Japan Insurance Market Size 2026-2030

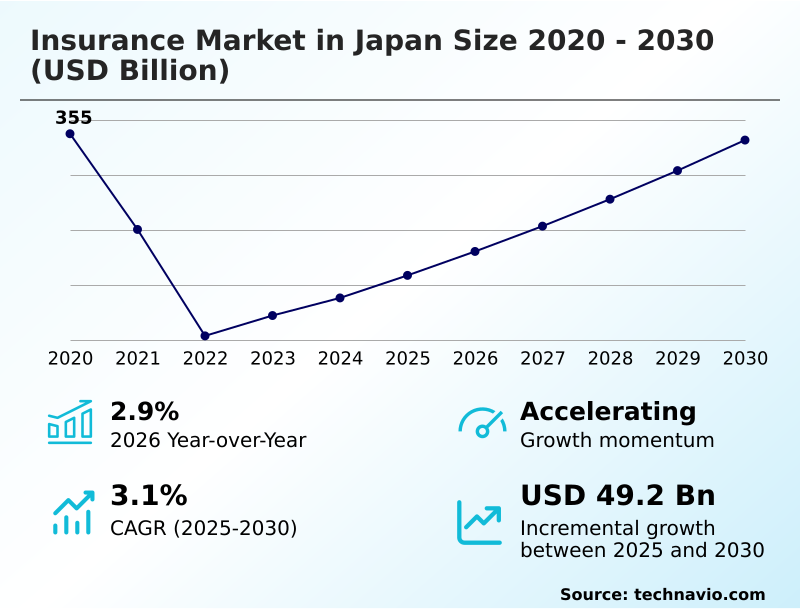

The japan insurance market size is valued to increase by USD 49.2 billion, at a CAGR of 3.1% from 2025 to 2030. Enhancement of cross-border transactional security will drive the japan insurance market.

Major Market Trends & Insights

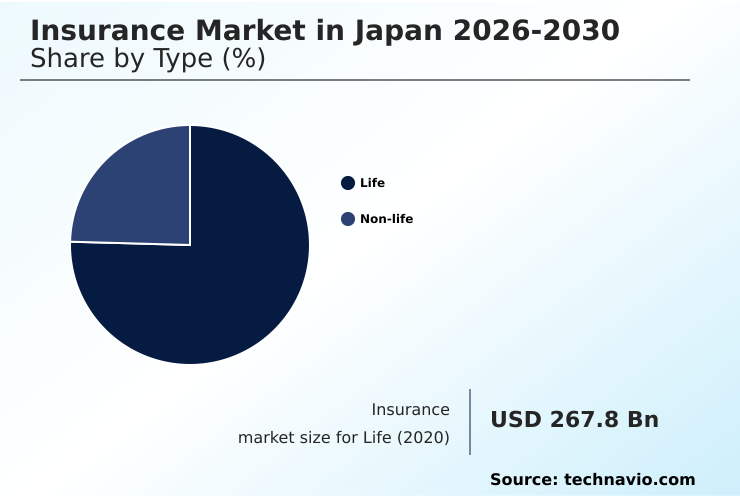

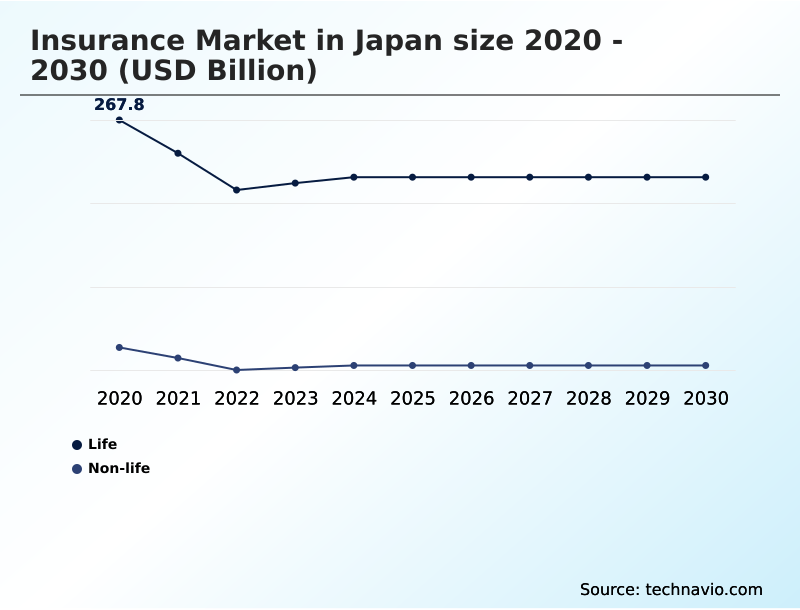

- By Type - Life segment was valued at USD 222.4 billion in 2024

- By Channel - Sales personnel segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 2.3 billion

