Healthcare Revenue Cycle Management (RCM) Software Market Size 2026-2030

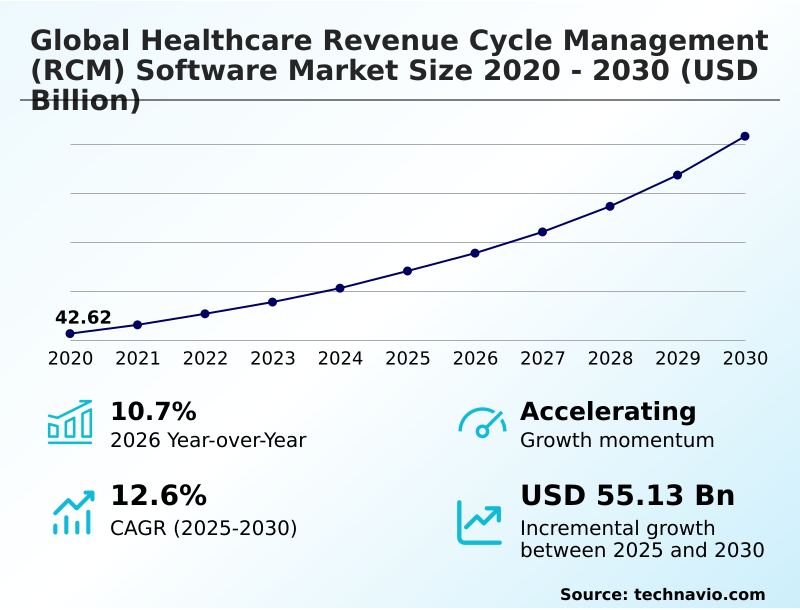

The healthcare revenue cycle management (rcm) software market size is valued to increase by USD 55.13 billion, at a CAGR of 12.6% from 2025 to 2030. Proliferation of agentic AI and autonomous coding workflows will drive the healthcare revenue cycle management (rcm) software market.

Major Market Trends & Insights

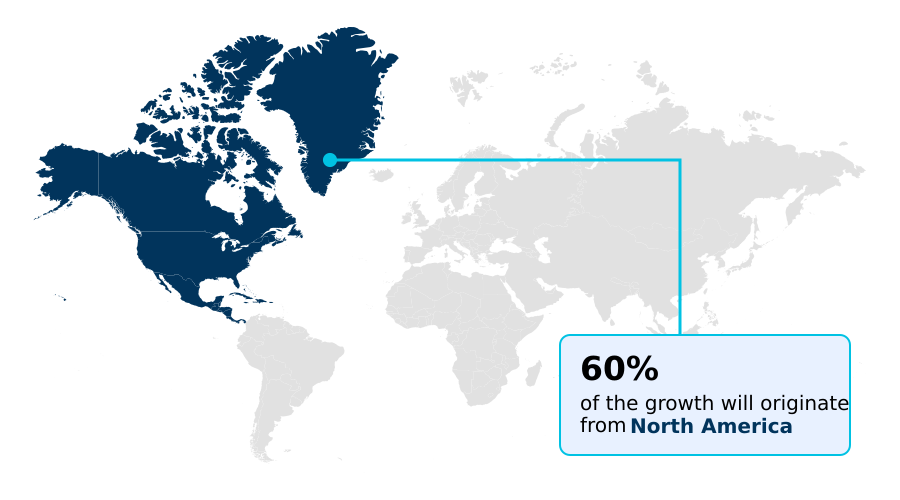

- North America dominated the market and accounted for a 60.1% growth during the forecast period.

