Marine Electronics Market Size 2026-2030

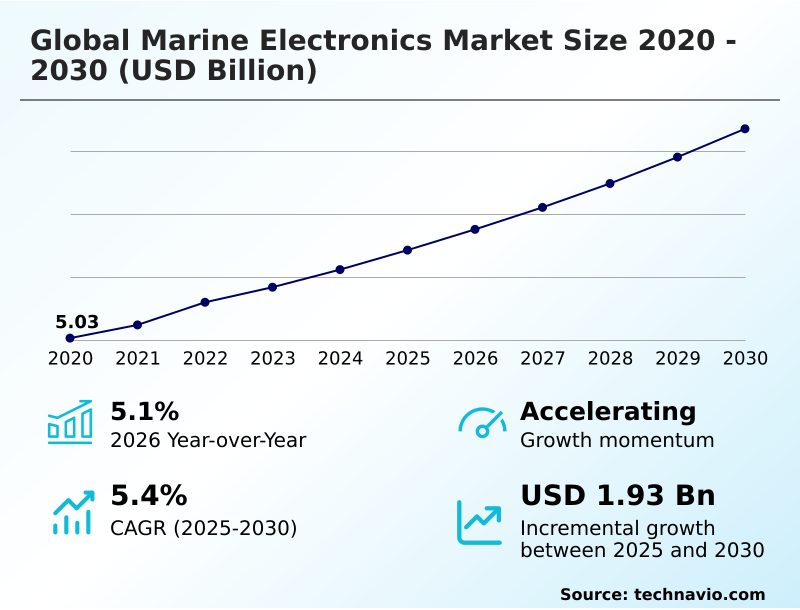

The marine electronics market size is valued to increase by USD 1.93 billion, at a CAGR of 5.4% from 2025 to 2030. Increasing emphasis on marine safety and security regulations will drive the marine electronics market.

Major Market Trends & Insights

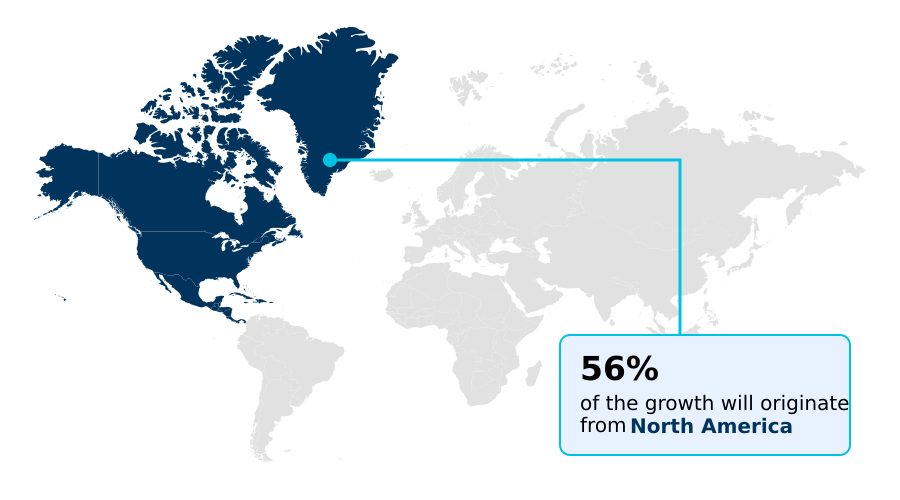

- North America dominated the market and accounted for a 55.9% growth during the forecast period.

