Fiber Based Packaging Market Size 2026-2030

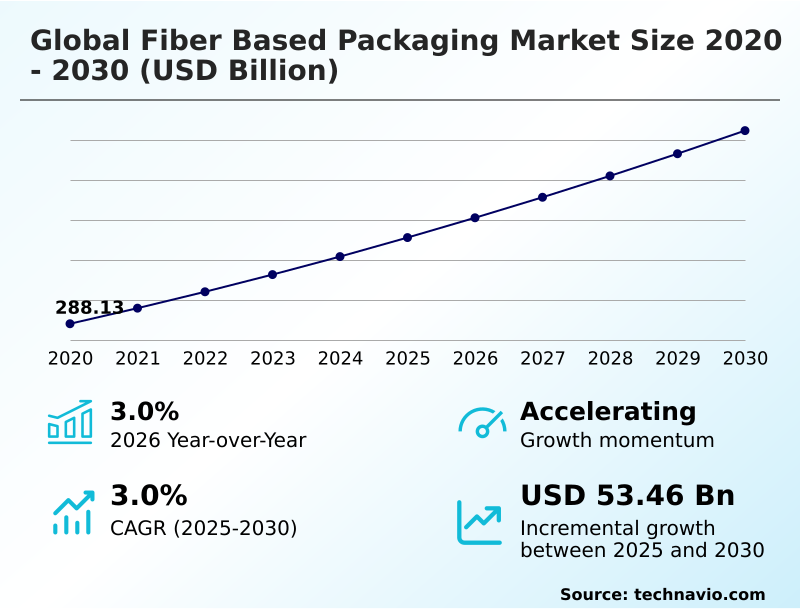

The fiber based packaging market size is valued to increase by USD 53.46 billion, at a CAGR of 3% from 2025 to 2030. Shifting consumer sentiment and corporate sustainability pledges will drive the fiber based packaging market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 49.8% growth during the forecast period.