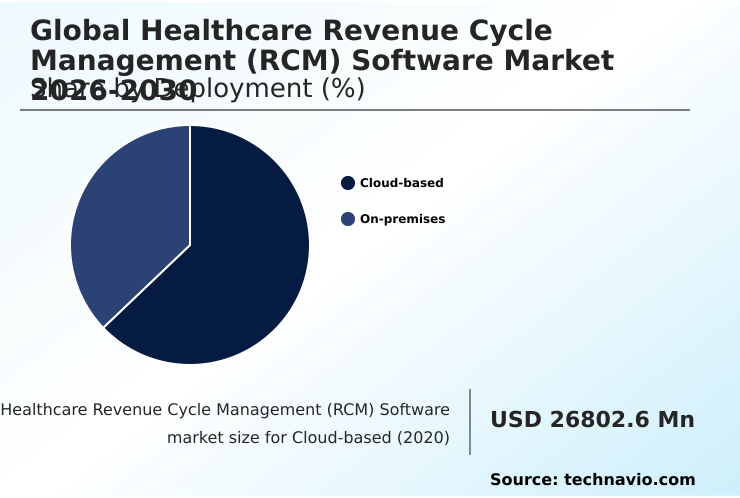

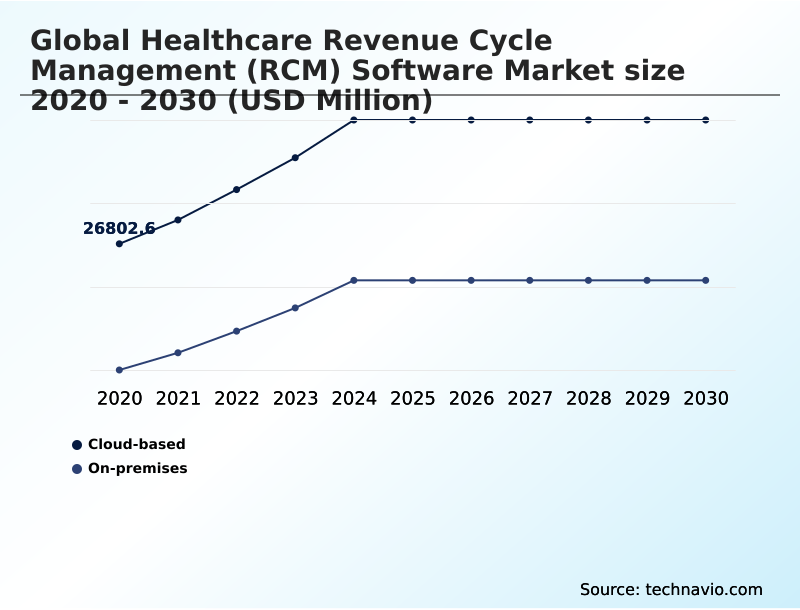

- By Deployment - Cloud-based segment was valued at USD 37.58 billion in 2024

- By End-user - Hospitals segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 80.73 billion

- Market Future Opportunities: USD 55.13 billion

- CAGR from 2025 to 2030 : 12.6%

Market Summary

- The Healthcare Revenue Cycle Management (RCM) Software market is undergoing a significant transformation, driven by the need to streamline financial operations and enhance revenue integrity. As healthcare providers face mounting pressure from complex reimbursement models and labor shortages, the adoption of advanced software has become a strategic imperative.

- The market is characterized by a strong trend towards automation, particularly through the use of agentic AI in RCM for tasks like medical coding automation and denial management. This technological shift addresses the high volume of administrative work, which can account for up to 40% of hospital expenses.

- For instance, a large health system can leverage an integrated platform for real-time eligibility verification and prior authorization automation, significantly reducing claim denials and accelerating cash flow. This proactive approach, which also includes robust patient financial engagement tools, moves beyond reactive problem-solving to create a more resilient and efficient financial ecosystem.

- The integration with EHRs and adherence to interoperability standards are also key, ensuring seamless data flow and billing compliance across the care continuum.

What will be the Size of the Healthcare Revenue Cycle Management (RCM) Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Healthcare Revenue Cycle Management (RCM) Software Market Segmented?

The healthcare revenue cycle management (rcm) software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- Cloud-based

- On-premises

- End-user

- Hospitals

- Physicians

- Medical labs

- Product type

- RCM services

- Integrated RCM software

- Standalone RCM modules

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Deployment Insights

The cloud-based segment is estimated to witness significant growth during the forecast period.

