Game Development Software Market Size 2026-2030

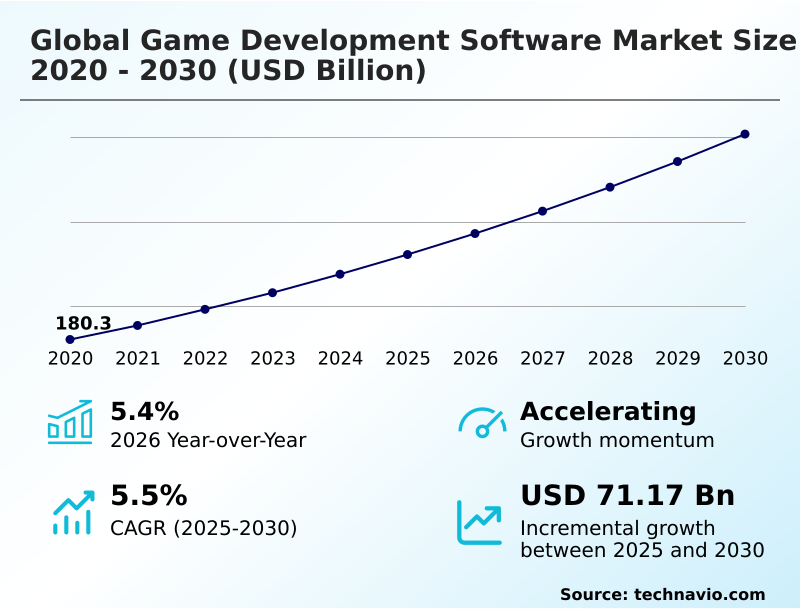

The game development software market size is valued to increase by USD 71.17 billion, at a CAGR of 5.5% from 2025 to 2030. Rapid growth of global gaming industry and expanding player base will drive the game development software market.

Major Market Trends & Insights

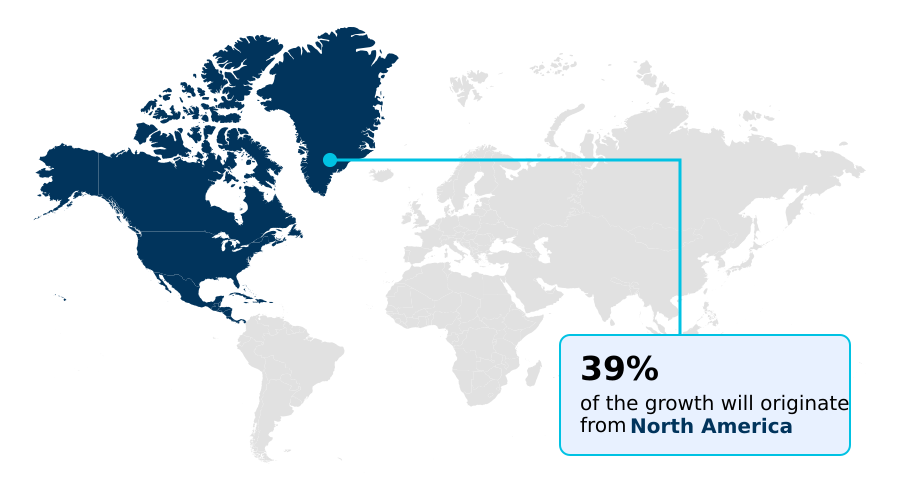

- North America dominated the market and accounted for a 39% growth during the forecast period.

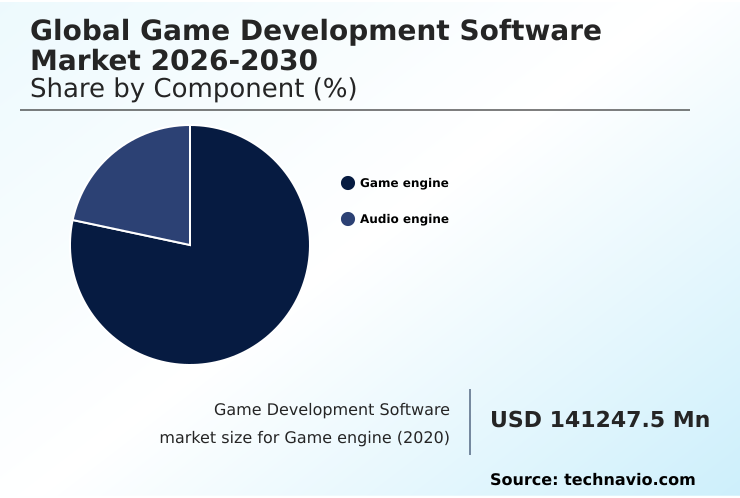

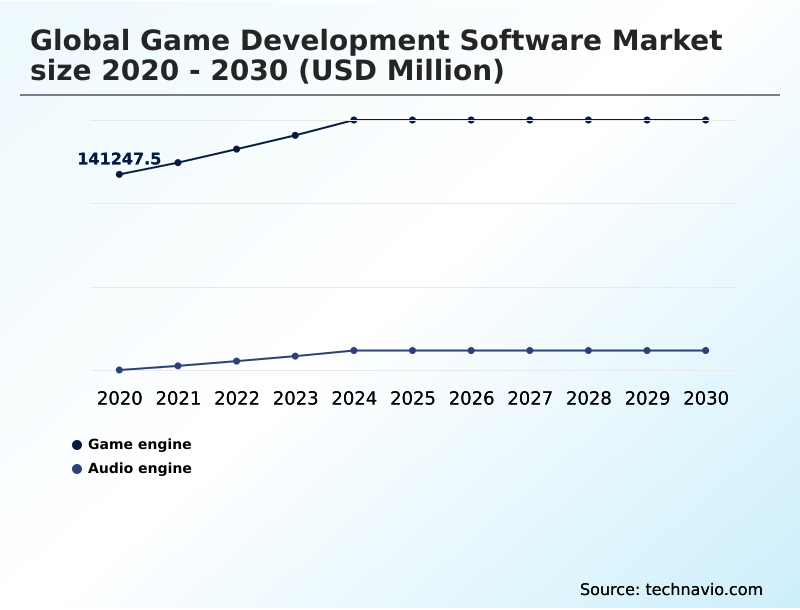

- By Component - Game engine segment was valued at USD 169.66 billion in 2024

- By End-user - Enterprises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 121.38 billion

- Market Future Opportunities: USD 71.17 billion

- CAGR from 2025 to 2030 : 5.5%

Market Summary

- The game development software market is undergoing a significant transformation, driven by the escalating demand for immersive, high-fidelity interactive entertainment across a broadening spectrum of platforms. The core of this market consists of sophisticated toolsets, from the foundational cross-platform game engine to specialized applications for animation and audio.

- Growth is propelled by the expanding global player base and the extension of game technologies into non-gaming sectors like architectural visualization and automotive design. Key trends shaping the landscape include the integration of artificial intelligence to streamline content creation, such as procedural generation of environments, and the shift toward cloud-based development environments that facilitate remote collaboration for globally distributed teams.

- For instance, a large studio can leverage a cloud-based pipeline to coordinate hundreds of artists and engineers, significantly reducing asset integration time. However, this progress is met with challenges, including the steep learning curve of advanced tools and the immense cost and complexity associated with developing top-tier, 'AAA' titles, which can inhibit smaller studios and independent creators from competing effectively.

- The industry's trajectory is toward greater accessibility and automation, aiming to democratize high-end production capabilities.

What will be the Size of the Game Development Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Game Development Software Market Segmented?

The game development software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Game engine

- Audio engine

- End-user

- Enterprises

- Individual

- Deployment

- Cloud-based

- On-premises

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- South Korea

- Europe

- UK

- Germany

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By Component Insights

The game engine segment is estimated to witness significant growth during the forecast period.

The game engine segment is the core of the market, providing the architectural framework for digital content creation tools.

A modern cross-platform game engine integrates a sophisticated real-time rendering engine with tools for physics-based rendering, enabling the creation of a compelling interactive 3d experience.

This evolution supports an interactive development workflow, where studios can achieve up to 40% faster iteration on design elements.

The use of a flexible gameplay scripting language and robust asset creation tools is critical for both the demanding aaa game production pipeline and more accessible indie game developer tools.

Beyond entertainment, these platforms are increasingly used as an architectural visualization engine and for complex simulation and training applications, driving demand for advanced mobile game optimization and streamlined real-time 3d creation.

The Game engine segment was valued at USD 169.66 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Game Development Software Market Demand is Rising in North America Get Free Sample

Regional dynamics are defined by distinct specializations and investment priorities. North America leads in creating the aaa game production pipeline, heavily utilizing advanced 3d modeling software and virtual production software for cinematic sequences.

The region's focus on high-fidelity visuals drives innovation in the cinematic sequence editor and particle effects editor.

In APAC, where market expansion outpaces North America, the focus is on mobile and online games, requiring strong non-player character AI and procedural animation techniques.

Europe excels in simulation and training applications and digital twin simulation, leveraging the physics simulation library and spatial audio engine for realism.

Emerging hubs are contributing to the decentralized asset marketplace, using advanced level design software to create unique interactive content for a global audience.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Developer focus is increasingly specialized, driving demand for tailored toolsets across diverse applications. Studios exploring game development software for vr are prioritizing spatial audio for immersive experiences, while those targeting mass-market adoption seek the best game engine for mobile. A key decision point involves a cross-platform development tools comparison, weighing efficiency against platform-specific performance.

- The use of ai in procedural content generation is becoming a standard practice for managing assets in large projects, automating tasks that were previously resource-intensive. Beyond entertainment, real-time rendering for architectural visualization is a rapidly growing segment.

- The shift to remote work has amplified the need for cloud collaboration tools for developers, while live-service titles require robust live ops management for service games and backend services for user authentication. For high-end productions, optimizing game performance on consoles and mastering the character rigging and animation pipeline remain critical skills.

- Developers are building multiplayer games with unreal and using visual scripting for prototyping to accelerate iteration. Success also depends on integrating monetization sdk in unity, creating cinematic sequences in-engine, and using effective tools for indie game marketing.

- As the industry evolves, expertise in automated testing for mobile games, developing games for the metaverse, and utilizing low-code platforms for 2d games will become even more crucial, especially as growth in regions like APAC outpaces North America, creating new market dynamics.

What are the key market drivers leading to the rise in the adoption of Game Development Software Industry?

- The rapid growth of the global gaming industry, coupled with an expanding player base, is a key driver for the game development software market.

- Key market drivers are centered on live services and the creator economy, which demand robust backend infrastructure and continuous engagement.

- The need for seamless cross-platform multiplayer experiences is fueling demand for a sophisticated multiplayer networking framework and scalable game server hosting.

- A comprehensive live operations backend, integrated with a game analytics platform, is critical for success, as live service titles demonstrate a 30% higher player retention rate.

- Effective monetization sdk integration and in-game economy management are essential, with player data analytics correlating to a 20% uplift in revenue.

- The push for graphical fidelity is supported by real-time ray tracing, while low-latency game streaming and esports broadcasting tools expand audience reach, all powered by backend as a service for games.

What are the market trends shaping the Game Development Software Industry?

- The rising adoption of real-time game engines is a prominent trend. This shift enables more interactive and efficient development workflows across the industry.

- Market trends are increasingly shaped by intelligent automation and immersive technologies. The adoption of a visual scripting interface is accelerating low-code game development, making complex creation more accessible. AI-driven game design is now central, with ai-driven animation and procedural content generation automating repetitive tasks.

- Studios are leveraging a cloud-based development environment to enable collaborative game development across global teams, improving project efficiency by over 25%. For building the next generation of interactive media, a dedicated virtual reality sdk and augmented reality toolkit are essential for immersive experience design.

- Furthermore, the rise of the creator economy tools is empowering a user-generated content platform, which is foundational to the emerging metaverse development platform, where user engagement is paramount.

What challenges does the Game Development Software Industry face during its growth?

- High development costs and the rising complexity of game creation present a key challenge affecting industry growth.

- Significant market challenges stem from rising production complexity and the high cost of quality assurance. The intricate character animation system and the resources required for photogrammetry asset creation increase development overhead. Crafting advanced visuals requires specialized shader development tools, while managing large projects necessitates robust version control integration.

- The process of console game porting can extend project timelines by up to 35%, complicated by the need for extensive game performance profiling using in-engine profiling tools. Ensuring quality across platforms requires comprehensive automated testing tools and effective game localization tools.

- Moreover, developers face pressure from rising costs for game security solutions and content delivery network for games, alongside competition on every asset store marketplace while working on procedural world building.

Exclusive Technavio Analysis on Customer Landscape

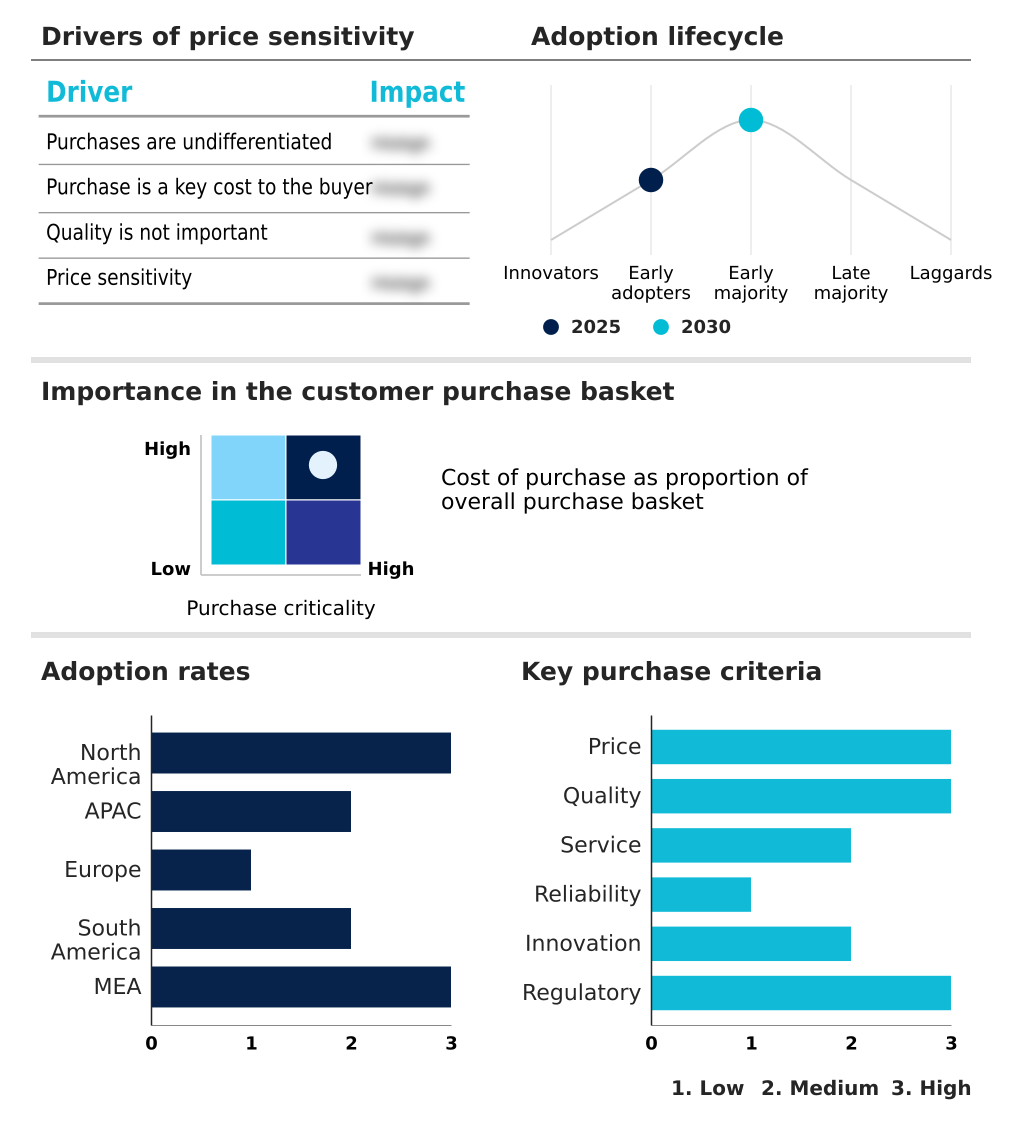

The game development software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the game development software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Game Development Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, game development software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon Web Services Inc. - Foundational offerings include real-time engines, cloud services, and specialized tools for modeling, animation, and live operations that power cross-platform interactive content development.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon Web Services Inc.

- Autodesk Inc.

