Command And Control Systems Market Size 2026-2030

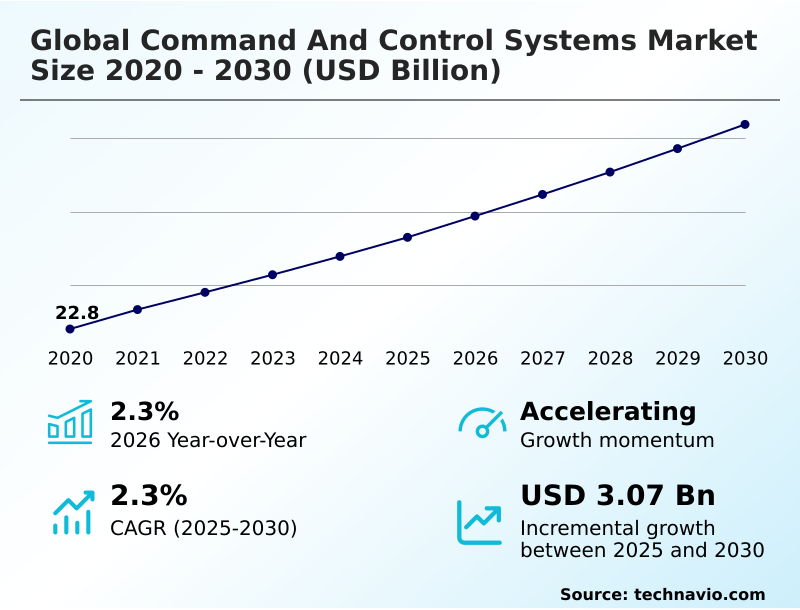

The command and control systems market size is valued to increase by USD 3.07 billion, at a CAGR of 2.3% from 2025 to 2030. Escalating demand for network centric warfare and multi domain integration will drive the command and control systems market.

Major Market Trends & Insights

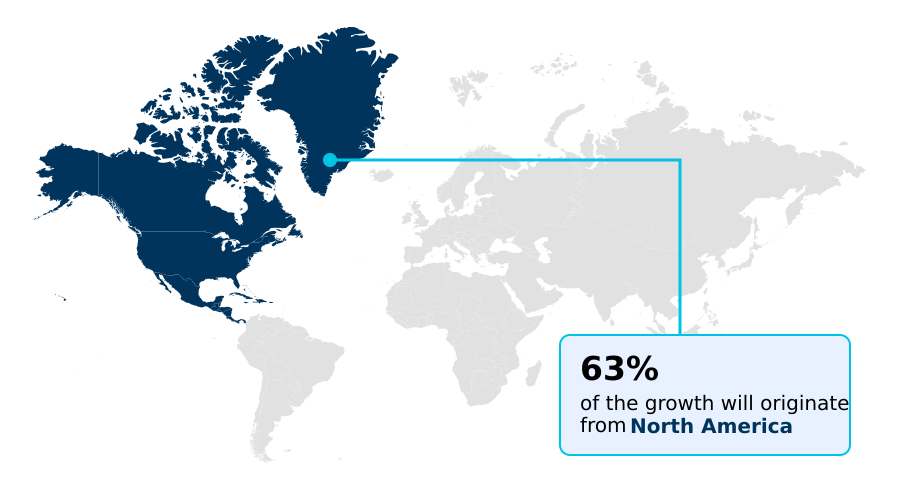

- North America dominated the market and accounted for a 63% growth during the forecast period.

