Insulated Water Bottles Market Size and Growth Forecast 2026-2030

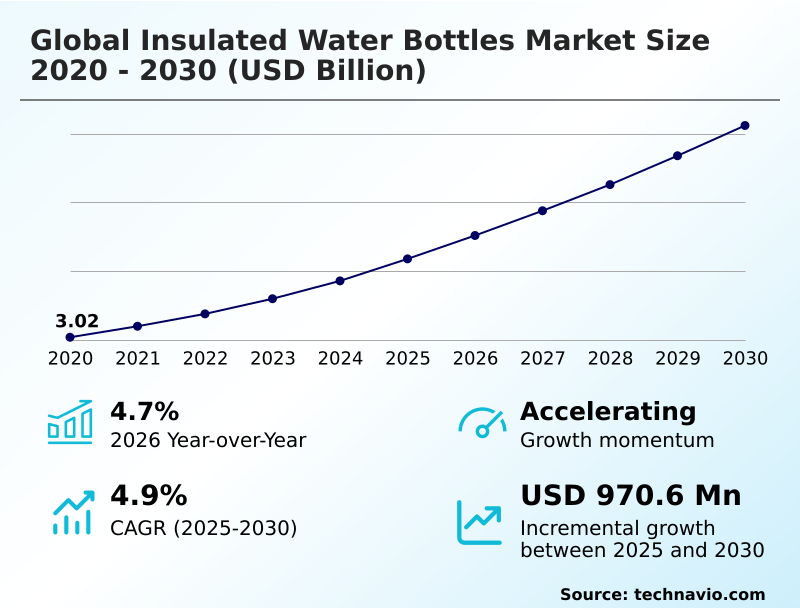

The Insulated Water Bottles Market size was valued at USD 3.59 billion in 2025 growing at a CAGR of 4.9% during the forecast period 2026-2030.

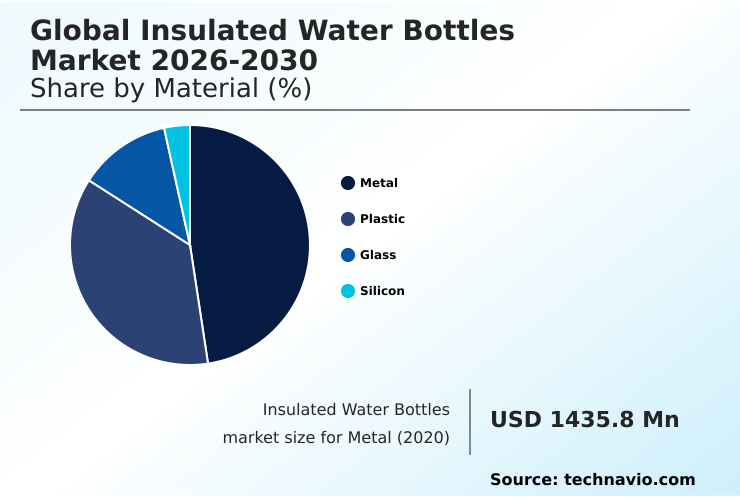

APAC accounts for 38.3% of incremental growth during the forecast period. The Metal segment by Material was valued at USD 1.66 billion in 2024, while the Big mouth segment holds the largest revenue share by Product Type.

The market is projected to grow by USD 1.54 billion from 2020 to 2030, with USD 970.6 million of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Insulated Water Bottles Market Overview

The insulated water bottles market is shaped by a confluence of health-conscious consumerism and stringent environmental mandates. A profound shift away from disposable packaging, driven by regulations like the EU Single-Use Plastics Directive, structurally supports demand for durable, reusable beverage containers. This is complemented by a wellness culture that positions consistent hydration as a key health metric. In practice, a corporate campus implementing a ban on single-use plastics will often provision employees with co-branded bottles featuring a powder coat finish, turning a policy change into a large-scale procurement driver. With APAC accounting for approximately 38% of the incremental growth, the global dynamic is a blend of mature market saturation in the West and rapid first-time adoption in emerging economies. The technical focus remains on enhancing thermal retention through innovations like copper lining and improving user experience with features such as a modular design and advanced leak-proof lid mechanisms. The industry's trajectory is toward creating products that are both high-performance tools and symbols of personal commitment to sustainability and health, integrating non-toxic materials throughout the product lifecycle.

Drivers, Trends, and Challenges in the Insulated Water Bottles Market

Strategic decision-making for firms is increasingly complex, navigating a landscape where the choice between stainless steel vs glass water bottle is no longer just about material but about supply chain resilience and brand positioning.

