Generative AI In Gaming Market Size 2025-2029

The generative ai in gaming market size is valued to increase by USD 7.85 billion, at a CAGR of 39.2% from 2024 to 2029. Increasing demand for hyper personalized and dynamic gaming experiences will drive the generative ai in gaming market.

Major Market Trends & Insights

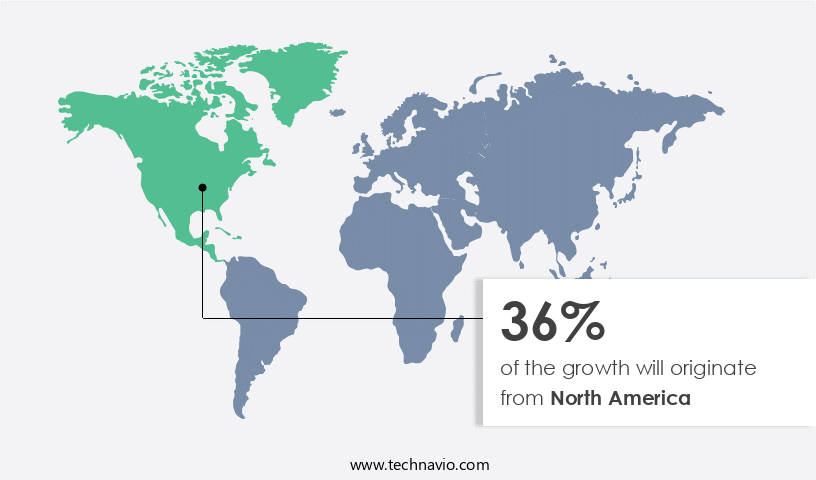

- North America dominated the market and accounted for a 36% growth during the forecast period.

- CAGR from 2024 to 2029 : 39.2%

Market Summary

- In the ever-expanding realm of gaming, Generative AI is making a significant impact by delivering hyper-personalized and dynamic experiences. This technology, which allows systems to create content in real-time, is revolutionizing the industry with the introduction of sophisticated AI companions and persistent non-player characters. These entities offer players unparalleled interaction, adapting to their choices and behaviors, creating a unique and immersive gaming experience. However, the integration of Generative AI in gaming is not without challenges. Ethical, copyright, and regulatory complexities persist, requiring careful navigation. For instance, ensuring AI companions exhibit appropriate behavior and respect user privacy is crucial.

- Moreover, copyright issues arise when AI generates content that mimics existing intellectual property. Regulatory bodies must establish clear guidelines to address these challenges and ensure a level playing field for developers. Despite these hurdles, the market for Generative AI in gaming is experiencing remarkable growth. As the technology continues to evolve, we can anticipate more sophisticated AI interactions, blurring the lines between human and machine, and redefining the boundaries of gaming.

What will be the Size of the Generative AI In Gaming Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Generative AI In Gaming Market Segmented and what are the key trends of market segmentation?

The generative ai in gaming industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

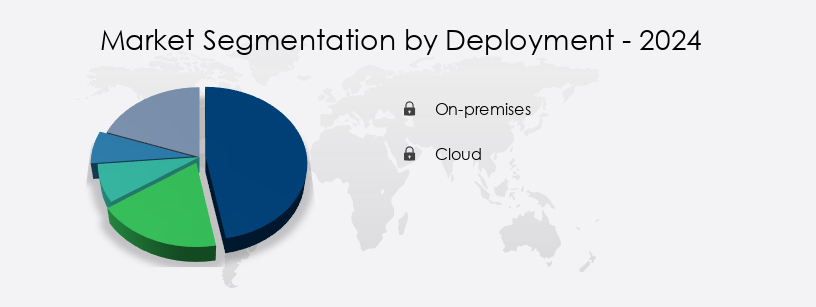

- Deployment

- On-premises

- Cloud

- Genre

- Action and adventure

- RPG

- Simulation

- Others

- End-user

- Game Studios

- Developers

- Artists

- Players

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Deployment Insights

The on-premises segment is estimated to witness significant growth during the forecast period.

The generative AI gaming market continues to evolve, with significant advancements in multiplayer game AI, quest generation systems, and level design automation. Real-time game rendering, dialogue generation systems, and dynamic difficulty adjustment are increasingly powered by AI-driven game design. Integration of physics engines, virtual reality, deep learning models, and procedural generation algorithms is becoming standard. Text-to-speech synthesis and player experience metrics are enhancing user interface design, while AI-powered cheat detection, collision detection systems, and interactive narrative generation optimize game balance and adaptive game mechanics.