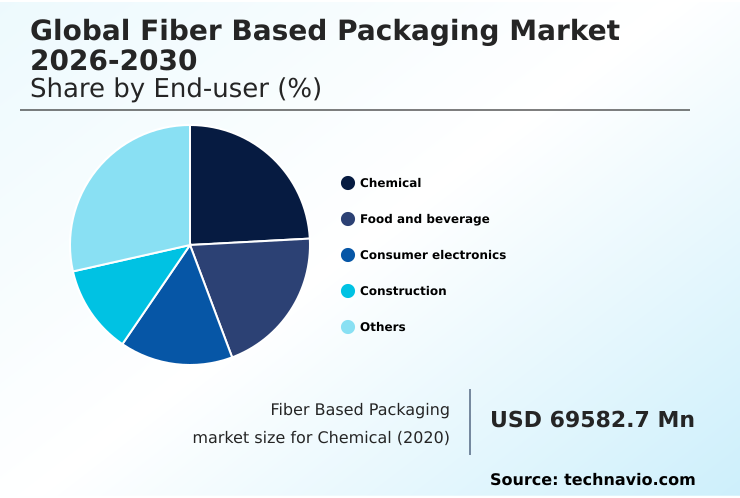

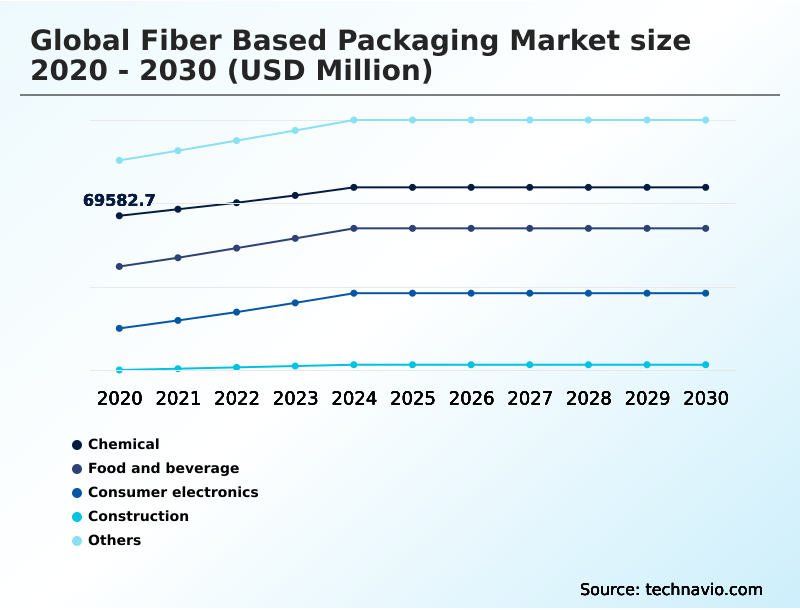

- By End-user - Chemical segment was valued at USD 76.05 billion in 2024

- By Product - Corrugated boxes segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 96.56 billion

- Market Future Opportunities: USD 53.46 billion

- CAGR from 2025 to 2030 : 3%

Market Summary

- The fiber based packaging market is undergoing a significant transformation, driven by a global mandate for sustainability and circularity. This shift is steering the industry away from traditional single-use plastics toward renewable, recyclable, and biodegradable alternatives. Key market dynamics include stringent environmental regulations, growing consumer awareness of plastic pollution, and corporate commitments to reduce carbon footprints.

- For example, a major consumer goods company might overhaul its entire product line to use only sustainable fiber solutions, from folding cartons to shipping containers. This involves not only changing materials but also redesigning supply chains to prioritize sustainable resource procurement and optimize logistics with lightweighting designs.

- The challenge lies in achieving this transition without compromising on product protection, shelf life, or cost-effectiveness. Technological innovation in areas like high-performance barrier coatings and molded pulp technology is therefore crucial, enabling fiber-based materials to meet the rigorous demands of industries ranging from food and beverage to electronics and e-commerce.

- The market's future will be shaped by the ability of manufacturers to deliver scalable, high-performance solutions that align with the principles of a circular economy.

What will be the Size of the Fiber Based Packaging Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Fiber Based Packaging Market Segmented?

The fiber based packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Chemical

- Food and beverage

- Consumer electronics

- Construction

- Others

- Product

- Corrugated boxes

- Folding cartons

- Paper bags and sacks

- Others

- Source

- Recycled fiber

- Virgin fiber

- Others

- Geography

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By End-user Insights

The chemical segment is estimated to witness significant growth during the forecast period.

The industrial chemicals sector is shifting toward sustainable fiber solutions, adopting reinforced fiber containers for non-hazardous material transport. Advanced materials offer enhanced grease and moisture resistance, a critical requirement for product stability.

The focus on lightweighting designs reduces shipping costs and environmental impact, while internal protection is provided by paper-based cushioning and custom molded fiber trays.

This move away from plastics streamlines disposal, feeding directly into the fiber recycling stream rather than landfills. Adoption of these solutions, which include folding cartons and paperboard cartons, has been shown to improve supply chain efficiencies by over 10%.

The versatility of these materials is also driving innovation in specialized fields like medtech packaging and advanced components packaging.

The Chemical segment was valued at USD 76.05 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 49.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Fiber Based Packaging Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the fiber based packaging market is diversifying, with significant growth in containerboard production across APAC to meet regional demand.

In North America, the e-commerce boom has spurred demand for recyclable paper mailers and other packaging solutions, with some logistics firms reporting a 25% reduction in shipping damages by switching to engineered fiber formats.

European markets are driven by stringent environmental sustainability regulations, promoting the use of paper bags and sacks in retail and biodegradable food packaging.

Manufacturers in regions like South America are focusing on using locally sourced kraft paper to reduce scope three greenhouse gas emissions.

The adoption of smart packaging technologies, including traceability codes, is a global phenomenon, enhancing supply chain transparency from Asia to Europe. This regional specialization is shaping global paperboard manufacturing and industrial packaging supply chains.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the fiber-based packaging market requires a detailed understanding of its complex trade-offs and technical nuances. A critical consideration is the cost-effectiveness of recycled versus virgin fiber, which directly influences sourcing strategies and final product pricing. The technical performance of materials, such as the moisture barrier properties of coated paperboard, determines their suitability for food and beverage applications.

- The impact of e-commerce on corrugated box design is undeniable, forcing innovations in structural integrity and user experience. This includes exploring the role of molded pulp in electronics packaging and finding effective fiber-based alternatives to plastic bubble wrap.

