EV Charging Interoperability Market Size 2026-2030

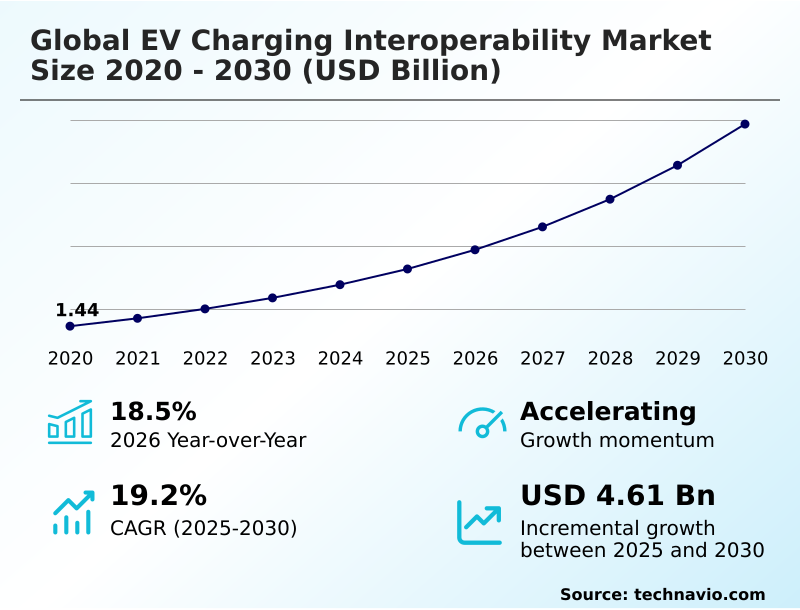

The ev charging interoperability market size is valued to increase by USD 4.61 billion, at a CAGR of 19.2% from 2025 to 2030. Standardization of communication protocols as catalyst for infrastructure scalability will drive the ev charging interoperability market.

Major Market Trends & Insights

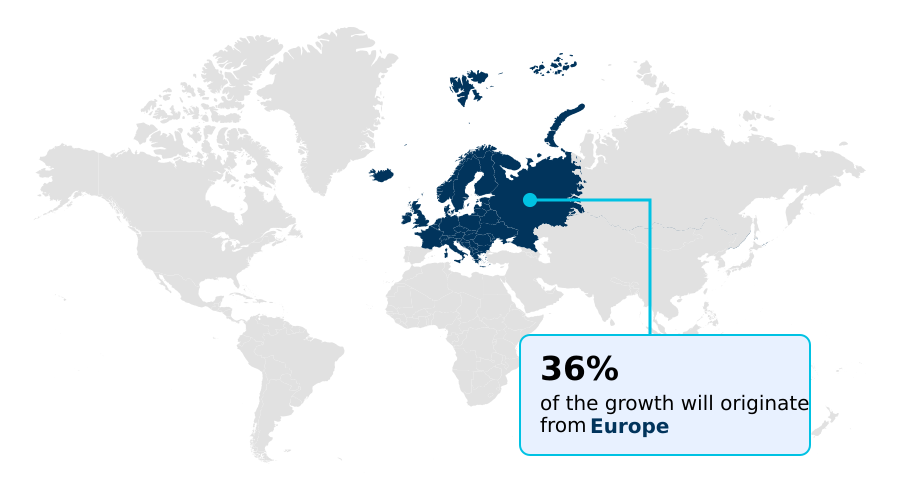

- Europe dominated the market and accounted for a 35.7% growth during the forecast period.