Character animation systems, world simulation engines, natural language processing, and reinforcement learning agents enable more personalized player experiences. NPC behavior modeling and pathfinding algorithms are advancing AI-driven game testing and engine optimization. A notable statistic: AI-powered game testing has reduced development time by up to 30% in some cases. This market's ongoing activities reflect the industry's commitment to delivering immersive, intelligent, and engaging gaming experiences.

Regional Analysis

North America is estimated to contribute 36% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Generative AI In Gaming Market Demand is Rising in North America Request Free Sample

The market is currently witnessing significant growth and innovation, with North America leading the charge. This region, particularly the United States, is home to a high concentration of foundational AI research laboratories, major technology corporations, and game publishers. The presence of a vibrant and well-funded startup ecosystem, coupled with a mature consumer market, creates an ideal environment for the adoption and development of generative AI in gaming. Major technology firms in North America are at the forefront of developing the foundational models and hardware that power generative AI.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing rapid growth as game developers seek to create more immersive and dynamic gaming experiences. AI character behavior customization tools are revolutionizing non-player character (NPC) interactions, enabling more realistic and unpredictable behavior that keeps players engaged. Procedural generation of diverse game environments, powered by AI, offers virtually limitless possibilities for game designers, ensuring that each player's experience remains unique. Real-time AI-driven character interaction systems are another key trend, allowing players to engage in dynamic, evolving conversations with NPCs using natural language processing. Reinforcement learning for dynamic game balancing optimizes gameplay, ensuring a fair challenge for players at all skill levels.

Neural network-based game asset generation techniques produce high-quality, realistic game assets, reducing development time and costs. Advancements in AI-powered adaptive difficulty in action games ensure that the challenge level adjusts to each player's skill level, enhancing the overall gaming experience. Generative adversarial networks (GANs) are used to create realistic game assets, from textures to 3D models, enabling developers to produce visually stunning games. Deep learning models for predicting player behavior help game designers create more engaging and personalized experiences. Integration of physics engines with AI-driven game systems results in more realistic game environments and character interactions. AI-powered automated game testing and quality assurance tools streamline the development process, reducing the need for manual testing and ensuring a higher quality final product.

Compared to traditional game development methods, the adoption of generative AI technologies is accelerating the pace of innovation, enabling developers to create more engaging, immersive, and personalized gaming experiences. By 2025, it is estimated that over 80% of major game studios will have integrated generative AI into their development pipelines.

What are the key market drivers leading to the rise in the adoption of Generative AI In Gaming Industry?

- The escalating need for hyper-personalized and dynamic gaming experiences serves as the primary market catalyst, propelling growth in this sector.

- The market is experiencing significant growth due to the increasing player demand for hyper-personalized and dynamic gameplay. In advanced gaming markets, such as North America and Europe, gamers are moving away from pre-scripted narratives and repetitive gameplay towards emergent, player-driven worlds that offer genuine agency and unique outcomes. Traditional game development methodologies, while capable of producing high-fidelity content, struggle to meet this demand for bespoke experiences at scale. Manually creating branching narratives, reactive NPCs, and procedurally generated worlds is resource-intensive and often results in an illusion of choice rather than genuine dynamism.

- According to recent research, The market is expected to reach a significant market size, with an increasing number of gaming companies adopting AI technologies to enhance their games' player experience. The integration of generative AI in gaming is revolutionizing the industry by enabling the creation of emergent gameplay and more immersive gaming experiences.

What are the market trends shaping the Generative AI In Gaming Industry?

- The rise of dynamic AI companions and persistent non-player characters represents an emerging market trend in artificial intelligence technology.

- The market is experiencing a transformative shift, with the emergence of dynamic AI companions and persistent non-player characters (NPCs) becoming a defining trend. Traditional game design has long relied on static NPCs with pre-scripted dialogue trees and limited behavioral loops. However, the industry is moving towards creating memory-driven characters that engage in unscripted conversations, learn from player interactions, and evolve over time. This transition significantly enhances the gaming experience, making NPCs more than just quest dispensers or environmental dressing. This trend is most prominent in advanced markets like North America and Europe, where players demand high levels of narrative depth and immersion.

- The integration of generative AI in gaming is poised to revolutionize the industry, offering limitless possibilities for character development and player engagement.

What challenges does the Generative AI In Gaming Industry face during its growth?

- The growth of the industry is significantly hindered by the intricate ethical dilemmas, copyright issues, and regulatory complexities that necessitate careful navigation.