The EU's Circular Economy Action Plan, for instance, pressures companies to design for longevity and recyclability, influencing material selection toward recycled stainless steel and away from plastics.

An operational scenario involves a product development team evaluating the total cost of ownership for a new line; choosing a durable, chip-resistant coating adds upfront cost but reduces warranty claims and enhances the brand's premium perception, a key factor when creating an insulated tumbler with handle and straw for a competitive market segment.

Sourcing decisions are critical; a reliance on a single region for manufacturing creates vulnerabilities, whereas diversifying suppliers, although potentially increasing costs by 5-10%, mitigates risks from trade tariffs and logistical disruptions.

The question of what is the best insulated bottle for hiking is answered through a combination of lightweight material choice and a secure, leak-proof insulated bottle for travel, demonstrating how use-case-specific engineering drives value.

Ultimately, success hinges on balancing performance, such as creating an insulated water bottle for hot and cold beverages, with a transparent, sustainable narrative that resonates with environmentally conscious consumers.

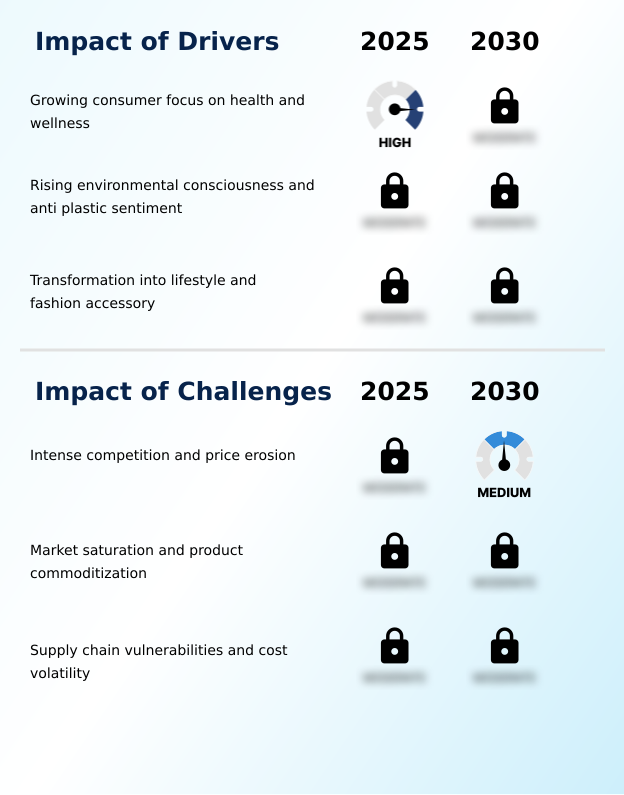

Primary Growth Driver: The market's primary driver is the growing consumer focus on health and wellness, elevating hydration to a central pillar of a healthy lifestyle.

Market growth is fundamentally driven by the product's successful transformation from a utilitarian item into a form of brand identity expression and a key fitness accessory.

This shift, amplified by social media, encourages a replacement cycle based on style and seasonality rather than just product failure. This accessory-fication allows brands to command premium prices.

A parallel driver is the powerful anti-plastic movement, which positions the insulated bottle as a visible and tangible sustainable hydration solution.

This consumer-led momentum is structurally reinforced by corporate wellness programs and institutional bans on disposable plastics, creating a consistent demand pipeline.

This confluence of environmental consciousness and lifestyle branding propels the market forward, turning a simple reusable beverage container into a statement piece with significant cultural and commercial value.

Emerging Market Trend: The integration of smart technology and deep personalization options are transforming insulated water bottles from simple containers into connected wellness devices that reflect individual identity.

Key trends are pushing products into new categories, blurring the lines between drinkware and consumer electronics. The integration of smart bottle technology, utilizing Bluetooth standards for connectivity, enables features like hydration tracking and provides a platform for ongoing user engagement. This move toward a connected personal hydration device is a significant avenue for creating premium product tiers.

Beyond digital enhancements, there is a strong push toward multi-functional design, with innovations like integrated storage compartments for keys or supplements and advanced, all-in-one lids that offer multiple drinking methods. Another prominent trend is the adoption of UV-C self-cleaning technology, which addresses consumer demand for improved hygiene and convenience.

These advancements are indicative of a market that is innovating beyond simple thermal performance to offer enhanced utility and a more integrated wellness experience.

