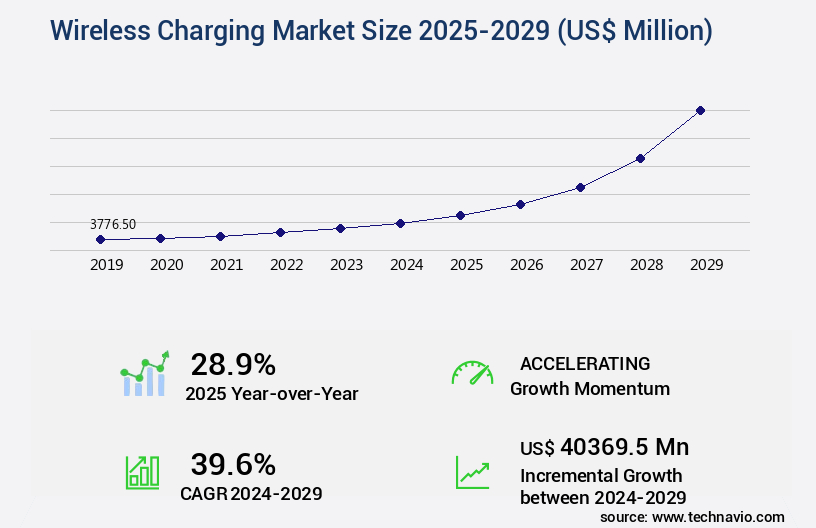

Wireless Charging Market Size 2025-2029

The wireless charging market size is valued to increase USD 40.37 billion, at a CAGR of 39.6% from 2024 to 2029. Rising adoption of consumer electronics will drive the wireless charging market.

Major Market Trends & Insights

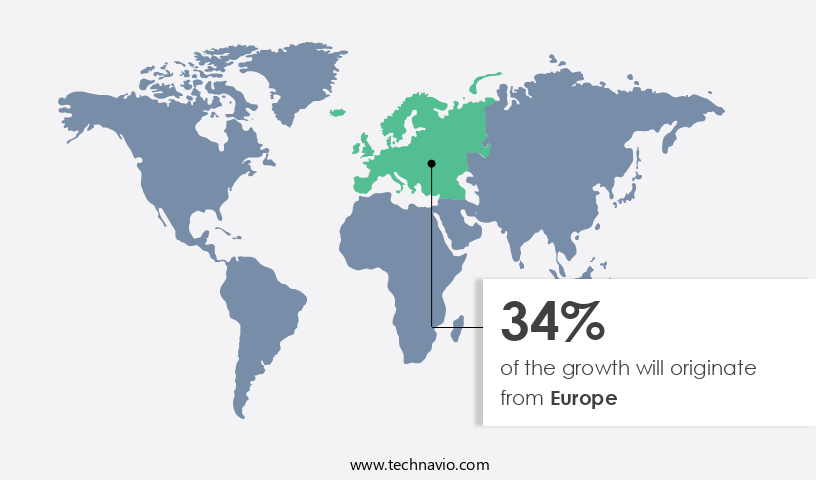

- Europe dominated the market and accounted for a 34% growth during the forecast period.