- Market Future Opportunities: USD 49.2 billion

- CAGR from 2025 to 2030 : 3.1%

Market Summary

- The insurance market in Japan is undergoing a significant transformation, driven by demographic shifts and a complex regulatory environment. A super-aging population is increasing demand for specialized health, long-term care, and retirement products, compelling insurers to innovate beyond traditional life and savings policies.

- Concurrently, the implementation of new economic value-based solvency standards is forcing a strategic pivot towards greater capital efficiency and more sophisticated interest rate risk management. This involves leveraging advanced reinsurance structures and a move towards protection-type policies.

- For instance, a major life insurer might divest from a block of high-guarantee legacy annuities through an offshore reinsurance transaction to improve its economic solvency ratio and free up capital for developing new, less capital-intensive health products.

- This landscape is further complicated by the need to modernize distribution, moving from a traditional tied-agency model to incorporating digital-first channels to meet evolving consumer expectations for transparency and convenience.

What will be the Size of the Japan Insurance Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Japan Insurance Market Segmented?

The japan insurance industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Life

- Non-life

- Channel

- Sales personnel

- Insurance agencies

- Sector

- Public/government insurance companies

- Private insurance companies

- Geography

- APAC

- Japan

- APAC

By Type Insights

The life segment is estimated to witness significant growth during the forecast period.

The life insurance market in Japan, shaped by unique demographic pressures, is pivotal for long-term savings and retirement planning.

Companies are now shifting focus from traditional savings products to offerings like supplementary health insurance and long-term care insurance, addressing the specific needs of an aging population.

This strategic pivot involves leveraging digital verification platforms and cloud-based database systems for greater efficiency. The modernization is evident in urban redevelopment projects that spur new policy creation.

This transition, which includes managing products covering business interruption policies and shared ownership structures, has led to improving policy persistency rates by over 5% through more relevant retirement planning instruments and automated title search technologies for property-linked assets.

The Life segment was valued at USD 222.4 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the insurance market in Japan is now dominated by the complexities of the new solvency regime. Understanding the impact of j-ics on capital management is no longer optional; it is the central strategic challenge. Firms are actively developing strategies for managing duration mismatch risk, as the new framework penalizes such imbalances more severely than before.

- This has amplified the role of reinsurance in legacy liability transfer, with companies exploring sophisticated arrangements to optimize their balance sheets. For many, achieving compliance with the economic value-based solvency regime has necessitated a fundamental shift in product strategy. This includes developing protection-type policies for aging demographics, which are less capital-intensive and better aligned with current risk appetites.

- However, executives must also carefully evaluate the risk of asset-intensive reinsurance transactions to ensure that financial reporting benefits do not mask underlying counterparty exposures, a concern that has led to a 20% increase in due diligence requirements for such deals.

What are the key market drivers leading to the rise in the adoption of Japan Insurance Industry?