Key Industry Challenge: Intense competition from a fragmented landscape of brands and private labels creates significant price erosion, challenging sustained profitability.

A critical structural challenge is the high dependency on a geographically concentrated supply chain, exposing the market to significant volatility. The majority of manufacturing is centered in a few regions, making the industry susceptible to disruptions from trade policy, geopolitical tensions, and logistical bottlenecks, which can impact the availability of products featuring an ergonomic handle or specific lid types.

Furthermore, the cost of core raw materials, particularly food grade stainless steel, is subject to global commodity price fluctuations, which can directly compress profit margins in a highly competitive retail environment. Navigating these supply chain vulnerabilities requires sophisticated risk management.

Adherence to increasingly stringent ESG reporting standards, like those from the IFRS Foundation, adds another layer of complexity, demanding greater transparency in sourcing and manufacturing processes for all components, including those made of BPA-free plastic.

Explore Full Market Dynamics Analysis Request Free Sample

Insulated Water Bottles Market Segmentation

The insulated water bottles industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Material Segment Analysis

The metal segment is estimated to witness significant growth during the forecast period.

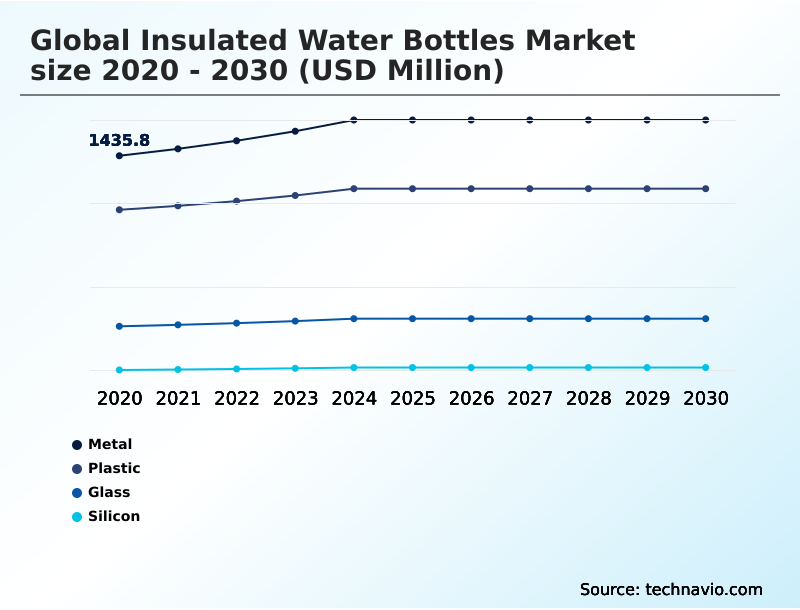

The metal segment, primarily utilizing food grade stainless steel, forms the foundation of the market. Its dominance is anchored in the superior performance of double wall vacuum insulation, which ensures exceptional thermal retention.

This technology, combined with the inherent durability and flavor neutrality of 18/8 stainless steel, positions these products as a premium, long-lasting choice.

Growth is driven by the alignment with sustainable hydration solution demands, as consumers seek robust alternatives to single-use plastics.

Differentiation is achieved not just through technical prowess but through branding that associates products with an eco-conscious consumerism, advanced powder coat finish options for grip and aesthetics, and innovations in leak-proof lid designs.

The segment's significance is underscored by its substantial contribution to the overall market revenue.

The Metal segment was valued at USD 1.66 billion in 2024 and showed a gradual increase during the forecast period.

Insulated Water Bottles Market by Region: APAC Leads with 38.3% Growth Share

APAC is estimated to contribute 38.3% to the growth of the global market during the forecast period.

The global geographic landscape is characterized by a divergence between mature and emerging regions. North America and Europe, representing a combined market opportunity of over 51%, are sophisticated markets where growth hinges on replacement cycles and the lifestyle accessory trend.

Here, purchasing decisions are influenced by brand identity and advanced features. In contrast, APAC, which contributes over 38% of the market opportunity, is a high-growth engine fueled by rising disposable incomes and first-time adoption.

Government actions, such as the plastic bottle ban in Assam, India, act as significant catalysts, creating structural demand for a reusable beverage container.

This regional disparity requires manufacturers to employ distinct strategies, balancing premium, feature-rich offerings like a cup holder compatible base for developed markets with durable, cost-effective sustainable hydration solution models for price-sensitive regions.