The market is rapidly expanding its adoption of cloud-based RCM solutions, as providers prioritize scalability, real-time data access, and reduced capital expenditure.

These healthcare billing platforms allow for the integration of complex billing processes, including payment posting automation, with disparate EHR systems. The shift is driven by the need for enhanced cybersecurity and frequent software updates to align with changing payer rules.

Advanced healthcare analytics embedded in these systems enable more accurate patient responsibility estimation and strategies for bad debt reduction, with some AI-native RCM automation software achieving significantly higher profitability profiles compared to legacy systems.

This model facilitates the use of predictive analytics to forecast patient payment behaviors and minimize denial rates, improving overall cash flow.

The Cloud-based segment was valued at USD 37.58 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 60.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Healthcare Revenue Cycle Management (RCM) Software Market Demand is Rising in North America Get Free Sample

The geographic landscape is led by North America, which accounts for over 60% of the incremental growth, driven by an aggressive deployment of agentic AI to achieve revenue integrity and automate denial management.

This region focuses on patient access management tools that provide real-time cost estimates. In contrast, Europe's market is shaped by regulatory compliance, with an emphasis on data governance and transparency in claims adjudication.

The APAC region is experiencing the most rapid expansion, with a growth rate of 13.6%, by leapfrogging legacy systems in favor of cloud-native architectures that ensure charge capture accuracy. South America is modernizing with integrated solutions for real-time financial oversight.

These regional dynamics highlight a global shift towards sophisticated healthcare financial management and medical claims processing tools, including patient self-service portals.

Market Dynamics

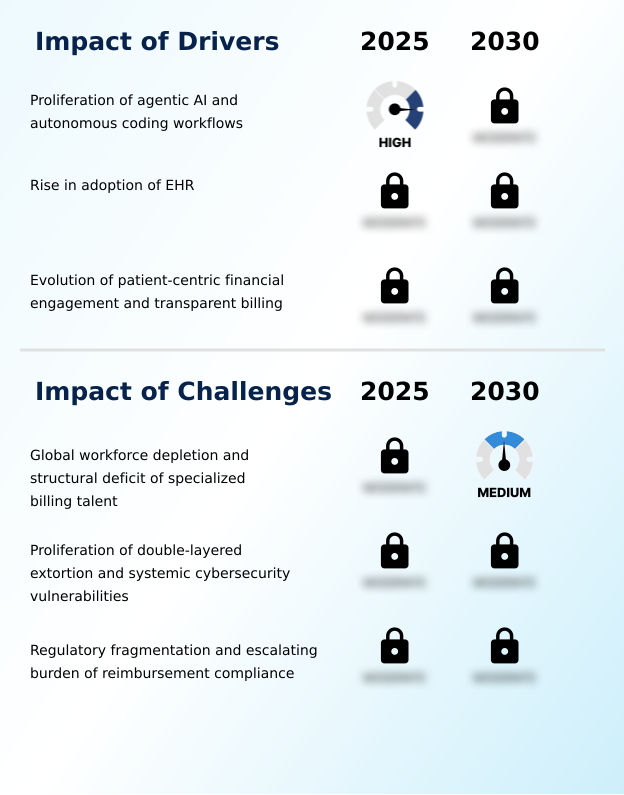

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The future of the healthcare RCM software market is centered on achieving complete financial and administrative autonomy. This evolution is powered by autonomous coding workflows for healthcare RCM, where AI interprets clinical notes and assigns codes without human review, significantly improving clean claim rate with automation.

- Concurrently, AI-driven tools for medical necessity validation are becoming essential for preventing denials before they occur, scrutinizing documentation against payer rules with precision. This proactive stance is complemented by patient cost estimation and transparency tools, which address surprise billing act compliance by providing clear, upfront financial information.

- The backbone of this ecosystem is the cloud-based RCM platform integration with EHR, creating a single source of truth. Enhanced interoperability for payer-provider data exchange allows for automating claims status inquiry and follow-up, drastically reducing administrative burden in healthcare. Digital payment rails in healthcare billing are also streamlining patient collections, while predictive analytics for patient payment propensity tailor financial counseling.

