINT) to provide situational awareness.

This segment, which accounts for nearly half of the market, focuses on the passive detection and analysis of radiated energy for immediate threat recognition.

The adoption of cognitive electronic warfare is transforming this space, with threat detection algorithms processing vast datasets to counter advanced threats. Operations are shifting toward decentralized intelligence gathering, leveraging passive surveillance systems and unmanned aerial system countermeasures.

This evolution from static libraries to dynamic, real-time spectrum analysis is critical for identifying adversary electronic orders of battle and enabling effective electronic attack systems and protection measures in contested environments.

The Support segment was valued at USD 11.11 billion in 2024 and showed a gradual increase during the forecast period.

Electronic Warfare (Ew) Market by Region: North America Leads with 39% Growth Share

North America is estimated to contribute 39% to the growth of the global market during the forecast period.

The geographic landscape of the electronic warfare (EW) market is dominated by North America, which accounts for over 39% of market growth, driven by large-scale modernization programs in the United States.

This region is focused on achieving electromagnetic spectrum dominance through advanced airborne self-protection suites and stand-off jamming platforms.

Meanwhile, the APAC region is the fastest-growing theater, contributing over 30% of new growth, fueled by geopolitical tensions and the need to counter sophisticated integrated air defense systems (IADS).

Nations in this region are heavily investing in naval EW systems and ground-based jamming systems to protect maritime trade routes and territorial claims.

Europe follows, with a focus on collaborative defense initiatives to develop next-generation EW capabilities and ensure interoperability among NATO allies, particularly in electronic intelligence (ELINT) gathering.

Customer Landscape Analysis for the Electronic Warfare (Ew) Market

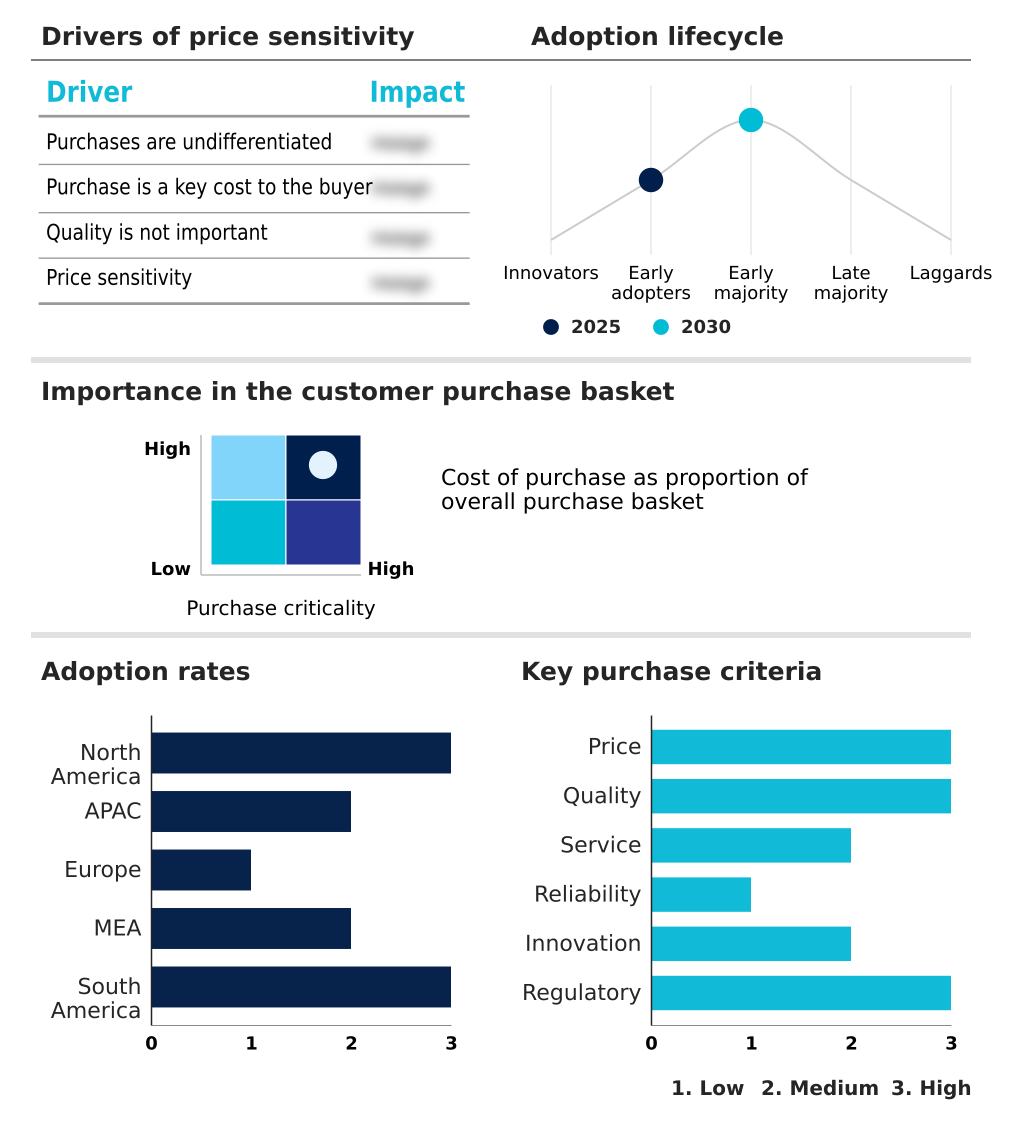

The electronic warfare (ew) market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the electronic warfare (ew) market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Electronic Warfare (Ew) Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the electronic warfare (ew) market industry.

