Fitness And Recreational Sports Centers Market Size 2026-2030

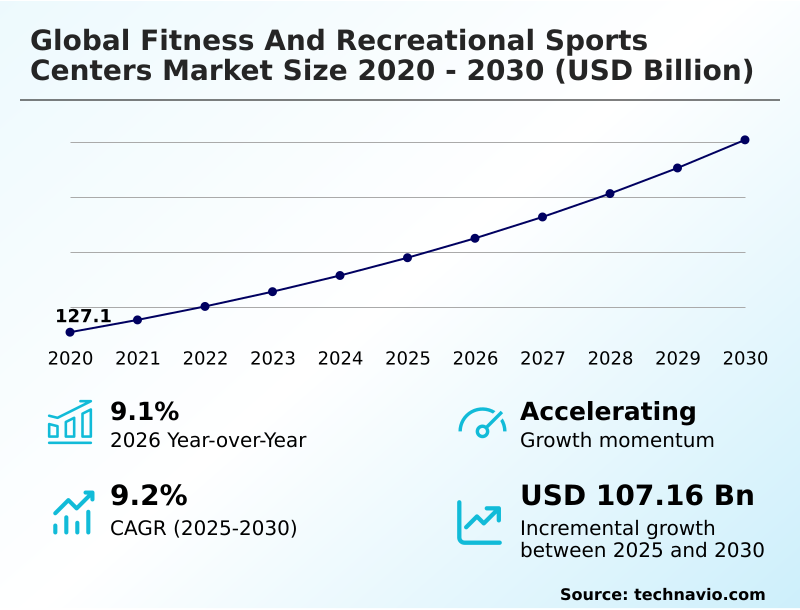

The fitness and recreational sports centers market size is valued to increase by USD 107.16 billion, at a CAGR of 9.2% from 2025 to 2030. Growing health and wellness awareness driving memberships will drive the fitness and recreational sports centers market.

Major Market Trends & Insights

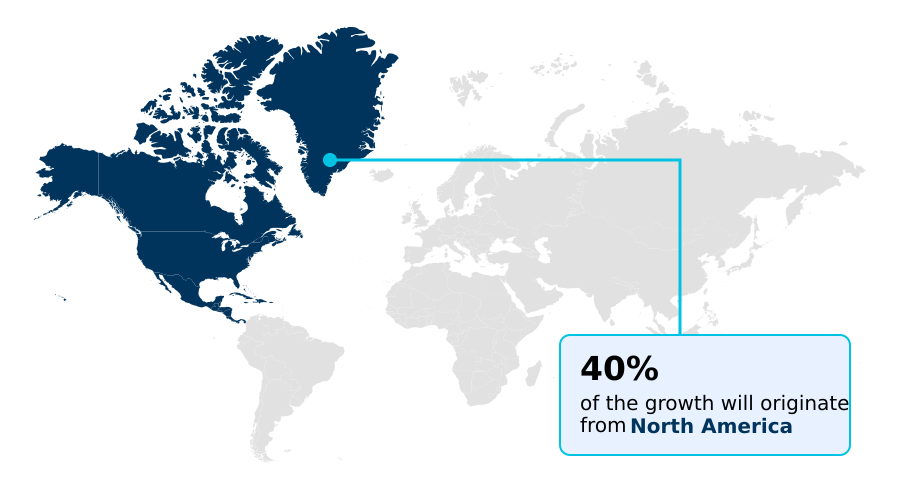

- North America dominated the market and accounted for a 39.5% growth during the forecast period.

