Intravenous (IV) Fluid Bags Market Size 2026-2030

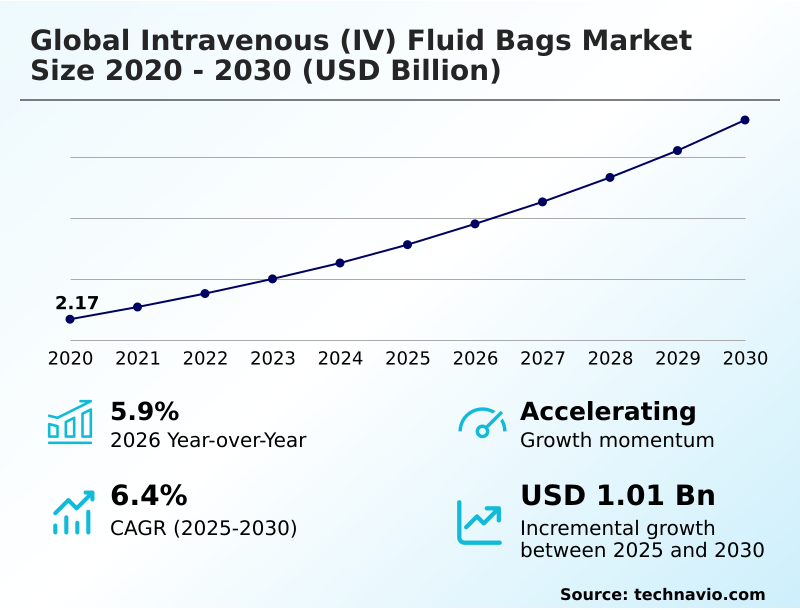

The intravenous (iv) fluid bags market size is valued to increase by USD 1.01 billion, at a CAGR of 6.4% from 2025 to 2030. Rising prevalence of chronic diseases will drive the intravenous (iv) fluid bags market.

Major Market Trends & Insights

- Asia dominated the market and accounted for a 30.9% growth during the forecast period.

