Epidermal Growth Factor Receptor (EGFR) Inhibitors Market Size 2026-2030

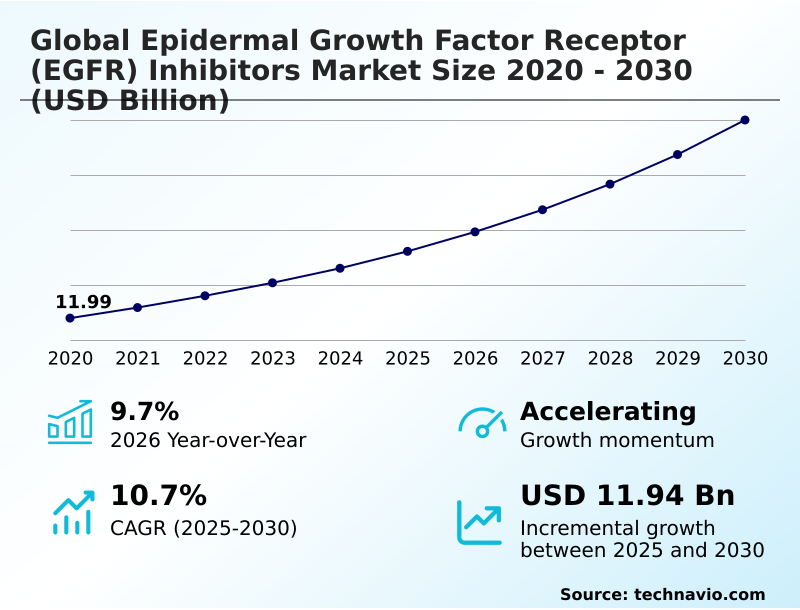

The epidermal growth factor receptor (egfr) inhibitors market size is valued to increase by USD 11.94 billion, at a CAGR of 10.7% from 2025 to 2030. Advancements in combination therapies and regulatory approvals will drive the epidermal growth factor receptor (egfr) inhibitors market.

Major Market Trends & Insights

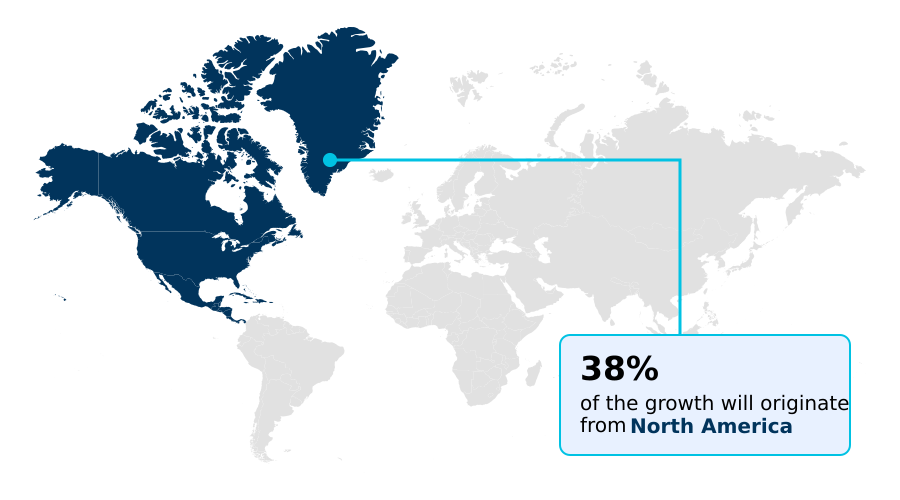

- North America dominated the market and accounted for a 37.8% growth during the forecast period.