- Revenue integrity solutions for value-based care are crucial for tracking outcomes, while patient access solutions for financial clearance ensure viability from the first touchpoint. Even the most complex issues, like managing denials with machine learning algorithms, are becoming automated.

- This technology is not just for large hospitals; RCM software for specialty clinics and labs is also optimizing accounts receivable with AI, proving that advanced systems can reduce denial rates by more than double compared to legacy platforms, enhancing patient financial experience with software while mitigating cybersecurity for healthcare financial data.

- Ultimately, advanced analytics for RCM key performance indicators will guide strategic decisions in this new paradigm.

What are the key market drivers leading to the rise in the adoption of Healthcare Revenue Cycle Management (RCM) Software Industry?

- The proliferation of agentic AI and autonomous coding workflows is a key driver for market growth, reshaping ROI expectations for RCM software.

- A primary driver is the rapid shift from basic automation to agentic AI in RCM, which enables autonomous decision-making. These platforms use large language models for tasks like medical coding automation and prior authorization automation without human intervention.

- This shift is critical as providers face sophisticated payer algorithms; matching AI on the provider side allows for first-pass accuracy rates that human staff cannot achieve at scale.

- Furthermore, tight electronic health record (EHR) integration ensures that financial data is captured at the point of care for immediate financial clearance.

- The ability of AI in revenue cycle management to handle over 30% of routine administrative burdens, including real-time eligibility verification, has made it a core component of modern financial infrastructure, with seamless practice management software integration.

What are the market trends shaping the Healthcare Revenue Cycle Management (RCM) Software Industry?

- The market is shaped by a major trend toward cloud-native platforms. These platforms enable fully interoperable revenue ecosystems that enhance financial workflow management.

- A transformative trend involves the hyper-personalization of patient financial engagement, utilizing digital patient payment solutions and advanced payment rails to improve collection rates. As patient financial responsibility increases, providers are prioritizing software that mirrors modern e-commerce transparency. Tools using behavioral data now deliver customized financial counseling and flexible payment plans through mobile-first channels.

- This proactive engagement, supported by robust claims scrubbing, reduces the confusion that leads to non-payment. Additionally, the strategic push for interoperability between payers and providers, essential for value-based reimbursement models, is creating seamless data corridors.

- This alignment supports complex payer contract management and automated remittance advice processing, with real-time payment mechanisms seeing nearly 7% growth in the third quarter of 2025.

What challenges does the Healthcare Revenue Cycle Management (RCM) Software Industry face during its growth?

- A significant challenge affecting industry growth is the global depletion of the workforce and the structural deficit of specialized talent in medical billing and coding.

- A primary challenge is the structural deficit in specialized billing talent, which increases documentation errors and slows claims processing. While autonomous coding platforms are being deployed, their success is hampered by the capital needed to train staff for supervision. This labor shortage elevates days in accounts receivable and claim denial frequency, making collections optimization difficult.

- The necessity for human intervention in complex appeals and medical necessity validation means software alone is insufficient. Moreover, navigating fragmented global regulatory landscapes and ensuring billing compliance is increasingly difficult. The lack of robust interoperability standards also complicates data exchange with healthcare clearinghouse services, impacting overall revenue cycle optimization and automated denial prediction.

Exclusive Technavio Analysis on Customer Landscape

The healthcare revenue cycle management (rcm) software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the healthcare revenue cycle management (rcm) software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Healthcare Revenue Cycle Management (RCM) Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, healthcare revenue cycle management (rcm) software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3M Co. - Delivers advanced coding and reimbursement platforms that are engineered to optimize financial workflows and ensure comprehensive coding accuracy within complex healthcare provider environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- Athenahealth Inc.

- Chetu Inc.

- Cognizant Technology Solution

- CompuGroup Medical SE and Co.

- Epic Systems Corp.

- Experian Plc

- IBM Corp.

- OSP Labs

- ProHance

- Quest Diagnostics Inc.

