Next Generation Air Defense System Market Size 2026-2030

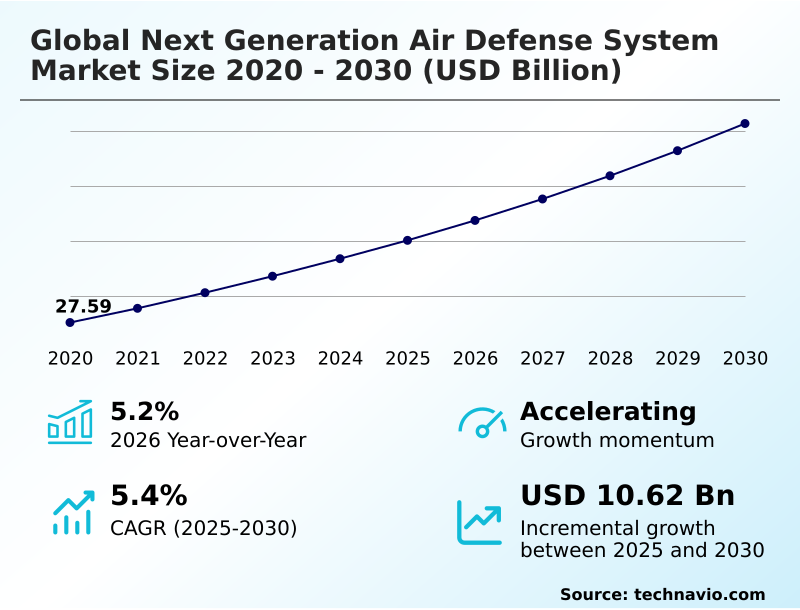

The next generation air defense system market size is valued to increase by USD 10.62 billion, at a CAGR of 5.4% from 2025 to 2030. Escalating geopolitical tensions will drive the next generation air defense system market.

Major Market Trends & Insights

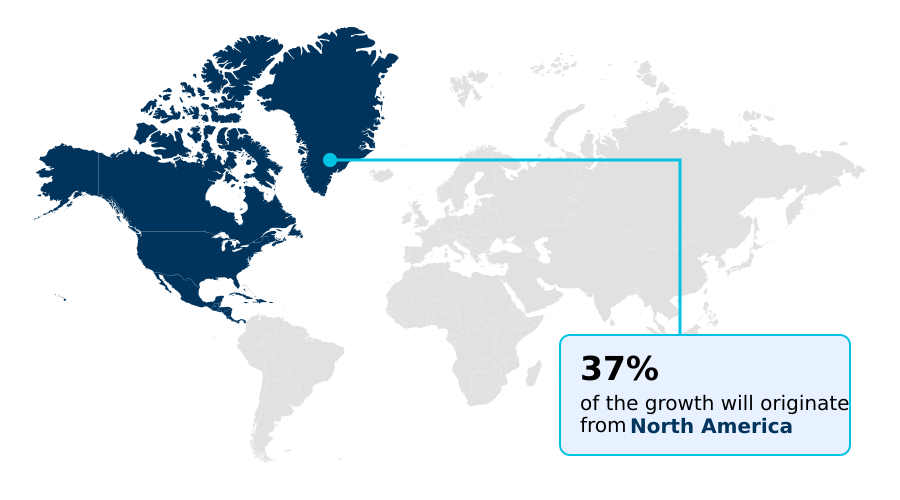

- North America dominated the market and accounted for a 37.1% growth during the forecast period.