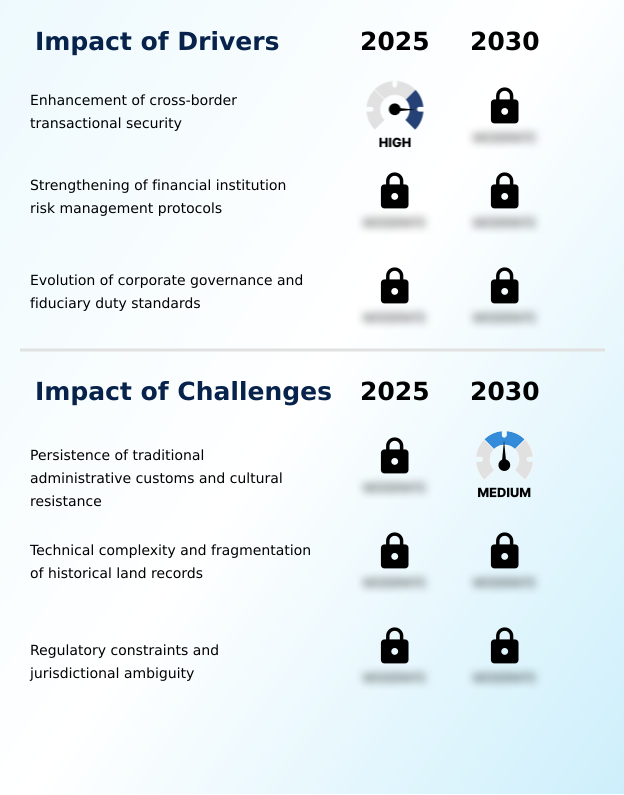

- The enhancement of cross-border transactional security is a key driver, bolstering international investor confidence and supporting market expansion.

- Growth drivers are increasingly tied to capital management and operational efficiency under the new solvency rules. The imperative for capital efficiency optimization is a primary motivator, compelling insurers to refine legacy liability management and develop more profitable protection-type policies.

- This strategic shift has led to a 10% increase in the launch of foreign currency-denominated products, offering higher potential yields. Enhanced corporate governance standards and policyholder protection frameworks are also driving change, pushing for greater transparency.

- The adoption of automated claims processing has reduced operational costs by up to 20% for leading firms.

- While the traditional tied agency force model remains relevant, growth is accelerating through bancassurance partnerships, which provide broader and more efficient distribution, contributing to a more robust economic solvency ratio.

What are the market trends shaping the Japan Insurance Industry?

- The integration of advanced digital verification is emerging as a transformative market trend, enhancing both underwriting precision and overall operational efficiency.

- Key trends are reshaping the market as it adapts to both demographic and regulatory pressures. The influence of super-aging population dynamics and the corresponding low birth rate impact are accelerating the shift toward personalized health products and away from traditional savings vehicles.

- This transition is enabled by advanced data analytics, which allows for more precise risk segmentation and pricing, improving underwriting margins by an average of 5%. To meet new international solvency standards, firms are prioritizing interest rate risk management and capital adequacy assessment. This often involves using complex reinsurance structures to manage liabilities.

- Consequently, the adoption of digital-first distribution channels has become critical for reaching younger demographics, with mobile platforms seeing a 40% year-over-year increase in policy inquiries.

What challenges does the Japan Insurance Industry face during its growth?

- The persistence of traditional administrative customs and cultural resistance presents a key challenge, impeding the broader adoption of modern risk management products and practices.

- Challenges persist in balancing modernization with structural market realities. Insurtech startup integration, while promising efficiency gains, often clashes with legacy IT systems, with nearly 40% of integration projects exceeding budget. The existence of robust social safety net provisions creates a complex environment for private insurance supplementation, requiring insurers to clearly articulate the value beyond baseline government coverage.

- This has intensified the need for multi-carrier product comparison tools and heightened consumer choice enhancement, yet the market's fragmented nature makes direct comparisons difficult. Key strategic challenges include duration mismatch reduction and navigating the complexities of asset-intensive reinsurance, which requires rigorous counterparty risk scrutiny and collateral risk assessment to mitigate potential losses.

- The non-life insurance segment, in particular, faces continuous pressure to innovate beyond standard offerings.

Exclusive Technavio Analysis on Customer Landscape

The japan insurance market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the japan insurance market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Japan Insurance Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, japan insurance market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AFLAC Inc. - Analysis indicates a focus on providing specialized supplemental health, life, and accident insurance products, strategically addressing specific risk and protection gaps within the market.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AFLAC Inc.

- Allianz SE

- American International Group

- Anicom Holdings Inc.

- AXA Group

- Chubb Ltd.

- Dai ichi Life Holdings Inc.

- Japan Post Holdings Co. Ltd.

- Meiji Yasuda Life Insurance Co.

- MS and AD Insurance Group

- Munich Reinsurance Co.

- Nippon Life Insurance Co.

- Rakuten Group Inc.

- Secom Co. Ltd.

- Sompo Holdings Inc.