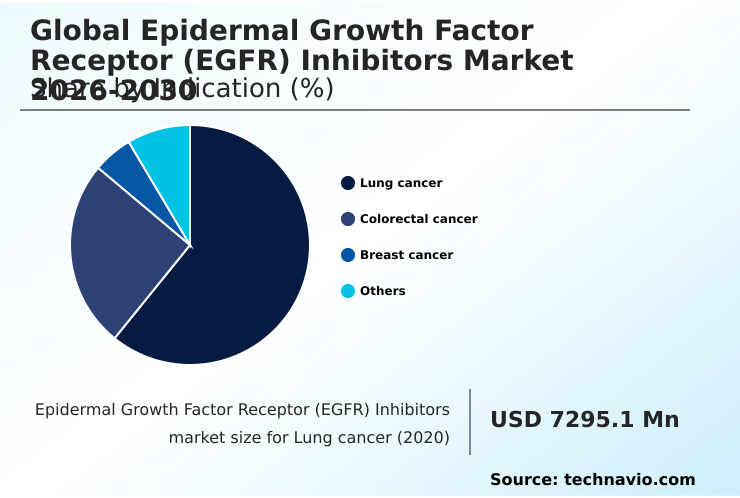

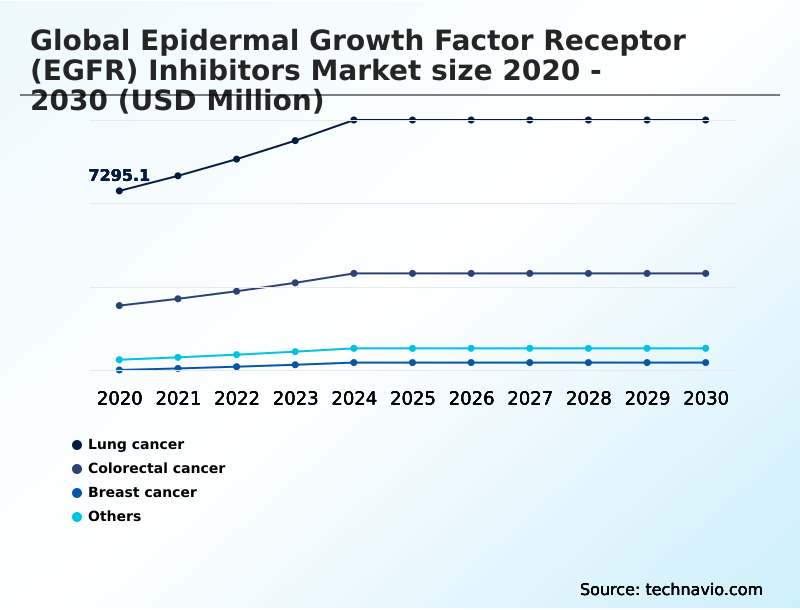

- By Indication - Lung cancer segment was valued at USD 9.93 billion in 2024

- By Distribution Channel - Retail pharmacies segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 18.01 billion

- Market Future Opportunities: USD 11.94 billion

- CAGR from 2025 to 2030 : 10.7%

Market Summary

- The Epidermal Growth Factor Receptor (EGFR) Inhibitors market is expanding, primarily driven by the integration of precision medicine into standard oncology care. This evolution is marked by a strategic shift from monotherapies to advanced combination regimens that demonstrate superior clinical outcomes.

- A key trend is the development of next-generation inhibitors designed to overcome acquired resistance, a common challenge that limits long-term treatment efficacy. For instance, a hospital system implementing routine liquid biopsies to monitor treatment response can adjust therapeutic strategies in real-time, significantly improving patient outcomes and optimizing resource allocation.

- This approach relies heavily on sophisticated companion diagnostics to accurately identify patient populations with specific mutations. The industry's focus is on creating more durable responses and improving quality of life, which involves managing treatment-related toxicities through innovative drug formulations and supportive care protocols.

- Furthermore, the development of molecules with enhanced central nervous system penetration is a critical area of research to address brain metastases, a significant unmet need for patients with advanced disease. The competitive landscape fosters continuous innovation, ensuring a robust pipeline of novel therapies.

What will be the Size of the Epidermal Growth Factor Receptor (EGFR) Inhibitors Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Epidermal Growth Factor Receptor (EGFR) Inhibitors Market Segmented?

The epidermal growth factor receptor (egfr) inhibitors industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Indication

- Lung cancer

- Colorectal cancer

- Breast cancer

- Others

- Distribution channel

- Retail pharmacies

- Hospital pharmacies

- Online pharmacies

- Drug class

- Small molecule TKIs

- Monoclonal antibodies

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Indication Insights

The lung cancer segment is estimated to witness significant growth during the forecast period.

