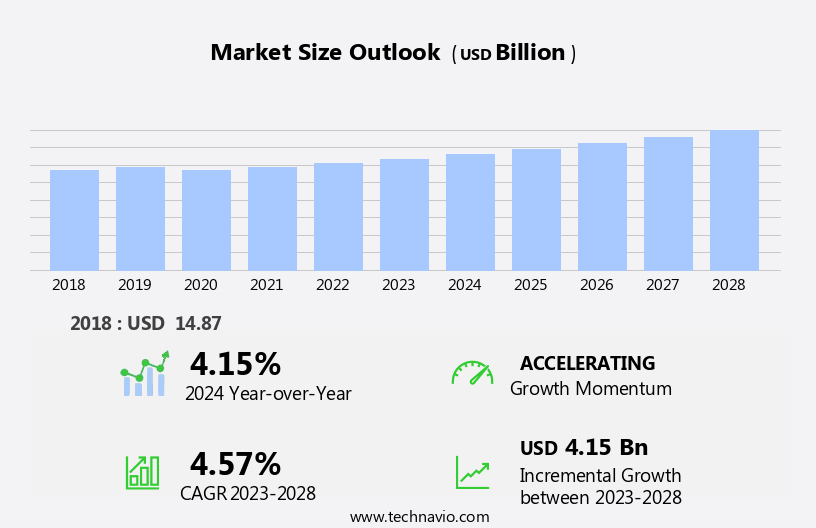

Food Texture Market Size 2024-2028

The food texture market size is forecast to increase by USD 4.15 billion, at a CAGR of 4.57% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing demand for food products with extended shelf lives. This trend is driven by the evolving consumer preferences for convenience and longer product durability. Furthermore, strategic alliances among market companies are shaping the competitive landscape, as companies collaborate to innovate and expand their offerings. Another key factor influencing the market is the rising demand for clean-label and natural ingredients in food products. Consumers are increasingly seeking healthier and more natural food options, leading to a growing demand for texturizers derived from natural sources.

- This trend presents both opportunities and challenges for market participants. While the shift towards natural ingredients offers potential for differentiation and increased consumer appeal, it also requires significant investment in research and development to source and produce these alternatives. Companies must navigate this challenge effectively to remain competitive and meet evolving consumer demands.

What will be the Size of the Food Texture Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by advancements in emulsion stability analysis, texture-based product design, and the exploration of food ingredient interactions. Starch gelatinization kinetics, particle size distribution, and mastication simulation are integral to understanding the behavior of food systems. Instrumental texture analysis, employing data analysis techniques, texture modification techniques, and strategies, shear force measurement, texture perception models, and rheological properties measurement, provide valuable insights into food structure and mouthfeel attributes. Rheometer calibration and consumer acceptability testing are crucial components of the texture analysis process. Sensory panel selection, sensory data analysis, water holding capacity, and sample preparation protocols are essential considerations for mouthfeel characterization.

Viscoelasticity determination, texture profile analysis, food microstructure imaging, and sensory evaluation methods contribute to the comprehensive understanding of food texture. Optimal processing parameters, sensory attribute mapping, and consumer texture preference are essential factors in food product development. The ongoing research and development in this field aim to provide innovative solutions for enhancing food texture and improving consumer satisfaction. The continuous unfolding of market activities and evolving patterns reflect the dynamic nature of the market.

How is this Food Texture Industry segmented?

The food texture industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Cellulose derivatives

- GPG

- Starch

- Others

- Source

- Natural

- Synthetic

- Type

- Gelling Agents

- Emulsifiers

- Stabilizers

- Thickeners

- Others

- Application

- Bakery

- Dairy

- Confectionery

- Meat Products

- Beverages

- Geography

- North America

- Canada

- Mexico

- Europe

- France

- Germany

- UK

- Middle East and Africa

- UAE

- APAC

- China

- India

- Indonesia

- Japan

- Malaysia

- South Korea

- Thailand

- South America

- Brazil

- Rest of World (ROW)