- Sony Life Insurance Co. Ltd

- Sumitomo Life Insurance Co

- The Kyoei Fire and Marine

- Tokio Marine Holdings Inc.

- Zurich Insurance Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Japan insurance market

- In April, 2025, Sompo Holdings Inc. initiated the issuance of $1.3 billion in senior unsecured notes, specifically structured to qualify as structurally subordinated Tier 2 capital under newly enacted solvency requirements.

- In March, 2025, Aflac Re Bermuda Ltd., a subsidiary of AFLAC Inc., entered into a reinsurance agreement with Japan Post Insurance Co. Ltd. to reinsure a block of whole life annuities, marking a strategic move to optimize capital efficiency.

- In February, 2025, Nippon Life Insurance Co. initiated legal proceedings against the OpenAI Foundation in a US district court, alleging tortious interference with a contract, highlighting emerging conflicts between traditional insurance operations and AI tools.

- In January, 2025, the Japan Financial Services Agency introduced a comprehensive proposed amendment to the Supervisory Guideline for Insurance Companies, targeting the oversight of asset-intensive reinsurance transactions to ensure genuine risk transfer.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Japan Insurance Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 182 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3.1% |

| Market growth 2026-2030 | USD 49.2 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 2.9% |

| Key countries | Japan |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The insurance market in Japan is undergoing a fundamental recalibration driven by new regulatory frameworks that prioritize economic reality over accounting conventions. The mandate for economic value-based solvency and rigorous capital adequacy assessment is compelling a widespread review of balance sheets, with a sharp focus on interest rate risk management.

- To align with international solvency standards, firms are increasingly employing sophisticated reinsurance structures for legacy liability management, achieving significant capital efficiency optimization. This has catalyzed a pivot toward protection-type policies and foreign currency-denominated products, moving away from high-guarantee savings vehicles.

- As companies work to improve their economic solvency ratio, duration mismatch reduction has become a critical operational goal, with some firms achieving a 15% improvement in asset-liability matching.

- This environment also heightens the importance of scrutinizing asset-intensive reinsurance deals, demanding stringent counterparty risk scrutiny and collateral risk assessment to ensure true risk transfer in a market where public pension programs are supplemented by private long-term care insurance and supplementary health insurance.

What are the Key Data Covered in this Japan Insurance Market Research and Growth Report?

-

What is the expected growth of the Japan Insurance Market between 2026 and 2030?

-

USD 49.2 billion, at a CAGR of 3.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Life, and Non-life), Channel (Sales personnel, and Insurance agencies), Sector (Public/government insurance companies, and Private insurance companies) and Geography (APAC)

-

-

Which regions are analyzed in the report?

-

APAC

-

-

What are the key growth drivers and market challenges?

-

Enhancement of cross-border transactional security, Persistence of traditional administrative customs and cultural resistance

-

-

Who are the major players in the Japan Insurance Market?

-

AFLAC Inc., Allianz SE, American International Group, Anicom Holdings Inc., AXA Group, Chubb Ltd., Dai ichi Life Holdings Inc., Japan Post Holdings Co. Ltd., Meiji Yasuda Life Insurance Co., MS and AD Insurance Group, Munich Reinsurance Co., Nippon Life Insurance Co., Rakuten Group Inc., Secom Co. Ltd., Sompo Holdings Inc., Sony Life Insurance Co. Ltd, Sumitomo Life Insurance Co, The Kyoei Fire and Marine, Tokio Marine Holdings Inc. and Zurich Insurance Co. Ltd.

-

Market Research Insights

- Market dynamics are shaped by a strategic push towards operational modernization and enhanced consumer engagement. Insurers leveraging bancassurance partnerships see a 10% higher cross-sell ratio compared to those relying solely on a tied agency force model. The adoption of automated claims processing has enabled leading firms to reduce settlement times by up to 30%, directly improving policyholder protection frameworks.

- Furthermore, adherence to heightened corporate governance standards is becoming a key differentiator, with companies employing advanced analytics for risk assessment showing 15% lower loss ratios. This focus on capital efficiency optimization is driving the development of new foreign currency-denominated products and protection-type policies to navigate the complex environment of legacy liability management.

We can help! Our analysts can customize this japan insurance market research report to meet your requirements.

RIA -

RIA -