Industrial Enclosures Market Size 2025-2029

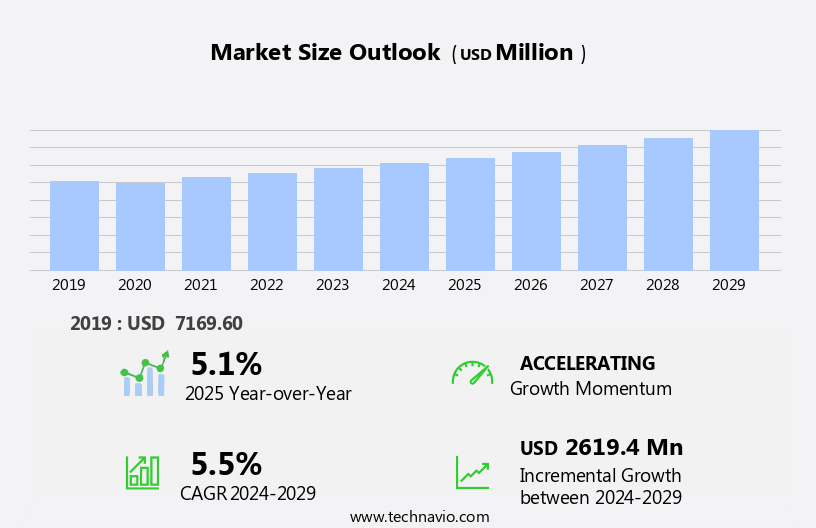

The industrial enclosures market size is forecast to increase by USD 2.62 billion at a CAGR of 5.5% between 2024 and 2029.

- The market is experiencing significant growth, driven by the increasing use of electrical and electronic equipment in manufacturing processes and the expansion of the smart cities industry. These trends are fueling the demand for robust and reliable enclosure solutions to protect and house these critical components. However, market growth is not without challenges. Volatile input costs, particularly for raw materials, have intensified price competition among market participants. Furthermore, regulatory hurdles impact adoption, as stricter safety and environmental regulations necessitate higher production costs and more stringent testing procedures. To capitalize on market opportunities and navigate these challenges effectively, companies must focus on innovation, operational efficiency, and strategic partnerships. Furthermore, the expansion of smart cities is leading to increased adoption of industrial automation systems, thereby boosting the market

- By investing in research and development to create advanced, cost-effective enclosure solutions that meet evolving regulatory requirements, companies can differentiate themselves and capture market share. Additionally, collaborating with suppliers and industry partners to mitigate the impact of volatile input costs and optimize supply chain operations can help ensure a stable and profitable business. Overall, the market presents significant growth potential for companies that can navigate these challenges and deliver value to customers through innovative, reliable, and cost-effective solutions. The increasing adoption of renewable energy sources and the electrification of industries will continue to drive the demand for industrial enclosures.

What will be the Size of the Industrial Enclosures Market during the forecast period?

- The market is characterized by continuous innovation, with manufacturers focusing on developing enclosures that adhere to stringent regulations while offering optimal deployment solutions. Enclosure support services and warranty are crucial aspects of the market, ensuring seamless integration and maintenance throughout the product lifecycle. Logistics and cost optimization are also key trends, with enclosure manufacturers providing simulation tools and value engineering to streamline the deployment process. Enclosure trends include advanced ergonomics, remote management, and security features, enabling businesses to optimize performance metrics and enhance safety. Standards and certification play a significant role in the market, with enclosure engineering prioritizing sustainability, durability, and integration. The market in the US is experiencing significant growth due to increasing global energy consumption in energy-intensive industries such as manufacturing, oil and gas, and power generation.