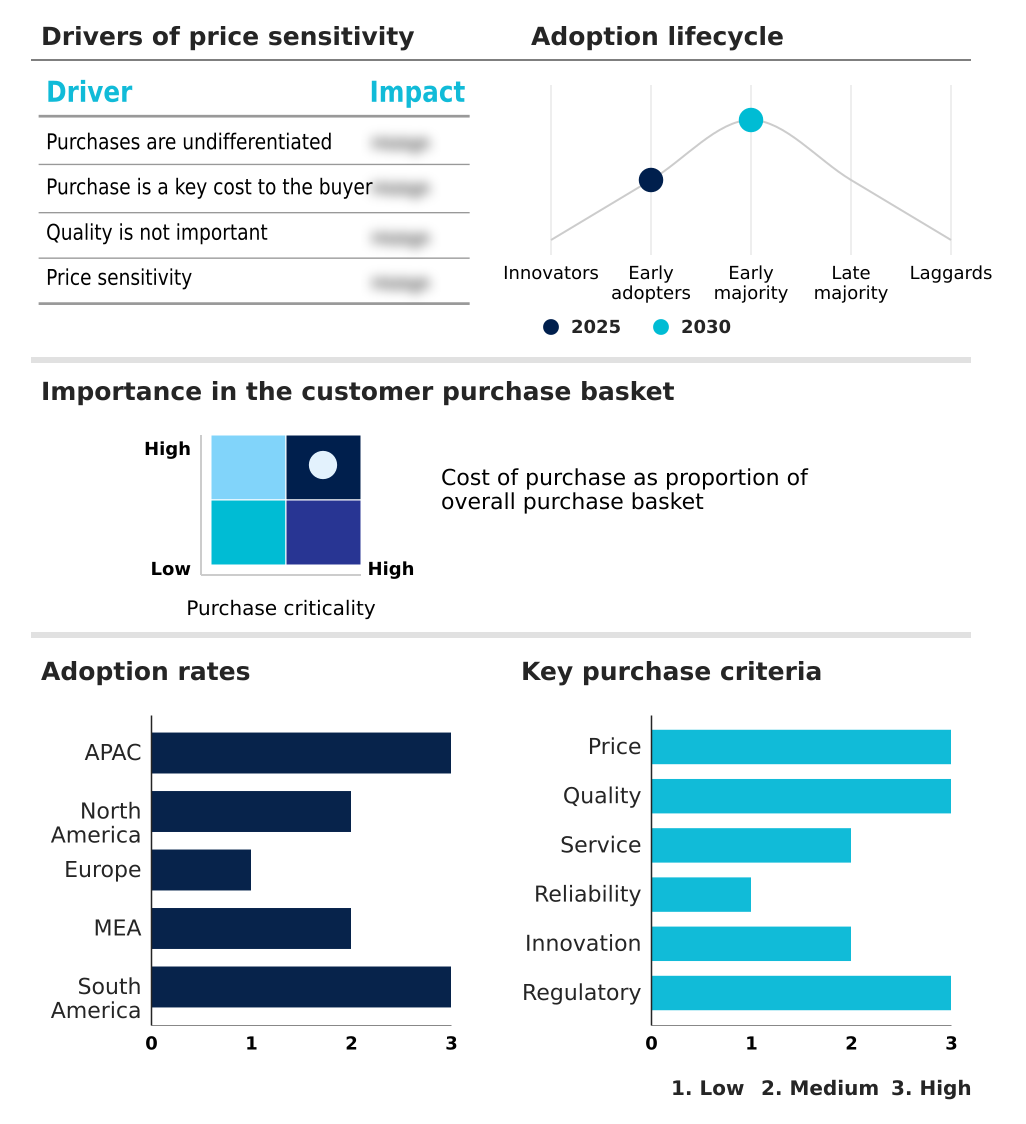

Customer Landscape Analysis for the Insulated Water Bottles Market

The insulated water bottles market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the insulated water bottles market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Insulated Water Bottles Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the insulated water bottles market industry.

Bivo LLC - The company offers performance-engineered hydration solutions specifically designed for the rigorous demands of cycling and outdoor recreational activities.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Bivo LLC

- Black Blum

- CamelBak Products

- Chillys Bottles Ltd.

- Contigo Brands

- Klean Kanteen

- MIRA Brands

- Nalge Nunc International Corp.

- Pacific Market International LLC

- RTIC Outdoors LLC

- S well

- SIGG Switzerland Bottles AG

- Simple Modern LLC

- Steel Technology LLC

- Thermos LLC

- Tiger Corp.

- Trove Brands LLC.