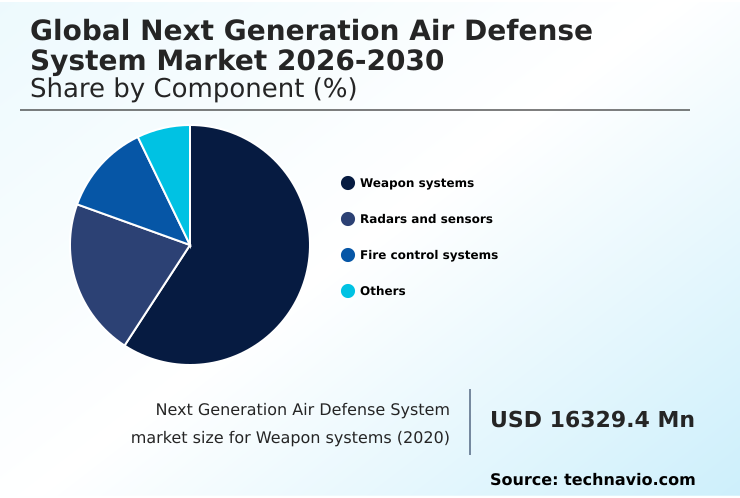

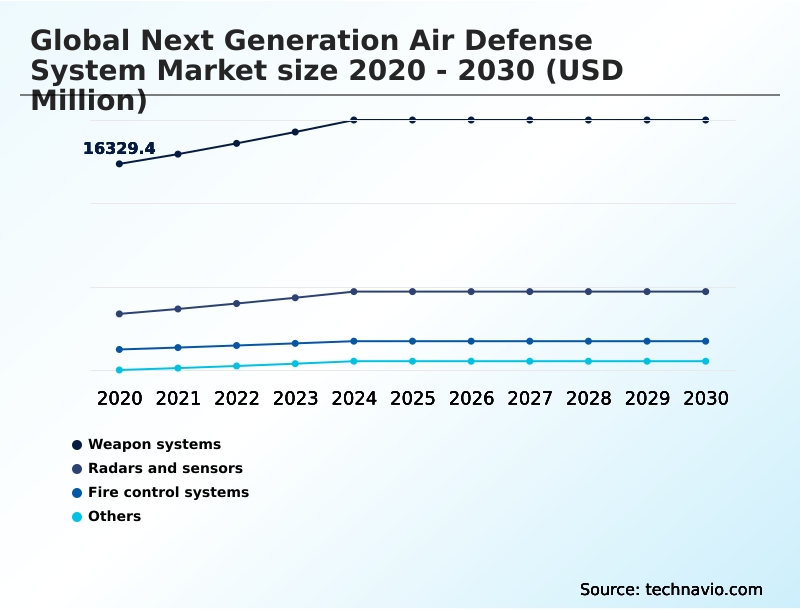

- By Component - Weapon systems segment was valued at USD 19.38 billion in 2024

- By Platform - Land based segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 18.09 billion

- Market Future Opportunities: USD 10.62 billion

- CAGR from 2025 to 2030 : 5.4%

Market Summary

- The next generation air defense system market is driven by the imperative to protect sovereign airspace against a rapidly diversifying array of aerial threats. Escalating geopolitical tensions and the proliferation of advanced platforms, including unmanned aerial vehicles and hypersonic weapons, have compelled nations to abandon legacy systems in favor of dynamic, integrated solutions.

- This modernization focuses on creating a layered defense architecture that combines long-range ballistic missile defense with agile short-range air defense for comprehensive critical infrastructure protection. A core technological shift involves the adoption of AESA radars and advanced sensor fusion, enabling superior situational awareness and multi-target engagement.

- For instance, a defense agency managing procurement cycles for urban air defense must now balance the high life cycle cost of advanced kinetic interceptors against the cost-effectiveness of directed energy weapons for counter-UAS roles. This requires a sophisticated systems engineering methodology to ensure system interoperability across a resilient defense ecosystem.

- The integration of artificial intelligence into command and control systems is no longer a niche capability but a fundamental requirement for reducing reaction times and managing the complexities of network-centric warfare and multi-domain operations.

What will be the Size of the Next Generation Air Defense System Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Next Generation Air Defense System Market Segmented?

The next generation air defense system industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Weapon systems

- Radars and sensors

- Fire control systems

- Others

- Platform

- Land based

- Naval

- Airborne

- Type

- Long range

- Medium range

- Short range

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Component Insights

The weapon systems segment is estimated to witness significant growth during the forecast period.

The weapon systems segment is evolving through a dual-focus on advanced kinetic interceptors and maturing directed energy weapons. Development is centered on countering hypersonic weapons and loitering munitions, driving innovation in hit-to-kill technology and non-kinetic intercept solutions.

This technological arms race, fueled by geopolitical tensions, necessitates a focus on kill chain effectiveness and managing life cycle cost.

For instance, laser-based counter-UAS platforms are gaining traction as they offer a cost-per-shot reduction exceeding 95% compared to traditional surface-to-air missiles, transforming the economics of asset protection and force protection.

This shift reflects a broader emphasis on achieving strategic autonomy through a diverse and adaptable arsenal, including advanced air-to-air missile capabilities for comprehensive sovereign airspace security.

The Weapon systems segment was valued at USD 19.38 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Next Generation Air Defense System Market Demand is Rising in North America Get Free Sample

The market's geographic landscape is shaped by distinct regional security dynamics. North America, contributing over 37% of incremental growth, focuses on technological superiority and continental defense, driving investments in joint all-domain command and control and advanced electronic warfare suites.