- North America

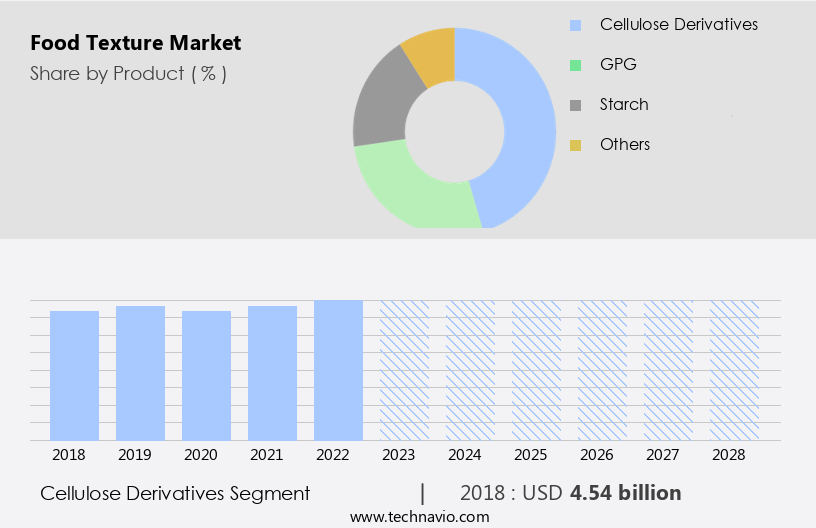

By Product Insights

The cellulose derivatives segment is estimated to witness significant growth during the forecast period.

The market is experiencing significant advancements, with a focus on emulsion stability analysis, texture-based product design, and food ingredient interactions. Cellulose derivatives, derived from natural sources and modified to enhance thickening, gelling, stabilizing, and emulsifying properties, are driving growth in this sector. Methylcellulose, carboxymethylcellulose (CMC), hydroxypropyl methylcellulose (HPMC), and microcrystalline cellulose (MCC) are commonly used cellulose derivatives in food applications. Their utilization in dairy, bakery, sauces, dressings, confectionery, and meat products improves texture, mouthfeel, shelf-life stability, and consumer acceptability. Starch gelatinization kinetics and particle size distribution are also crucial factors influencing food texture. Mastication simulation, compressive strength testing, gel strength analysis, and fat crystallization behavior are essential techniques for understanding texture properties.

Instrumental texture analysis, data analysis techniques, and texture modification strategies are employed to optimize processing parameters and sensory attribute mapping. Consumer texture preference is a critical consideration in food product development, and sensory evaluation methods are used to assess mouthfeel characterization, viscoelasticity determination, texture profile analysis, and food microstructure imaging. Rheological properties measurement and rheometer calibration ensure accurate texture analysis. Sensory panel selection and sensory data analysis are integral to consumer acceptability testing. Water holding capacity and sample preparation protocols are essential considerations in food texture research.

The Cellulose derivatives segment was valued at USD 4.54 billion in 2018 and showed a gradual increase during the forecast period.

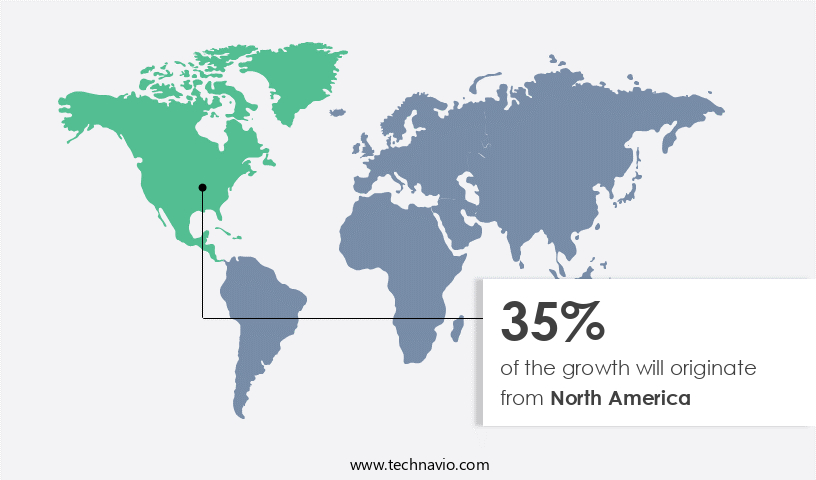

Regional Analysis

North America is estimated to contribute 35% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is experiencing steady growth due to increasing consumer preference for healthier food options, leading to a higher demand for fat replacers, emulsifiers, and other functional ingredients. This trend is particularly prominent in the US market. However, the use of unhealthy food texture products may hinder market growth. companies such as Archer Daniels Midland Co., Cargill Inc., and Ingredion Inc. Are expanding their production capacities to meet the growing demand for food texture products. These capacity expansions could accelerate market growth in North America during the forecast period. Texture-based product design plays a crucial role in food product development, with food ingredient interactions and starch gelatinization kinetics being essential considerations.