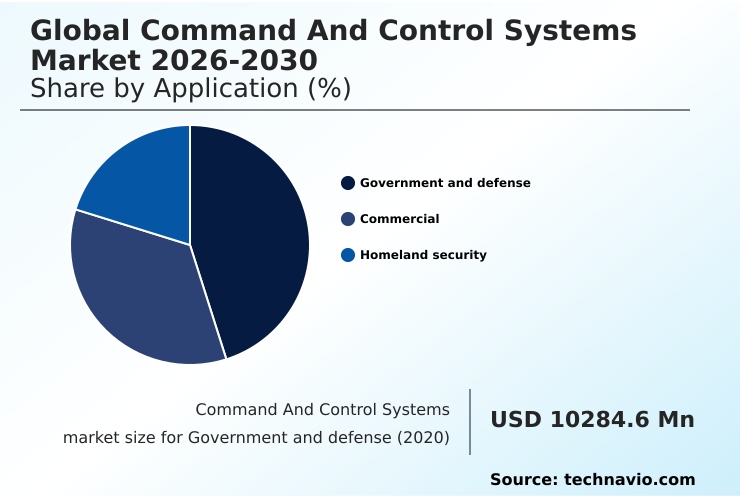

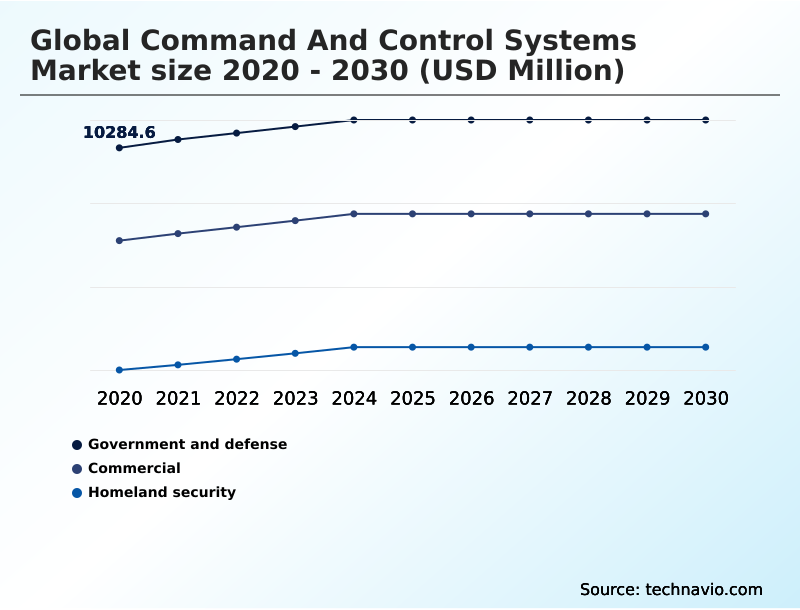

- By Application - Government and defense segment was valued at USD 11.00 billion in 2024

- By Platform - Land segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 5.57 billion

- Market Future Opportunities: USD 3.07 billion

- CAGR from 2025 to 2030 : 2.3%

Market Summary

- The command and control systems market is undergoing a significant transformation, driven by the need for enhanced situational awareness and rapid decision-making cycles in complex security environments. Modernization efforts focus on replacing siloed legacy platforms with interconnected, software-defined architectures.

- This shift is crucial for enabling multi-domain operations, where data from land, air, sea, space, and cyber assets are fused into a common operational picture. Key technologies like AI and machine learning are central to this evolution, with predictive analytics and automated data fusion tools helping commanders process vast amounts of intelligence, surveillance, and reconnaissance (ISR) data.

- For instance, a logistics command can use these systems for predictive maintenance, optimizing supply chain resilience and ensuring operational continuity. The adoption of open architecture frameworks promotes systems interoperability among allied forces, while zero-trust security models address pervasive cybersecurity vulnerabilities.

- This evolution toward intelligent, resilient, and integrated platforms is redefining strategic superiority and ensuring forces can maintain information dominance against sophisticated adversaries. The emphasis on a robust digital backbone supports this shift, making the command and control landscape more agile and responsive.

What will be the Size of the Command And Control Systems Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Command And Control Systems Market Segmented?

The command and control systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Government and defense

- Commercial

- Homeland security

- Platform

- Land

- Airborne

- Naval

- Space

- Solution

- Software

- Hardware

- Services

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- UK

- Germany

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Application Insights

The government and defense segment is estimated to witness significant growth during the forecast period.

The government and defense segment drives market demand, fueled by the imperative to modernize military infrastructure for multi-domain threats. A strategic shift is underway from legacy systems to agile, software-defined architectures supporting Joint All Domain Command and Control (JADC2) frameworks.

This transition prioritizes the integration of AI and cloud-native architectures for achieving decision superiority. Defense establishments are adopting open architecture frameworks and zero-trust security models to ensure systems interoperability and a high-fidelity operational picture.

These advanced battle management systems are crucial for national security, enabling forces to maintain a technological edge. The implementation of automated data fusion tools improves decision-making cycles by up to 40%, ensuring operational effectiveness in contested environments with resilient networks.

The Government and defense segment was valued at USD 11.00 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 63% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Command And Control Systems Market Demand is Rising in North America Get Free Sample

The geographic landscape of the command and control systems market is led by North America, which is projected to contribute approximately 63% of the market's incremental growth.

This dominance is driven by aggressive modernization initiatives focused on achieving JADC2 capabilities through software-defined architectures and AI integration.

The region's market is expanding at a rate of 3.5%, significantly outpacing Europe's 1.5% growth, reflecting substantial investments in cloud-native architectures and zero-trust security models to ensure information dominance.

APAC is also a fast-growing region, with nations focusing on building sovereign capabilities and modernizing forces to handle regional tensions.