- Value-added services, such as customization, connectivity, and monitoring, are becoming increasingly important, providing businesses with flexibility and improved operational efficiency. Enclosure materials and finishes are also evolving to meet the demands of various applications, ensuring reliability, aesthetics, and compliance with industry regulations. As the market continues to evolve, enclosure manufacturers are focusing on enhancing enclosure performance metrics and engineering, enabling businesses to make informed decisions and optimize their industrial operations. Lifecycle management and safety remain top priorities, with enclosure manufacturers offering comprehensive solutions to help businesses navigate the complexities of enclosure deployment and maintenance.

How is this Industrial Enclosures Industry segmented?

The industrial enclosures industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Process

- Discrete

- Type

- Metallic

- Non-metallic

- Product

- Junction boxes

- Control cabinets

- Server racks

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

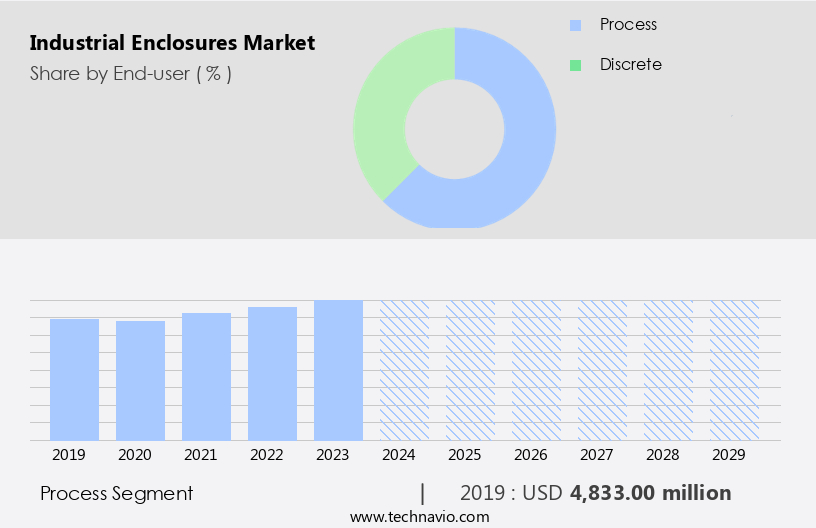

By End-user Insights

The process segment is estimated to witness significant growth during the forecast period. The market is driven by the need for protecting various types of equipment used in manufacturing processes from environmental hazards. In 2024, the process segment dominated the market, with significant demand coming from power generation, oil and gas, chemical and petrochemical, food and beverages, and pharmaceutical industries. These industries rely heavily on machines such as HVAC systems, compressors, motors, conveyors, pumps, and other process equipment that need to operate continuously. Exposure to dust and moisture can cause damage to motor control units or switchboards, leading to production halts and increased operational expenses. Indoor enclosures are commonly used to house control panels, PLCs, and HMI systems in various industries. These industries rely heavily on continuous operation of machinery such as HVAC systems, compressors, motors, conveyors, pumps, and other process equipment.

Enclosure design focuses on providing ingress protection, electromagnetic compatibility, and thermal management. Custom enclosures cater to specific application requirements, while panel builders and system integrators offer enclosure solutions for various industries. NEMA ratings and IP ratings ensure the required level of protection against various environmental factors. Military and defense applications require explosion-proof and corrosion-resistant enclosures, while food and beverage industries demand weatherproof and stainless steel enclosures. Energy and power sectors require heavy-duty enclosures for harsh environments, while data centers demand high-density, efficient enclosure cooling solutions. Rfi shielding and electromagnetic compatibility are essential for sensitive electronics manufacturing applications.

Enclosure manufacturing involves various processes, including enclosure assembly, labeling, testing, and installation. Enclosure accessories such as ventilation systems, heating, and enclosed systems cater to specific application requirements. Enclosure maintenance and security are crucial aspects of ensuring the longevity and functionality of industrial enclosures. In summary, the market is diverse, with various types of enclosures catering to different industries and applications. The focus on environmental protection, electromagnetic compatibility, and thermal management is driving market growth. Customization and innovation are key trends in the market, with ongoing research and development in materials, design, and manufacturing processes.