- YETI Holdings Inc.

- Zojirushi America Corp

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Insulated Water Bottles Market

- In September, 2024, YETI Holdings Inc. announced a multi-year partnership with a major international sports league, becoming the official and exclusive reusable drinkware provider for all teams and venues, a deal valued in the high eight figures.

- In November, 2024, Trove Brands LLC's Owala brand, launched its 'Owala IQ' line, a new series of smart bottles featuring integrated hydration tracking sensors and a proprietary app that syncs with popular fitness platforms, following a USD 25 million Series B funding round.

- In February, 2025, Klean Kanteen announced it achieved its goal of constructing 100% of its stainless steel products using certified 90% post-consumer recycled steel, a milestone verified by SCS Global Services.

- In April, 2025, Pacific Market International LLC's Stanley brand collaborated with a luxury electric vehicle manufacturer to release a limited-edition, co-branded Quencher tumbler designed to fit seamlessly into the vehicle's interior, sold exclusively through the automaker's showrooms.

Research Analyst Overview: Insulated Water Bottles Market

The market has moved beyond simple utility, forcing boardroom decisions to weigh investment in smart bottle technology against the proven returns of aesthetic innovation and material sustainability. While the metal segment remains dominant, its leadership is sustained not by performance alone but by a constant cycle of design-driven updates.

A key strategic challenge is justifying premium pricing in a crowded field. This involves deep integration of non-toxic materials and communicating a commitment to flavor neutrality. Compliance with evolving standards, such as the French Anti-Waste Law (AGEC), compels a focus on the entire product lifecycle, from sourcing recycled stainless steel to ensuring end-of-life recyclability.

For instance, developing a new powder coat finish that is more chip-resistant and eco-friendly is a significant R&D investment but directly addresses consumer concerns about longevity and environmental impact.

Therefore, capital allocation must balance the pursuit of high-tech features like hydration tracking with foundational investments in durability, material safety, and superior thermal retention to defend market share and command premium positioning.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Insulated Water Bottles Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 294 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.9% |

| Market growth 2026-2030 | USD 970.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.7% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Insulated Water Bottles Market: Key Questions Answered in This Report

-

What is the expected growth of the Insulated Water Bottles Market between 2026 and 2030?

-

The Insulated Water Bottles Market is expected to grow by USD 970.6 million during 2026-2030, registering a CAGR of 4.9%. Year-over-year growth in 2026 is estimated at 4.7%%. This acceleration is shaped by growing consumer focus on health and wellness, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Material (Metal, Plastic, Glass, and Silicon), Product Type (Big mouth, Fine mouth, Tumblers, and Mugs), Distribution Channel (Offline, and Online) and Geography (APAC, North America, Europe, Middle East and Africa, South America). Among these, the Metal segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC, North America, Europe, Middle East and Africa and South America. APAC is estimated to contribute 38.3% to market growth during the forecast period. Country-level analysis includes China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is growing consumer focus on health and wellness, which is accelerating investment and industry demand. The main challenge is intense competition and price erosion, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Insulated Water Bottles Market?

-

Key vendors include Bivo LLC, Black Blum, CamelBak Products, Chillys Bottles Ltd., Contigo Brands, Klean Kanteen, MIRA Brands, Nalge Nunc International Corp., Pacific Market International LLC, RTIC Outdoors LLC, S well, SIGG Switzerland Bottles AG, Simple Modern LLC, Steel Technology LLC, Thermos LLC, Tiger Corp., Trove Brands LLC., YETI Holdings Inc. and Zojirushi America Corp. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Insulated Water Bottles Market Research Insights

Market dynamics are increasingly governed by the tension between commoditization and brand expression. While the underlying double wall vacuum insulation technology is widely accessible, premium brands differentiate through design, a chip-resistant coating, and by cultivating a strong brand identity expression. This is critical in a landscape where consumer choice is influenced by social media and lifestyle accessory trends.

Geographically, growth is not uniform; the market in APAC is expanding at a faster pace than in North America, reflecting different stages of market maturity and consumer awareness. The ongoing negotiations for a UN global plastics treaty provide a powerful tailwind, reinforcing the market for any single-use plastic alternative and embedding circular economy principles into long-term corporate strategy.

This pressures manufacturers to innovate beyond aesthetics and focus on aspects like product lifecycle sustainability and the use of recycled materials to meet future compliance and consumer expectations.

We can help! Our analysts can customize this insulated water bottles market research report to meet your requirements.

RIA -

RIA -