Farm Management Software Market Size 2024-2028

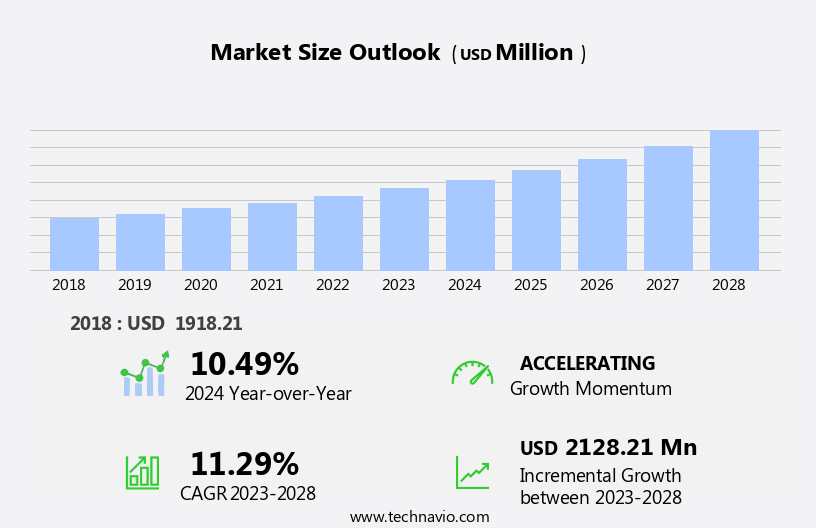

The farm management software market size is forecast to increase by USD 2.13 billion at a CAGR of 11.29% between 2023 and 2028.

- The market is experiencing significant growth, driven by the increasing popularity of precision farming. This approach to agriculture utilizes data-driven insights to optimize crop yields and reduce operational costs. Another trend is the use of farm management software for virtual fencing, enabling farmers to manage livestock more efficiently and effectively as well as facilitating livestock monitoring.

- However, challenges remain, such as the lack of internet connectivity in remote areas, which can hinder the adoption of these technologies. Despite these hurdles, the market is poised for continued expansion as farmers seek to improve productivity and profitability through technology integration.

What will be the Size of the Farm Management Software Market During the Forecast Period?

How is this Farm Management Software Industry segmented and which is the largest segment?

The farm management software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Precision farming

- Precision livestock

- Precision aquaculture

- Others

- Deployment

- Cloud-based

- Web-based

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- APAC

- China

- Middle East and Africa

- South America

- North America

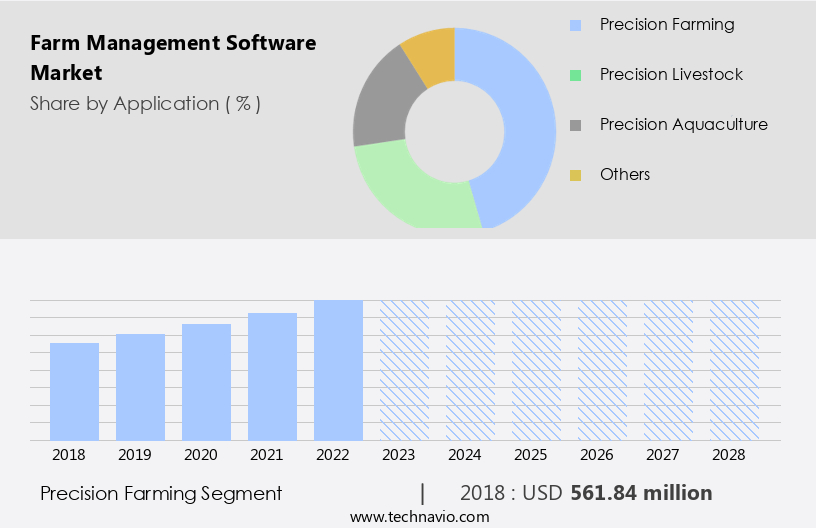

By Application Insights

- The precision farming segment is estimated to witness significant growth during the forecast period.

Farm management software is experiencing significant growth due to the increasing implementation of precision farming techniques in agriculture. Yield monitoring, a component of precision farming, enables farmers to make informed decisions based on data collected through sensors and agricultural drones. This data is utilized for field mapping, allowing for the variable application of irrigation and fertilizers. Identifying high- and low-performing areas of a field is facilitated through yield monitoring and field mapping. Key providers of yield monitoring software for farm management are Ag Leader Technology and Trimble Inc. Additionally, farm management software is essential for livestock monitoring, precision aquaculture, smart greenhouses, vertical farming, and indoor farming.

Rapid urbanization, rising population, water shortage issues, climate changes, recession, farming equipment, labor shortages, investment scenario, and the requirement for big data analytics are driving the demand for advanced farm management software. This software assists in crop health and growth monitoring, harvest time optimization, profitability analysis, farm office management, crop yields enhancement, fertilizer requirement estimation, soil mapping, and weather pattern analysis. Animal health monitoring is also facilitated through farm management software, ensuring sustainable farming practices.

