EV Charger Service Market Size 2025-2029

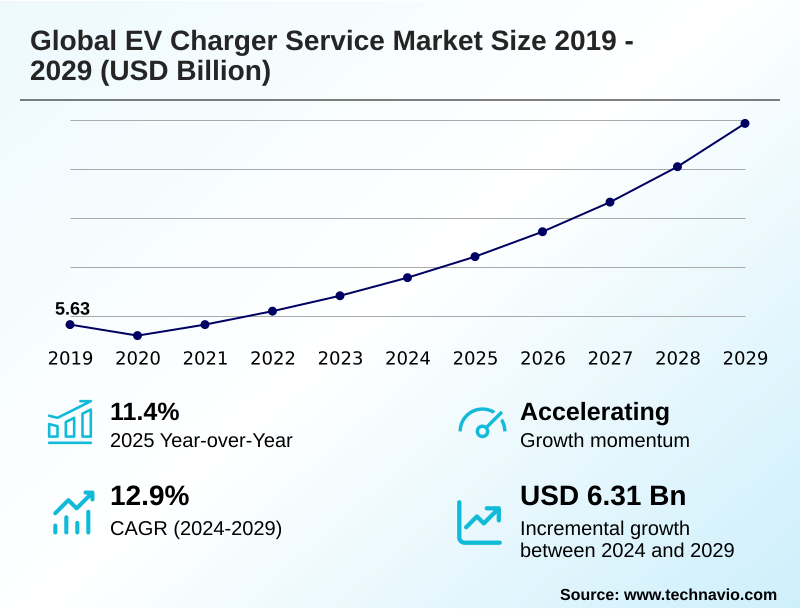

The ev charger service market size is valued to increase by USD 6.31 billion, at a CAGR of 12.9% from 2024 to 2029. Government incentives and subsidies for EV charging infrastructure developments will drive the ev charger service market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 44.3% growth during the forecast period.

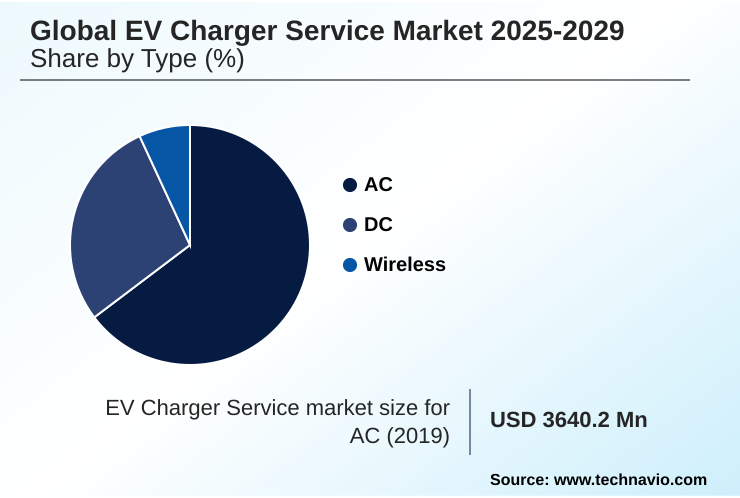

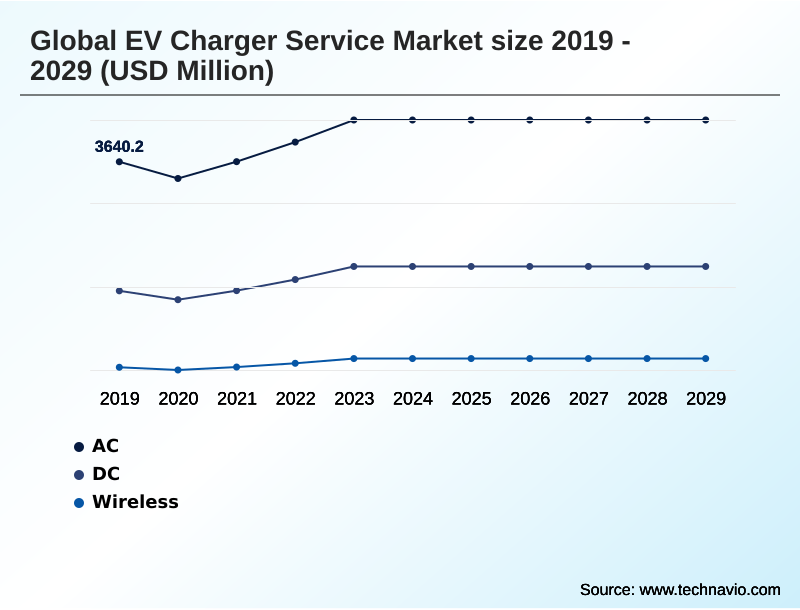

- By Type - AC segment was valued at USD 4.30 billion in 2023

- By Power Output - 10-50 kW segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 8.23 billion

