Floating Production Storage and Offloading Market Size 2024-2028

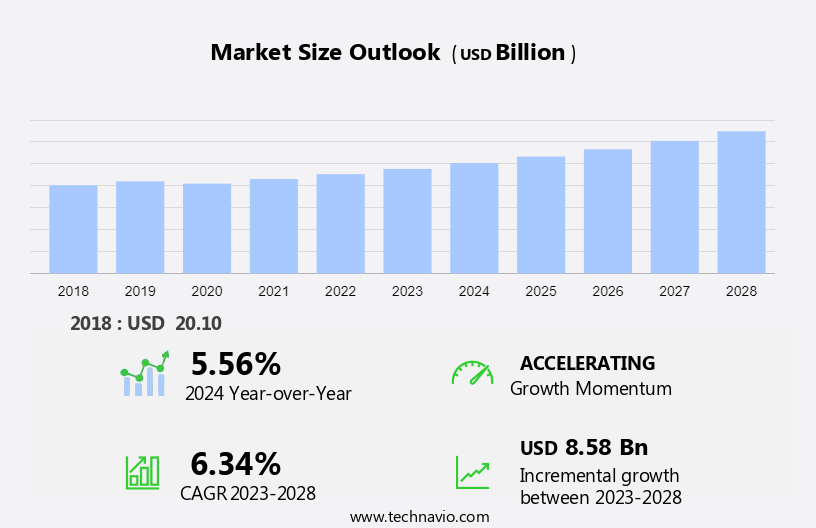

The floating production storage and offloading market size is forecast to increase by USD 8.58 billion at a CAGR of 6.34% between 2023 and 2028.

- The Floating Production Storage and Offloading (FPSO) market is experiencing significant growth due to key drivers such as increasing investments in offshore exploration and production (E&P) activities and the rise in deepwater and ultra-deepwater projects. These trends are being fueled by the need to access increasingly difficult-to-reach reserves. The market is driven by the rise in deepwater and ultra-deepwater projects, which require advanced FPSO vessels equipped with settling tanks, crude oil tanks, ballast tanks, slop tanks, methanol tanks, and utility tanks.

- Despite the volatility in crude oil prices, which can affect the supply of oil and gas, the FPSO market is still expected to grow. Companies are increasingly looking for innovative solutions to optimize offshore resource production. With technological advancements and a stronger focus on sustainable energy, the market's future remains promising, offering new opportunities for growth.

What will be the Floating Production Storage and Offloading Market Size During the Forecast Period?

- The floating production storage and offloading (FPSO) market encompasses the use of specialized vessels that process and store hydrocarbons from marginal fields, which are often located in deep waters or remote locations where traditional onshore facilities are not feasible. These fields may include subsea wells, which require the use of separation facilities to extract crude oil and natural gas from the produced fluids. FPSOs typically feature oil storage tanks, such as crude oil tanks, ballast tanks, slop tanks, methanol tanks, and utility tanks, that provide the necessary capacity to store and transport the extracted hydrocarbons. The design of these tanks is crucial, with considerations given to tank internals, intakes, and structural voids to ensure optimal performance and safety.

- Additionally, the offloading process involves transferring the stored hydrocarbons to an oil tanker or LNG carrier for further transportation to refineries or markets. This process is carried out using flexible production tubes and spread mooring systems, which allow the FPSO to remain in place while the transfer takes place. Environmental limits play a significant role in the FPSO market, with stringent regulations governing the design and operation of these vessels to minimize their environmental impact. Dry dock inspections and maintenance are essential to ensure the structural integrity and efficient operation of the FPSO's tanks and systems. In summary, the FPSO market offers a cost-effective and efficient solution for producing and transporting hydrocarbons from marginal fields. The design and operation of these vessels require careful consideration of tank design, tank internals, and environmental regulations to ensure safe and sustainable production.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Single