- Qway Healthcare Inc.

- R1 RCM Inc.

- The SSI Group LLC

- TruBridge Inc.

- United Health Group Inc.

- Waystar Holding Corp.

- WellSky Corp.

- ZH Healthcare Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Healthcare revenue cycle management (rcm) software market

- In May, 2025, Smarter Technologies launched an AI-powered revenue management platform designed to help hospitals streamline administrative workflows and improve financial performance.

- In July, 2025, Astrana Health completed its acquisition of Prospect Health, a move indicating ongoing consolidation and the need for scalable RCM infrastructures in expanding health systems.

- In July, 2025, Omega Healthcare announced an expanded collaboration with Microsoft to deploy more than twenty generative and agentic AI solutions, aiming to automate high-friction tasks like medical coding.

- In November, 2025, the merger of AleraCare and Pure Healthcare formed a national platform for specialty care, driving demand for unified billing software to manage complex therapies.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Healthcare Revenue Cycle Management (RCM) Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 293 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 12.6% |

| Market growth 2026-2030 | USD 55132.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, Switzerland, China, India, Japan, South Korea, Australia, Singapore, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Healthcare Revenue Cycle Management (RCM) software market is rapidly evolving beyond simple billing functions into a strategic asset for financial health. The integration of agentic AI in RCM is central to this shift, automating complex processes like claims scrubbing and payer contract management. For boardroom decisions, the focus is on how these technologies impact operational budgets and compliance.

- For example, adopting platforms with robust clinical documentation improvement (CDI) and medical necessity validation capabilities directly addresses revenue integrity and mitigates audit risks. The move towards full electronic health record (EHR) integration and sophisticated healthcare analytics provides unprecedented visibility into financial performance, enabling proactive denial management and collections optimization.

- This technological adoption, which can reduce administrative tasks by over 30%, allows providers to manage accounts receivable more effectively. Key offerings now focus on end-to-end automation, from patient access management and financial clearance to final remittance advice processing and bad debt reduction, ensuring billing compliance and improving patient responsibility estimation.

What are the Key Data Covered in this Healthcare Revenue Cycle Management (RCM) Software Market Research and Growth Report?

-

What is the expected growth of the Healthcare Revenue Cycle Management (RCM) Software Market between 2026 and 2030?

-

USD 55.13 billion, at a CAGR of 12.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud-based, and On-premises), End-user (Hospitals, Physicians, and Medical labs), Product Type (RCM services, Integrated RCM software, and Standalone RCM modules) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Proliferation of agentic AI and autonomous coding workflows, Global workforce depletion and structural deficit of specialized billing talent

-

-

Who are the major players in the Healthcare Revenue Cycle Management (RCM) Software Market?

-

3M Co., Athenahealth Inc., Chetu Inc., Cognizant Technology Solution, CompuGroup Medical SE and Co., Epic Systems Corp., Experian Plc, IBM Corp., OSP Labs, ProHance, Quest Diagnostics Inc., Qway Healthcare Inc., R1 RCM Inc., The SSI Group LLC, TruBridge Inc., United Health Group Inc., Waystar Holding Corp., WellSky Corp. and ZH Healthcare Inc.

-

Market Research Insights

- The market dynamics are heavily influenced by a push toward automation and consumer-centric financial experiences. Providers are leveraging RCM automation software to address administrative burdens, with advanced platforms demonstrating the ability to reduce claim denials by up to 44% through automated denial prediction. The evolution toward value-based care models is also compelling the adoption of sophisticated healthcare financial management tools.

- A key driver is the integration of AI in revenue cycle management, which automates tasks and can absorb over 30% of routine administrative duties, freeing staff for higher-value work. This push for efficiency extends to the patient side, with a focus on patient payment solutions and digital patient engagement to improve collection rates and satisfaction.

- Interoperability standards remain critical for connecting disparate systems, enabling seamless data flow for better revenue cycle optimization.

We can help! Our analysts can customize this healthcare revenue cycle management (rcm) software market research report to meet your requirements.

RIA -

RIA -