The emphasis across all key geographies is on achieving systems interoperability and deploying resilient networks to maintain operational continuity in contested environments, making multi-domain integration a global priority.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of modern defense strategy hinges on the adoption of sophisticated command and control capabilities. Central to this is the implementation of ai driven decision support architectures, which are becoming standard for enhancing situational awareness for commanders.

- These systems enable the automated processing of battlefield data, allowing for the predictive analysis of adversary maneuvers and the rapid automating data classification and prioritization of threats. A key application is the orchestration of complex joint force operations, which requires seamless interoperability between allied nation forces.

- For example, the integration of an aegis combat system c2 integration with joint air and missile defense systems is now more streamlined. Systems like the integrated air and missile defense battle command system (ibcs) rely on this cohesion. The focus on mobility and flexibility is driving demand for software defined radio communication systems to ensure resilient command in contested environments.

- This is particularly vital for cyber hardened multi domain operations and the coordination of heterogeneous unmanned vehicles. Modernization programs, such as those for modernization of legacy ground control systems and global positioning systems operational control, are now prioritized.

- The effectiveness of distributed battle management command and control platforms, which focus on securing data integrity in transit, has shown to reduce response times by more than half compared to older, siloed systems. Ultimately, the successful deployment of technologies like the tactical airspace integration system functionality and integrated battle management system adoption defines the future of digital warfare.

What are the key market drivers leading to the rise in the adoption of Command And Control Systems Industry?

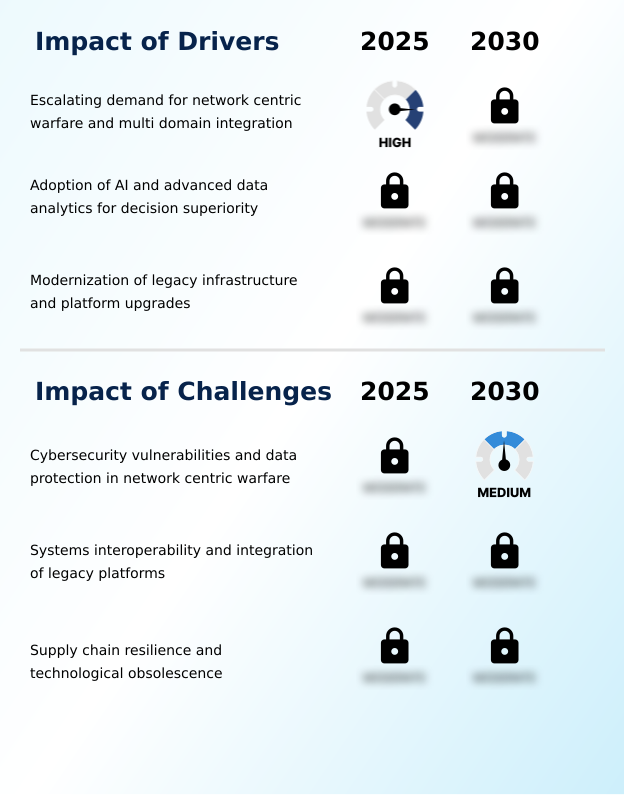

- The escalating demand for network-centric warfare capabilities and seamless multi-domain integration is a foundational driver propelling market expansion.

- The market is fundamentally driven by the need for network-centric warfare and multi-domain integration, improving the speed of information transfer by a factor of 10 in some cases.

- This enables forces to achieve a shared operational picture and attain decision superiority.

- A second major driver is the adoption of AI and predictive analytics to process vast data volumes, which can reduce the cognitive load on personnel by over 50%.

- These technologies automate the analysis of ISR data, allowing for faster identification of threats. Finally, the modernization of legacy infrastructure through open architecture frameworks is critical.

- This approach extends the life of existing assets while integrating modern capabilities like secure communication channels, making it a cost-effective strategy for maintaining operational readiness.

What are the market trends shaping the Command And Control Systems Industry?

- The integration of AI for autonomous orchestration is a transformative market trend. It enables automated, machine-driven decision support to manage complex operational data.

- A primary market trend is the integration of AI for autonomous orchestration, moving from manual data processing to automated, machine-driven decision support. This use of human-autonomy teaming and collaborative autonomy is essential for managing the high volume of sensor data on modern battlefields and reduces crew workload by up to 45%.

- Another key trend is the migration toward decentralized architectures and cloud-native designs. By utilizing edge computing solutions, forces can maintain information dominance in environments with degraded connectivity. This architectural shift ensures resilient networks and allows for rapid capability updates; deployment cycles for new software capabilities can be accelerated by over 70% compared to monolithic systems.