Instrumental texture analysis, including techniques such as compressive strength testing, gel strength analysis, and shear force measurement, are used to evaluate food texture properties. Mouthfeel attributes, including viscoelasticity determination and texture profile analysis, are also essential in food texture research. Texture modification techniques and strategies, such as particle size distribution, mastication simulation, and protein network formation, are employed to optimize food texture. Rheological properties measurement and rheometer calibration are essential for understanding the behavior of food textures. Consumer acceptability testing, sensory panel selection, and sensory data analysis are crucial in ensuring consumer texture preference and optimal processing parameters. Water holding capacity and sample preparation protocols are also essential aspects of food texture research.

Food microstructure imaging and sensory evaluation methods provide valuable insights into food texture characteristics, enabling companies to develop innovative and high-quality food texture products. Overall, the market in North America is expected to continue growing as companies invest in research and development to meet the evolving consumer demand for healthier and more innovative food products.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market continues to evolve, with ongoing research focusing on the impact of ingredient ratios and rheological properties in shaping desirable textures for various food applications. Consumer perception plays a significant role in the food texture landscape, as sensory attributes such as mouthfeel, viscosity, and elasticity are increasingly prioritized. Instrumental techniques and methods for evaluating food texture changes are essential in understanding the correlations between instrumental and sensory assessments. Microstructural characteristics and optimal processing conditions are also critical factors in achieving desired textures. As food microstructure and sensory texture continue to intertwine, techniques for improving food texture stability and understanding consumer preferences become increasingly important. Ingredient interactions and moisture content also significantly influence texture formation, while rheological models and predictive analyses help in measuring food texture changes during storage and in different food matrices. Temperature's impact on food texture stability is also a significant consideration, highlighting the intricate relationship between food composition and texture properties.

What are the key market drivers leading to the rise in the adoption of Food Texture Industry?

- The surge in demand for food texture solutions that enhance the shelf stability of food products serves as the primary market driver. The market experiences significant growth due to the increasing demand for food products with extended shelf-life and desirable textures. Consumers' preference for convenient, ready-to-eat options intensifies the need for food items that maintain their freshness and sensory appeal. Texture-modifying ingredients, including stabilizers, gums, and emulsifiers, play a crucial role in enhancing food products' structural integrity and moisture retention properties. These ingredients help delay spoilage and preserve food quality during storage. Emulsion stability analysis, particle size distribution, and starch gelatinization kinetics are essential factors in texture-based product design. Mastication simulation, compressive strength testing, gel strength analysis, and fat crystallization behavior are other critical considerations in ensuring the desired texture and stability of food products.

- Food ingredient interactions are also vital in creating the optimal texture and preserving the food's freshness. By focusing on these factors, food manufacturers can produce high-quality, texturally appealing, and longer-lasting food items that meet consumers' expectations.

What are the market trends shaping the Food Texture Industry?

- The emergence of strategic alliances among market companies represents a significant market trend. This development reflects the increasing recognition of the benefits derived from collaborative business relationships.

- The market experiences significant growth due to the increasing number of strategic alliances among companies. These collaborations enable companies to combine their expertise, resources, and technologies, resulting in the development of innovative texture-enhancing solutions. By partnering with other companies, firms can access a broader range of ingredients, processing techniques, and market insights, leading to the creation of superior food texture-modifying products. Moreover, strategic alliances facilitate entry into new distribution channels and market segments, expanding market reach and penetration. With competition intensifying and the demand for texture-enhanced food products continuing to rise, these collaborations are essential for driving innovation, market expansion, and overall growth within the market.

- Instrumental texture analysis, data analysis techniques, texture modification techniques, and rheological properties measurement play crucial roles in enhancing food texture. companies employ texture perception models and shear force measurement to ensure the desired mouthfeel attributes are achieved. These strategies contribute to the development of harmonious and immersive food textures that cater to diverse consumer preferences and market demands.

What challenges does the Food Texture Industry face during its growth?

- The food industry faces significant growth challenges due to escalating consumer preferences for clean-label and natural ingredients in food products.

- The market experiences significant growth due to the increasing consumer preference for clean-label and natural ingredients. With health consciousness on the rise, consumers are becoming more discerning about the ingredients in their food, leading to a demand for minimally processed, recognizable ingredients with simple and transparent labels. This trend necessitates food manufacturers to reformulate their products, replacing synthetic or chemically modified texture agents with natural alternatives. However, finding suitable natural substitutes that can replicate the functionality and performance of synthetic ingredients while maintaining the desired texture, stability, and sensory attributes is a challenge for food formulators.