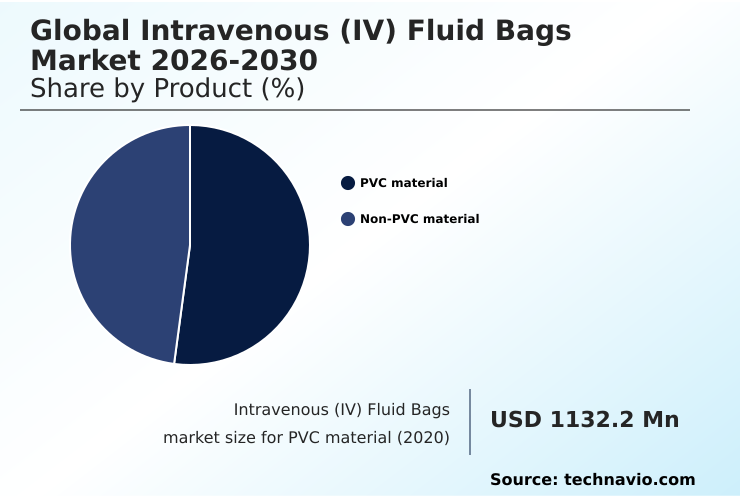

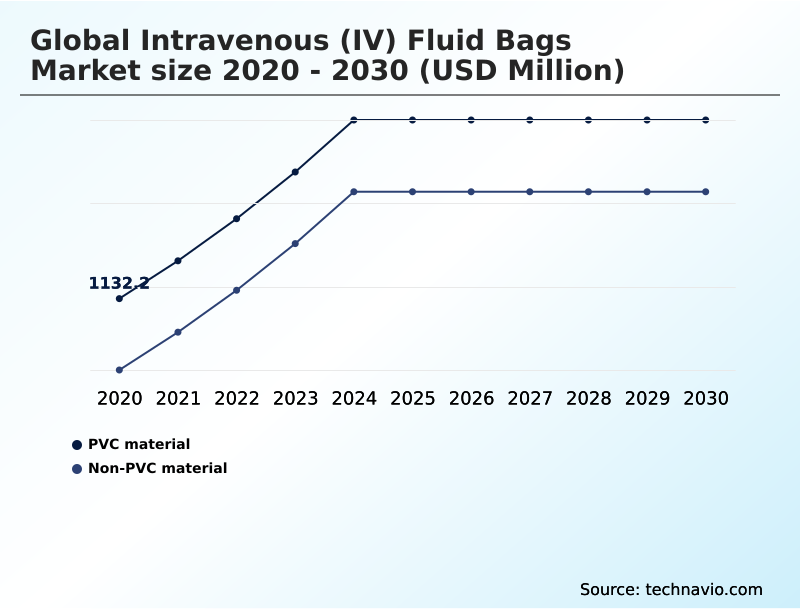

- By Product - PVC material segment was valued at USD 1.36 billion in 2024

- By End-user - Hospitals segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.63 billion

- Market Future Opportunities: USD 1.01 billion

- CAGR from 2025 to 2030 : 6.4%

Market Summary

- The intravenous (IV) fluid bags market is defined by a consistent need for sterile, reliable fluid delivery systems across global healthcare settings. Growth is fundamentally driven by the rising prevalence of chronic diseases requiring long-term therapy and an expanding volume of surgical procedures.

- In response, a key trend is the shift toward value-added products, such as premixed solutions that minimize medication errors and multi-chamber bags for complex nutritional therapies. However, the industry grapples with significant challenges, including supply chain fragility exposed by regional disruptions and regulatory pressure to transition toward safer, non-PVC materials.

- A common business scenario involves hospital procurement teams balancing the cost-effectiveness of traditional PVC bags for general hydration against the clinical necessity and higher expense of advanced, DEHP-free containers for sensitive drug administration. This decision-making is further complicated by the need to secure a resilient supply chain, often requiring a dual-sourcing strategy to mitigate risks from single-point manufacturing failures.

- The market's evolution hinges on balancing innovation in materials and smart technology with the overriding imperatives of cost control, patient safety, and supply continuity.

What will be the Size of the Intravenous (IV) Fluid Bags Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Intravenous (IV) Fluid Bags Market Segmented?

The intravenous (iv) fluid bags industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- PVC material

- Non-PVC material

- End-user

- Hospitals

- Home healthcare

- Others

- Product type

- Single-chamber IV bags

- Multi-chamber IV bags

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Asia

- Rest of World (ROW)

- North America

By Product Insights

The pvc material segment is estimated to witness significant growth during the forecast period.

The market is segmented by material, with non-pvc material options driving significant evolution in product design.

Healthcare facilities are increasingly adopting these advanced polymer formulations, including polypropylene films and polyethylene films, to mitigate risks associated with traditional plastics and align with sustainable medical packaging goals.

The emphasis on biocompatible materials is a response to both regulatory pressures and a clinical focus on patient safety. This transition supports circular economy principles by simplifying medical waste management and reducing the environmental impact of pvc medical waste.

While the cost analysis of dehp-free iv bags remains a consideration, facilities that have adopted these ecofriendly medical supplies report an over 70% reduction in harmful emissions during disposal, making multilayer films a strategic choice.

The PVC material segment was valued at USD 1.36 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Asia is estimated to contribute 30.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Intravenous (IV) Fluid Bags Market Demand is Rising in Asia Get Free Sample

The geographic landscape is dynamic, with Asia poised to capture over 30% of incremental growth, driven by investments in healthcare infrastructure and a focus on building domestic manufacturing capacity.

This region shows accelerated adoption of advanced intravenous therapy solutions for applications like surgical fluid management and emergency fluid resuscitation.