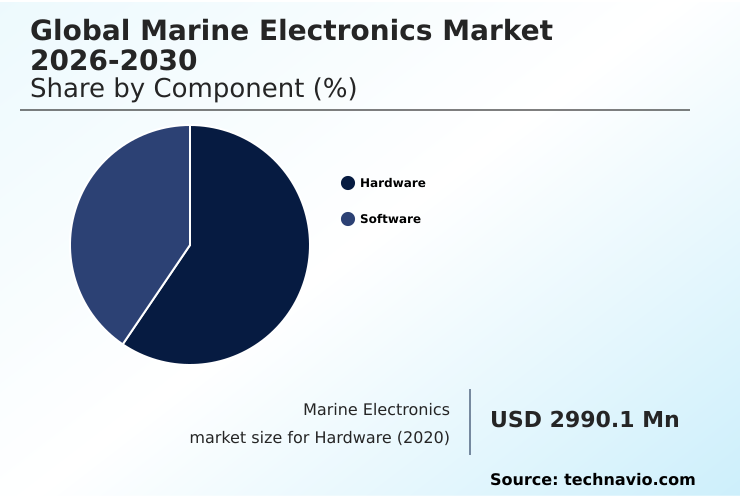

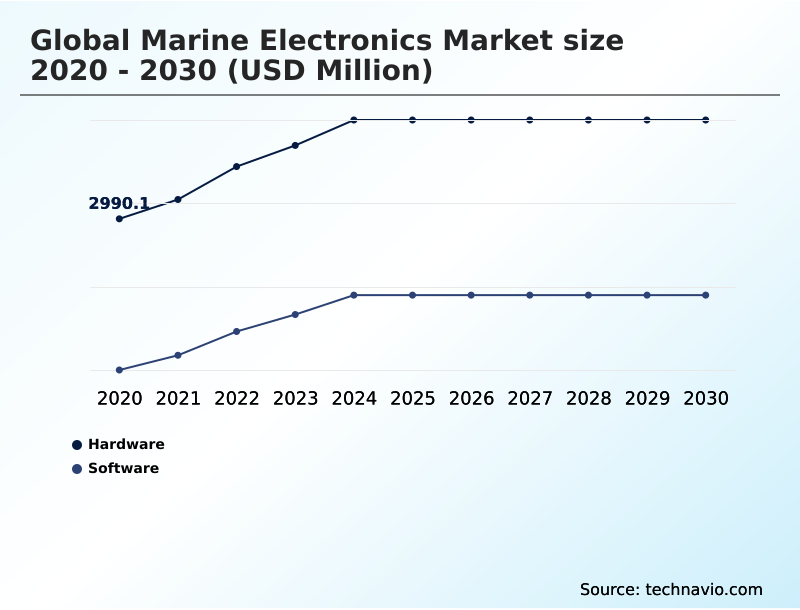

- By Component - Hardware segment was valued at USD 3.61 billion in 2024

- By Product - Sonar systems segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.33 billion

- Market Future Opportunities: USD 1.93 billion

- CAGR from 2025 to 2030 : 5.4%

Market Summary

- The marine electronics market is undergoing a significant transformation, driven by the convergence of stringent regulatory mandates and the pursuit of operational efficiency. Digitalization is reshaping vessel management, with a strong trend towards integrated systems that consolidate data from multiple sensors into a single, intuitive interface.

- This evolution is critical for enhancing situational awareness and supporting complex decision-making in diverse maritime environments. For instance, a commercial fleet operator can leverage an integrated bridge system to fuse data from radar, GPS, and engine monitors. This allows for real-time performance analytics, enabling predictive maintenance schedules that reduce unexpected downtime and optimize fuel consumption across voyages.

- The industry is also moving towards greater autonomy and connectivity, demanding more sophisticated software and robust cybersecurity measures to protect critical onboard systems. This shift creates opportunities for innovation in sensor technology, data analytics, and remote monitoring capabilities, fundamentally altering how vessels are operated and managed.

What will be the Size of the Marine Electronics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Marine Electronics Market Segmented?

The marine electronics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Hardware

- Software

- Product

- Sonar systems

- Radars

- GPS tracking devices

- Type

- Merchant vessels

- Recreational boats

- Fishing vessels

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- Germany

- France

- UK

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- Turkey

- UAE

- Rest of World (ROW)

- North America

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment forms the tangible core of the marine electronics market, comprising the physical devices essential for navigation, communication, and safety.

This area is defined by capital-intensive assets and is directly influenced by new vessel construction, retrofitting activities, and regulatory compliance. Key devices include multifunction displays (MFDs) and various sensors providing critical data.

Growth is sustained by the continuous need for enhanced operational efficiency and safety at sea, with technological shifts from analog to digital systems driving innovation. Modern hardware, such as solid-state Doppler radar and advanced sonar systems, offers superior performance.

The demanding marine environment necessitates ruggedized designs, with systems engineered to withstand harsh conditions, ensuring reliability and a long service life. Interoperability remains a key consideration, with standards like NMEA 2000 facilitating integration.

The Hardware segment was valued at USD 3.61 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 55.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Marine Electronics Market Demand is Rising in North America Get Free Sample

The geographic landscape of the marine electronics market is led by North America, which is projected to account for 55.9% of the market's incremental growth. This dominance is driven by a large recreational boating sector and significant defense spending.