In contrast, APAC is the fastest-growing region, with nations bolstering anti-access/area denial capabilities and maritime domain awareness in response to regional pressures; spending on these systems is up nearly 20% in some areas.

Europe is prioritizing strategic autonomy and system interoperability through collaborative programs. The Middle East remains a key market focused on asset protection against asymmetric threats like drones and missiles, necessitating advanced short-range air defense and vertical launching systems.

South America emphasizes border protection and airspace surveillance against illicit activities, reflecting a different set of operational readiness requirements.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic planning in the next generation air defense system market increasingly revolves around the integration of AI in air defense to automate and accelerate the kill chain. A primary focus is countering hypersonic missile threats, which requires revolutionary advances in space-based tracking and interceptor technology.

- Equally important is detecting low observable aerial targets, a challenge driving innovation in multi-spectrum sensors and quantum radar research. The principle of a layered defense for critical infrastructure has become standard doctrine, combining different systems for robust protection. Decision-makers are closely analyzing the cost-effectiveness of directed energy weapons, especially for countering low-cost threats.

- Furthermore, ensuring interoperability in multinational defense operations is a key challenge, demanding common data links and architectures. Specialized solutions for c-uas for urban environment protection are now a distinct market segment, addressing the unique kinematics of drone threats. The foundational role of GaN in AESA radars cannot be overstated, as it enables the required power and sensitivity.

- This supports a network-centric approach for IAMD, linking sensors and shooters seamlessly. However, the challenges of integrating diverse systems remain a significant hurdle. Development of next generation fire control systems is crucial for managing this complexity, especially considering the impact of drone swarms on shorad. The growing reliance on space-based sensors for missile defense is changing strategic calculations.

- Planners are also focused on enhancing naval air defense capabilities against anti-ship missiles. Key R&D areas include advancements in kinetic interceptor technology and ensuring JADC2 and air defense integration. Finally, the effectiveness of EW suites for fighter self-protection and robust cybersecurity for air defense networks is paramount.

- Modern systems achieve a reducing reaction time with machine learning, with platforms leveraging AI showing nearly double the engagement speed of their manually operated predecessors, thereby optimizing the delicate act of balancing cost and capability in procurement.

What are the key market drivers leading to the rise in the adoption of Next Generation Air Defense System Industry?

- Escalating geopolitical tensions and the increasing frequency of regional instabilities serve as a primary catalyst for the expansion of the global next-generation air defense system market.

- Escalating geopolitical tensions and a rapidly evolving threat landscape evolution are compelling nations to modernize their defense capabilities.

- Increased defense budget allocation, with some countries boosting spending by over 15%, is accelerating the acquisition of integrated air and missile defense systems.

- The proliferation of unmanned aerial vehicles and hypersonic weapons drives demand for advanced AESA radars and sophisticated sensor fusion techniques to ensure sovereign airspace security.

- Technological advancements are pivotal; AI-enabled C4ISR systems process data up to 50% faster, enabling rapid decision-making.

- This push is creating a highly competitive defense industrial base focused on delivering solutions for continental defense and border protection that can adapt to new challenges and support multi-domain operations.

What are the market trends shaping the Next Generation Air Defense System Industry?

- A prominent market trend is the significantly increased focus on developing robust counter-UAS capabilities. This is driven by the need to address the transformed aerial threat landscape posed by unmanned platforms.

- The market is increasingly shaped by the integration of machine learning to enhance threat detection algorithms and engagement optimization. This allows for a reaction time reduction of up to 40% in complex scenarios involving asymmetric threats. A key trend is the development of robust counter-UAS capabilities, where layered defense architecture combines electro-optical/infrared sensors and other systems to improve situational awareness.

- Such integrated systems, which are crucial for urban air defense and critical infrastructure protection, have shown an 85% success rate against drone swarms. The emphasis on network-centric warfare and creating a resilient defense ecosystem through a common operating picture ensures that data from multi-function radars and other assets are used effectively, supporting multi-target engagement and enhancing overall operational readiness.

What challenges does the Next Generation Air Defense System Industry face during its growth?

- The immense complexity of integrating diverse, multi-vendor air defense systems represents a significant challenge to achieving seamless interoperability and full operational effectiveness.

- A primary challenge is ensuring system interoperability among diverse platforms, a complex task where the lack of open architecture standards can increase integration costs by over 40%. The rapid threat landscape evolution means that even new systems face obsolescence, demanding continuous R&D and straining defense budget allocation.

- The high life cycle cost of ballistic missile defense and other advanced systems, with lengthy procurement cycles often exceeding a decade, creates significant financial barriers. Furthermore, protecting cyber-hardened systems from sophisticated attacks is a growing concern.