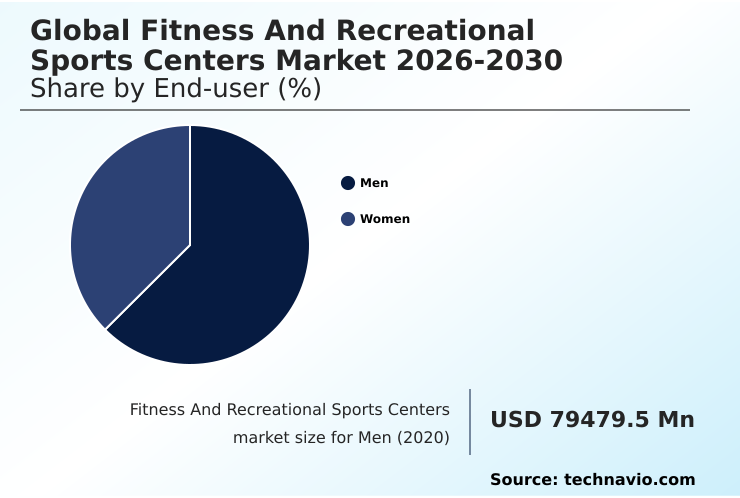

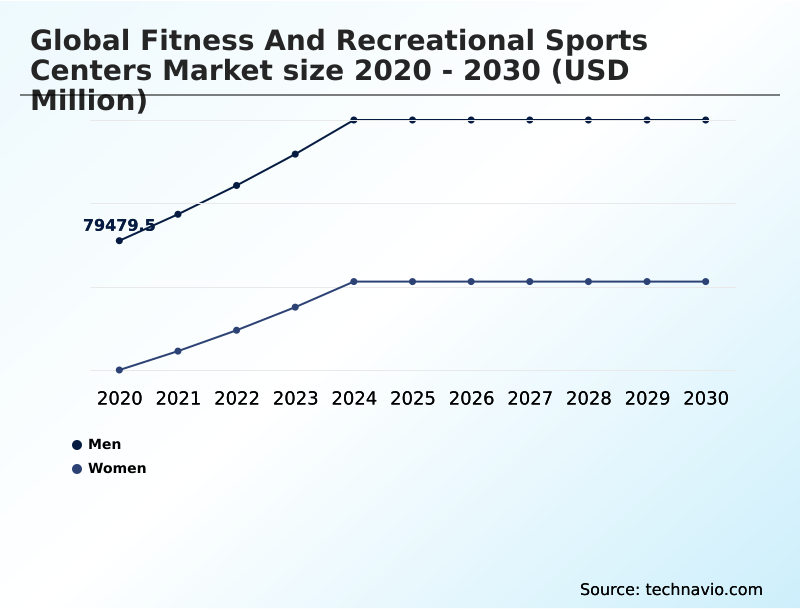

- By End-user - Men segment was valued at USD 109.23 billion in 2024

- By Age Group - 35 and younger segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 174.85 billion

- Market Future Opportunities: USD 107.16 billion

- CAGR from 2025 to 2030 : 9.2%

Market Summary

- The fitness and recreational sports centers market is undergoing a significant transformation, moving beyond conventional gym models to become comprehensive wellness destinations. This evolution is driven by a heightened consumer focus on holistic health, encompassing mental well-being alongside physical fitness.

- Facilities are increasingly integrating specialized services such as mind-body disciplines, advanced recovery therapies, and personalized nutritional counseling to meet these demands. The rise of digital health platforms and wearable technology integration allows for unprecedented data-driven personalization of workout regimens.

- For instance, a facility can leverage AI-driven fitness tracking data to optimize class schedules and equipment availability in real-time, reducing member wait times by up to 25% and improving operational efficiency. However, this progress is met with challenges, including the high operational costs of continuous technological upgrades and intense competition from hybrid fitness models.

- Success in this evolving landscape requires a strategic balance between offering cutting-edge, personalized experiences and maintaining accessible, community-centric environments that foster long-term member loyalty.

What will be the Size of the Fitness And Recreational Sports Centers Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Fitness And Recreational Sports Centers Market Segmented?

The fitness and recreational sports centers industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Men

- Women

- Age group

- 35 and younger

- 35-54

- 55 and older

- Service type

- Gym and fitness centers

- Sports clubs

- Yoga and pilates studios

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- Spain

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By End-user Insights

The men segment is estimated to witness significant growth during the forecast period.

The men's segment is evolving beyond traditional weightlifting, driven by a demand for data-driven performance metrics and community-based fitness. This demographic increasingly seeks facilities offering high-intensity interval training (HIIT) and advanced recovery therapies.

Operators observe that the adoption of wearable technology integration for performance tracking has boosted member engagement by over 15%.

A focus on longevity and biological optimization is a primary driver for middle-aged participants, fueling investment in premium memberships that include preventative health solutions.

The appeal of community-centric environments and professional coaching services remains a critical factor, compelling centers to offer specialized functional fitness programs and athletic resorts that cater to these specific wellness goals, ensuring high retention within this key end-user group.

The Men segment was valued at USD 109.23 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Fitness And Recreational Sports Centers Market Demand is Rising in North America Get Free Sample

The geographic landscape of the fitness and recreational sports centers market is characterized by varied maturity and growth dynamics.