In contrast, North America remains a mature market where the emphasis is on optimizing existing fluid administration systems and ensuring regulatory compliance for medical grade polymers. The push for dehp-free packaging and innovations in aseptic filling and sealing are prominent.

This bifurcation highlights a global need for reliable intravenous medication delivery, from single-use fluid transfer systems for biopharmaceutical fluid transfer to long-term parenteral nutrition bags, with a universal goal of preventing contamination in iv fluid bags.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the market requires a nuanced understanding of evolving product technologies and their specific applications. The benefits of non-pvc iv bags, for instance, are most pronounced in sensitive applications like pediatric and neonatal iv fluid solutions, where the biocompatibility of iv bag materials is paramount.

- Advancements in multi-chamber iv bag design are critical for delivering long-term parenteral nutrition bags and complex drug regimens, particularly in the role of iv bags in chemotherapy. At the same time, the industry is addressing key operational hurdles.

- The challenges in medical plastic recycling and the overall environmental impact of pvc medical waste are driving innovation toward more sustainable materials and disposal protocols. From a business perspective, a thorough cost analysis of dehp-free iv bags is essential for budget-conscious healthcare systems.

- Technologically, the adoption of smart iv bags for inventory management is transforming hospital logistics, with facilities using such systems reporting a reduction in expired stock write-offs by more than 50%. Innovations like forward osmosis technology for iv bags are opening new possibilities for decentralized intravenous therapy models, especially for intravenous fluid bags for home healthcare.

- Ensuring safety across the supply chain involves a focus on preventing contamination in iv fluid bags through techniques like aseptic filling and sealing of iv bags and the use of specialized aseptic connectors for iv administration.

- Furthermore, regulatory compliance for medical grade polymers and the development of single-use systems for bioprocessing are shaping the future of both clinical and manufacturing practices. These factors collectively influence the market's trajectory, demanding that companies balance innovation, cost, and regulatory adherence to maintain a competitive edge.

What are the key market drivers leading to the rise in the adoption of Intravenous (IV) Fluid Bags Industry?

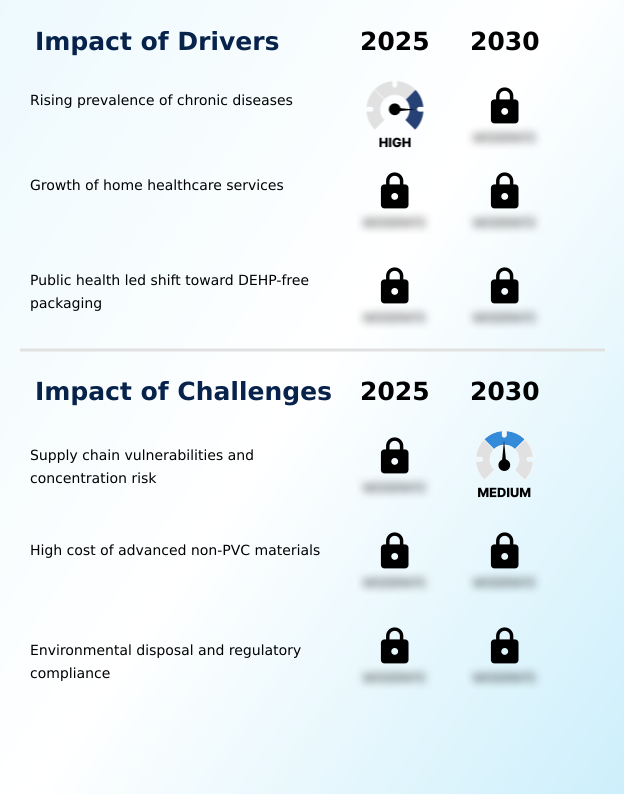

- The rising prevalence of chronic diseases is a foundational driver propelling growth in the intravenous fluid bags market.

- The rising prevalence of chronic conditions is a primary driver, sustaining demand for single-chamber iv bags and specialized multi-chamber iv bags used for clinical nutrition solutions.