The lung cancer segment's market dominance is driven by the high prevalence of targetable mutations in non-small cell lung cancer. This has accelerated the development of advanced targeted cancer therapy and next-generation inhibitors.

The evolution from broad chemotherapy to precision oncology is evident, with new tyrosine kinase inhibitors designed as first-line treatment for metastatic disease. Clinical efficacy is increasingly measured by improvements in progression-free survival and overall survival rates.

The push for personalized medicine and chemotherapy-free regimens is supported by rigorous EGFR mutation testing, with some clinical trials for new agents achieving objective response rates nearing 60%, showcasing a significant leap in treatment effectiveness and a move toward more tailored patient care.

The Lung cancer segment was valued at USD 9.93 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Epidermal Growth Factor Receptor (EGFR) Inhibitors Market Demand is Rising in North America Get Free Sample

The global landscape for EGFR inhibitors is led by North America, which accounts for approximately 37.8% of incremental growth, driven by high R&D investment and accelerated regulatory approval pathways. Europe follows, with its harmonized regulatory system supporting consistent market access.

The Asia region, however, is projected to be the fastest-growing, with a market expansion of 12.2%, fueled by the high prevalence of EGFR mutations and increasing access to advanced healthcare.

Regional success depends on robust pharmacovigilance infrastructure and the local availability of active pharmaceutical ingredient supplies. Companies are navigating varied reimbursement frameworks and health technology assessment requirements.

The development of monoclonal antibodies and therapies targeting unresectable stage three mutations and the c797s mutation are key focus areas, with real-world evidence playing a crucial role in shaping regional adoption within specialty oncology networks.

Market Dynamics

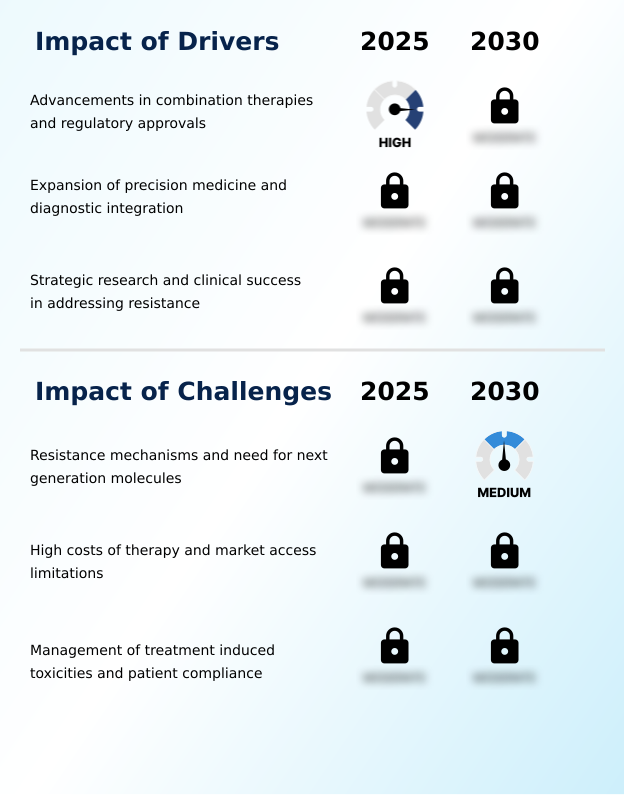

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic imperative in the Epidermal Growth Factor Receptor (EGFR) Inhibitors market is overcoming EGFR TKI resistance mechanisms, which drives the entire research and development pipeline. This includes the focused development of EGFR inhibitors for brain metastases, a frequent site of disease progression.

- The evolution toward combination therapy for EGFR-mutated NSCLC as a standard of care necessitates a parallel focus on managing toxicities of EGFR inhibitor therapy to ensure patient compliance and quality of life. The role of liquid biopsy in EGFR monitoring has become pivotal, enabling real-time tracking of tumor dynamics and informing treatment adjustments.

- This is closely linked to the discovery of new biomarkers for predicting EGFR inhibitor response. Operationally, the advancements in subcutaneous EGFR inhibitor delivery are reshaping supply chains and clinical workflows, offering a more efficient alternative to hospital-based infusions. As portfolios expand, the cost-effectiveness of targeted cancer drugs comes under intense scrutiny from payers, influencing market access strategies.