The Process segment was valued at USD 4.83 billion in 2019 and showed a gradual increase during the forecast period. StartFragment The Industrial Enclosures Market is driven by advancements in enclosure customization, simulation, and certification, ensuring compliance with enclosure standards and regulations. Enhanced enclosure finishes and aesthetics improve functionality and visual appeal, while enclosure ergonomics prioritize user experience. Growing emphasis on enclosure sustainability and lifecycle management enhances environmental responsibility. Enclosure value engineering and cost optimization streamline production, boosting efficiency. Improved enclosure logistics support seamless distribution, while robust enclosure warranty programs ensure reliability. Cutting-edge enclosure innovation expands applications and integration, enhancing reliability, durability, and safety. Advanced security features, connectivity, and monitoring optimize performance across industries.

Regional Analysis

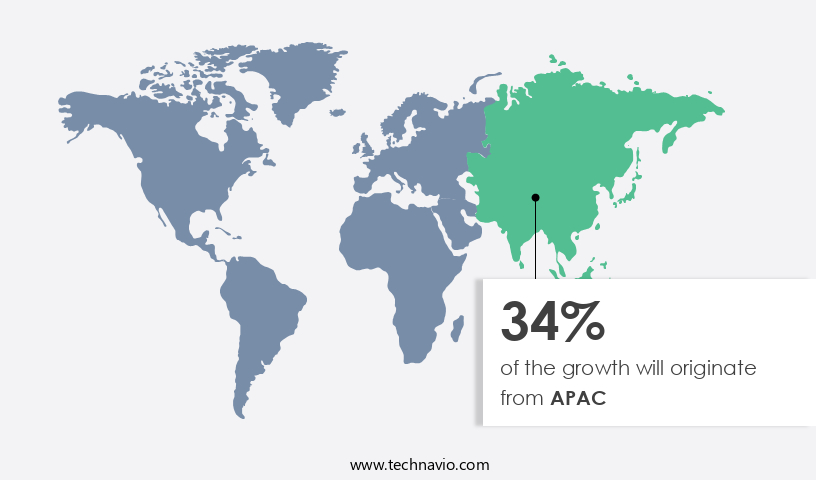

APAC is estimated to contribute 34% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. StartFragment The Industrial Enclosures Market continues to evolve, driven by advancements in enclosure simulation, certification, and adherence to enclosure regulations ensuring compliance and safety. Improved enclosure aesthetics enhance design appeal, while efficient enclosure lifecycle management optimizes longevity. Enclosure cost optimization remains a priority, balancing affordability with performance. Diverse enclosure applications demand seamless enclosure integration for enhanced operational efficiency. Strengthened enclosure reliability and durability ensure long-term functionality, while enclosure safety standards mitigate risks. Enhanced enclosure security features bolster protection, and enclosure connectivity facilitates smart monitoring and automation.

The market in Asia Pacific (APAC) is experiencing significant growth, driven by the process industries such as oil and gas, power, healthcare, and pharmaceutical. APAC is the fastest-growing regional market for industrial enclosures, with a shift from metallic to non-metallic enclosures observed in industries like automotive, electronics, and semiconductors. This trend is attributed to the increasing investments in process and discrete industries in the region. Additionally, some companies in APAC have seen increased production plant investments to meet the rising demand for industrial enclosures. However, electricity supply remains a challenge for many developing countries in the region.

Indoor enclosures, such as control panels and panel builders, continue to dominate the market. Custom enclosures, including NEMA rated and military & defense enclosures, are also gaining popularity due to their specific applications. Enclosure design, cooling, sealing, and labeling are essential considerations for various industries, including food & beverage, machine building, energy & power, and electronics manufacturing. Enclosure types like rfi shielding, thermal management, PLC enclosures, and hazardous location enclosures cater to specific industrial needs. Environmental protection, enclosure maintenance, and security are crucial factors for industries like oil & gas, chemical processing, and data centers. Light duty and heavy-duty enclosures, as well as modular and floor mount enclosures, offer flexibility and customization for various applications.