- This trend is amplified by the expansion of decentralized healthcare models, where ambulatory infusion services and home infusion therapy supplies are essential.

- The market for intravenous fluid bags for home healthcare is expanding, with demand for parenteral nutrition bags used in the role of iv bags in chemotherapy and other long-term treatments growing by over 15% in certain demographics.

- Medical packaging innovation, such as the forward osmosis iv bag, addresses logistical challenges in remote settings. This shift also supports specialized needs like pediatric and neonatal iv fluid solutions and strengthens the push for greater domestic manufacturing capacity.

What are the market trends shaping the Intravenous (IV) Fluid Bags Industry?

- A key trend influencing the market is the increasing adoption of smart intravenous fluid bags integrated with RFID technology, which enhances inventory management and reduces medication administration errors.

- The adoption of smart intravenous bags is reshaping infusion therapy standards, with innovations like rfid tracking for intravenous fluid bags enabling enhanced hospital inventory management. This technology facilitates a closed loop medication administration process, which has been shown to improve dispensing accuracy by over 95%.

- Concurrently, the shift toward premixed iv solutions and user-friendly medical devices with advanced closure systems simplifies workflows and is critical for reducing medication errors. These trends, including advancements in multi-chamber iv bag design, align with patient-centered care models by supporting automated dispensing systems and enhancing safety.

- The integration of a digital fluid monitoring system further optimizes clinical oversight and resource allocation.

What challenges does the Intravenous (IV) Fluid Bags Industry face during its growth?

- Significant supply chain vulnerabilities and manufacturing concentration risk present a primary challenge affecting the intravenous fluid bags market’s stability.

- Significant challenges persist around supply chain resilience for iv fluids, as disruptions can impact hospital fluid delivery of essential medical infusion bags used for fluid resuscitation techniques. Production concentration has led to shortages where over 85% of facilities are affected during a single event.

- Concurrently, environmental concerns regarding medical plastic recycling of medical grade plastic bags and sterile medical containers are intensifying. Disposal of specialized polymer films and other materials used in sterile packaging solutions requires complex protocols.

- Proper aseptic fluid handling for both gravity based infusion and pump assisted infusion systems generates substantial waste, complicating logistics for items like containers for plasma-derived therapies and creating regulatory hurdles for providers.