- These factors challenge the defense industrial base to innovate within a framework of systems engineering methodology that balances capability with affordability, especially for countering low-observable targets and other advanced threats that require state-of-the-art target recognition systems and trajectory prediction software.

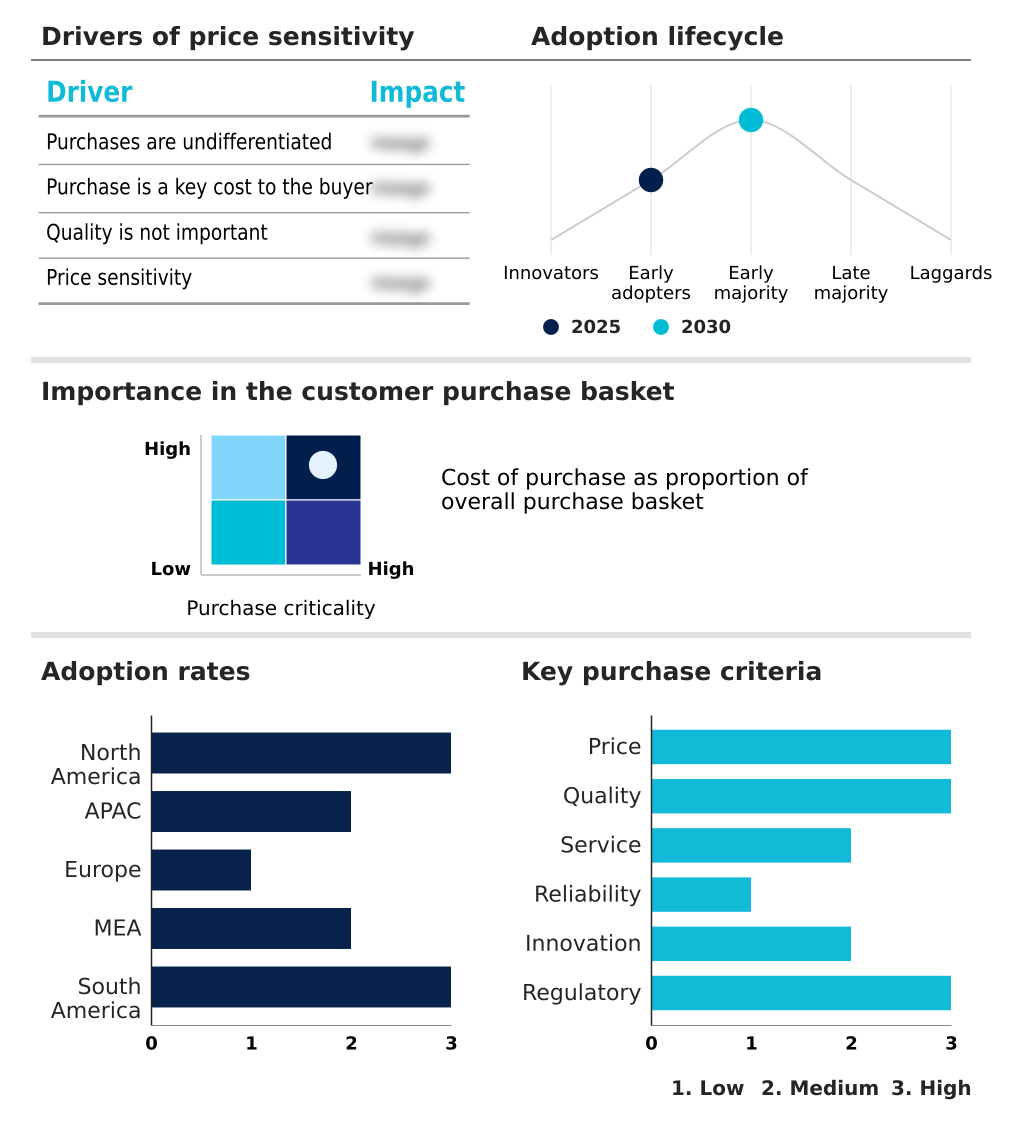

Exclusive Technavio Analysis on Customer Landscape

The next generation air defense system market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the next generation air defense system market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Next Generation Air Defense System Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, next generation air defense system market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ASELSAN AS - Provider of integrated electronic systems, combat platforms, and cyber intelligence solutions, delivering advanced defense and security capabilities for complex operational environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ASELSAN AS

- BAE Systems Plc

- Diehl Stiftung and Co. KG

- Elbit Systems Ltd.