- Double

- Product Type

- Converted

- Newly built

- Geography

- South America

- Brazil

- Middle East and Africa

- Nigeria

- APAC

- China

- Europe

- UK

- North America

- South America

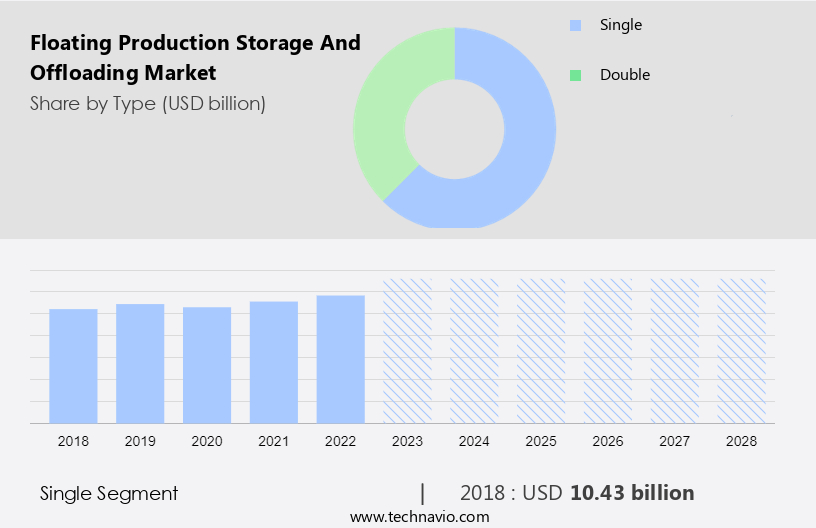

By Type Insights

- The single segment is estimated to witness significant growth during the forecast period.

Floating Production Storage and Offloading (FPSO) involves converting existing transportation vessels, such as tankers or bulk carriers, into production units. This cost-effective solution reduces the capital expenditure required compared to designing and constructing a new FPSO, which can reach up to a billion US dollars for the same capacity. The benefits of using converted FPSOs include lower costs and the ability to produce hydrocarbons from sub-sea oil wells in shallow fields. These vessels can be used for the storage, transportation, and processing of hydrocarbons, eliminating the need for pipelines in certain situations. Converting a tanker into an FPSO requires minimal modifications, making it a practical solution for oil and gas companies. This cost-effective and efficient method is a valuable asset in the energy sector, particularly for producing hydrocarbons from sub-sea oil wells in shallow fields where pipelines are not feasible.

Get a glance at the market report of share of various segments Request Free Sample

The single segment was valued at USD 10.43 billion in 2018 and showed a gradual increase during the forecast period.

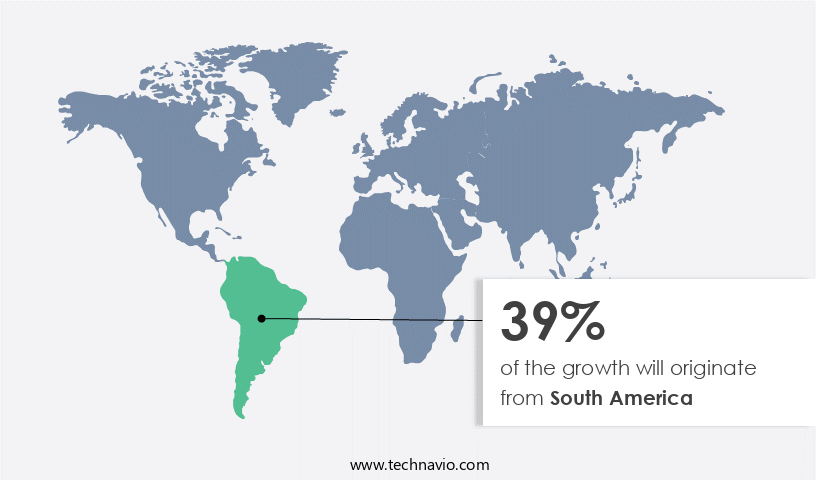

Regional Analysis

- South America is estimated to contribute 39% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The Floating Production Storage and Offloading (FPSO) market in South America is poised for growth due to increasing investments in the upstream oil and gas sector. The Brazilian government's commitment to spend USD 5.4 billion on oil and gas exploration activities from 2024 to 2030 is expected to boost E and P activities, leading to an increase in crude oil and natural gas production. This surge in production will necessitate expansions to the pipeline network to transport refined products and crude oil to consumers, thereby fueling demand for FPSOs.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Floating Production Storage and Offloading Market?