- This agility is critical for maintaining a technological edge.

What challenges does the Command And Control Systems Industry face during its growth?

- Persistent cybersecurity vulnerabilities and the critical need for data protection in network-centric warfare environments present a significant challenge to industry growth.

- A paramount challenge is managing escalating cybersecurity vulnerabilities, as the shift to interconnected digital battlefields can increase the attack surface for cyber threats by up to 300%. Ensuring data integrity protection requires constant monitoring and the implementation of zero-trust security models, which is a resource-intensive task.

- Another significant hurdle is systems interoperability, particularly the integration of modern software with legacy hardware. These legacy platform integration projects often exceed budgets by 25-40% due to the complexity of bridging proprietary systems. Furthermore, supply chain resilience is a growing concern.

- Geopolitical tensions create risks of component shortages and technological obsolescence, threatening the production and long-term readiness of mission-critical systems and disrupting operational continuity.

Exclusive Technavio Analysis on Customer Landscape

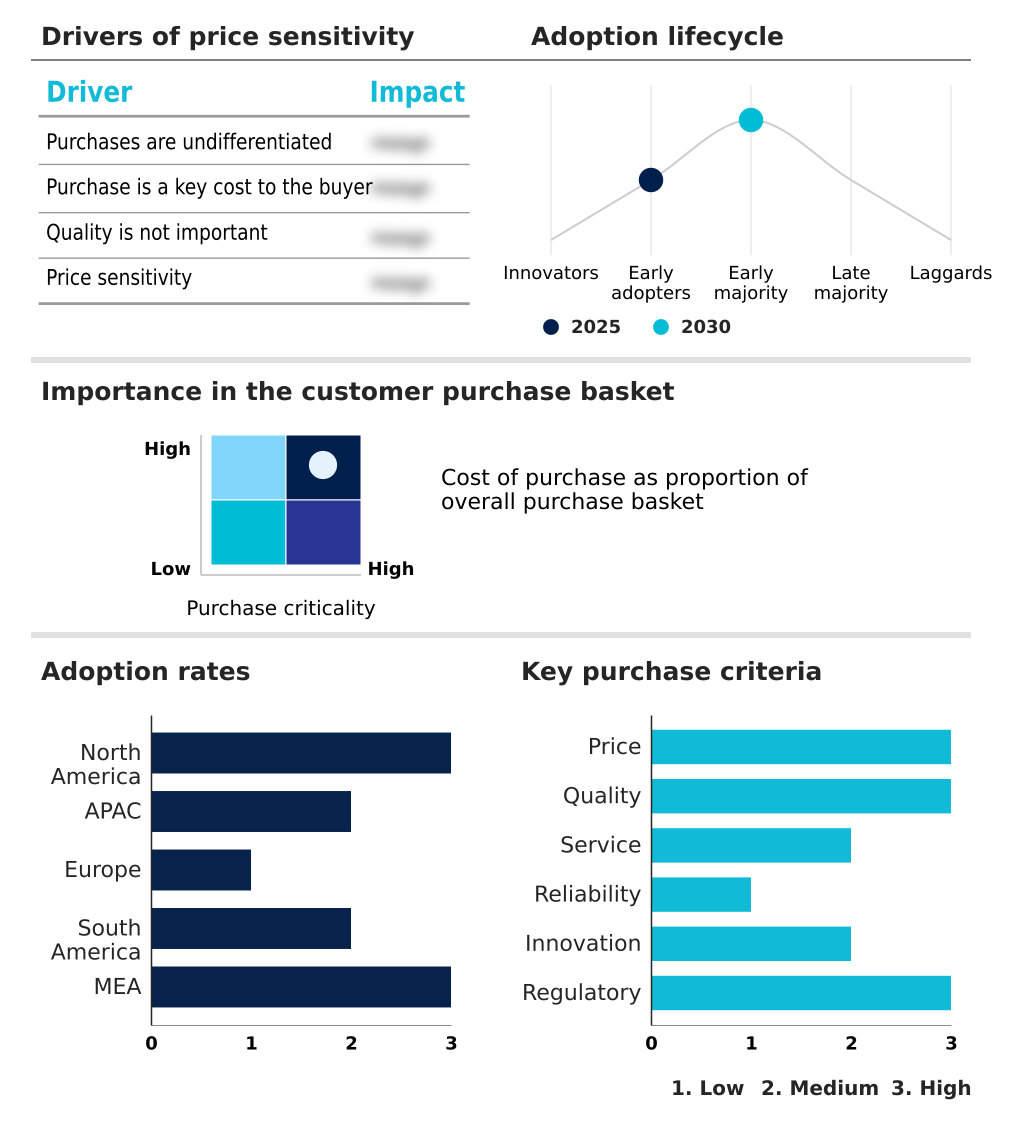

The command and control systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the command and control systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Command And Control Systems Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, command and control systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Airbus SE - Offers integrated battle management, air defense coordination, and battlefield situational awareness through a suite of advanced command and control systems solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airbus SE

- Atos SE

- BAE Systems Plc

- Elbit Systems Ltd.

- General Dynamics Corp.

- IBM Corp.

- Indra Sistemas SA

- Kongsberg Gruppen ASA

- L3Harris Technologies Inc.

- Leidos Holdings Inc.

- Leonardo S.p.A.

- Lockheed Martin Corp.

- Motorola Solutions Inc.

- Northrop Grumman Corp.

- Palantir Technologies Inc.

- Rheinmetall AG

- RTX Corp.

- Saab AB

- Thales Group

- The Boeing Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Command and control systems market

- In January 2025, the Department of Defense released the Defense Business Board report on supply chain illumination, recommending enhanced visibility and risk mitigation across critical defense sectors.

- In August 2025, the United States Navy awarded Northrop Grumman a significant contract for the Providence Distributed Battle Management Command and Control Systems, aiming to enhance interoperable and secure information dominance.

- In September 2025, the Department of Defense added the K1000ULE unmanned aerial system to the Blue UAS Cleared List, enabling its use for collaborative teaming and shared mission layer operations across multiple domains.

- In April 2026, the United States Space Force terminated its contract with RTX for the Global Positioning Systems Next Generation Operational Control System, signaling a strategic shift toward more rapid, incremental capability delivery models.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Command And Control Systems Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 310 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 2.3% |

| Market growth 2026-2030 | USD 3074.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 2.3% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, UK, Germany, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The command and control systems market is advancing rapidly, driven by the strategic shift toward network-centric warfare and multi-domain integration. The core objective is achieving decision superiority by leveraging technologies like AI, predictive analytics, and data fusion tools. These systems process vast streams of intelligence, surveillance, and reconnaissance (ISR) data to create a common operational picture, enhancing situational awareness.

- A key boardroom consideration is the investment in open architecture frameworks and Modular Open Systems Approach (MOSA), which mitigate technological obsolescence and improve systems interoperability. Modern battle management systems, such as the command post of the future (CPOF), are essential for mission planning and battlefield visualization.

- The adoption of cloud-native and decentralized architectures, combined with edge computing solutions, ensures operational resilience against anti-access/area denial (A2AD) tactics. Moreover, implementing zero-trust security models is critical for countering cybersecurity vulnerabilities. This integrated approach reduces the time to achieve a shared operational picture by over 60% compared to legacy systems, enabling effective joint force operations and robust electronic warfare resilience.

What are the Key Data Covered in this Command And Control Systems Market Research and Growth Report?

-

What is the expected growth of the Command And Control Systems Market between 2026 and 2030?

-

USD 3.07 billion, at a CAGR of 2.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Government and defense, Commercial, and Homeland security), Platform (Land, Airborne, Naval, and Space), Solution (Software, Hardware, and Services) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalating demand for network centric warfare and multi domain integration, Cybersecurity vulnerabilities and data protection in network centric warfare

-

-

Who are the major players in the Command And Control Systems Market?

-

Airbus SE, Atos SE, BAE Systems Plc, Elbit Systems Ltd., General Dynamics Corp., IBM Corp., Indra Sistemas SA, Kongsberg Gruppen ASA, L3Harris Technologies Inc., Leidos Holdings Inc., Leonardo S.p.A., Lockheed Martin Corp., Motorola Solutions Inc., Northrop Grumman Corp., Palantir Technologies Inc., Rheinmetall AG, RTX Corp., Saab AB, Thales Group and The Boeing Co.

-

Market Research Insights

- The dynamics of the command and control systems market are defined by the pursuit of information dominance and strategic superiority. Modern defense forces are architecting a new digital backbone, shifting from legacy platforms to agile, software-defined architectures to support multi-domain operations. The core objective is ensuring operational continuity on digital battlefields.

- This transition addresses national security priorities by enabling mission-critical responsiveness and a high-fidelity operational picture. Systems leveraging AI have been shown to improve decision-making cycles by up to 40% and reduce the cognitive load on personnel by over 50%.

- The emphasis is on incremental capability delivery and building resilient networks for effective threat landscape navigation, ensuring robust command chain protection and maintaining command authority in any scenario.

We can help! Our analysts can customize this command and control systems market research report to meet your requirements.

RIA -

RIA -