- Hanwha Group

- HENSOLDT AG

- Israel Aerospace Ltd.

- Kongsberg Gruppen ASA

- L3Harris Technologies Inc.

- Leonardo S.p.A.

- Lockheed Martin Corp.

- MBDA

- Mitsubishi Heavy Ltd.

- Northrop Grumman Corp.

- Rafael Advanced Defense Ltd.

- Rheinmetall AG

- RTX Corp.

- Saab AB

- Thales Group

- The Boeing Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Next generation air defense system market

- In February 2025, Lockheed Martin received a contract from the Missile Defense Agency for the development of THAAD 6.0, aimed at enhancing interceptor capabilities against new threats.

- In March 2025, the Missile Defense Agency and the US Navy conducted a simulated interception of a hypersonic threat utilizing an upgraded Standard Missile 6 (SM-6), marking progress in counter-hypersonic defense.

- In March 2025, Anduril and Zone 5 Technologies were awarded contracts to advance the development of palletized munitions platforms for integration into advanced fire control networks.

- In May 2025, Raytheon delivered the inaugural AN/TPY-2 radar featuring a GaN array to the Missile Defense Agency, a system specifically engineered for tracking hypersonic weapons.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Next Generation Air Defense System Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 309 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.4% |

| Market growth 2026-2030 | USD 10618.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.2% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, Russia, France, Italy, Spain, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The next generation air defense system market is defined by a race to counter increasingly sophisticated threats, from stealthy low-observable targets and loitering munitions to hypersonic weapons. To address this, development has pivoted toward integrated solutions featuring advanced AESA radars powered by gallium nitride technology for superior airspace surveillance.

- These systems utilize complex threat detection algorithms and trajectory prediction for precise engagement optimization. The arsenal combines advanced kinetic interceptors using hit-to-kill technology with emerging directed energy weapons for non-kinetic intercept roles. These are deployed via vertical launching systems and include sophisticated surface-to-air missiles and air-to-air missile platforms.

- Central to this paradigm is a layered defense architecture that integrates everything from short-range air defense to ballistic missile defense. This network-centric warfare model relies on open architecture standards and robust C4ISR systems for effective sensor fusion. The goal is to achieve comprehensive integrated air and missile defense through joint all-domain command and control frameworks, enabling autonomous multi-domain operations.

- The integration of command and control systems with electro-optical/infrared sensors and electronic warfare suites is critical for target recognition systems and delivering soft-kill options. AI-powered systems have shown a 30% reduction in threat classification time, a critical metric influencing boardroom budgeting for these cyber-hardened systems that are essential for countering unmanned aerial vehicles and enabling autonomous engagement.

What are the Key Data Covered in this Next Generation Air Defense System Market Research and Growth Report?

-

What is the expected growth of the Next Generation Air Defense System Market between 2026 and 2030?

-

USD 10.62 billion, at a CAGR of 5.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Weapon systems, Radars and sensors, Fire control systems, and Others), Platform (Land based, Naval, and Airborne), Type (Long range, Medium range, and Short range) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Escalating geopolitical tensions, Complexity of integrating diverse systems

-

-

Who are the major players in the Next Generation Air Defense System Market?

-

ASELSAN AS, BAE Systems Plc, Diehl Stiftung and Co. KG, Elbit Systems Ltd., Hanwha Group, HENSOLDT AG, Israel Aerospace Ltd., Kongsberg Gruppen ASA, L3Harris Technologies Inc., Leonardo S.p.A., Lockheed Martin Corp., MBDA, Mitsubishi Heavy Ltd., Northrop Grumman Corp., Rafael Advanced Defense Ltd., Rheinmetall AG, RTX Corp., Saab AB, Thales Group and The Boeing Co.

-

Market Research Insights

- Market dynamics are increasingly shaped by the need for a resilient defense ecosystem capable of adapting to a rapidly evolving threat landscape evolution. The focus on system interoperability and achieving a common operating picture has driven the adoption of open architectures, which has been shown to reduce system upgrade costs by over 25%.

- Escalating geopolitical tensions are accelerating procurement cycles and prompting higher defense budget allocation toward technologies that enhance situational awareness and sovereign airspace security. AI-driven platforms are demonstrating a significant impact on operational readiness, with some systems achieving a 40% reaction time reduction in threat engagement scenarios.

- This technological arms race pressures the defense industrial base to deliver solutions for critical infrastructure protection that are both highly capable and sustainable over their life cycle cost.

We can help! Our analysts can customize this next generation air defense system market research report to meet your requirements.

RIA -

RIA -