- Portfolios centered on validated combination therapies show a substantially higher clinical success rate than those focused on monotherapies alone. Addressing the c797s mutation in EGFR is a core component of fourth-generation EGFR inhibitors development. Concurrently, improving CNS penetration of TKIs and advancing EGFR bispecific antibodies in clinical trials are critical for future growth, supported by real-world evidence for EGFR inhibitors.

What are the key market drivers leading to the rise in the adoption of Epidermal Growth Factor Receptor (EGFR) Inhibitors Industry?

- The approval of advanced combination therapies is a key driver for the market, enhancing clinical outcomes and expanding treatment options.

- Market growth is fueled by the expansion of precision medicine, integrating advanced diagnostics with targeted treatments.

- The use of companion diagnostics and non-invasive diagnostics like liquid biopsies ensures treatments for mutation-driven tumors are administered to the correct patient population with over 95% accuracy.

- This synergy between biomarker discovery and drug development is exemplified in treatments for kras g12c mutated colorectal cancer. Innovations in genomic profiling and bioinformatics are enabling more sophisticated patient stratification, leading to better clinical trial endpoints and outcomes.

- The development of multi-target approaches and the use of digital diagnostic platforms address the challenge of tumor heterogeneity, making treatment more effective. This data-driven approach has improved progression-free survival by up to 15 months in certain patient cohorts.

What are the market trends shaping the Epidermal Growth Factor Receptor (EGFR) Inhibitors Industry?

- A key market trend is the advancement of next-generation tyrosine kinase inhibitors (TKIs). These are specifically engineered to target complex and resistant mutational profiles.

- Key trends are reshaping the therapeutic landscape, focusing on enhancing patient convenience and tackling complex mutations. The shift from intravenous administration to subcutaneous delivery is significant, with new formulations reducing infusion-related reactions by over 40%. This transition improves quality of life and aligns with new dosing strategies. Concurrently, biosimilar development is introducing market competition.

- Advances in molecular modeling are facilitating the design of novel antibody-drug conjugates and bispecific antibody therapies targeting the tyrosine kinase domain with high precision. This therapeutic innovation is crucial for addressing exon 20 insertion mutations and improving central nervous system penetration, a persistent challenge in treating brain metastases.

- AI-driven screening is also accelerating patient identification for clinical trials by 2x, speeding up development timelines.

What challenges does the Epidermal Growth Factor Receptor (EGFR) Inhibitors Industry face during its growth?

- A key challenge affecting industry growth is the emergence of drug resistance mechanisms, which necessitates continuous development of next-generation molecules.

- Persistent challenges constrain market potential, led by acquired resistance and the high cost of therapy. The emergence of cancer treatment resistance from factors like HER2 mutations requires continuous R&D investment. Developing therapies with effective blood-brain barrier penetration to treat leptomeningeal disease remains a significant hurdle.

- Furthermore, adverse events management is critical, as toxicities lead to treatment discontinuation in nearly 20% of patients on certain regimens, negatively impacting patient-reported outcomes. The high cost of therapy creates access barriers, with cost-effectiveness analysis often delaying reimbursement. This leads to the implementation of patient assistance programs as a partial solution.

- Aligning with supportive care guidelines and established treatment guidelines is essential for mitigating these challenges and ensuring patient adherence and safety.