North America remains a dominant force, projected to account for 39% of the market's incremental growth, driven by a robust infrastructure of athletic resorts and high adoption of digital health platforms.

Meanwhile, the APAC region is forecast to exhibit the fastest expansion, with a growth rate approaching 10%, fueled by rising health and wellness awareness and government-led corporate wellness initiatives in countries like China and India.

Europe showcases a sophisticated market with a strong emphasis on sustainable facility design and boutique fitness studios.

The high concentration of certified fitness professionals in developed regions enhances service quality, while franchise-based gym expansion drives growth in emerging economies across South America and the Middle East and Africa.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Analyzing the fitness and recreational sports centers market reveals a complex interplay between technology, service models, and consumer expectations. Strategic decisions now revolve around the impact of VR workouts on member retention and the roi of digital health platform integration.

- The integration of holistic wellness in fitness centers has become a key differentiator, compelling operators to evaluate the cost-benefit of functional training zones and advanced recovery therapies in athletic resorts. Technology for personalized fitness programming is central, with a focus on AI fitness tracking for user engagement and the challenges of biometric data integration.

- Businesses are also exploring how to develop effective corporate wellness partnerships and implement strategies to reduce high member churn. The role of boutique studios in market growth continues to expand, driven by specialized offerings like hiit programming for diverse demographics and a rising demand for mind-body disciplines in gyms.

- Simultaneously, operators are assessing the growth of racquet sports facility investment and the operating costs of modern aquatic centers. Business model innovation is evident in the rising popularity of pay-as-you-go gym membership trends, which cater to consumer demand for flexibility.

- Facilities that successfully design community-centric fitness environments and offer robust preventative health solutions, sometimes incorporating medical diagnostic tools in fitness centers, report member satisfaction scores nearly double those of traditional gyms, underscoring a clear shift in market priorities.

What are the key market drivers leading to the rise in the adoption of Fitness And Recreational Sports Centers Industry?

- The primary market driver is the growing consumer awareness of health and wellness, which is directly fueling membership growth across facilities.

- Market growth is fundamentally propelled by rising health and wellness awareness and the increasing prevalence of lifestyle-related diseases. Corporate wellness initiatives that subsidize gym access have proven highly effective, boosting employee participation by over 50% in partner companies.

- This B2B approach creates a stable revenue stream for facilities offering professional coaching services.

- Simultaneously, the demand for preventative health solutions has intensified, with personalized training plans and data-driven fitness programs helping partner insurance firms reduce long-term healthcare claims by 10%.

- This integration of fitness into the broader healthcare ecosystem, supported by digital health platforms, positions fitness centers as essential service providers, driving both membership and strategic partnerships across various age-specific fitness programs.

What are the market trends shaping the Fitness And Recreational Sports Centers Industry?

- The integration of virtual and augmented reality for immersive workouts represents a significant emerging trend, reshaping mainstream fitness experiences.

- The market is defined by a significant shift toward technology-driven, experiential fitness. The integration of immersive virtual reality fitness and gamified fitness sessions is transforming workouts into engaging events, leading to a 40% increase in user participation in some boutique fitness studios.

- This trend is complemented by the expansion of holistic wellness services, including mind-body disciplines, which help facilities achieve a 15% higher average revenue per member. Sustainable facility design is also gaining traction as a key differentiator. Furthermore, the rise of functional fitness programs and dedicated strength-training zones reflects a consumer focus on performance-based training.

- These technology-centric and wellness-oriented shifts are reshaping business models and creating new opportunities for growth and member engagement.

What challenges does the Fitness And Recreational Sports Centers Industry face during its growth?

- A primary challenge impacting industry growth is high member churn, which complicates the implementation of effective customer retention strategies.

- Operators face significant financial and operational hurdles that temper market growth. The necessity for continuous technological upgrades, including AI-driven fitness tracking and other tools for data-driven personalization, has increased capital expenditures by nearly 20% in the last two years.

- This financial pressure is compounded by persistently high member churn, with some facilities experiencing annual attrition rates exceeding 35% despite investing in member retention strategies. This volatility complicates revenue forecasting and limits profitability.

- Furthermore, competition from flexible hybrid fitness models and an array of low-impact exercise options available online challenges the value proposition of traditional, physical-first centers, demanding constant innovation to maintain market share.

Exclusive Technavio Analysis on Customer Landscape

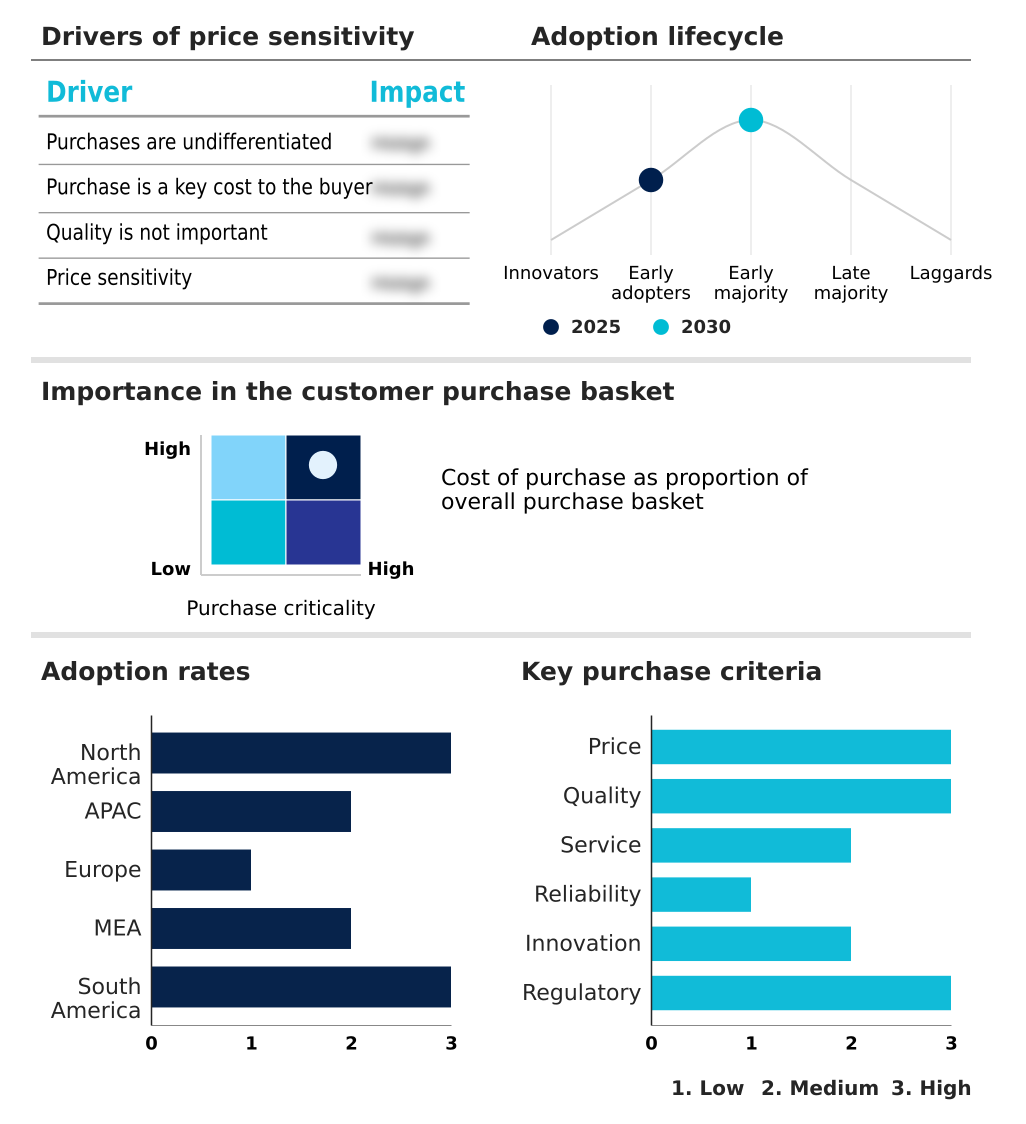

The fitness and recreational sports centers market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the fitness and recreational sports centers market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Fitness And Recreational Sports Centers Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, fitness and recreational sports centers market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

24 Hour Fitness USA LLC - Key solutions encompass full-service gymnasiums, diverse group classes, aquatic facilities, and personalized training, addressing comprehensive fitness needs across member segments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 24 Hour Fitness USA LLC

- Anytime Fitness Franchisor LLC

- Barrys

- Crunch LLC

- Curves NA Inc.