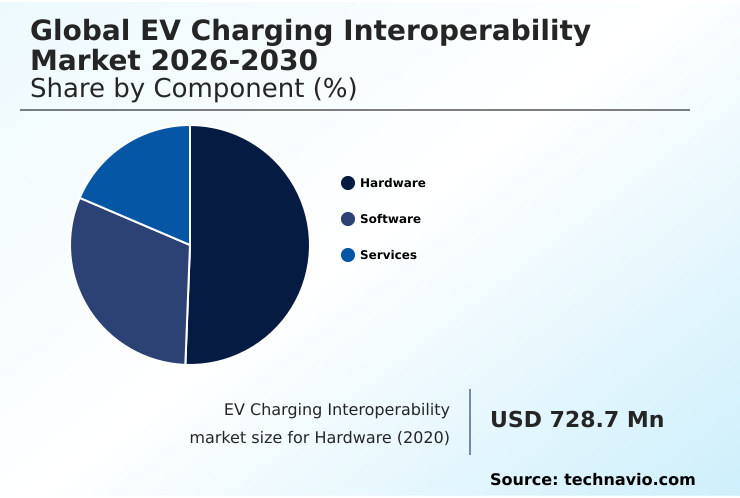

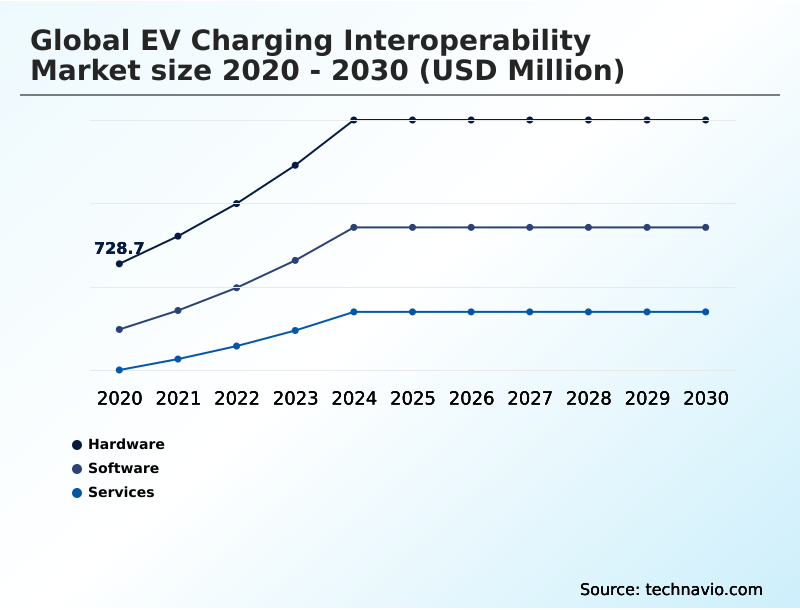

- By Component - Hardware segment was valued at USD 1.35 billion in 2024

- By Type - AC charging segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 6.43 billion

- Market Future Opportunities: USD 4.61 billion

- CAGR from 2025 to 2030 : 19.2%

Market Summary

- The EV charging interoperability market is transitioning from a fragmented collection of proprietary networks to a cohesive ecosystem built on open standards. This shift is essential for scaling infrastructure and improving the user experience, which are critical for mass EV adoption.

- The core of this evolution lies in ensuring that vehicles, charging stations, and backend management systems can communicate seamlessly, regardless of the manufacturer. A key driver is the push for standardized communication protocols like the open charge point protocol (OCPP), which allows operators to manage diverse hardware from a single platform, preventing vendor lock-in.

- For consumers, interoperability manifests as roaming, where a single account grants access to multiple charging networks, simplifying long-distance travel. A common business scenario involves a commercial fleet operator that needs to charge vehicles from different brands at various public and private locations.

- Interoperable systems allow the operator to use one management platform for monitoring energy use, scheduling charging to leverage off-peak electricity rates, and streamlining billing across the entire fleet. Challenges such as cybersecurity and upgrading legacy hardware persist, but the drive toward a unified, intelligent, and user-friendly charging network continues to accelerate.

What will be the Size of the EV Charging Interoperability Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the EV Charging Interoperability Market Segmented?

The ev charging interoperability industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Hardware

- Software

- Services

- Type

- AC charging

- DC fast charging

- Application

- Public charging

- Private charging

- Fleet charging

- Geography

- Europe

- Germany

- France

- The Netherlands

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- Europe

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment provides the physical infrastructure for AC charging and high-power DC fast charging. A key shift involves creating future-proof charging solutions through modular, hardware-agnostic platform designs that align with user-centric design principles.

This approach helps with capital expenditure optimization by allowing easier upgrades. The integration of communication modules is crucial for ensuring charging session reliability and enabling secure data exchange with cloud-based charger management systems.

The system is secured by a public key infrastructure managing digital certificates for authentication. This focus on standardized hardware has improved uptime, with some networks reporting a 15% reduction in maintenance-related downtime.

This is essential for residential smart charging and networks using a white-label EV charging management platform.