In contrast, APAC is emerging as the fastest-growing region, fueled by its massive shipbuilding industry in countries like China, South Korea, and Japan, which creates immense demand for new electronic installations.

Europe remains a key market, with a strong focus on regulatory compliance, sustainability, and high-value shipbuilding, particularly in the cruise and mega-yacht segments.

The integration of advanced sonar systems, battery management systems (BMS), and vessel traffic management systems (VTMS) varies by region, reflecting diverse priorities from leisure-focused features to commercial efficiency and naval superiority.

The use of CHIRP sonar technology is becoming widespread across these regions for enhanced underwater imaging.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the marine electronics market is deeply influenced by the need to balance technological advancement with practical implementation across diverse maritime sectors. A key discussion revolves around the benefits of solid-state radar technology, which offers enhanced reliability and target detection compared to traditional magnetron systems.

- However, the impact of NMEA 2000 on interoperability remains a critical factor, as achieving seamless plug-and-play functionality between multi-vendor systems is still a challenge. In the commercial sphere, the role of GNSS in fleet management has become foundational, enabling precise tracking and route optimization.

- This contrasts with the focus in the recreational sector, where advancements in recreational sonar technology, including detailed underwater imaging, drive consumer demand. The increasing reliance on networked systems brings forth significant challenges in marine electronics cybersecurity, necessitating robust protection for critical operational data.

- Furthermore, the role of AI in autonomous navigation is a transformative trend, pushing the development of sophisticated collision avoidance algorithms. The adoption of advanced autopilot systems for fuel efficiency highlights a clear return on investment, with some operators reporting greater gains than others.

- As vessels become more electrified, the importance of battery management systems in hybrid vessels grows, ensuring both safety and performance. This complex interplay of innovation, regulation, and practical application continues to shape the industry's trajectory.

What are the key market drivers leading to the rise in the adoption of Marine Electronics Industry?

- An increasing emphasis on stringent marine safety and security regulations, established by international and national maritime authorities, serves as a key driver for the market.

- Market growth is primarily propelled by stringent international safety regulations and the persistent pursuit of operational efficiency.

- Mandates from maritime authorities compel the adoption of certified equipment such as the electronic chart display (ECDIS) and automatic identification systems (AIS), affecting over 90% of the global commercial fleet and creating a continuous replacement and upgrade cycle.

- Beyond compliance, economic pressures drive investment in advanced technologies. For instance, the integration of high-precision global navigation satellite system (GNSS) receivers with modern autopilot systems can reduce fuel consumption by up to 5% on long voyages.

- The expanding leisure marine segment, particularly in North America, further fuels demand, with consumers seeking sophisticated features that enhance convenience and enjoyment on the water, driving rapid innovation in user-friendly interfaces and connectivity.

What are the market trends shaping the Marine Electronics Industry?

- The market is witnessing a fundamental shift from standalone devices to highly integrated and connected vessel ecosystems. This trend is reshaping product development and end-user expectations across all maritime sectors.

- Key trends are reshaping the marine electronics market, driven by a move toward highly integrated systems and sustainability. The rise of connected vessel ecosystems, where data from multiple sources is unified on a single interface, is enhancing operational control. This integration enables advanced features like autonomous navigation, with some automated docking systems reducing maneuvering time by over 20%.

- Concurrently, there is a strong emphasis on electrification, creating demand for specialized electronics like battery management systems (BMS) to ensure the safe and efficient operation of hybrid and electric propulsion. These systems provide critical data on energy consumption, with real-time monitoring improving range prediction accuracy by up to 15%.

- This shift toward smarter, greener vessels is compelling manufacturers to innovate in both hardware and software.

What challenges does the Marine Electronics Industry face during its growth?

- A key challenge affecting industry growth is addressing the pervasive system complexity and persistent interoperability hurdles associated with integrated marine electronics.

- The market faces significant challenges related to escalating system complexity and global supply chain volatility. Achieving seamless interoperability between devices from different manufacturers remains a persistent hurdle, with the lack of standardized implementation leading to integration issues. The shortage of technicians skilled in modern IT networking has increased vessel downtime for complex electronic repairs by an average of 25%.

- Furthermore, the industry's reliance on a constrained global supply chain for critical components like semiconductors exposes it to significant risk. Recent disruptions have caused component lead times to surge by over 200% in some cases, severely hampering production planning and eroding profit margins.