- Market Future Opportunities: USD 6.31 billion

- CAGR from 2024 to 2029 : 12.9%

Market Summary

- The EV charger service market is undergoing a significant transformation, driven by stringent emissions regulations and rising consumer demand for sustainable transport. Growth is propelled by advancements in high-power charging and smart charging technologies that optimize grid integration and energy consumption.

- For instance, commercial fleet operators are increasingly adopting charging-as-a-service models, which bundle hardware, software, and maintenance into a subscription, shifting capital expenditure to operational expenditure. This approach allows them to achieve fleet electrification targets while ensuring high uptime reliability and leveraging energy management systems for cost-effective charging.

- However, the market faces challenges related to interoperability between different charging standards and the high initial cost of deploying extensive public charging networks. The development of turnkey solutions and roaming agreements is becoming crucial to create a seamless user experience.

- Furthermore, integrating renewable energy sources and bidirectional charging capabilities represents a key trend, positioning EV charging as a vital component of a smarter, more resilient energy ecosystem. Progress in battery technology and the expansion of charging hubs will be critical for overcoming range anxiety and accelerating mass-market EV adoption.

What will be the Size of the EV Charger Service Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the EV Charger Service Market Segmented?

The ev charger service industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- AC

- DC

- Wireless

- Power output

- 10-50 kW

- Up to 10 kW

- 50-150 kW

- Above 150 kW

- Installation type

- Residential chargers

- Commercial chargers

- Workplace chargers

- Public chargers

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Type Insights

The ac segment is estimated to witness significant growth during the forecast period.

The EV charger service market is segmented by type, power output, and installation. These segments include innovations in ac charging, dc fast charging, and emerging wireless charging.

Power output ranges from low-kilowatt units to high-power charging systems, while installation types cover residential, commercial, and public applications.

A key dynamic is the need for enhanced charging station management to support the diverse requirements of commercial fleet charging and public charging networks.