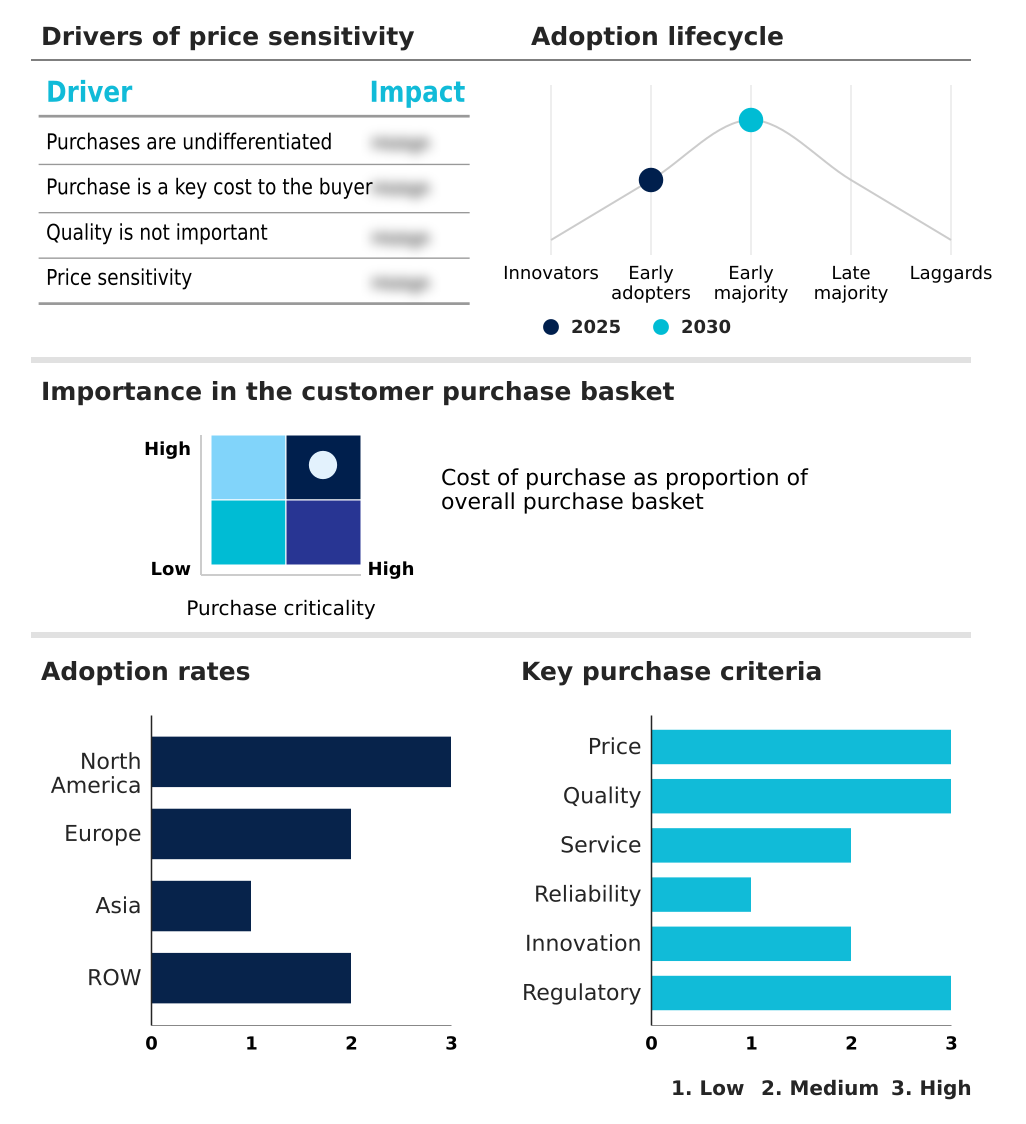

Exclusive Technavio Analysis on Customer Landscape

The intravenous (iv) fluid bags market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the intravenous (iv) fluid bags market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Intravenous (IV) Fluid Bags Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, intravenous (iv) fluid bags market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adagia Partners - Provides a comprehensive portfolio of premixed intravenous fluids and empty flexible containers for clinical fluid management and medication delivery.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adagia Partners

- B.Braun SE

- Baxter International Inc.

- Becton Dickinson and Co.

- Fosmo Med

- Fresenius SE and Co. KGaA

- ICU Medical Inc.

- Medicopack

- Medline Inc.

- Mitra Industries Pvt. Ltd.

- Otsuka Holdings Co. Ltd.

- POLYCINE GmbH

- Puerto Life Sciences Pvt. Ltd.

- RENOLIT SE

- Rusoma Laboratories Pvt. Ltd.

- Sanisure

- Sartorius AG

- Sippex

- The Metrix Co.

- Vioser SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Intravenous (iv) fluid bags market

- In September, 2024, Baxter International faced significant production disruptions after its North Cove, North Carolina facility, a major source of intravenous fluids for the US, was severely damaged by Hurricane Helene, leading to nationwide shortages and allocation limits.

- In December, 2024, Endo International introduced the first FDA-approved, manufacturer-prepared ADRENALIN (epinephrine) premixed intravenous bag in the United States, designed to reduce preparation errors and simplify use in clinical settings.

- In January, 2025, Akkad Holdings announced a $200 million investment to construct an intravenous fluid factory in Mecca, Saudi Arabia, a strategic move to address global supply constraints through localized manufacturing and enhance regional self-reliance.