Airbus SE - Offerings center on advanced survivability pods and multi-class soft-kill systems, delivering enhanced platform protection and cyber-electromagnetic superiority across contested operational domains.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airbus SE

- ASELSAN AS

- BAE Systems Plc

- Elbit Systems Ltd.

- General Dynamics Corp.

- Israel Aerospace Ltd.

- L3Harris Technologies Inc.

- Leonardo S.p.A.

- Lockheed Martin Corp.

- Mercury Systems Inc.

- Northrop Grumman Corp.

- RTX Corp.

- Saab AB

- Sierra Nevada Corp.

- Teledyne Technologies Inc.

- Thales Group

- The Boeing Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Electronic Warfare (Ew) Market

- In August, 2024, the United States Navy awarded a significant contract to initiate full-rate production of its Surface Electronic Warfare Improvement Program (SEWIP) Block 3, a system designed to provide enhanced electronic attack capabilities for fleet assets.

- In November, 2024, the Australian Department of Defence announced a strategic agreement aimed at expanding the domestic production of critical electronic attack components for its fleet of EA-18G Growler aircraft, reinforcing sovereign industrial capability.

- In March, 2025, The French Ministry of the Armed Forces successfully conducted the first comprehensive operational flight test of the SPECTRA electronic warfare suite under the Rafale F4.2 standard, which integrates AI to automate threat detection and response.

- In April, 2025, a prominent European Union defense consortium launched a pilot program to integrate advanced cognitive sensors into existing naval reconnaissance fleets, aiming to automate the classification of complex and unidentified radar signals in real-time.

Research Analyst Overview: Electronic Warfare (Ew) Market

The electronic warfare (EW) market is undergoing a fundamental realignment driven by the operational demands of multi-domain operations. This shift necessitates investment in advanced capabilities like cognitive electronic warfare and directed energy weapons (DEW) to achieve electromagnetic spectrum dominance.

Boardroom decisions for prime contractors now center on balancing the high R&D expenditure for proprietary electronic attack systems against the adoption of open standards like the Sensor Open Systems Architecture (SOSA). This strategic choice is heavily influenced by compliance with frameworks such as the International Traffic in Arms Regulations (ITAR), which impacts international sales and partnerships.

As North America contributes over 39% of market growth, the technological race is intensifying. A key focus is on integrating digital radio frequency memory (DRFM) and gallium nitride (GaN) amplifiers into next-generation airborne self-protection suites and naval EW systems to ensure platform survivability.

The complexity of countering threats requires a move toward integrated solutions, combining electronic protection measures, signal intelligence (SIGINT), and cyber-electromagnetic activities (CEMA) to secure tactical data link security and command and control (C2) protection across all domains.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Electronic Warfare (Ew) Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6% |

| Market growth 2026-2030 | USD 8024.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.4% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, Israel, South Africa, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Electronic Warfare (Ew) Market: Key Questions Answered in This Report

-

What is the expected growth of the Electronic Warfare (Ew) Market between 2026 and 2030?

-

The Electronic Warfare (Ew) Market is expected to grow by USD 8.02 billion during 2026-2030, registering a CAGR of 6%. Year-over-year growth in 2026 is estimated at 5.4%%. This acceleration is shaped by rising geopolitical tensions and conflicts, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Support, Protection, and Attack), Platform (Airborne, Ground, Naval, and Space), Technology (IR missile warning, Antennas, Anti-jam system, and Others) and Geography (North America, APAC, Europe, Middle East and Africa, South America). Among these, the Support segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, APAC, Europe, Middle East and Africa and South America. North America is estimated to contribute 39% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, Israel, South Africa, Turkey, Brazil, Argentina and Colombia, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is rising geopolitical tensions and conflicts, which is accelerating investment and industry demand. The main challenge is high development and integration costs, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Electronic Warfare (Ew) Market?

-

Key vendors include Airbus SE, ASELSAN AS, BAE Systems Plc, Elbit Systems Ltd., General Dynamics Corp., Israel Aerospace Ltd., L3Harris Technologies Inc., Leonardo S.p.A., Lockheed Martin Corp., Mercury Systems Inc., Northrop Grumman Corp., RTX Corp., Saab AB, Sierra Nevada Corp., Teledyne Technologies Inc., Thales Group and The Boeing Co.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Electronic Warfare (Ew) Market Research Insights

The electronic warfare (EW) market is increasingly governed by Modular Open Systems Approach (MOSA) mandates, compelling a strategic shift in procurement and system design. This push for interoperability fundamentally alters the competitive landscape, favoring vendors who offer adaptable and upgradable platform survivability equipment.

For example, a naval fleet command can now source a best-in-class cognitive radar system from one supplier and integrate it with a next generation jammer (NGJ) from another, reducing vendor lock-in and total cost of ownership. This modularity allows for rapid insertion of technologies like adaptive signal processing to counter emerging non-kinetic attack capabilities.

As a result, the support segment is growing at a different pace than the attack segment, reflecting the foundational investment in flexible, future-proof architectures.

We can help! Our analysts can customize this electronic warfare (ew) market research report to meet your requirements.

RIA -

RIA -