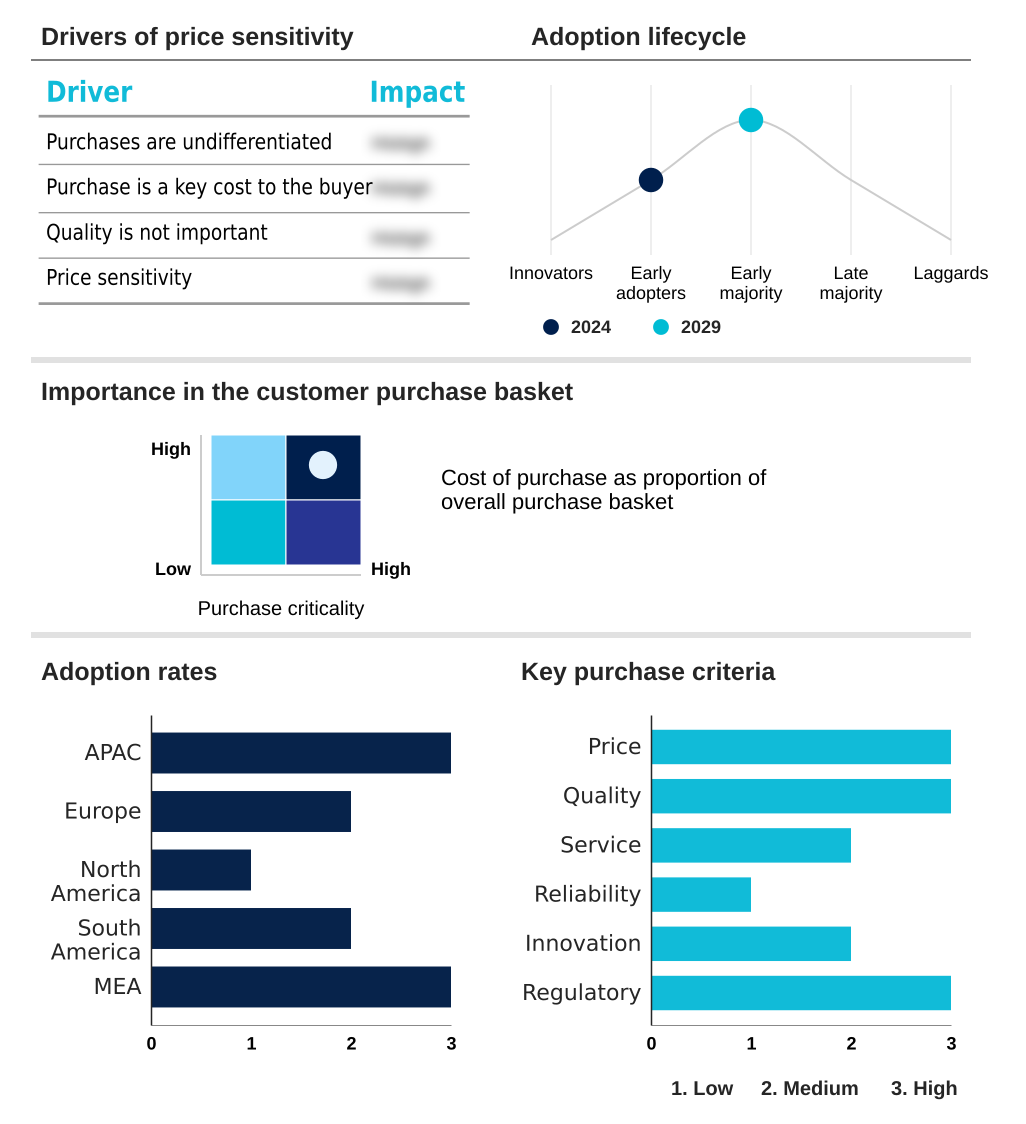

APAC accounts for over 44% of the market's incremental growth, underscoring the importance of regional deployment strategies.

Effective charging-as-a-service models and strong charging infrastructure investment are essential for supporting rising ev adoption rates and advancing emobility services, shaping the competitive landscape.

The AC segment was valued at USD 4.30 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 44.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How EV Charger Service Market Demand is Rising in APAC Get Free Sample

The geographic landscape is characterized by distinct regional dynamics and varying levels of market maturity. APAC contributes 44.3% to the market's incremental growth, driven by massive ev charging infrastructure deployment and fleet electrification initiatives.

In North America, government ev incentives and private investment in a public charging network are accelerating the adoption of the north american charging standard and turnkey solutions.

Europe focuses on stringent regulatory compliance, pushing interoperability standards and roaming agreements to create a unified ecosystem. The expansion of charging hubs and deployment of on-street charging address urban density challenges.

Across all regions, successful ev charging technology deployment depends on effective grid integration and the availability of robust predictive maintenance services to ensure high uptime reliability and manage overall charging station economics.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The successful deployment of a robust charging ecosystem hinges on addressing specific technical and operational challenges. For commercial fleet charging management, optimizing charging schedules through workplace ev charging load balancing is critical to minimize operational costs and avoid placing undue electrical grid strain.

- The proliferation of ac level 2 smart charger technology in residential and commercial settings provides a foundation for this, but ensuring public ev charging station uptime requires sophisticated ev charging station maintenance services. The industry is moving toward predictive maintenance for ev chargers to preempt failures.

- The dc fast charging station cost remains a barrier for widespread deployment, although residential ev charger installation incentives are helping drive home adoption. For long-distance travel, high power charging for long-haul routes is being enabled by the development of megawatt charging for electric trucks.

- Interoperability remains paramount, with advancements in iso 15118 plug and charge and efforts to standardize ev charging interoperability ccs nacs. Concurrently, ev charging network roaming agreements are essential for a seamless user experience.

- Innovations like wireless ev charging pad installation and vehicle to grid pilot programs are creating new service opportunities, while solar powered off grid ev charging and ev battery swapping station logistics address infrastructure gaps in remote areas. Ultimately, managing ev charging station profitability while expanding urban on-street charging solutions will determine long-term success.

What are the key market drivers leading to the rise in the adoption of EV Charger Service Industry?