- The market is undergoing significant evolution, presenting both opportunities and challenges for developers and publishers. Ethical, copyright, and regulatory complexities pose a formidable hurdle, particularly in heavily regulated markets like North America and the European Union. This uncertainty arises from the use of large datasets, often sourced from the public internet, to train foundational generative models. These datasets frequently contain copyrighted materials, such as text, images, and code, which are ingested without consent or compensation for the original creators. Despite these challenges, the market's potential is substantial.

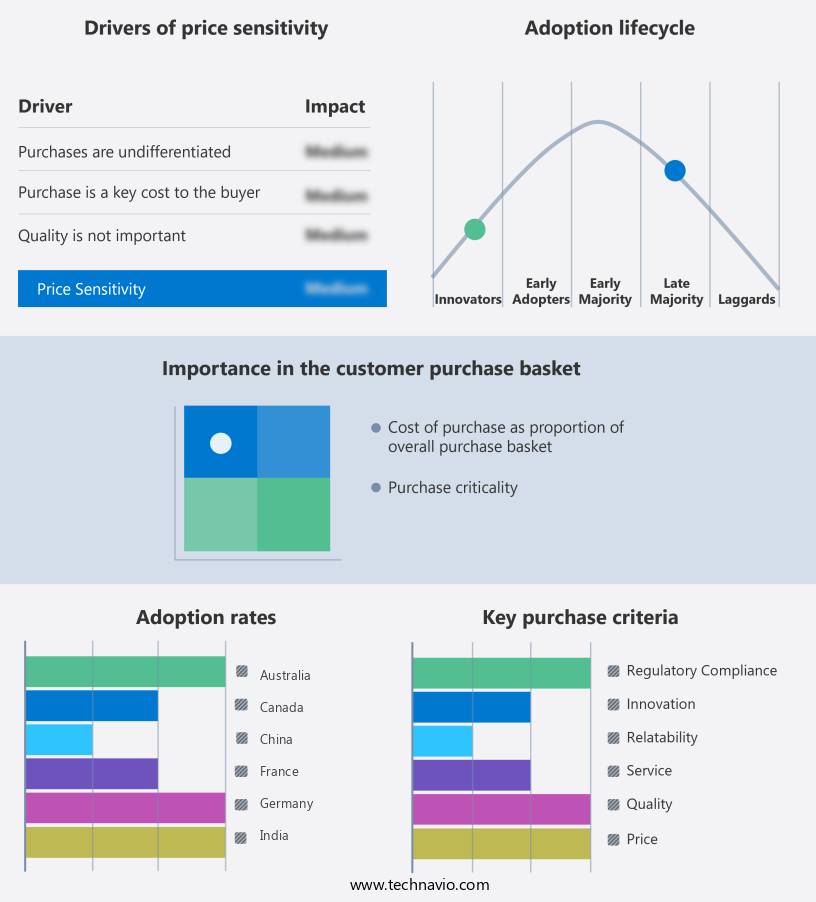

Exclusive Technavio Analysis on Customer Landscape

The generative ai in gaming market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the generative ai in gaming market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Generative AI In Gaming Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, generative ai in gaming market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Character.AI - The company pioneers generative AI in gaming through the development of realistic, personalized avatars and non-player characters (NPCs) using advanced models such as Variational Autoencoders (VAEs), Generative Adversarial Networks (GANs), and Recurrent Neural Networks (RNNs). These technologies enable ultra-realistic and customizable digital personas, enhancing user experience in the gaming industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Character.AI

- Charisma Entertainment Ltd.

- DEEPMOTION INC.

- Electronic Arts Inc.

- Epic Games Inc.

- Inworld AI

- Kinetix

- Latent Technology

- Luma AI

- Masterpiece Studio

- Microsoft Corp.

- Modl.ai

- OpenAI

- Promethean AI, Inc.

- Runway AI Inc.

- Series Entertainment Inc.

- Ubisoft Entertainment SA

- Unity Technologies Inc.

- Zibra AI, Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Generative AI In Gaming Market

- In January 2024, Unity Technologies, a leading platform for creating and operating interactive, real-time 3D (RT3D) content, announced the release of Unity ML-Agents, an open-source machine learning framework for training and deploying AI agents in Unity games (Unity Technologies, 2024). This development allowed game developers to create more intelligent and interactive non-player characters (NPCs) and player avatars, enhancing the overall gaming experience.

- In March 2024, Epic Games, the creator of Fortnite, partnered with NVIDIA to integrate NVIDIA's GauGAN AI-powered landscape design tool into Unreal Engine, enabling developers to create photorealistic landscapes for their games with minimal manual input (Epic Games, 2024). This collaboration brought significant advancements in the generation of realistic game environments using AI.