The market for industrial enclosures is diverse, with applications ranging from process control and system integration to industrial automation and enclosed systems. Enclosure testing, ventilation, and heating are essential for ensuring optimal performance and longevity. Access control, corrosion-resistant, and explosion-proof enclosures cater to specific industries and applications. The market in APAC is experiencing growth due to increasing investments in process and discrete industries. The trend towards non-metallic enclosures, customized solutions, and environmental protection is driving innovation and growth in the market. Companies are investing in production plants to meet the rising demand for industrial enclosures, addressing the challenges of electricity supply in the region.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the Industrial Enclosures market drivers leading to the rise in the adoption of Industry?

- The escalating reliance on electrical and electronic equipment in manufacturing processes serves as the primary market catalyst. Industrial electrical enclosures play a crucial role in safeguarding electronic components and instruments, including variable frequency drives (VFDs), low harmonic drives, vacuum contactors, and motor control centers, from external elements and electrical hazards. With the increasing focus on energy efficiency and cost savings, these enclosures have gained significant importance in various industries, particularly in regions experiencing power shortages. Enclosure design incorporates ingress protection ratings, ensuring the enclosures are dustproof and waterproof, while enclosure cooling systems maintain optimal operating temperatures. Panel builders and OEMs require custom enclosures to accommodate specific control panels and components.

- Nema ratings provide standardized specifications for enclosure design and sealing. In addition, enclosures are utilized in military and defense applications, as well as in the food and beverage industry, where strict hygiene requirements necessitate enclosure access control and easy cleaning. Free-standing enclosures offer flexibility in installation and can be used in both indoor and outdoor applications.

What are the Industrial Enclosures market trends shaping the Industry?

- The smart cities industry is experiencing significant growth, making it a noteworthy market trend for professionals. This sector's expansion presents valuable opportunities for innovation and development. The market is experiencing growth due to the increasing demand for protective housing solutions for advanced infrastructure in various industries, particularly in the context of smart city development. These enclosures provide a controlled environment for sensitive electrical and electronic devices, shielding them from environmental hazards such as dust, water, and extreme temperatures. The implementation of traffic management systems, which rely on real-time data gathering and communication between sensors and other devices, necessitates the use of enclosures to house and safeguard these components. Additionally, enclosures are essential for ensuring electromagnetic compatibility and thermal management, which are crucial for the optimal performance of various systems.

- System integrators and machine builders increasingly rely on enclosures for enclosure mounting, labeling, and testing to ensure the proper installation and functionality of their equipment. Heavy-duty enclosures offer enhanced protection against corrosion, while light-duty enclosures cater to less demanding applications. Overall, the market for industrial enclosures is driven by the need for reliable and durable housing solutions for the diverse range of electrical and electronic devices used in various industries.

How does Industrial Enclosures market faces challenges during its growth?

- The volatile input costs posing a significant challenge to businesses in the industry by intensifying price competition and hindering sustainable growth must be carefully managed to mitigate their impact. Industrial enclosures are essential components in various industries, including electronics manufacturing, process control, chemical processing, and data centers. These enclosures come in different types, such as HMI enclosures, outdoor enclosures, and explosion-proof enclosures, among others. Enclosure solutions cater to diverse applications, including enclosure ventilation, heating, EMI shielding, and hazardous location enclosures. The manufacturing of industrial enclosures involves major raw materials like stainless steel, rigid plastics, and aluminum. The price instability of these raw materials significantly impacts the production cost of industrial enclosures. While larger companies often secure long-term contracts with suppliers to mitigate the impact of raw material price fluctuations, smaller companies are more vulnerable.

- Industrial enclosures are primarily fabricated using a steel mono-block and incorporate steel parts for most accessories. Consequently, any volatility in steel prices directly influences the cost of industrial enclosures. Enclosure types like weatherproof enclosures and stainless steel enclosures are particularly sensitive to steel price changes due to their extensive use of this material.