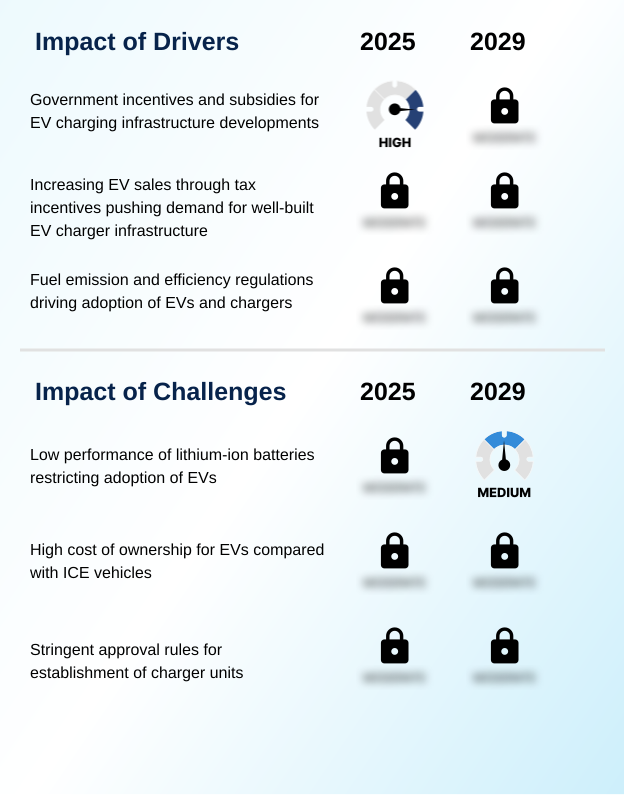

- Government incentives and subsidies for the development of EV charging infrastructure represent a key driver for market growth.

- Government policies and technological advancements are primary drivers of market expansion. Supportive regulatory frameworks, including government ev incentives and utility integration programs, are lowering deployment costs.

- For instance, some tax credit programs cover up to 30% of installation expenses for commercial entities. These financial supports are critical for the build-out of a comprehensive ev charging infrastructure, particularly for highway fast charging.

- At the same time, improvements in ev battery performance and the standardization of protocols like ocpp 2.0.1 are boosting consumer confidence.

- The widespread availability of evse hardware compatible with both the combined charging system and north american charging standard is simplifying the user experience and encouraging investment in the sector, furthering market penetration.

What are the market trends shaping the EV Charger Service Industry?

- A significant market trend is the accelerated installation of DC fast charging stations. This development is crucial for addressing range anxiety and supporting long-distance electric travel.

- Key trends are reshaping the service landscape, with a strong focus on enhancing charging speed and convenience. The development of v2h technology is advancing, with pilot programs demonstrating that bidirectional charging can reduce household energy bills by up to 15%. This innovation transforms residential charging solutions into active grid assets.

- Concurrently, the demand for workplace charging stations is surging; one analysis showed that charging sessions grew by 64% in a single year, far outpacing new hardware installations. This highlights a significant opportunity in charging-as-a-service.

- Progress in battery swapping and the deployment of the megawatt charging system are critical for commercial and fleet depot charging, directly addressing operational downtime and range anxiety solutions for heavy-duty vehicles.

What challenges does the EV Charger Service Industry face during its growth?

- The restricted adoption of EVs due to the performance limitations of lithium-ion batteries presents a key challenge to industry growth.

- Despite strong growth drivers, the market faces significant operational and infrastructural challenges. Achieving consistent uptime reliability across vast networks remains a primary concern, with data indicating that over 20% of public charging attempts fail due to equipment malfunctions or payment system errors. This directly impacts consumer trust in the public charging network.

- The high initial capital required for high-power charging infrastructure, coupled with the long-term uncertainty of charging station economics, also constrains rapid expansion. Furthermore, the electrical grid strain from unmanaged charging events is a growing issue, as peak demand can increase by up to 25% in areas with high EV concentration.

- Addressing these hurdles requires advanced load balancing, robust energy management systems, and a strategic approach to grid integration.

Exclusive Technavio Analysis on Customer Landscape

The ev charger service market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ev charger service market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of EV Charger Service Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ev charger service market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Offerings center on turnkey solutions, providing integrated hardware, advanced energy management systems, and scalable service models to support diverse electric vehicle charging applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Bayerische Motoren Werke AG

- BP Plc

- BYD Co. Ltd.

- ChargePoint Holdings Inc.

- Diebold Nixdorf Incorp.