- In May 2024, Improbable, a leading UK-based tech company specializing in simulation technology, secured a USD200 million Series E funding round, bringing its total funding to over USD500 million (Improbable, 2024). The investment was aimed at further developing its SpatialOS platform, which enables developers to create complex, persistent, and scalable virtual worlds for games using AI.

- In April 2025, Valve Corporation, the video game developer and digital distribution company, introduced Steam Workshop Integration for AI-generated content, allowing developers to share and distribute AI-generated game assets, levels, and mods on the Steam platform (Valve Corporation, 2025). This initiative opened up new opportunities for creators to experiment with AI in gaming and for players to access a wider variety of AI-generated content.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Generative AI In Gaming Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

224 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 39.2% |

|

Market growth 2025-2029 |

USD 7850.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

36.3 |

|

Key countries |

China, South Korea, India, Australia, Japan, Germany, UK, France, US, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the ever-evolving world of gaming, generative AI is revolutionizing various aspects, from multiplayer experiences to game design and development. One notable area of advancement is the implementation of AI in quest generation systems, enabling dynamic and personalized missions that adapt to player behavior. Level design automation, fueled by deep learning models and procedural generation algorithms, generates unique environments, ensuring endless exploration possibilities. Real-time game rendering, driven by AI, enhances visual experiences by optimizing graphics and improving frame rates. Dialogue generation systems bring characters to life with natural, contextually relevant conversations, while dynamic difficulty adjustment ensures an engaging challenge for every player.

- AI-driven game design integrates physics engines and virtual reality, creating immersive experiences that mimic real-world interactions. Neural network architectures and reinforcement learning agents are employed for gameplay feedback systems, providing real-time adjustments to enhance player experience. Text-to-speech synthesis and natural language processing enable interactive narrative generation, allowing players to influence storylines through their choices. Game balance optimization, adaptive game mechanics, and character animation systems further enhance player engagement by adapting to individual playing styles. World simulation engines and AI-powered game testing streamline development processes, ensuring high-quality games and reducing the need for manual testing.

- Generative adversarial networks and personalized player experiences offer tailored content, while NPC behavior modeling and pathfinding algorithms create more realistic and responsive non-player characters. AI-driven storytelling and AI-powered cheat detection are the latest advancements, providing immersive narratives and maintaining fair gameplay. These innovations underscore the transformative impact of generative AI on the gaming industry, offering endless opportunities for growth and improvement. According to recent studies, the AI in gaming market is projected to grow at a significant rate, with a notable increase in investment and research in this area. This data underscores the immense potential of generative AI in gaming and its role in shaping the future of interactive entertainment.

What are the Key Data Covered in this Generative AI In Gaming Market Research and Growth Report?

-

What is the expected growth of the Generative AI In Gaming Market between 2025 and 2029?

-

USD 7.85 billion, at a CAGR of 39.2%

-

-

What segmentation does the market report cover?

-

The report segmented by Deployment (On-premises and Cloud), Genre (Action and adventure, RPG, Simulation, and Others), End-user (Game Studios, Developers, Artists, and Players), and Geography (North America, APAC, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for hyper personalized and dynamic gaming experiences, Navigating unresolved ethical, copyright, and regulatory complexities

-

-

Who are the major players in the Generative AI In Gaming Market?

-

Key Companies Character.AI, Charisma Entertainment Ltd., DEEPMOTION INC., Electronic Arts Inc., Epic Games Inc., Inworld AI, Kinetix, Latent Technology, Luma AI, Masterpiece Studio, Microsoft Corp., Modl.ai, OpenAI, Promethean AI, Inc., Runway AI Inc., Series Entertainment Inc., Ubisoft Entertainment SA, Unity Technologies Inc., and Zibra AI, Inc.

-

Market Research Insights

- The generative AI market in gaming continues to evolve, with advancements in technology driving innovation in various areas. Unsupervised learning algorithms, such as genetic programming and deep reinforcement learning, are increasingly being used for AI-powered content creation. Convolutional neural networks and recurrent neural networks are key technologies enabling the development of sophisticated AI agents. These agents employ exploration-exploitation balance, value functions, and reward functions to make informed decisions.

- For instance, deep reinforcement learning algorithms use Q-learning and policy gradients to optimize agent behavior. Additionally, transfer learning applications and model compression methods help reduce training time and improve performance. Despite these advancements, overfitting prevention techniques like data augmentation and semi-supervised learning remain essential to maintain the balance between model accuracy and generalization ability. As the market continues to grow, the focus will be on refining AI agents' decision-making algorithms, improving exploration-exploitation balance, and enhancing game state representation and world synthesis using graph neural networks and agent-based modeling.

We can help! Our analysts can customize this generative ai in gaming market research report to meet your requirements.

RIA -

RIA -