Exclusive Technavio Analysis on Customer Landscape

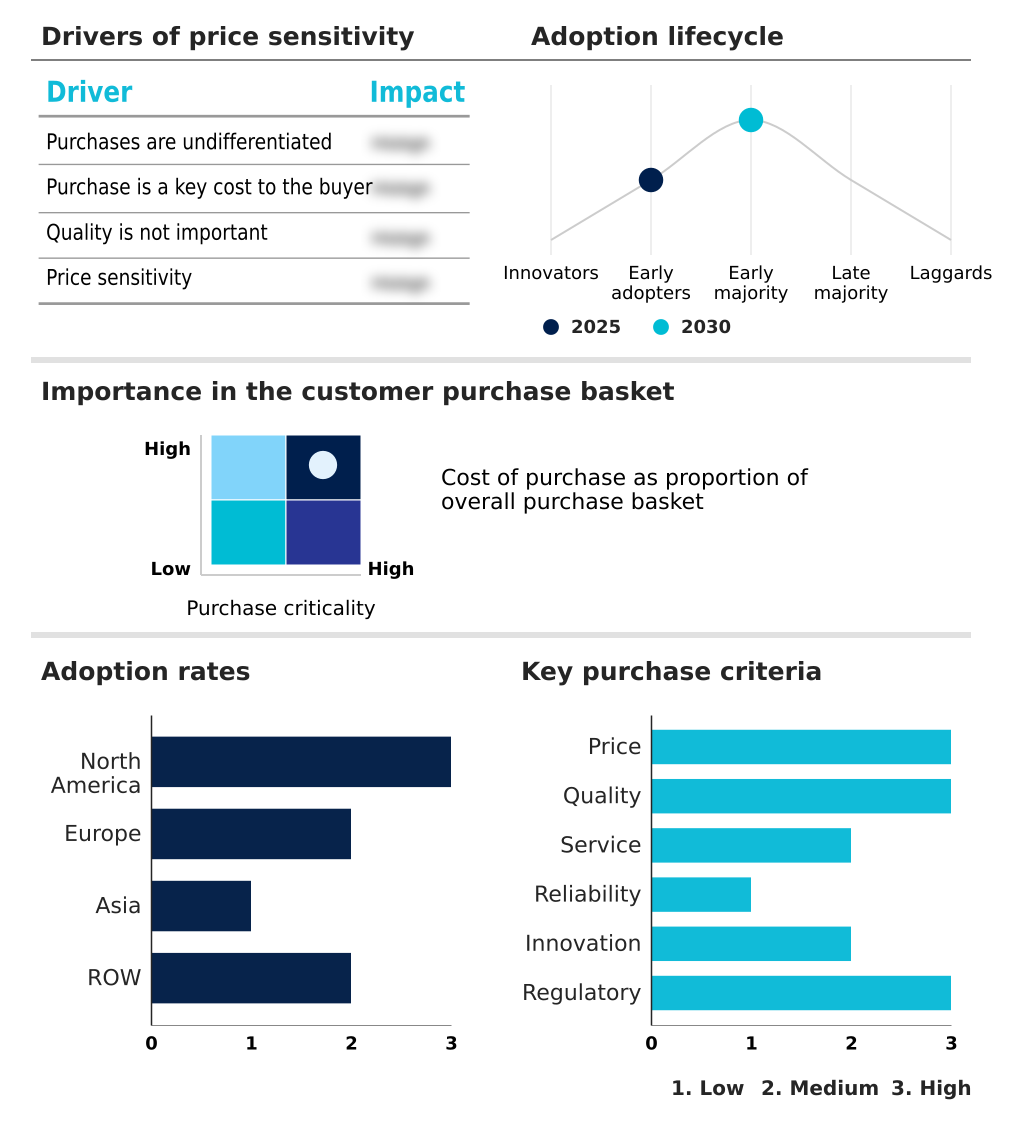

The epidermal growth factor receptor (egfr) inhibitors market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the epidermal growth factor receptor (egfr) inhibitors market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Epidermal Growth Factor Receptor (EGFR) Inhibitors Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, epidermal growth factor receptor (egfr) inhibitors market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amgen Inc. - Delivering human therapeutics focused on mutation-driven tumor signaling pathways through targeted oncology research programs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amgen Inc.

- AstraZeneca Plc

- Boehringer Ingelheim GmbH

- Bristol Myers Squibb Co.

- Checkpoint Therapeutics Inc.

- Eli Lilly and Co.

- F. Hoffmann La Roche Ltd.

- Hansoh Pharmaceutical Group Co. Ltd.

- Hutchison China Meditech Ltd.

- Jiangsu Hengrui Pharmaceuticals Co. Ltd.

- Johnson and Johnson Services

- Lutris Pharma

- Merus N.V.

- Otsuka Holdings Co. Ltd.

- Pfizer Inc.

- Pierre Fabre SA

- Puma Biotechnology Inc.

- Takeda Pharmaceutical Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Epidermal growth factor receptor (egfr) inhibitors market

- In August, 2024, Johnson and Johnson Inc received regulatory approval for the combination of Rybrevant and lazertinib, offering a new first-line chemotherapy-free option for patients with common EGFR mutations.