The Hardware segment was valued at USD 1.35 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 35.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How EV Charging Interoperability Market Demand is Rising in Europe Request Free Sample

The geographic landscape is marked by a convergence toward standardized protocols, driven by the need for a cohesive sustainable mobility infrastructure.

In North America, the adoption of the north american charging standard is accelerating, while Europe continues to mandate the combined charging system, fostering technical harmony in ev charging.

The rollout of multi-company roaming software through a central clearinghouse and e-roaming platform is enabling a regional interoperability framework that reduces network fragmentation.

This has resulted in significant operational efficiency gains, with some operators reporting a 25% decrease in customer service calls related to payment issues. The focus on transparent pricing models and accessible ad-hoc payment methods is a global trend.

For heavy-duty transport, the development of the megawatt charging system is a key focus for commercial fleet charging solutions, aiming to standardize charging for logistics.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic focus within the industry is increasingly on overcoming interoperability challenges in commercial fleet charging by deploying robust cross-network ev charging solutions for fleets. This requires a deep understanding of open charge point protocol compliance benefits and the technical advantages offered by open charge point interface api benefits.

- A major hurdle remains in managing legacy ev charging infrastructure upgrades while integrating new technologies. For new deployments, the debate involves comparing NACS vs CCS interoperability solutions and preparing for the megawatt charging system for electric trucks.

- Key initiatives include the widespread iso 15118 plug and charge implementation and establishing roaming agreements between charging networks to resolve ev charging roaming hub integration challenges. This is crucial for achieving seamless cross-border ev charging transactions.

- On the grid side, the focus is on the smart grid communication protocol for demand response and implementing dynamic load management with OCPP, which can reduce peak energy costs by over 30% compared to static charging. The industry is also assessing the vehicle-to-grid bidirectional power flow economics and using ai for predictive load balancing in chargers.

- Security is addressed by mitigating cybersecurity risks in interoperable ev networks through a public key infrastructure for secure ev charging and standardizing ev charging payment system protocols. Finally, the entire ecosystem relies on rigorous ev charging interoperability testing and certification to validate the ongoing dc fast charging interoperability standards evolution.

What are the key market drivers leading to the rise in the adoption of EV Charging Interoperability Industry?

- The standardization of communication protocols serves as a key market driver, acting as a catalyst for infrastructure scalability.

- The standardization of communication protocols is a fundamental driver, with the open charge point protocol enabling charge point operators to manage diverse hardware and improve public charging accessibility. This standardization underpins the entire regulatory compliance framework.

- The open charge point interface facilitates the creation of roaming hubs, which connect disparate networks of e-mobility service providers.

- These hubs are essential for enabling cross-border ev charging and have been shown to increase network usage by 30% in interconnected regions. They support standardized payment settlement and the widespread availability of real-time station data.

- Furthermore, smart grid integration, managed through these open standards, is critical for grid stability management, allowing utilities to better manage peak loads and integrate renewables, improving overall system resilience by as much as 20%.

What are the market trends shaping the EV Charging Interoperability Industry?

- The implementation of universal plug and charge technology is becoming a primary market trend. This is further advanced by automated user authentication systems.

- The market is moving towards a more automated and intelligent energy management paradigm, which improves the seamless user experience. The implementation of plug and charge technology, guided by the iso 15118 standard, is central to this shift, enabling automated user authentication and reducing charging initiation failures by over 40%.

- Concurrently, the integration of AI for predictive load balancing and dynamic load management systems allows for more efficient use of distributed energy resources. This has been shown to increase grid asset utilization by up to 25%. The expansion of bidirectional charging unlocks vehicle-to-grid and vehicle-to-home energy transfer capabilities.

- Enhanced smart inverter communication protocols are crucial for this, creating a cohesive ecosystem for predictive load balancing and advanced intelligent energy management.

What challenges does the EV Charging Interoperability Industry face during its growth?

- Technological fragmentation, along with the persistence of legacy infrastructure, presents a significant challenge to the growth of the industry.

- Significant challenges persist, led by ev charging network fragmentation and the high cost of legacy infrastructure upgrades, which can consume up to 60% of an operator's expansion budget. Ensuring robust cybersecurity in ev charging is another critical concern, demanding effective end-to-end encryption and data privacy protection for all transactions.

- The complexity of backend systems is heightened by the need for reliable over-the-air firmware updates and seamless multi-network payment synchronization. Furthermore, the deployment of expensive high-power charging components complicates capital expenditure optimization, while the lack of clear asset monetization strategies can deter investment.