Increasing investments in offshore E&P activities is the key driver of the market.

- The Floating Production Storage and Offloading (FPSO) market is experiencing significant growth due to the increasing exploration and production (E&P) activities in offshore oil and gas fields. With the depletion of easily accessible onshore resources, oil and gas companies are turning to less explored areas, leading to an increase in FPSO demand. Moreover, rising global crude oil prices are making offshore drilling more economically viable, further boosting FPSO market growth. Several countries are planning to commence production from new oil and gas fields, contributing to market expansion. FPSOs provide an effective solution for producing and storing hydrocarbons from subsea wells, reducing the need for costly onshore facilities.

- Additionally, these vessels offer flexibility in terms of location, allowing production from marginal fields and shallow fields that may not be economically viable through traditional methods. FPSOs consist of a floating vessel, processing equipment, separation facilities, and various tanks such as crude oil tanks, ballast tanks, slop tanks, methanol tanks, utility tanks, and settling tanks. They also include intakes, oil separators, seawater treatment, gas dehydration, and gas compression systems. FPSOs can be connected to subsea oil wells via a pipeline or directly transferred to an oil tanker. The market dynamics of FPSO are influenced by factors such as environmental limits, oilfield infrastructure, and transportation requirements.

- In conclusion, FPSOs offer environmental benefits by reducing the need for extensive onshore infrastructure and the associated emissions. Additionally, they provide accommodation facilities for personnel working on offshore installations. FPSOs are essential for the production and offloading of hydrocarbons from subsea wells in deepwater and remote locations. Their flexibility, efficiency, and ability to handle various hydrocarbon mixtures make them an attractive solution for oil and gas companies looking to maximize production from offshore fields.

What are the market trends shaping the Floating Production Storage and Offloading Market?

An increase in deepwater and ultra-deepwater projects is the upcoming trend in the market.

- The Floating Production Storage and Offloading (FPSO) market has gained significant traction in the oil and gas industry due to the increasing focus on marginal fields and the exploration of deep and ultra-deep waters. FPSOs offer a cost-effective solution for producing oil and gas from subsea wells, particularly in areas where pipelines to onshore facilities are not feasible or economically viable. These floating vessels are equipped with separation facilities, including oil separators, gas dehydration units, and seawater treatment systems, to process hydrocarbons before storing them in crude oil tanks, ballast tanks, slop tanks, methanol tanks, utility tanks, and structural voids. FPSOs are designed to operate in harsh sea conditions and can be moored using spread mooring systems or docked in dry docks for maintenance. The flexibility of FPSOs allows for the production of hydrocarbons from subsea oil wells and the offloading of crude oil to oil tankers or pipelines for transportation to refineries.

- Additionally, the market for FPSOs is expected to grow as oil and gas companies continue to explore deeper waters and seek to maximize production from marginal fields. Deepwater projects require substantial investments and time compared to shallow water or onshore projects. However, advancements in processing equipment and technology have made it possible to access previously inaccessible areas. FPSOs offer a mobile offshore production solution that eliminates the need for long-distance pipelines, reducing transportation costs and environmental impact. The market for FPSOs is expected to continue growing as companies seek to optimize production and reduce costs in the oilfield.

What challenges does Floating Production Storage and Offloading Market face during the growth?

Volatility in crude oil prices restraining oil and gas supply is a key challenge affecting the market growth.