Exclusive Customer Landscape

The industrial enclosures market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the industrial enclosures market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, industrial enclosures market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - This company specializes in the manufacturing and supply of industrial enclosures for various applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- AZZ Inc.

- BCH Electric Ltd.

- Chatsworth Products Inc.

- Eaton Corp. plc

- Emerson Electric Co.

- Friedhelm Loh Stiftung and Co. KG

- HTE Technologies

- Hubbell Inc.

- IMS Companies LLC

- Industrial Enclosure Corp.

- KDM Steel

- Legrand SA

- Marmon Holdings Inc.

- nVent Electric Plc

- Phoenix Contact GmbH and Co. KG

- ROLEC Gehause Systeme GmbH

- Rose Systemtechnik GmbH

- Sanmina Corp.

- Schneider Electric SE

- TAKACHI ELECTRONICS ENCLOSURE Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Industrial Enclosures Market

- In February 2024, Schneider Electric, a leading energy management and automation company, announced the launch of its new line of Modular Power Distribution Boards (MPDB) with integrated Industrial Enclosures. These enclosures offer enhanced protection against harsh environments and improve overall system efficiency (Schneider Electric Press Release, 2024).

- In July 2025, ABB, a global technology leader, entered into a strategic partnership with Honeywell to expand their joint offering in the market. This collaboration aims to provide integrated automation and electrical solutions to customers in the oil and gas, power, and industrial sectors (ABB Press Release, 2025).

- In October 2024, Siemens AG completed the acquisition of Sensotec, a leading provider of industrial sensors and enclosures. This acquisition strengthened Siemens' portfolio in the field of industrial automation and digitalization, enabling the company to offer more comprehensive solutions to its customers (Siemens AG Press Release, 2024).

- In March 2025, the European Union introduced new regulations on the RoHS2 directive, which includes stricter requirements for industrial enclosures. These regulations aim to reduce the use of hazardous substances in electronic and electrical equipment, promoting sustainable manufacturing practices in the industry (European Commission, 2025).

Research Analyst Overview

The market showcases a dynamic and evolving landscape, with various sectors integrating innovative enclosure solutions to meet their unique requirements. Machine building applications demand robust and custom enclosures, ensuring ingress protection and environmental sealing. Server enclosures in data centers prioritize thermal management and electromagnetic compatibility. Industries such as energy & power and military & defense necessitate heavy-duty enclosures with high NEMA ratings and RFI shielding for optimal performance and protection. In the food & beverage sector, corrosion-resistant and weatherproof enclosures are essential for maintaining hygiene and operational efficiency. System integrators play a crucial role in designing and implementing enclosure systems for diverse applications, from control panels to HMI enclosures.

Enclosure labeling and mounting solutions cater to the need for organization and ease of installation. Emerging trends include thermal management systems, PLC enclosures, and enclosure testing to ensure optimal performance and longevity. Enclosure ventilation and heating solutions cater to the demands of harsh environments, such as chemical processing and hazardous locations. The market continues to unfold with ongoing advancements in materials, such as stainless steel and aluminum, and enclosure types, including modular and explosion-proof designs. Enclosure accessories, including floor and wall mount enclosures, further expand the market's versatility. Environmental protection and security are paramount, with enclosure solutions addressing access control and IP ratings.

The market's continuous evolution underscores its importance in various industries, from industrial automation and electronics manufacturing to oil & gas and process control.

Dive into Technavio's strong research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Industrial Enclosures Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

220 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.5% |

|

Market growth 2025-2029 |

USD 2.62 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

5.1 |

|

Key countries |

US, China, Germany, India, UK, Japan, Canada, France, South Korea, and Australia |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Industrial Enclosures Market Research and Growth Report?

- CAGR of the Industrial Enclosures industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the industrial enclosures market growth of industry companies

We can help! Our analysts can customize this industrial enclosures market research report to meet your requirements.

RIA -

RIA -