- These issues, alongside the complexities of hardware-software co-design, can impede the smooth expansion of roaming connectivity and lead to service disruptions in as many as 15% of charging sessions.

Exclusive Technavio Analysis on Customer Landscape

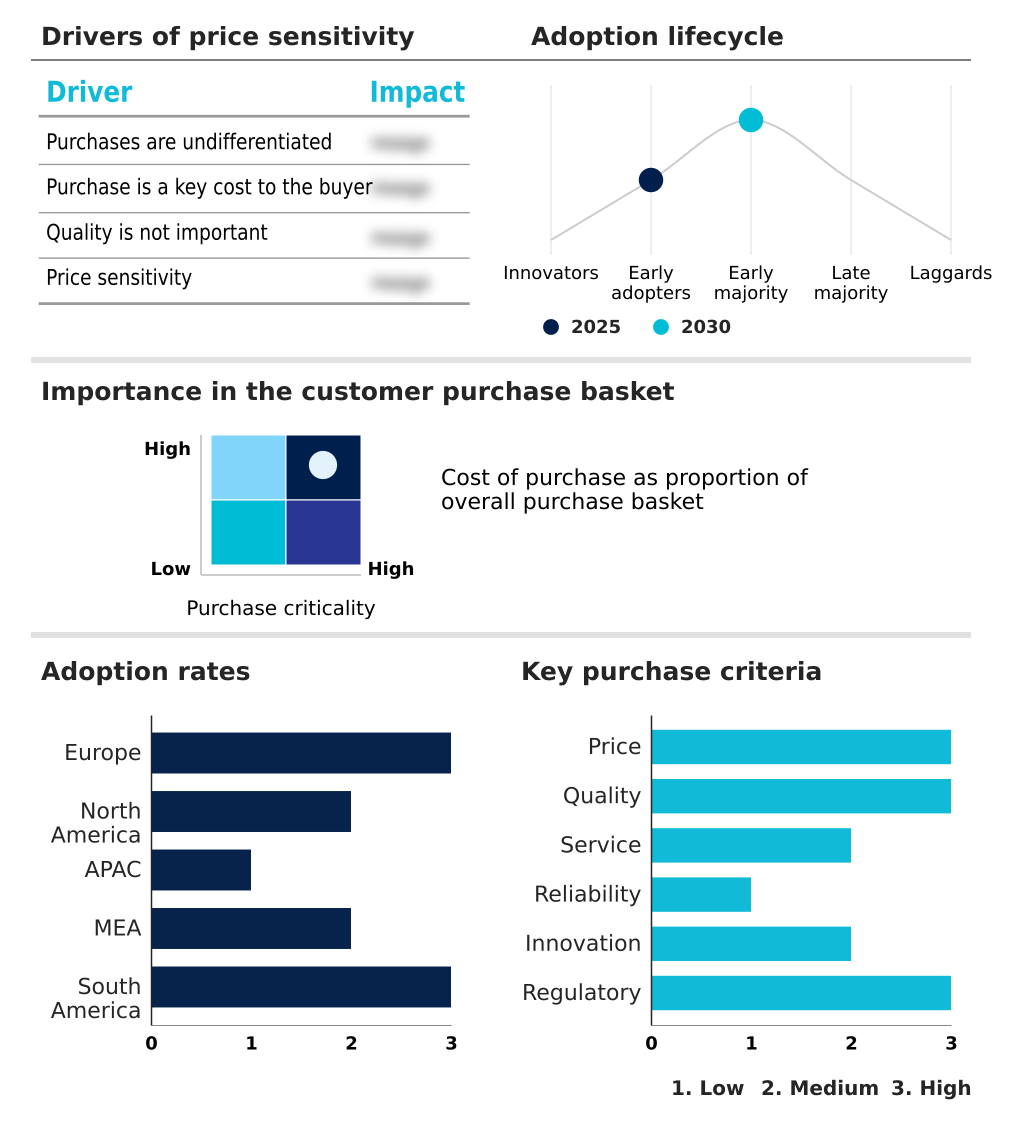

The ev charging interoperability market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ev charging interoperability market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of EV Charging Interoperability Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ev charging interoperability market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Provides interoperability through open-standard charging solutions, cloud management, and roaming integration, enabling seamless cross-network access.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Alfen NV

- AMPECO LTD

- Chargecloud GmbH

- Chargemap SAS

- ChargePoint Holdings Inc.