- The Floating Production Storage and Offloading (FPSO) market encompasses the use of floating vessels for the production, processing, and offloading of hydrocarbons from marginal fields, including subsea wells. FPSOs integrate onshore facilities such as separation facilities and oil storage tanks onboard, enabling the production of oil and gas from sub-sea oil wells. These vessels feature flexible production tubes, spread moorings, and structural voids for settling tanks, crude oil tanks, ballast tanks, slop tanks, methanol tanks, utility tanks, and intakes for seawater treatment and oil separation.

- However, FPSOs provide flexibility for oilfield development in shallow fields and deepwater areas, allowing for the transportation of hydrocarbons via pipeline or oil tanker. Environmental limits dictate the design and internals of these tanks, including the implementation of gas dehydration, gas compression, water injection, and seawater treatment systems. FPSOs serve as mobile offshore production units, accommodating processing equipment and living quarters for personnel. Despite fluctuations in crude oil prices, the FPSO market continues to grow, providing essential solutions for the production and offloading of hydrocarbons in the oil and gas industry.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BUMI ARMADA BERHAD

- Bluewater Energy Services BV

- BP Plc

- BW Offshore Ltd.

- Chevron Corp.

- China National Offshore Oil Corp.

- Exxon Mobil Corp.

- Hyundai Heavy Industries Co. Ltd.

- Mitsubishi Heavy Industries Ltd.

- MODEC Inc.

- Petroleo Brasileiro SA

- Saipem S.p.A.

- SBM Offshore NV

- Shell plc

- TechnipFMC plc

- TotalEnergies SE

- Vietnam Oil and Gas Group

- Woodside Energy Group Ltd.

- Yinson Holdings Berhad

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The floating production storage and offloading (FPSO) market represents a significant advancement in the oil and gas industry, enabling the exploitation of marginal fields that were once deemed uneconomical. This technology combines production, processing, and storage capabilities on a floating vessel, reducing the need for costly onshore facilities. FPSOs are designed to operate in various environments, from shallow waters to deep-sea locations. They can be utilized for both oil and liquefied natural gas (LNG) production. The process begins with the extraction of hydrocarbons from subsea wells, which are transported through flexible production tubes to the FPSO's separation facilities. The separation facilities onboard the FPSO are responsible for processing crude oil and separating it from water, gas, and other impurities. This is crucial to ensure the quality of the final product and minimize environmental impacts. The processed oil is then stored in crude oil tanks, while water and gas are disposed of or re-injected into the reservoir. Ballast tanks are an essential component of FPSO design, as they allow the vessel to maintain its stability during production and offloading operations.

Additionally, these tanks can also be used for storing water, slop, and methanol, among other substances. Utility tanks provide the FPSO with essential services, such as water treatment, gas dehydration, and gas compression. FPSOs are typically moored using spread mooring systems, which consist of multiple anchors and tether lines. This design ensures the stability of the vessel in harsh marine conditions. The offloading process involves transferring the hydrocarbons to an oil tanker or, in the case of LNG, to a pipeline for further transportation. The flexibility of FPSOs makes them an attractive solution for oilfields located in remote or challenging environments. They can be deployed in areas with limited infrastructure, reducing the need for extensive onshore facilities. Moreover, FPSOs can be re-deployed to different fields, making them a cost-effective solution for oilfield operators.

In summary, mobile offshore production platforms, including FPSOs, have revolutionized the oil and gas industry by enabling the exploitation of marginal fields that were once inaccessible. These platforms offer numerous advantages, including reduced costs, increased efficiency, and improved environmental performance. The FPSO market is expected to continue growing, driven by the increasing demand for energy and the need to extract hydrocarbons from increasingly complex reservoirs. In conclusion, the market plays a vital role in the oil and gas industry by providing a cost-effective and efficient solution for the production, processing, and storage of hydrocarbons. FPSOs offer numerous benefits, including flexibility, environmental performance, and reduced infrastructure requirements, making them an attractive solution for oilfield operators in various environments.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

156 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.34% |

|

Market growth 2024-2028 |

USD 8.58 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.56 |

|

Key countries |

Angola, Nigeria, China, UK, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across South America, Middle East and Africa, APAC, Europe, and North America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -