Generative AI In Material Science Market Size 2025-2029

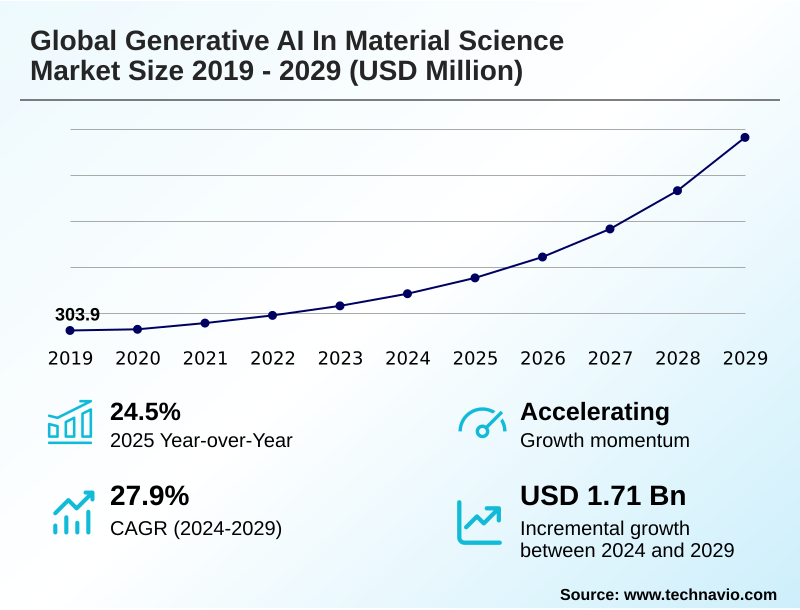

The generative ai in material science market size is valued to increase by USD 1.71 billion, at a CAGR of 27.9% from 2024 to 2029. Intensifying industrial demand for next-generation materials will drive the generative ai in material science market.

Major Market Trends & Insights

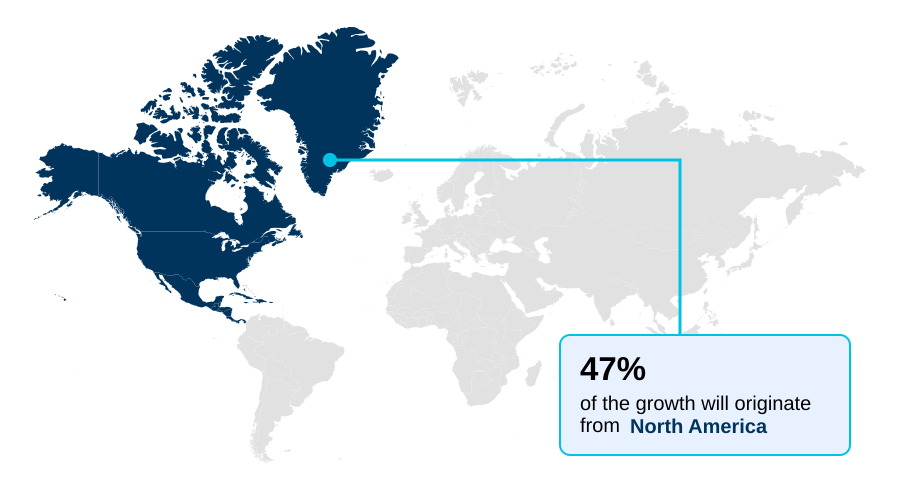

- North America dominated the market and accounted for a 46.9% growth during the forecast period.

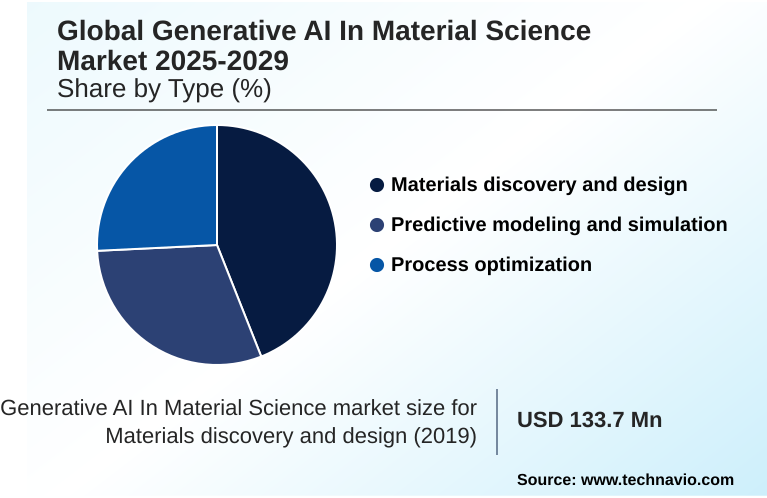

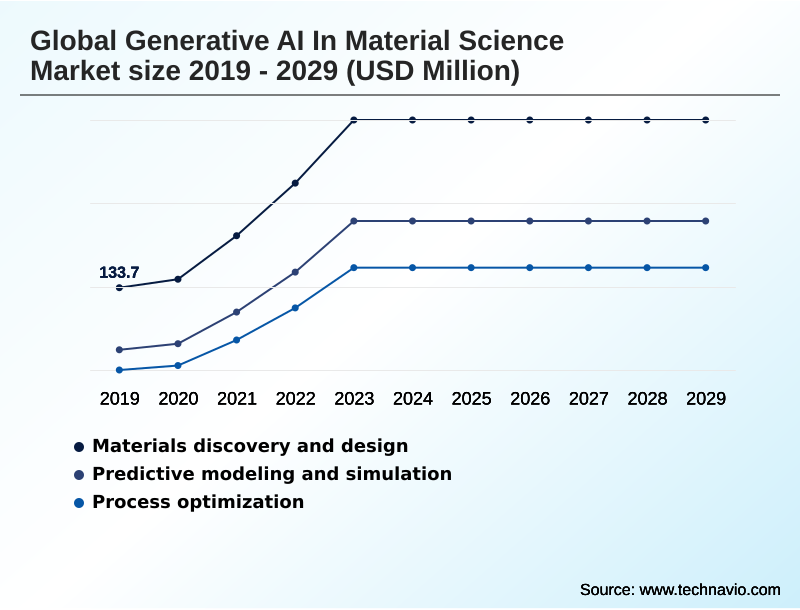

- By Type - Materials discovery and design segment was valued at USD 246.6 million in 2023

- By Deployment - Cloud-Based segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 2.11 billion

- Market Future Opportunities: USD 1.71 billion

- CAGR from 2024 to 2029 : 27.9%

Market Summary

- The generative AI in material science market is fundamentally reshaping industrial innovation by replacing traditional, linear R&D with accelerated, purpose-driven discovery. This market utilizes sophisticated algorithms to learn underlying physical principles from vast datasets, enabling an inverse design methodology where desired properties dictate the creation of novel molecular structures.

- This approach is critical in sectors facing material limitations, such as an aerospace firm seeking to develop a new lightweight alloy with specific thermal resistance and tensile strength. Instead of years of iterative testing, generative models can propose and computationally validate thousands of candidates in weeks.

- This capability is pivotal for developing everything from advanced battery cathode materials to sustainable polymers. However, realizing this potential is contingent on overcoming significant hurdles related to data quality and the practical synthesizability of computationally designed materials, which requires a deep integration of AI with physical laboratory validation.

- The convergence of high-performance computing, algorithmic advancements, and urgent industrial demand defines the dynamic landscape.

What will be the Size of the Generative AI In Material Science Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Generative AI In Material Science Market Segmented?

The generative ai in material science industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Materials discovery and design

- Predictive modeling and simulation

- Process optimization

- Deployment

- Cloud based

- On premises

- Hybrid

- Application

- Pharmaceuticals and chemicals

- Automotive and aerospace

- Electronics and semiconductors

- Energy storage and conversion

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Type Insights

The materials discovery and design segment is estimated to witness significant growth during the forecast period.

The materials discovery and design segment is pioneering a paradigm shift, moving beyond traditional R&D toward advanced computational materials science.

This evolution centers on inverse design methodology, where generative adversarial networks (GANs) and other models create novel molecular structures to meet predefined performance targets.

This approach is not merely theoretical; its application in designing solid-state electrolyte candidates has been shown to reduce initial screening timelines by over 90% compared to conventional methods.

The core objective is to leverage materials informatics and high-performance computing (HPC) to navigate and unlock vast, unexplored areas of chemical space exploration.

This enables the de novo design of next-generation electronics and high-energy-density batteries, making it the primary engine of innovation in the market.

The Materials discovery and design segment was valued at USD 246.6 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 46.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Generative AI In Material Science Market Demand is Rising in North America Get Free Sample

The geographic landscape of the generative AI in material science market is led by North America, which commands over 46% of the global opportunity, driven by its robust venture capital ecosystem and a high concentration of specialized talent.

The region hosts numerous self-driving laboratories focused on creating battery cathode materials and rare-earth-free magnets.

Europe is a strong secondary market, focusing its materials characterization efforts on sustainability and supporting the circular economy materials transition, with initiatives aiming for a 30% improvement in resource efficiency.

Meanwhile, the APAC region, backed by significant government investment, leverages the technology for manufacturing and securing technological self-sufficiency in strategic areas like decarbonization technologies.

The development of advanced aluminum alloys and ceramic matrix composites is a key focus, with regional players aiming to reduce reliance on foreign technology.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The practical application of generative AI in material science is rapidly expanding across diverse industrial challenges, moving beyond theoretical models to deliver tangible results. A primary focus is on generative AI for lightweight alloy design, crucial for the aerospace and automotive sectors, where new compositions are computationally generated to meet stringent strength-to-weight targets.

- In parallel, AI-driven catalyst discovery for carbon capture is gaining momentum, as inverse design of rare-earth-free magnets and custom catalysts enables the creation of materials with superior performance. Predictive modeling for battery material stability is essential for the energy transition, with generative AI for solid-state electrolyte discovery accelerating the development of safer, high-capacity batteries.

- This is complemented by foundation models for green hydrogen catalyst design, which address another key energy challenge. In the polymer and plastics industries, multi-objective optimization in polymer design and using generative AI to design biodegradable plastics are tackling sustainability goals head-on.

- The semiconductor industry is also a major beneficiary, using generative AI in semiconductor material exploration and generative models for next-generation semiconductors to overcome the limitations of silicon. This breadth of applications, from developing high-strength steel with generative models to AI-assisted design of biocompatible polymers, underscores the technology's transformative potential.

- For instance, the efficiency gains in this space are significant, with AI platforms for advanced composite materials demonstrating an ability to shorten development cycles by more than half compared to conventional methods.

What are the key market drivers leading to the rise in the adoption of Generative AI In Material Science Industry?

- The market is primarily driven by intensifying industrial demand for next-generation materials with unprecedented performance characteristics across sectors like aerospace, automotive, and electronics.

- The growth of the generative AI in material science market is propelled by a confluence of powerful drivers.

- The foremost is intense industrial demand for next-generation materials like high-strength steel alloys and biocompatible polymers, where traditional R&D can no longer meet accelerated timelines. Generative AI addresses this by enabling rapid materials discovery and design.

- Secondly, the global mandate for sustainability is creating a significant pull for circular economy materials and decarbonization technologies. AI-designed catalysts for green chemistry principles have demonstrated a potential to increase carbon capture efficiency by over 30%.

- Finally, the technological convergence of advanced computation and data proliferation, including physics-based simulations and quantum simulation, is a critical enabler.

- The accessibility of cloud-native R&D platforms has reduced upfront R&D costs for some firms by 50%, democratizing access to powerful material exploration tools.

What are the market trends shaping the Generative AI In Material Science Industry?

- A key market trend is the integration of generative AI with autonomous laboratories. This creates closed-loop discovery platforms that automate the design-build-test-learn cycle for accelerated material innovation.

- Key trends are reshaping the generative AI in material science market, moving from theoretical prediction to automated, end-to-end material innovation solutions. The integration of generative AI with self-driving laboratories is creating closed-loop discovery platforms, where automated synthesis and materials characterization are directly guided by AI. This approach can accelerate discovery cycles by up to 10 times compared to manual methods.

- Another significant trend is the development of domain-specific foundation models, which are pre-trained on vast datasets of molecular structures and material properties, lowering the entry barrier for organizations. Furthermore, the industry is shifting towards multi-objective optimization, enabling the design of materials that balance performance, cost, and manufacturability.

- This approach has improved the commercial viability of AI-designed sustainable polymers by 40% by ensuring they can be produced at scale.

What challenges does the Generative AI In Material Science Industry face during its growth?

- A key challenge affecting industry growth is the scarcity of high-quality, accessible, and standardized data required to train robust and generalizable AI models.

- Despite its potential, the generative AI in material science market faces significant challenges that temper its growth. The primary hurdle is data scarcity and the lack of standardized, high-quality information needed for robust predictive modeling and simulation and force field integration. This can lead to model inaccuracies of up to 20% when applied to novel material classes.

- Another major challenge is the chasm between computational prediction and physical viability, as many AI-generated materials are difficult to synthesize. This synthesis pathway prediction issue is a critical bottleneck. Lastly, high implementation costs and a severe scarcity of interdisciplinary talent are significant barriers, with talent shortages driving up project labor costs by an estimated 35%.

- This makes it difficult for smaller entities to adopt advanced techniques like large quantitative models (LQMs) for process optimization.

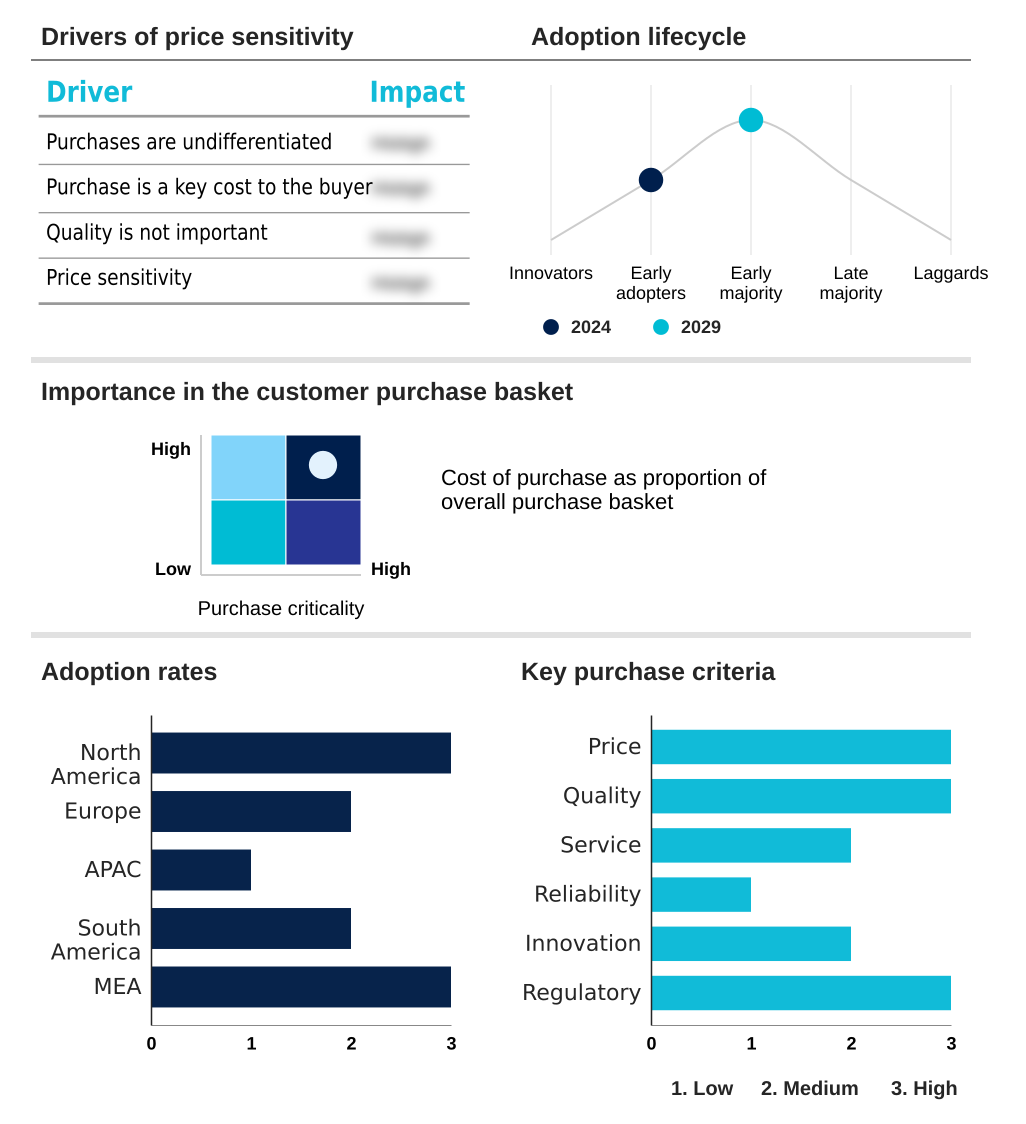

Exclusive Technavio Analysis on Customer Landscape

The generative ai in material science market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the generative ai in material science market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Generative AI In Material Science Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, generative ai in material science market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aionics Inc. - Delivers a dedicated materials informatics platform using AI to accelerate chemical and material product development through virtual lab functionalities and integrated data management.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aionics Inc.

- Arzeda Corp.

- BASF SE

- Citrine Informatics Inc.

- Dassault Systemes SE

- DeepMaterials LLC

- Google LLC

- IBM Corp.

- Kebotix Inc.

- Mat3ra Inc.

- MaterialsZone Ltd.

- Microsoft Corp.

- NVIDIA Corp.

- Optibrium

- Orbital Materials Inc.

- Phaseshift Inc.

- Quantum Generative Materials LLC

- sandboxAQ

- Schrodinger Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Generative ai in material science market

- In October 2024, BASF SE announced a strategic partnership with Kebotix Inc. to build a fully autonomous, AI-driven laboratory for discovering sustainable polymers, integrating Kebotix's self-driving lab technology with BASF's extensive materials data.

- In November 2024, NVIDIA Corp. launched 'NVIDIA Chimera,' a new cloud platform featuring foundation models specifically pre-trained on chemical and materials science data to accelerate the design of novel alloys and catalysts.

- In January 2025, Dassault Systemes SE completed the acquisition of Phaseshift Inc. for an undisclosed sum, integrating Phaseshift's rapid alloy design (RAD) platform into its BIOVIA portfolio to enhance its multi-objective material design capabilities.

- In April 2025, Orbital Materials Inc. announced it had secured a USD 50 million Series B funding round to scale its AI-powered platform, Orb, for designing cleantech materials, including novel carbon capture sorbents and green hydrogen catalysts.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Generative AI In Material Science Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 309 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 27.9% |

| Market growth 2025-2029 | USD 1705.3 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 24.5% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The generative AI in material science market is fundamentally altering the innovation pipeline, driven by the maturation of core technologies like generative adversarial networks (GANs) and, more recently, transformers and diffusion models. These algorithms enable a sophisticated inverse design methodology, allowing for the de novo design of materials with precisely tailored characteristics.

- The application of graph neural networks (GNNs) and tools like Graph Networks for Materials Exploration (GNoME) is facilitating unprecedented chemical space exploration, leading to the discovery of millions of new crystalline materials. This computational power is being applied to solve critical industrial problems, from creating novel metal-organic frameworks (MOFs) for carbon capture to designing high-performance solid-state battery materials.

- The integration of high-performance computing (HPC) with high-throughput screening has been particularly impactful. For instance, a single project demonstrated the ability to screen over 32 million potential material candidates, a scale that drastically accelerates the identification of viable options for real-world applications. This capability is enabling breakthroughs in atomistic design, molecular dynamics simulation, and understanding complex structure-property relationships.

What are the Key Data Covered in this Generative AI In Material Science Market Research and Growth Report?

-

What is the expected growth of the Generative AI In Material Science Market between 2025 and 2029?

-

USD 1.71 billion, at a CAGR of 27.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Materials discovery and design, Predictive modeling and simulation, Process optimization), Deployment (Cloud-Based, On-Premises, Hybrid), Application (Pharmaceuticals and chemicals, Electronics and semiconductors, Energy storage and conversion, Automotive and aerospace, Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Intensifying industrial demand for next-generation materials, Data scarcity and accessibility

-

-

Who are the major players in the Generative AI In Material Science Market?

-

Aionics Inc., Arzeda Corp., BASF SE, Citrine Informatics Inc., Dassault Systemes SE, DeepMaterials LLC, Google LLC, IBM Corp., Kebotix Inc., Mat3ra Inc., MaterialsZone Ltd., Microsoft Corp., NVIDIA Corp., Optibrium, Orbital Materials Inc., Phaseshift Inc., Quantum Generative Materials LLC, sandboxAQ and Schrodinger Inc.

-

Market Research Insights

- The generative AI in material science market is defined by a dynamic interplay of technological advancements and strategic industrial imperatives. The adoption of autonomous laboratories for material innovation solutions is accelerating R&D cycles, with some automated platforms demonstrating a 70% reduction in experimental validation time.

- Concurrently, physics-based simulations, enhanced by AI-driven molecular prediction and real-time experiment suggestion, are becoming central to AI-guided product development. This has enabled firms to improve formulation optimization accuracy by over 25% compared to traditional modeling. The pursuit of supply chain resilience is another critical factor, pushing industries toward discovering alternative materials.

- This approach is facilitated by cloud-native R&D platforms that offer scalable computational power, making advanced atomistic simulation accessible to a broader range of organizations and driving innovation in process optimization and materials discovery and design.

We can help! Our analysts can customize this generative ai in material science market research report to meet your requirements.

RIA -

RIA -