- David Lloyd Leisure Ltd.

- Equinox Holdings Inc.

- FIT House of Brands

- Golds Gym Club Holding LLC

- Life Time Inc.

- Planet Fitness Inc.

- RSG Group GmbH

- Snap Fitness Inc

- SoulCycle

- The Gym Group

- Ultimate Fitness Group LLC

- Virgin Active Ltd.

- YouFit Gyms

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Fitness and recreational sports centers market

- In August 2024, Innovatech launched its BioSync biometric integration platform, allowing gym members to sync real-time metabolic data with facility equipment to automatically customize resistance levels.

- In November 2024, Global PharmaCo, in collaboration with the Boutique Fitness Alliance, launched the Cycle-Syncing Initiative, a program that aligns exercise intensity with the physiological phases of the female menstrual cycle.

- In May 2025, Prestige Hospitality Group announced a strategic partnership with Wellness Diagnostics Inc. to integrate medical-grade diagnostic screenings into its luxury fitness centers, catering to growing interest in preventative health.

- In April 2025, Vitality Health and FitCorp introduced a groundbreaking collaboration allowing medical professionals to prescribe gym memberships as part of chronic disease management protocols.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Fitness And Recreational Sports Centers Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 290 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.2% |

| Market growth 2026-2030 | USD 107161.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.1% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, Spain, France, Italy, The Netherlands, UAE, Saudi Arabia, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The fitness and recreational sports centers market is rapidly advancing from traditional exercise facilities to high-tech wellness ecosystems. This evolution is defined by the convergence of immersive virtual reality fitness, gamified fitness sessions, and comprehensive holistic wellness services. Leading facilities are distinguished by their dedicated strength-training zones and advanced functional fitness programs, which are enhanced by wearable technology integration.

- The core of this transformation is data-driven personalization, enabled by AI-driven fitness tracking and biometric data integration, which allows for highly specific personalized training plans. Boardroom decisions are increasingly influenced by this data, guiding capital expenditure toward new recovery therapies and medical-grade diagnostic tools over simple facility expansion.

- Operators are adopting hybrid fitness models and pay-as-you-go membership options to improve member retention strategies. The market includes a diverse range of players, from luxury athletic resorts and aquatic centers to specialized boutique fitness studios offering high-intensity interval training (HIIT) and mind-body disciplines.

- These trends are supported by corporate wellness initiatives and a broader consumer shift toward preventative health solutions, solidifying the industry's role in modern healthcare. The integration of such technologies has been shown to reduce member attrition by over 25% within the initial months of adoption.

What are the Key Data Covered in this Fitness And Recreational Sports Centers Market Research and Growth Report?

-

What is the expected growth of the Fitness And Recreational Sports Centers Market between 2026 and 2030?

-

USD 107.16 billion, at a CAGR of 9.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Men, and Women), Age Group (35 and younger, 35-54, and 55 and older), Service Type (Gym and fitness centers, Sports clubs, Yoga and pilates studios, and Others) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Growing health and wellness awareness driving memberships, High member churn complicating customer retention strategies

-

-

Who are the major players in the Fitness And Recreational Sports Centers Market?

-

24 Hour Fitness USA LLC, Anytime Fitness Franchisor LLC, Barrys, Crunch LLC, Curves NA Inc., David Lloyd Leisure Ltd., Equinox Holdings Inc., FIT House of Brands, Golds Gym Club Holding LLC, Life Time Inc., Planet Fitness Inc., RSG Group GmbH, Snap Fitness Inc, SoulCycle, The Gym Group, Ultimate Fitness Group LLC, Virgin Active Ltd. and YouFit Gyms

-

Market Research Insights

- The market's dynamism is driven by a strategic shift toward experiential fitness and customer-centric service models. Facilities implementing data-driven member engagement initiatives report up to a 20% improvement in retention rates. Moreover, public-private fitness partnerships have expanded access to professional coaching services, increasing community participation by over 30% in targeted urban areas.

- The growth of franchise-based gym expansion into underserved regions is broadening market reach, while luxury wellness hubs are setting new standards for premium service. This environment, supported by flexible payment options and online booking systems, caters to modern consumer demands for convenience and personalization, fostering sustained industry momentum. Sustainable facility design and inclusive fitness programming are also becoming key differentiators.

We can help! Our analysts can customize this fitness and recreational sports centers market research report to meet your requirements.

RIA -

RIA -