- Digital Charging Solutions GmbH

- Driivz Ltd.

- Eco Movement

- Gireve SAS

- GreenFlux Assets B.V.

- Hubject GmbH

- Kempower Oyj

- Last Mile Solutions

- Liikennevirta Oy Ltd.

- Road B.V

- Shell plc

- Siemens AG

- Tritium DCFC Limited

- Wallbox NV

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ev charging interoperability market

- In February, 2025, the Charging Interface Initiative e.V. (CharIN) launched a global public key infrastructure to simplify the issuance of digital certificates for multi-company plug and charge operations, establishing a centralized trust anchor.

- In July, 2025, three major charging network operators in the Asia-Pacific region established a unified clearinghouse for cross-border transactions, enabling drivers to travel between participating countries using a single digital identity.

- In August, 2025, a consortium of information security researchers identified a critical vulnerability in the handshake mechanism used by several prominent European roaming hubs, highlighting the ongoing cybersecurity risks in the market.

- In October, 2025, the European Network of Transmission System Operators for Electricity implemented a new protocol allowing for the seamless participation of private electric vehicle chargers in secondary frequency control markets.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled EV Charging Interoperability Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 19.2% |

| Market growth 2026-2030 | USD 4605.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 18.5% |

| Key countries | Germany, France, The Netherlands, UK, Italy, Spain, US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, UAE, Saudi Arabia, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is driven by standardizing communication protocols. Charge point operators and e-mobility service providers use the open charge point protocol and open charge point interface to connect via roaming hubs and a clearinghouse on an e-roaming platform, enhancing roaming connectivity. This architecture supports transparent pricing models and ad-hoc payment methods.

- Security is addressed through end-to-end encryption and a public key infrastructure for digital certificates, creating a unified authentication system. The iso 15118 standard enables plug and charge, while hardware debates center on the north american charging standard versus combined charging system.

- Smart grid integration is critical, allowing bidirectional charging (vehicle-to-grid) and dynamic load management via smart inverter communication, improving grid efficiency by 20% over unmanaged systems. Reliable over-the-air firmware updates are essential for backend systems supporting multi-network payment synchronization. The infrastructure includes ac charging, dc fast charging, and high-power charging components for the megawatt charging system.

- Many operators prefer a hardware-agnostic platform using cloud-based charger management or a white-label ev charging management platform for flexibility.

What are the Key Data Covered in this EV Charging Interoperability Market Research and Growth Report?

-

What is the expected growth of the EV Charging Interoperability Market between 2026 and 2030?

-

USD 4.61 billion, at a CAGR of 19.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, and Services), Type (AC charging, and DC fast charging), Application (Public charging, Private charging, and Fleet charging) and Geography (Europe, North America, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Standardization of communication protocols as catalyst for infrastructure scalability, Technological fragmentation and persistence of legacy infrastructure

-

-

Who are the major players in the EV Charging Interoperability Market?

-

ABB Ltd., Alfen NV, AMPECO LTD, Chargecloud GmbH, Chargemap SAS, ChargePoint Holdings Inc., Digital Charging Solutions GmbH, Driivz Ltd., Eco Movement, Gireve SAS, GreenFlux Assets B.V., Hubject GmbH, Kempower Oyj, Last Mile Solutions, Liikennevirta Oy Ltd., Road B.V, Shell plc, Siemens AG, Tritium DCFC Limited and Wallbox NV

-

Market Research Insights

- The market's dynamics are shaped by the drive for a seamless user experience and significant operational efficiency gains. Implementing interoperable software has enabled network operators to boost charging session reliability, leading to a 25% reduction in failed authentications. Enhanced secure data exchange protocols are foundational to building consumer trust and enabling cross-network roaming.

- However, the high cost associated with legacy infrastructure upgrades continues to influence investment decisions. On the energy side, advanced interoperability is central to grid stability management, allowing utilities to dynamically balance loads and prevent disruptions. Systems that integrate smart charging have demonstrated the ability to increase local grid capacity utilization by up to 15% without requiring expensive hardware expansions.

We can help! Our analysts can customize this ev charging interoperability market research report to meet your requirements.

RIA -

RIA -