Get a glance at the Farm Management Software Industry report of share of various segments Request Free Sample

The Precision farming segment was valued at USD 561.84 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

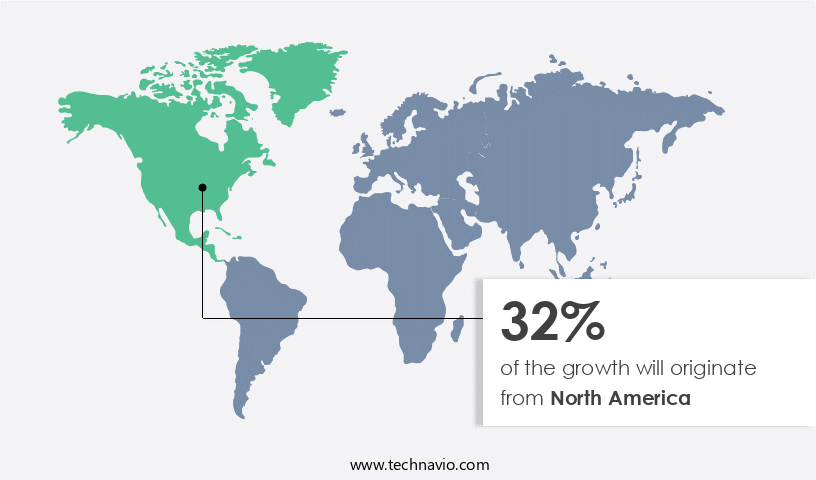

- North America is estimated to contribute 32% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The US is a significant player in the North American market, driven by its leadership in technology adoption withIn the agriculture sector. Precision farming, a key application of farm management software, has seen widespread usage in the US due to its ability to optimize crop yields and reduce resource consumption. Major American companies, such as AGCO Corp., Ag Leader Technology, Deere and Co., and Trimble Inc., are at the forefront of this trend, offering advanced solutions with features like big data analytics and precision farming integration. Other factors fueling the market include rapid urbanization, rising population, water shortage issues, climate changes, recession, farming equipment needs, labor shortages, and investment scenarios.

Farm management software enables farmers to monitor crop health, growth, and harvest time, optimizing profitability through data-driven insights. Additionally, it facilitates livestock monitoring, precision aquaculture, smart greenhouses, vertical farming, and indoor farming operations. Farm offices can manage fertilizer requirements, soil mapping, and weather patterns, ensuring efficient and sustainable farming practices.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Farm Management Software Industry?

Growing popularity of precision farming is the key driver of the market.

- Precision farming is revolutionizing the agricultural industry through the integration of machine learning and advanced software tools. These solutions optimize farm production with minimal inputs, addressing challenges posed by rapid urbanization, rising population, water shortage issues, and climate changes. Software applications are instrumental in managing various aspects of farming, including crop health and growth monitoring, harvest time prediction, and fertilizer requirement estimation. Precision farming software tools collect data from various sources, such as soil mapping, weather patterns, and crop yields, to provide farmers with actionable insights. For instance, Trimble Ag Software offers features for moisture, variety, and load tracking for crops grown on farms.

- Livestock monitoring is another crucial application of precision farming software, ensuring animal health and welfare. Moreover, precision farming extends to innovative farming methods like smart greenhouses, vertical farming, and indoor farming. Big data analytics plays a pivotal role In these modern farming practices, enabling farmers to make informed decisions regarding crop management and resource allocation. The compatibility of these software tools with multiple devices, such as smartphones and tablets, offers farmers the convenience of accessing real-time data on the go. Farm offices can benefit significantly from precision farming software, streamlining tasks and enhancing overall farm management efficiency. In the context of livestock farming, poultry and swine farms can leverage these tools to monitor animal health, manage feed requirements, and optimize production.

- Ultimately, precision farming software solutions contribute to improved profitability and sustainability In the face of labor shortages and economic recessions.

What are the market trends shaping the Farm Management Software Industry?

Usage of farm management software for virtual fencing is the upcoming market trend.

- Farm management software is a valuable investment for modern agricultural businesses, particularly In the context of machine learning and precision farming. This technology enables farmers to optimize resources and enhance productivity through advanced analytics and real-time monitoring. Precision farming, including livestock monitoring, is revolutionizing the industry. Virtual fencing technology, for instance, utilizes GPS and Internet-connected collars for livestock to eliminate the need for physical fences. This not only saves on labor and maintenance costs but also improves animal containment and welfare. Moreover, precision aquaculture, smart greenhouses, vertical farming, and indoor farming are gaining traction in response to rapid urbanization, rising population, water shortage issues, and climate changes.

- These farming methods rely heavily on data analysis for growth monitoring, harvest time prediction, and profitability assessment. Big data analytics plays a crucial role in farming, providing insights into crop health, fertilizer requirements, soil mapping, weather patterns, and animal health. Farm offices can access this data in real time, making informed decisions to optimize yields and reduce costs. The farming equipment sector is also adapting to these trends, integrating machine learning and automation to streamline operations. Labor shortages, a common challenge for the industry, are being addressed through technology. In summary, farm management software is a vital tool for agricultural businesses seeking to remain competitive and profitable In the face of evolving market dynamics.