- In December, 2024, AstraZeneca received European Commission approval for Tagrisso for use in patients with unresectable stage III EGFR-mutated non-small cell lung cancer following chemoradiotherapy.

- In January, 2025, HUTCHMED received acceptance and priority review from China's National Medical Products Administration for the combination of ORPATHYS and TAGRISSO for certain types of resistant lung cancer.

- In April, 2025, Johnson and Johnson obtained European Commission approval for its subcutaneous formulation of Rybrevant in combination with Lazcluze for the first-line treatment of advanced EGFR-mutated non-small cell lung cancer.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Epidermal Growth Factor Receptor (EGFR) Inhibitors Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 10.7% |

| Market growth 2026-2030 | USD 11937.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Indonesia, Thailand, Brazil, Saudi Arabia, UAE, Turkey, Argentina, Colombia, South Africa and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Epidermal Growth Factor Receptor (EGFR) Inhibitors market is in a state of continuous evolution, driven by the clinical need to address acquired resistance to existing therapies. The development pipeline is rich with next-generation inhibitors, including advanced tyrosine kinase inhibitors and monoclonal antibodies, designed to target specific resistance pathways like the c797s mutation.

- A primary focus is on creating antibody-drug conjugates and bispecific antibody platforms that offer novel mechanisms of action. Boardroom-level decisions are increasingly centered on allocating R&D funding toward therapies that demonstrate significant blood-brain barrier penetration to treat challenging conditions like leptomeningeal disease. Clinical trials incorporating genomic profiling have demonstrated a 25% higher success rate in patient stratification.

- The use of companion diagnostics and liquid biopsies is now standard for guiding first-line treatment in non-small cell lung cancer and managing metastatic disease. The shift toward subcutaneous delivery from intravenous administration is also redefining patient care models by enhancing convenience and reducing healthcare system burden, thereby improving patient-reported outcomes.

What are the Key Data Covered in this Epidermal Growth Factor Receptor (EGFR) Inhibitors Market Research and Growth Report?

-

What is the expected growth of the Epidermal Growth Factor Receptor (EGFR) Inhibitors Market between 2026 and 2030?

-

USD 11.94 billion, at a CAGR of 10.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Indication (Lung cancer, Colorectal cancer, Breast cancer, and Others), Distribution Channel (Retail pharmacies, Hospital pharmacies, and Online pharmacies), Drug Class (Small molecule TKIs, and Monoclonal antibodies) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Advancements in combination therapies and regulatory approvals, Resistance mechanisms and need for next generation molecules

-

-

Who are the major players in the Epidermal Growth Factor Receptor (EGFR) Inhibitors Market?

-

Amgen Inc., AstraZeneca Plc, Boehringer Ingelheim GmbH, Bristol Myers Squibb Co., Checkpoint Therapeutics Inc., Eli Lilly and Co., F. Hoffmann La Roche Ltd., Hansoh Pharmaceutical Group Co. Ltd., Hutchison China Meditech Ltd., Jiangsu Hengrui Pharmaceuticals Co. Ltd., Johnson and Johnson Services, Lutris Pharma, Merus N.V., Otsuka Holdings Co. Ltd., Pfizer Inc., Pierre Fabre SA, Puma Biotechnology Inc. and Takeda Pharmaceutical Ltd.

-

Market Research Insights

- The market's dynamics are shaped by therapeutic innovation aimed at improving patient quality of life and achieving durable response rates. The adoption of subcutaneous delivery methods reduces clinic administration time by over 50% compared to traditional intravenous infusions, minimizing infusion-related reactions.

- Advances in oncology drug development and personalized medicine are propelled by enhanced patient stratification techniques, leading to more effective treatments. The integration of digital diagnostic platforms improves patient identification accuracy for targeted therapies by up to 30%. This shift supports the broader use of chemotherapy-free regimens and oral oncology drugs, which align with current treatment guidelines and improve the patient experience.

- The focus on bioinformatics and non-invasive diagnostics is creating a more efficient and responsive healthcare ecosystem.

We can help! Our analysts can customize this epidermal growth factor receptor (egfr) inhibitors market research report to meet your requirements.

RIA -

RIA -