- For retail, the performance of paper bags in retail applications and the advancements in digital printing for folding cartons are key to brand presentation. Behind the scenes, there are significant operational hurdles. Meeting regulatory compliance for food-contact paper materials is a non-negotiable and complex process. Managing supply chain risks in global pulp sourcing has become a boardroom-level concern.

- There remain technological gaps in fiber-based flexible packaging that the industry is racing to close. The ability to accurately assess the recyclability of fiber packaging, especially when dealing with challenges in recycling mixed material paper packaging, is crucial for sustainability claims.

- Other key areas of R&D include improving grease resistance in foodservice packaging, ensuring automation compatibility of corrugated case designs, and comparing strength of different corrugated flutes for optimization.

- A comprehensive life cycle assessment of paper-based mailers can reveal truths about environmental impact, while research into the biodegradability of molded fiber in marine environments addresses end-of-life concerns, showing that some fiber products biodegrade up to 90% faster than plastics.

- This holistic view, covering everything from innovations in lightweighting for industrial packaging to detailed performance metrics, is essential for strategic decision-making.

What are the key market drivers leading to the rise in the adoption of Fiber Based Packaging Industry?

- Shifting consumer sentiment combined with corporate sustainability pledges serves as a key driver for market growth.

- Profound shifts in consumer perception and widespread corporate sustainability pledges are primary market drivers. Environmental responsibility is no longer a niche concern, influencing purchasing decisions for everyday consumer packaging.

- As a result, brands are rapidly adopting single-use plastic alternatives to meet both consumer expectations and regulatory pressures, contributing to a measurable carbon footprint reduction.

- This has spurred innovation in high-performance barrier coatings, allowing fiber to compete with plastic in demanding applications.

- According to circular economy principles, retail-ready packaging made from renewable packaging materials is gaining traction, with some retailers reporting a 15% improvement in shelf-stocking efficiency.

- The use of digital printing on corrugated materials, often sourced according to forest certification standards, allows for sophisticated branding while ensuring supply chain transparency.

What are the market trends shaping the Fiber Based Packaging Industry?

- The accelerated conversion from plastic to paper-based materials is a significant upcoming trend. This shift is reshaping packaging strategies across multiple industries.

- The plastic-to-paper conversion continues to accelerate, driven by consumer demand and corporate action. Innovations in molded pulp technology are enabling the creation of complex shapes for electronics and consumer goods, while advancements in de-inking technology improve the quality of recycled materials.

- A key trend is the development of curbside recyclable solutions, with companies achieving over 95% recyclability rates for new packaging formats. For instance, new flexible paper-based solutions for foodservice packaging are replacing multi-material plastics. This shift also enhances marketing; brands are leveraging packaging for unboxing experience personalization, which has been shown to increase brand loyalty enhancement by up to 20%.

- The integration of digital watermarks further supports this by enabling interactive consumer experiences.

What challenges does the Fiber Based Packaging Industry face during its growth?

- Raw material volatility and ongoing supply chain constraints present a key challenge affecting industry growth.

- The market faces significant hurdles, primarily from raw material volatility and persistent supply chain constraints. Securing consistent virgin fiber sourcing and high-quality post-consumer recycled content at stable prices remains a primary operational challenge. The efficacy of pulp purification technology is critical, yet scaling it to meet demand is capital-intensive, with new plant build-outs taking over 24 months.

- Furthermore, extended producer responsibility legislation is increasing compliance costs. While heavy-duty corrugated solutions are available for industrial use, optimizing their production requires significant investment in automated packaging lines. Ensuring food-grade safety standards for packaging made from biomaterials and recycled pulp adds another layer of complexity, demanding rigorous testing and sustainable resource procurement protocols.

Exclusive Technavio Analysis on Customer Landscape

The fiber based packaging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the fiber based packaging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Fiber Based Packaging Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, fiber based packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ahlstrom Oyj - Analysis points to a strategic focus on developing sustainable fiber-based materials for advanced filtration, diagnostic, and food packaging applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ahlstrom Oyj

- Brodrene Hartmann AS

- Genpak LLC

- Graphic Packaging Holding Co.

- Huhtamaki Oyj

- International Paper Co.