- These factors create a difficult operating environment, forcing manufacturers to balance innovation with the need for robust, long-term support and supply chain resilience.

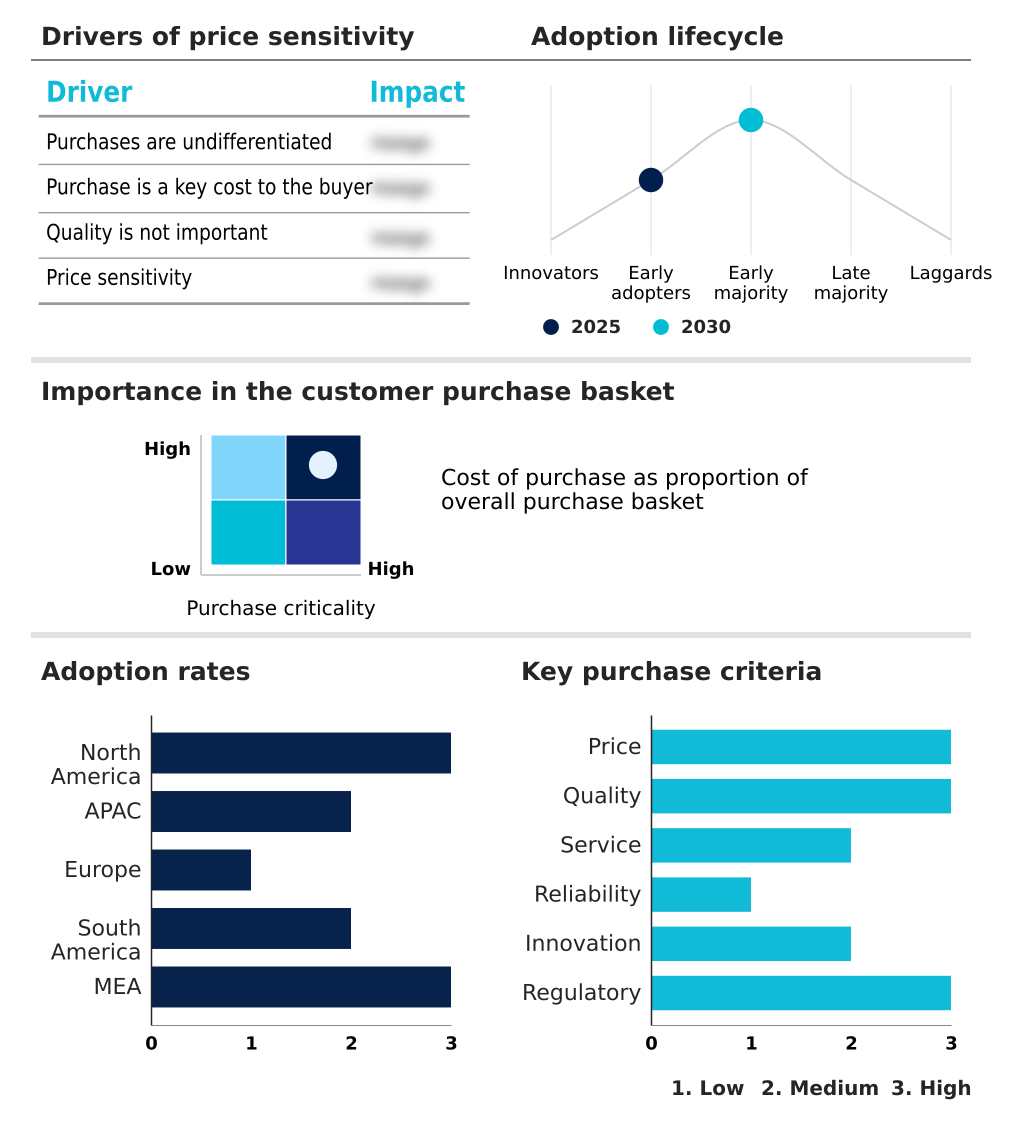

Exclusive Technavio Analysis on Customer Landscape

The marine electronics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the marine electronics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Marine Electronics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, marine electronics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ACR Electronics Inc. - Offerings are centered on integrated navigation and sonar systems, providing advanced situational awareness for both recreational and light commercial marine applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ACR Electronics Inc.

- Airmar Technology Corp.