- In May, 2025, ICU Medical and Otsuka Pharmaceutical Factory finalized their joint venture, creating Otsuka ICU Medical LLC, which establishes one of the largest global manufacturing networks for intravenous solutions with an estimated combined annual production of 1.4 billion units.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Intravenous (IV) Fluid Bags Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 284 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.4% |

| Market growth 2026-2030 | USD 1014.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.9% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, Russia, China, Japan, India, South Korea, Indonesia, Thailand, Singapore, Australia, Brazil, South Africa, UAE, Saudi Arabia and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The intravenous (IV) fluid bags market is evolving beyond a commodity-driven model, propelled by technological integration and material science advancements. The adoption of smart intravenous bags and digital fluid monitoring system technologies enables a closed loop medication administration process, enhancing patient safety.

- Concurrently, a decisive shift toward non-pvc material is underway, driven by demand for dehp-free packaging and more biocompatible materials like polypropylene films and polyethylene films. This transition requires significant boardroom-level capital investment decisions to retool manufacturing lines for these specialized polymer films and multilayer films, ensuring compliance with tightening regulations.

- Innovations such as advanced closure systems, which can reduce contamination risks by up to 75%, are becoming standard. From single-chamber iv bags for gravity based infusion to complex multi-chamber iv bags for parenteral nutrition bags and clinical nutrition solutions, the focus is on safety and efficiency.

- The market is also seeing niche growth in products like the forward osmosis iv bag for remote care and ecofriendly medical supplies to address medical plastic recycling challenges.

- The entire value chain, from aseptic fluid handling and aseptic filling and sealing of medical grade plastic bags and sterile medical containers to final intravenous medication delivery via pump assisted infusion, is being optimized. This extends to specialized applications like ambulatory infusion services, biopharmaceutical fluid transfer, surgical fluid management, and emergency fluid resuscitation.

- Ultimately, the industry's direction is toward creating safer, more efficient fluid administration systems and user-friendly medical devices through sustained medical packaging innovation.

What are the Key Data Covered in this Intravenous (IV) Fluid Bags Market Research and Growth Report?

-

What is the expected growth of the Intravenous (IV) Fluid Bags Market between 2026 and 2030?

-

USD 1.01 billion, at a CAGR of 6.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (PVC material, and Non-PVC material), End-user (Hospitals, Home healthcare, and Others), Product Type (Single-chamber IV bags, and Multi-chamber IV bags) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Rising prevalence of chronic diseases, Supply chain vulnerabilities and concentration risk

-

-

Who are the major players in the Intravenous (IV) Fluid Bags Market?

-

Adagia Partners, B.Braun SE, Baxter International Inc., Becton Dickinson and Co., Fosmo Med, Fresenius SE and Co. KGaA, ICU Medical Inc., Medicopack, Medline Inc., Mitra Industries Pvt. Ltd., Otsuka Holdings Co. Ltd., POLYCINE GmbH, Puerto Life Sciences Pvt. Ltd., RENOLIT SE, Rusoma Laboratories Pvt. Ltd., Sanisure, Sartorius AG, Sippex, The Metrix Co. and Vioser SA

-

Market Research Insights

- Market dynamics are shaped by a pronounced tension between persistent demand and supply chain fragility. The expansion of home infusion therapy supplies and decentralized healthcare models fuels consumption, yet reliance on concentrated manufacturing hubs creates significant risk. During recent disruptions, over 86% of hospitals reported shortages, with some suppliers imposing allocation limits as low as 60% of normal volumes.

- This volatility accelerates the adoption of innovations aimed at improving efficiency and safety. For instance, the use of premixed intravenous therapy solutions has been shown to reduce preparation errors by over 90% compared to manual compounding, directly impacting patient-centered care models.

- Strategic focus is therefore shifting toward enhancing supply chain resilience for iv fluids and investing in technologies that support safer, more efficient hospital fluid delivery and automated dispensing systems.

We can help! Our analysts can customize this intravenous (iv) fluid bags market research report to meet your requirements.

RIA -

RIA -