- Eaton Corp. Plc

- Efacec Power Solutions SGPS SA

- ENGIE SA

- Enphase Energy Inc.

- Gridserve Sustainable Energy Ltd.

- Schaffner Group

- Schneider Electric SE

- Shell plc

- Siemens AG

- SparkCharge Inc.

- SWTCH Energy Inc.

- Tesla Inc.

- TotalEnergies SE

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ev charger service market

- In September 2024, Allego announced the full network rollout of its Plug and Charge technology, based on the OCPP 2.0.1 protocol, which commenced in the fourth quarter of 2024 across its pan-European network.

- In September 2025, the collaboration between Pilot Company, General Motors, and EVgo announced its fast-charging network had expanded to over 200 locations across nearly 40 states, focusing on bridging charging gaps along key travel routes.

- In February 2025, Shell announced its plan to double its charging points at service stations beginning in 2025, aimed at creating fast-charging corridors connecting Argentina with Chile, Uruguay, and Brazil.

- In May 2025, Volkswagen began the rollout of its own branded ultra-fast charging stations in Europe, as part of a broader strategy to build out a comprehensive and reliable charging infrastructure.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled EV Charger Service Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 313 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 12.9% |

| Market growth 2025-2029 | USD 6305.5 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 11.4% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The ev charger service market is defined by a rapid technological evolution centered on enhancing efficiency and user convenience. The shift toward high-power charging is evident, with the megawatt charging system and liquid-cooled chargers enabling faster turnaround for commercial vehicles, a critical factor in fleet electrification strategies.

- Concurrently, advancements in smart charging, load balancing, and demand-response programs are crucial for mitigating electrical grid strain. The adoption of open standards like ocpp 2.0.1 and the mandated iso 15118 for plug and charge functionality are streamlining the charging session and fostering interoperability across networks through roaming agreements.

- For service providers, ensuring uptime reliability through predictive maintenance and offering flexible charging-as-a-service models are key differentiators. The development of power modules and battery energy storage system integration at charging hubs facilitates off-grid charging and supports grid integration.

- In residential and commercial spaces, bidirectional charging and v2h technology are transforming EVs into distributed energy assets, supported by turnkey solutions and sophisticated energy management systems. The market is also seeing niche growth in on-street charging and battery swapping, while the convergence of combined charging system and north american charging standard protocols simplifies the ecosystem.

- A critical boardroom focus is the transition to service-based revenue models, where data from evse hardware is leveraged to optimize power output and operational efficiency, reducing costs by over 15% for network operators.

What are the Key Data Covered in this EV Charger Service Market Research and Growth Report?

-

What is the expected growth of the EV Charger Service Market between 2025 and 2029?

-

USD 6.31 billion, at a CAGR of 12.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (AC, DC, Wireless), Power Output (10-50 kW, Up to 10 kW, 50-150 kW, Above 150 kW), Installation Type (Residential chargers, Commercial chargers, Workplace chargers, Public chargers) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Government incentives and subsidies for EV charging infrastructure developments, Low performance of lithium-ion batteries restricting adoption of EVs

-

-

Who are the major players in the EV Charger Service Market?

-

ABB Ltd., Bayerische Motoren Werke AG, BP Plc, BYD Co. Ltd., ChargePoint Holdings Inc., Diebold Nixdorf Incorp., Eaton Corp. Plc, Efacec Power Solutions SGPS SA, ENGIE SA, Enphase Energy Inc., Gridserve Sustainable Energy Ltd., Schaffner Group, Schneider Electric SE, Shell plc, Siemens AG, SparkCharge Inc., SWTCH Energy Inc., Tesla Inc. and TotalEnergies SE

-

Market Research Insights

- The market's momentum is defined by strategic charging network expansion and a focus on interoperability standards to enhance user experience. The demand for workplace charging stations is surging, with session volume growing 64% year-over-year, significantly outpacing new port installations at just 22%. This gap highlights a major opportunity in emobility services and commercial fleet charging.

- Concurrently, utility integration programs are becoming more sophisticated, supporting renewable energy integration and mitigating the grid impact of EV charging. These initiatives are critical as public charging network utilization rates have increased by over 25%, driven by rising EV adoption rates.

- Fleet depot charging and destination charging are evolving with smart technology to manage charging station economics, while government EV incentives continue to spur charging infrastructure investment and broader market development.

We can help! Our analysts can customize this ev charger service market research report to meet your requirements.

RIA -

RIA -