What challenges does the Farm Management Software Industry face during its growth?

Lack of internet connectivity in remote areas is a key challenge affecting the industry growth.

- The farming industry is experiencing significant transformation due to technological advancements and changing market dynamics. Machine learning and big data analytics are revolutionizing precision farming, enabling farmers to optimize crop health, growth monitoring, fertilizer requirement, soil mapping, and weather patterns. Precision farming extends to livestock monitoring, precision aquaculture, smart greenhouses, vertical farming, and indoor farming. Rapid urbanization, rising population, water shortage issues, and climate changes pose challenges for the farming sector. Farmers must adapt to these conditions to ensure profitability and maintain farm offices efficiently. Farm management software plays a crucial role in addressing these challenges. Advanced features, such as real-time animal health monitoring, harvest time optimization, and growth monitoring, are essential for poultry farms and swine farms.

- However, Internet connectivity remains a barrier for farmers in rural areas. With approximately 75% of Internet users in Europe and North America and 25% in other regions, the digital divide persists. Farmers in remote areas often lack access to fast Internet connections necessary for advanced software features. Addressing this challenge will be crucial for the investment scenario in farm management software.

Exclusive Customer Landscape

The farm management software market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the farm management software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, farm management software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Ag Leader Technology - Farm management software solutions, including SMS software, facilitate data-driven decision-making in agriculture. This technology gathers information from planting to harvest, transforming raw field data into intelligent management insights. By leveraging advanced analytics and real-time data processing, farmers can optimize their operations, improve yields, and enhance overall productivity.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ag Leader Technology

- AGCO Corp.

- Agrivi d.o.o.

- Bayer AG

- CNH Industrial NV

- Cropin Technology Solutions Pvt. Ltd.

- Deere and Co.

- Fairfax Financial Holdings Ltd.

- GEA Group AG

- International Business Machines Corp.

- Iteris Inc.

- Kubota Corp.

- Madison One Holdings LLC

- Nofence AS

- RELX Plc

- SemiosBio Technologies Inc.

- Syngenta Crop Protection AG

- Topcon Corp.

- Trimble Inc.

- TSI Inc.

- Microsoft Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is experiencing significant growth due to the increasing adoption of technology in agriculture. Precision farming techniques, which utilize machine learning algorithms to optimize crop yields, are driving demand for advanced software solutions. These technologies enable farmers to monitor crop health, growth, and fertilizer requirements in real time, leading to increased profitability and efficiency. Moreover, the rise of livestock monitoring systems is also contributing to the growth of the market. These systems allow farmers to track animal health and productivity, optimizing feed management and reducing labor costs. Precision aquaculture is another emerging sector, where software solutions enable farmers to monitor water quality, temperature, and fish growth, ensuring optimal conditions for production.

The trend towards smart greenhouses and vertical farming is further fueling the demand for farm management software. These modern farming methods require precise control over environmental conditions and automation of various processes. Software solutions enable farmers to monitor and adjust temperature, humidity, light, and nutrient levels, ensuring optimal growing conditions and higher yields. Rapid urbanization and a rising population are putting pressure on farmers to increase production while minimizing water usage and reducing their carbon footprint. Farm management software can help farmers address these challenges by providing real-time data on water usage, weather patterns, and soil mapping. Big data analytics can also be used to optimize irrigation schedules and fertilizer applications, reducing water waste and increasing crop yields.

Climate changes and recession are also impacting the farming industry, making it essential for farmers to adapt to new challenges. Farm management software can help farmers mitigate the effects of climate changes by providing real-time data on weather patterns and soil conditions. Additionally, during economic downturns, software solutions can help farmers optimize their operations and reduce costs, making their businesses more resilient. Farm offices are increasingly relying on farm management software to streamline their operations and improve profitability. These solutions enable farmers to manage their equipment inventory, track labor hours, and analyze financial data. Crop yields and harvest times can also be monitored and analyzed, allowing farmers to make data-driven decisions and optimize their production cycles.

The market is experiencing significant growth due to the increasing adoption of technology in agriculture. Precision farming, livestock monitoring, smart greenhouses, and vertical farming are all driving demand for advanced software solutions. Farmers are using these technologies to optimize crop yields, reduce labor costs, and address the challenges of climate changes, water shortages, and economic downturns. Farm management software is becoming an essential tool for farmers to remain competitive and profitable in an ever-changing agricultural landscape.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

180 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 11.29% |

|

Market growth 2024-2028 |

USD 2.13 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

10.49 |

|

Key countries |

US, Canada, China, UK, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Farm Management Software Market Research and Growth Report?

- CAGR of the Farm Management Software industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the farm management software market growth of industry companies

We can help! Our analysts can customize this farm management software market research report to meet your requirements.

RIA -

RIA -