- B and G

- Cobra Electronics Corp.

- Comar Systems Ltd.

- ComNav Technology Ltd.

- Digital Yacht Ltd

- Furuno Electric Co. Ltd.

- Garmin Ltd.

- Icom Inc.

- Japan Radio Co. Ltd.

- Johnson Outdoors Inc.

- Lowrance Electronics

- Navico

- Raymarine

- Shakespeare Co LLC

- Simrad Yachting

- SI-TEX Marine Electronics

- Standard Horizon

- Uniden America Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Marine electronics market

- In August 2024, Navico Group launched its Fathom e-power system, an integrated lithium-ion battery solution designed to replace traditional generators, advancing onboard energy management for a wide range of vessels.

- In January 2025, GE Vernova's Power Conversion division was selected to supply its hybrid-electric propulsion technology for three new Fleet Solid Support vessels for the United Kingdom's Ministry of Defence, signaling a push towards electrification in the naval sector.

- In February 2025, ADNOC L&S announced a partnership with SeaOwl to implement a new AI-driven vessel traffic management system in a major UAE port, aiming to optimize traffic flow and enhance port security through advanced analytics.

- In March 2025, the Indian government launched an initiative to modernize its fishing fleet by offering subsidies for the purchase of advanced marine electronics, including GPS and fish finders, to improve safety and operational efficiency.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Marine Electronics Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.4% |

| Market growth 2026-2030 | USD 1930.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.1% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, Germany, France, UK, Italy, Russia, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, Turkey, UAE, South Africa and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The marine electronics market is pivoting from a hardware-centric model to one defined by software and data analytics. This transition is evident in the rise of the integrated bridge system, which acts as the central nervous system for modern vessels.

- Key components such as the multifunction display (MFD) and electronic chart display (ECDIS) are no longer standalone devices but are deeply interconnected with an array of sensors, including solid-state Doppler radar and advanced sonar systems. For boardroom consideration, this shift requires a strategic approach to capital expenditure, weighing the benefits of full-fleet upgrades against phased retrofits.

- The integration of systems like the automatic identification system (AIS), battery management system (BMS), and voyage data recorders (VDRs) into a unified network enhances operational oversight. Technologies such as CHIRP sonar technology and dynamic positioning systems are becoming standard, while the adoption of vessel traffic management systems (VTMS) in ports improves logistical efficiency.

- Onboard systems reliant on the global navigation satellite system (GNSS) now offer precision that reduces auxiliary fuel consumption by up to 10% through optimized routing.

What are the Key Data Covered in this Marine Electronics Market Research and Growth Report?

-

What is the expected growth of the Marine Electronics Market between 2026 and 2030?

-

USD 1.93 billion, at a CAGR of 5.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, and Software), Product (Sonar systems, Radars, and GPS tracking devices), Type (Merchant vessels, Recreational boats, Fishing vessels, and Others) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing emphasis on marine safety and security regulations, Addressing pervasive system complexity and interoperability hurdles

-

-

Who are the major players in the Marine Electronics Market?

-

ACR Electronics Inc., Airmar Technology Corp., B and G, Cobra Electronics Corp., Comar Systems Ltd., ComNav Technology Ltd., Digital Yacht Ltd, Furuno Electric Co. Ltd., Garmin Ltd., Icom Inc., Japan Radio Co. Ltd., Johnson Outdoors Inc., Lowrance Electronics, Navico, Raymarine, Shakespeare Co LLC, Simrad Yachting, SI-TEX Marine Electronics, Standard Horizon and Uniden America Corp.

-

Market Research Insights

- The dynamics of the marine electronics market are increasingly shaped by the push for data-driven operational intelligence. The adoption of advanced driver-assistance systems (ADAS) and integrated platforms is delivering tangible benefits, with some automated docking systems reducing maneuvering time in congested ports by over 20%.

- Enhanced situational awareness, a key purchasing driver, is being achieved through the fusion of sensor data, which has been shown to decrease diagnostic time for network faults by more than 40%. Furthermore, the emphasis on remote vessel operation and performance monitoring is compelling a shift towards more robust connectivity solutions.

- This digital transformation is not only improving safety but also unlocking significant efficiencies for fleet managers, making investment in modern electronics a strategic imperative for maintaining a competitive edge.

We can help! Our analysts can customize this marine electronics market research report to meet your requirements.

RIA -

RIA -