- Mayr Melnhof Karton AG

- Mondi Plc

- Nine Dragons Paper Holdings Ltd.

- Oji Fiber Solutions

- Packaging Corp. of America

- Pactiv Evergreen Inc.

- Papacks Sales GmbH

- Pratt Industries Inc.

- ProAmpac Holdings Inc.

- Smurfit Westrock plc

- Sonoco Products Co.

- Stora Enso Oyj

- UFP Technologies Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Fiber based packaging market

- In February 2025, ProAmpac Holdings Inc. advanced its portfolio by extending its curbside recyclable packaging into new segments like frozen foods and overwraps.

- In March 2025, Georgia-Pacific initiated full-scale production from a new high-speed US manufacturing line for recyclable paper mailers featuring a proprietary cushioning technology.

- In April 2025, SCG Packaging Public Company Limited started operations at a new molded fiber plant in Vietnam, targeting the high demand for biodegradable food containers from quick-service restaurants.

- In May 2025, Amcor plc and Metsa Group formed a strategic alliance to pioneer advanced 3D molded fiber packaging, incorporating specialized lidding and liners for diverse food product applications.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Fiber Based Packaging Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3% |

| Market growth 2026-2030 | USD 53461.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.0% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The fiber based packaging market is defined by a dynamic push toward circularity and functional innovation. The industry is moving beyond basic containers, focusing on developing advanced packaging materials and biomaterials that meet specialized needs in sectors like medtech packaging and consumer packaging.

- Core activities such as containerboard production and paperboard manufacturing are being transformed by efficiency mandates and sustainability targets. We are seeing widespread adoption of molded pulp technology and flexible paper-based solutions, which offer viable alternatives to plastics. The development of high-performance barrier coatings is a critical enabler, providing essential grease and moisture resistance.

- R&D in pulp purification technology and de-inking technology is improving the quality of post-consumer recycled content, a key input. Companies are engineering lightweighting designs and heavy-duty corrugated solutions to optimize logistics. The use of recyclable paper mailers and molded fiber trays in e-commerce has demonstrated a reduction in material usage by up to 20% compared to legacy solutions.

- Ultimately, creating effective packaging solutions hinges on integrating everything from virgin fiber sourcing to the final folding cartons and paperboard cartons.

What are the Key Data Covered in this Fiber Based Packaging Market Research and Growth Report?

-

What is the expected growth of the Fiber Based Packaging Market between 2026 and 2030?

-

USD 53.46 billion, at a CAGR of 3%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Chemical, Food and beverage, Consumer electronics, Construction, and Others), Product (Corrugated boxes, Folding cartons, Paper bags and sacks, and Others), Source (Recycled fiber, Virgin fiber, and Others) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Shifting consumer sentiment and corporate sustainability pledges, Raw material volatility and supply chain constraints

-

-

Who are the major players in the Fiber Based Packaging Market?

-

Ahlstrom Oyj, Brodrene Hartmann AS, Genpak LLC, Graphic Packaging Holding Co., Huhtamaki Oyj, International Paper Co., Mayr Melnhof Karton AG, Mondi Plc, Nine Dragons Paper Holdings Ltd., Oji Fiber Solutions, Packaging Corp. of America, Pactiv Evergreen Inc., Papacks Sales GmbH, Pratt Industries Inc., ProAmpac Holdings Inc., Smurfit Westrock plc, Sonoco Products Co., Stora Enso Oyj and UFP Technologies Inc.

-

Market Research Insights

- The market is rapidly evolving beyond simple packaging, driven by a convergence of corporate sustainability pledges and consumer demand for environmental responsibility. The plastic-to-paper conversion is accelerating, with adoption rates in some consumer goods categories increasing by 30% in just two years. This shift is enabled by innovations that address previous material limitations.

- For instance, new barrier technologies have improved moisture resistance, making biodegradable food packaging a viable option for a wider range of products. The surge in e-commerce packaging demand is also a powerful force, pushing for curbside recyclable solutions that improve logistics efficiency.

- Companies adopting these solutions report a 10% improvement in customer satisfaction scores related to unboxing experience personalization and sustainability perception.

We can help! Our analysts can customize this fiber based packaging market research report to meet your requirements.

RIA -

RIA -