- Cocos

- Crytek GmbH

- Defold Foundation

- Electronic Arts Inc.

- Epic Games Inc.

- Meta Platforms Inc.

- Microsoft Corp.

- NVIDIA Corp.

- Perforce Software Inc.

- Roblox Corp.

- Scirra Ltd.

- Side Effects Software Inc.

- Solar2D LLC

- Unity Technologies Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Game development software market

- In August 2024, the Godot Engine project launched version 4.3, which featured significant enhancements to its web export pipeline and tools for creating browser-based interactive content.

- In September 2024, Unity Technologies announced a major overhaul of its pricing model, canceling its proposed runtime fee in favor of an updated seat-based structure to provide stability for developers.

- In October 2024, Unity Technologies globally launched Unity 6, its next-generation platform, delivering major performance boosts through GPU-based workloads and introducing end-to-end multiplayer development workflows.

- In March 2025, NVIDIA expanded its Omniverse platform with a new suite of generative artificial intelligence tools designed to automate the creation of complex 3D environments using advanced neural rendering techniques.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Game Development Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 284 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.5% |

| Market growth 2026-2030 | USD 71173.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.4% |

| Key countries | US, Canada, Mexico, China, Japan, South Korea, India, Australia, Indonesia, UK, Germany, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, UAE, Saudi Arabia, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The creative pipeline integrates specialized technologies, starting with digital content creation tools like 3d modeling software and photogrammetry asset creation. These assets are managed within a cross-platform game engine, a real-time rendering engine enhanced with real-time ray tracing and physics-based rendering. This engine uses a physics simulation library and a gameplay scripting language to build an interactive 3d experience.

- A visual scripting interface and procedural world building accelerate development, while artists use a particle effects editor, shader development tools, and level design software. The character animation system benefits from ai-driven animation, and a spatial audio engine enhances immersion alongside a virtual reality sdk or augmented reality toolkit. A cinematic sequence editor crafts narratives.

- For live titles, a multiplayer networking framework, live operations backend, and game backend services are vital, supported by a game analytics platform and monetization sdk integration.

- A cloud-based development environment with version control integration, in-engine profiling tools, and automated testing tools can reduce bug-related rework by over 20%, critical for projects using a user-generated content platform or decentralized asset marketplace for low-latency game streaming.

What are the Key Data Covered in this Game Development Software Market Research and Growth Report?

-

What is the expected growth of the Game Development Software Market between 2026 and 2030?

-

USD 71.17 billion, at a CAGR of 5.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Game engine, and Audio engine), End-user (Enterprises, and Individual), Deployment (Cloud-based, and On-premises) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rapid growth of global gaming industry and expanding player base, High development costs and rising complexity of game creation

-

-

Who are the major players in the Game Development Software Market?

-

Amazon Web Services Inc., Autodesk Inc., Cocos, Crytek GmbH, Defold Foundation, Electronic Arts Inc., Epic Games Inc., Meta Platforms Inc., Microsoft Corp., NVIDIA Corp., Perforce Software Inc., Roblox Corp., Scirra Ltd., Side Effects Software Inc., Solar2D LLC and Unity Technologies Inc.

-

Market Research Insights

- Market dynamics are shaped by a confluence of technological innovation and evolving business models. An interactive development workflow, enabled by real-time 3d creation, is now standard in the aaa game production pipeline, improving asset iteration speeds by over 30%.

- The push for collaborative game development is supported by game server hosting and a robust backend as a service for games, essential for cross-platform multiplayer functionality. AI-driven game design and non-player character AI are transforming content creation, with procedural animation techniques reducing manual effort.

- For creators, indie game developer tools and low-code game development platforms democratize access, feeding the asset store marketplace and creator economy tools. The industry also extends into virtual production software, architectural visualization engine, digital twin simulation, and simulation and training applications.

- Monetization is driven by in-game economy management and player data analytics, with mobile game optimization and console game porting being critical for reach.

- Ensuring quality requires game performance profiling, game security solutions, a content delivery network for games, and robust game localization tools for a global audience, while esports broadcasting tools and the metaverse development platform represent new frontiers for immersive experience design and a dynamic lighting system.

We can help! Our analysts can customize this game development software market research report to meet your requirements.

RIA -

RIA -