- To address this challenge, advanced technologies such as rheometer calibration, consumer acceptability testing, texture analyzer setup, sensory panel selection, sensory data analysis, and sample preparation protocols are employed. These techniques enable food manufacturers to evaluate the water holding capacity, mouthfeel characterization, and viscoelasticity determination of their formulations accurately. By utilizing these methods, food formulators can ensure the development of textured food products that meet consumer preferences while maintaining product quality and functionality.

Exclusive Customer Landscape

The food texture market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the food texture market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, food texture market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ajinomoto Co. Inc. - This company specializes in providing innovative food texturizing solutions for various industries, including Soups, Beverages, Bakery, Confectionery, Dairy, Meat, Poultry and Seafood, Plant-Based Proteins, Ready Meals, Sauces, Dressings and Condiments, and Savory Snacks. Their offerings enhance product quality and consumer experience by addressing texture-related challenges.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ajinomoto Co. Inc.

- Archer Daniels Midland Co.

- Ashland Inc.

- CP Kelco US Inc.

- Deosen Biochemical (Ordos) Ltd.

- Estelle Chemicals Pvt. Ltd.

- Fiberstar Inc.

- Ingredion Inc.

- International Flavors and Fragrances Inc

- JELU WERK J. Ehrler GmbH and Co. KG

- Jungbunzlauer Suisse AG

- Kerry Group Plc

- Koninklijke DSM NV

- Levapan S.A.

- Riken Vitamin Co. Ltd.

- Royal Avebe

- SELECTAROME

- Tate and Lyle PLC

- Willy Benecke GmbH

- Cargill Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Food Texture Market

- In January 2024, Danish food company, Arla Foods, announced the launch of its new line of textured vegetable proteins, named "Vegi-Tex," to cater to the growing demand for plant-based alternatives in the food industry (Arla Foods Press Release, 2024). This expansion marks a strategic move to diversify its product portfolio and tap into the burgeoning plant-based food market.

- In March 2024, Ingredion Incorporated, a leading global provider of ingredient solutions, entered into a strategic partnership with Meatless Farm, a UK-based producer of plant-based meat alternatives, to develop innovative textured plant proteins for various food applications (Ingredion Incorporated Press Release, 2024). This collaboration aims to leverage Ingredion's texturizing expertise and Meatless Farm's market knowledge to create high-quality, sustainable plant-based products.

- In May 2024, DuPont Nutrition & Biosciences, a leading global biotech company, announced a significant investment of USD100 million in its texturized soy protein production facility in the United States (DuPont Nutrition & Biosciences Press Release, 2024). This expansion is expected to increase the company's production capacity by 50%, solidifying its position as a key player in the textured protein market.

- In April 2025, the European Commission approved the use of plant-based textured proteins derived from pea and soy in the production of meat alternatives, paving the way for a more diverse and sustainable food industry in Europe (European Commission Press Release, 2025). This regulatory approval is expected to boost the growth of the textured protein market in Europe, as it opens up new opportunities for companies to develop and market innovative plant-based products.

Research Analyst Overview

- The market is characterized by a significant focus on optimizing food material rheology through advanced techniques such as emulsion droplet size analysis and rheological characterization. Texture optimization strategies employ experimental design methods to understand the impact of processing technology on gel network properties and product formulation. Consumer acceptance studies and sensory descriptive analysis play a crucial role in texture-based quality control. Instrumental texture profile and shear stress measurement are essential tools for quality assurance protocols. Viscoelastic food structure analysis is a key trend, with researchers exploring protein denaturation effects on compressive force profile and mouthfeel evaluation. Sensory attribute scaling and panel training are integral to consumer preference mapping.

- Statistical data analysis is employed to understand the relationship between sensory perception and food microstructure. Furthermore, starch granule morphology and fat crystal polymorphism are essential factors influencing texture perception science. The market is continually evolving, with ongoing research in texture sensory evaluation and sensory panel training to enhance the overall consumer experience.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Food Texture Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

173 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.57% |

|

Market growth 2024-2028 |

USD 4.15 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.15 |

|

Key countries |

US, Malaysia, Indonesia, Germany, UK, South Korea, France, Canada, Brazil, Thailand, UAE, Mexico, China, Japan, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Food Texture Market Research and Growth Report?

- CAGR of the Food Texture industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the food texture market growth of industry companies

We can help! Our analysts can customize this food texture market research report to meet your requirements.

RIA -

RIA -