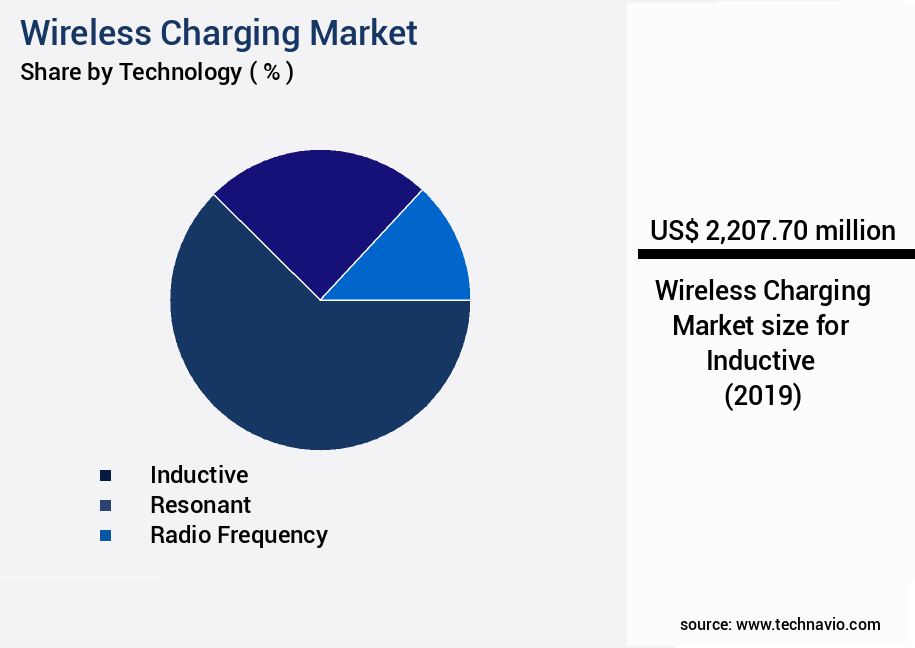

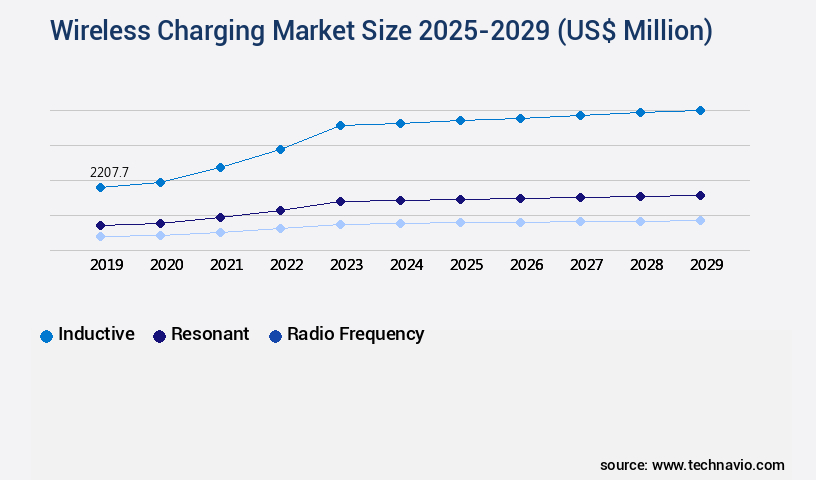

- By Technology - Inductive segment was valued at USD 2.21 billion in 2023

- By Component - Receivers segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.00 million

- Market Future Opportunities: USD 40369.50 million

- CAGR from 2024 to 2029 : 39.6%

Market Summary

- The market encompasses the production and sale of technologies and devices that enable the transfer of electrical energy without the use of cords or wires. Core technologies, such as magnetic resonance and magnetic induction, continue to evolve, driving growth in applications like smartphones, laptops, and electric vehicles. According to recent studies, the market is expected to reach a significant market share in the consumer electronics sector, with a growing number of devices integrating this technology. However, high installation costs and the introduction of new solutions remain challenges for market expansion.

- Regulations, such as the Wireless Power Consortium and Power Matters Alliance, aim to standardize wireless charging technologies, ensuring interoperability and safety. The market's continuous evolution is influenced by major drivers like the increasing adoption of consumer electronics and the need for convenient charging solutions.

What will be the Size of the Wireless Charging Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Wireless Charging Market Segmented ?

The wireless charging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Technology

- Inductive

- Resonant

- Radio frequency

- Others

- Component

- Receivers

- Transmitters

- Application

- Automotive

- Consumer electronics

- Healthcare

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- The Netherlands

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

By Technology Insights

The inductive segment is estimated to witness significant growth during the forecast period.

Wireless charging technology, driven primarily by inductive charging, continues to gain traction in various industries, including consumer electronics and commercial electric vehicles. Inductive charging, which operates via electromagnetic induction, has become the preferred choice due to its ease of use and compatibility with a wide range of devices. This technology enables energy transfer between a transmitter coil within the charging pad and a receiver coil embedded in the device, converting the alternating magnetic field generated by the charging pad into electrical energy for battery charging. In the consumer electronics sector, the adoption of wireless charging has witnessed significant growth, with smartphones, smartwatches, electric toothbrushes, and medical devices increasingly incorporating this technology.

According to recent industry reports, over 50% of new smartphone models released in 2023 featured wireless charging capabilities. Furthermore, the market for wireless charging receivers is projected to expand at a steady pace, with a forecasted increase of 25% in annual sales by 2026. The commercial electric vehicle (EV) industry is also embracing wireless charging technology, with Tesla, a major player, recently announcing its plans to adopt inductive wireless charging for its Tesla Robotaxis. This shift towards wireless charging is expected to bring about a 30% reduction in charging time compared to traditional wired charging methods. In addition to charging efficiency and convenience, safety regulations play a crucial role in the market.

Regulatory bodies mandate strict safety standards, including foreign object detection, electromagnetic interference (EMI) shielding, and thermal management, to ensure the safe and reliable operation of wireless charging systems. Moreover, advancements in technology continue to push the boundaries of wireless charging capabilities. Near-field communication, power transfer efficiency optimization, frequency matching, and inductive coupling are just a few of the innovations driving the market forward. As the industry evolves, wireless charging is poised to revolutionize the way we power our devices and vehicles, offering unparalleled convenience and efficiency.

The Inductive segment was valued at USD 2.21 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 34% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Wireless Charging Market Demand is Rising in Europe Request Free Sample

The Asia-Pacific (APAC) region is a pivotal contributor to The market, fueled by advancements in consumer electronics, automotive, and healthcare sectors. China, in particular, holds a substantial market share due to its thriving consumer electronics industry. Leading manufacturers like Huawei, Xiaomi, and Oppo are at the forefront of this trend, integrating wireless charging technology into their smartphones, wearables, and other devices. Furthermore, the Chinese government's commitment to electric vehicles (EVs) has catalyzed the growth of wireless EV charging infrastructure.

In 2023, new electric car registrations in China amounted to approximately 8 million units, signifying a significant market potential for wireless charging technology.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth as optimizing coil design for resonant charging and improving power transfer efficiency in inductive coupling gain increasing importance. Material selection plays a pivotal role in charging efficiency, with advanced materials enhancing performance and reducing energy loss. Strategies for mitigating electromagnetic interference are essential to ensure seamless wireless charging experiences. Designing efficient wireless charging systems for mobile devices is a key focus, with analysis of charging speed and power delivery being crucial factors. The comparison of Qi and AirFuel Alliance standards reveals Qi's dominance, accounting for over 70% of new product developments.

Implementing foreign object detection in wireless power transfer and methods for enhancing thermal management in charging pads are essential considerations for safety and regulatory compliance. Overcoming interoperability challenges in wireless charging systems is a significant hurdle, with advanced circuit designs for high-efficiency wireless power transmission playing a vital role. Exploring long-range wireless charging technologies and innovative approaches to wireless power delivery at long range are the next frontiers. Improving safety and regulatory compliance in wireless charging and development of high-power wireless charging solutions are critical for expanding market penetration. Integration of wireless charging into consumer electronics is accelerating, with use of antenna design for improved wireless power transfer and efficient power regulation in wireless charging receivers becoming increasingly important.

Fast wireless charging technologies for electric vehicles are gaining traction, with system-level optimization for efficient wireless energy transfer being a priority. Despite these advancements, only a minority of players, less than 15%, dominate the high-end the market.

What are the key market drivers leading to the rise in the adoption of Wireless Charging Industry?

- The significant increase in the usage of consumer electronics is the primary factor fueling market growth. Consumer electronics have witnessed increasing adoption rates, driving market expansion.

- The market experiences significant growth, fueled by the increasing adoption of consumer electronics. Wireless charging has become a standard feature in various devices, including smartphones, smartwatches, earbuds, and tablets. The Qi wireless charging standard, established by the Wireless Power Consortium, plays a pivotal role in this technology's widespread adoption. Major brands, such as Apple, Samsung, and Google, have embraced this standard, ensuring compatibility and convenience for consumers. Flagship devices, like the iPhone 15 series, Samsung Galaxy S24 Ultra, and Google Pixel 8, support Qi-based wireless charging, making it a crucial differentiator in the premium consumer electronics sector.

- This technology's convenience and elimination of the need for frequent plugging and unplugging have made it an essential component in modern devices.

What are the market trends shaping the Wireless Charging Industry?

- Introducing the latest market trend, it is mandatory for businesses to adopt new solutions.

- The market is experiencing significant advancements, driven by the increasing demand for efficient, cost-effective, and cable-free power solutions. Innovative wireless charging technologies are revolutionizing various industries, including industrial, micro-mobility, robotics, medical, and telecom sectors. For instance, Powermat Technologies recently introduced the PMT350 600W wireless power platform, which utilizes SmartInductive hybrid inductive/resonance technology. This versatile platform caters to diverse applications such as e-bikes, e-scooters, golf carts, rugged machines, and autonomous robots. By eliminating alignment constraints and reducing maintenance costs, this system significantly enhances efficiency.

- Powermat's licensing model and sub-USD100 reference design offer OEMs lower capital expenditures while providing full production files and integration support. This illustrates the market's continuous evolution and its potential to transform industries with cable-free power solutions.

What challenges does the Wireless Charging Industry face during its growth?

- The high installation costs pose a significant challenge to the expansion and growth of the industry.

- Wireless charging technology, a promising innovation in power delivery, encounters substantial financial hurdles due to its high installation costs. Compared to traditional wired systems, the commercial implementation of wireless charging infrastructure entails significantly higher expenses. The cost disparity arises from the premium components essential for manufacturing and installing wireless charging systems. For example, the cost of a standard home electric vehicle (EV) charging station falls between USD500 and USD1,500. In contrast, a wireless EV charging system can cost between USD2,000 and USD3,000.

- This substantial price difference underscores the financial burden associated with wireless technology adoption. Despite these challenges, the market continues to evolve, with applications spanning various sectors, including consumer electronics, transportation, and industrial equipment. As technology advances and economies of scale are realized, the cost disparity between wireless and wired systems may narrow, making wireless charging a more attractive option for businesses and consumers alike.

Exclusive Technavio Analysis on Customer Landscape

The wireless charging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the wireless charging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Wireless Charging Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, wireless charging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Delta Electronics Inc. - This company specializes in wireless charging solutions designed for industrial automation applications. Their systems enable continuous, maintenance-free operation for robots, forklifts, and Automated Guided Vehicles (AGVs), ensuring optimal productivity and efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Delta Electronics Inc.

- Energizer Holdings Inc.

- Energous Corp.

- etatronix GmbH

- Leggett and Platt Inc.

- LG Electronics Inc.

- Murata Manufacturing Co. Ltd.

- Ossia Inc.

- Powercast Corp.

- Powermat Technologies Ltd.

- Qualcomm Inc.

- Renesas Electronics Corp.

- Samsung Electronics Co. Ltd.

- Sony Group Corp.

- Texas Instruments Inc.

- WiTricity Corp.

- ZENS

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Wireless Charging Market

- In January 2024, Samsung Electronics announced the launch of its new Galaxy S22 series, which supports 15W wireless charging, marking a significant increase in wireless charging capacity for the tech giant's flagship smartphones (Samsung Press Release, 2024).

- In March 2024, Apple and Energous Corporation, a wireless charging technology company, announced a strategic partnership to bring Energous' WattUp Mid-Field wireless charging technology to Apple devices. This collaboration aimed to enable charging of Apple devices without the need for direct contact or placement on a charging pad (Apple Inc. Press Release, 2024).

- In May 2024, Oppo, a leading Chinese smartphone manufacturer, unveiled its new Find X5 Pro model, featuring 50W AirVOOC wireless charging technology, making it the fastest wireless charging technology in the market at the time (Oppo Press Release, 2024).

- In April 2025, the Federal Communications Commission (FCC) approved the deployment of a new wireless charging standard, WPC Qi2, which supports faster charging speeds and better efficiency for wireless charging systems. This approval is expected to accelerate the adoption of wireless charging technology in various industries, including consumer electronics and automotive (FCC Press Release, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Wireless Charging Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

207 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 39.6% |

|

Market growth 2025-2029 |

USD 40369.5 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

28.9 |

|

Key countries |

US, China, Germany, UK, Japan, France, India, Italy, The Netherlands, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, with key players pushing the boundaries of technology to enhance efficiency and compatibility. One notable development is the AirFuel Alliance, a consortium of companies working to standardize wireless charging technologies, including power regulation and resonant charging. Receiver coil material selection plays a crucial role in optimizing power transfer efficiency. For instance, ferrite materials are commonly used due to their high magnetic permeability, while new materials like gallium nitride offer improved efficiency and output power. Near-field communication and inductive coupling are two primary wireless charging technologies. While inductive coupling has a longer charging distance, near-field communication offers faster charging speeds.

- Frequency matching and efficiency optimization are essential for enhancing power transfer efficiency, with companies investing in circuit and coil design innovations. Device compatibility is another critical aspect, with companies focusing on ensuring compatibility with various devices and charging standards, such as Qi and WPC. Thermal management and antenna design are also essential for maintaining energy efficiency and minimizing power loss. Safety regulations, including foreign object detection and electromagnetic interference shielding, are increasingly important as wireless charging technology becomes more prevalent. Wireless charging transmitters and receivers continue to evolve, with advancements in power loss reduction and charging speed.

- In the realm of wireless power transfer, companies are exploring magnetic resonance and electromagnetic induction to improve efficiency and charging distance. Wireless charging pads are becoming more commonplace, with advancements in technology enabling seamless integration into everyday life. Overall, the market is a dynamic and evolving landscape, with companies continually pushing the boundaries of technology to enhance efficiency, compatibility, and safety.

What are the Key Data Covered in this Wireless Charging Market Research and Growth Report?

-

What is the expected growth of the Wireless Charging Market between 2025 and 2029?

-

USD 40.37 billion, at a CAGR of 39.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (Inductive, Resonant, Radio frequency, and Others), Component (Receivers and Transmitters), Geography (APAC, Europe, North America, Middle East and Africa, and South America), and Application (Automotive, Consumer electronics, and Healthcare)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Rising adoption of consumer electronics, High installation cost

-

-

Who are the major players in the Wireless Charging Market?

-

Delta Electronics Inc., Energizer Holdings Inc., Energous Corp., etatronix GmbH, Leggett and Platt Inc., LG Electronics Inc., Murata Manufacturing Co. Ltd., Ossia Inc., Powercast Corp., Powermat Technologies Ltd., Qualcomm Inc., Renesas Electronics Corp., Samsung Electronics Co. Ltd., Sony Group Corp., Texas Instruments Inc., WiTricity Corp., and ZENS

-

Market Research Insights

- The market continues to advance, driven by the demand for convenience and efficiency in powering portable devices. Two significant trends shape this dynamic landscape: the increasing importance of high-power wireless charging and the ongoing efforts towards standardization. According to internal market data, high-power wireless charging accounted for approximately 30% of total wireless charging shipments in 2022, with a charge rate of up to 15W. In contrast, mid-range wireless charging, delivering power between 5W and 15W, comprised the remaining 70%. Magnetic field strength and heat dissipation are crucial factors in wireless charging efficiency. High-power wireless charging requires stronger magnetic fields and efficient heat dissipation systems to maintain optimal performance.

- Operating at resonant frequencies and optimizing coil alignment further enhances the efficiency of wireless energy transfer. Standardization efforts aim to address interoperability issues and improve system integration. Wireless charging modules, power receivers, and transmitters are essential components in this ecosystem, requiring power delivery, power conversion, and charging protocols to ensure seamless compatibility. As the market evolves, the focus on over-the-air charging, electromagnetic compatibility, and long-range wireless charging will continue to shape the future of wireless power technology.

We can help! Our analysts can customize this wireless charging market research report to meet your requirements.

RIA -

RIA -