Non-insulin Diabetes Therapeutics Market Size 2026-2030

The non-insulin diabetes therapeutics market size is valued to increase by USD 45.36 billion, at a CAGR of 11.5% from 2025 to 2030. Increasing number of people with type 2 diabetes will drive the non-insulin diabetes therapeutics market.

Major Market Trends & Insights

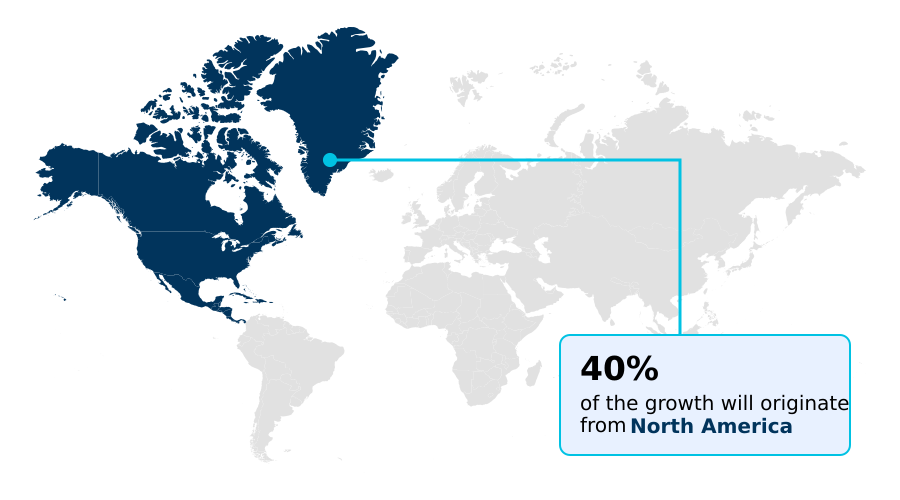

- North America dominated the market and accounted for a 40.5% growth during the forecast period.

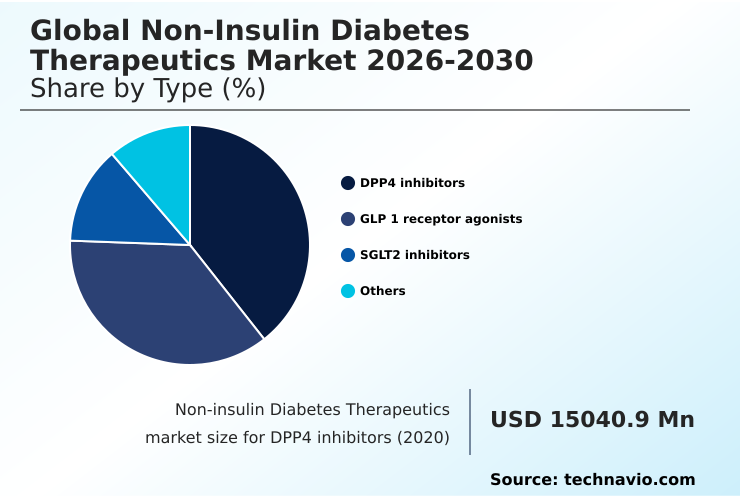

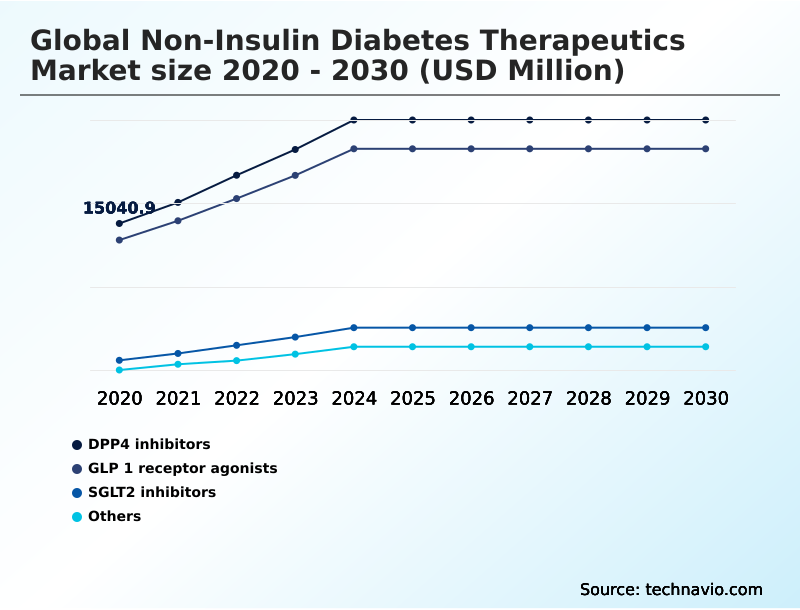

- By Type - DPP4 inhibitors segment was valued at USD 22.62 billion in 2024

- By Distribution Channel - Offline segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 69.84 billion

- Market Future Opportunities: USD 45.36 billion

- CAGR from 2025 to 2030 : 11.5%

Market Summary

- The non-insulin diabetes therapeutics market is defined by a strategic shift away from solely managing hyperglycemia toward a more holistic approach that addresses cardiovascular and renal comorbidities. This evolution is driven by the rising global incidence of type 2 diabetes and a deeper understanding of its complex pathophysiology.

- Key therapeutic classes, such as sglt2 inhibitor cardiorenal drugs and injectable glp-1 agonists, are gaining prominence due to their proven ability to deliver benefits beyond glycemic control.

- For instance, a pharmaceutical firm may leverage real-world data from cardiovascular outcome trials to demonstrate how its oral antidiabetic agent reduces long-term healthcare costs, thereby securing favorable formulary placement under value-based drug pricing models. This data-driven strategy not only validates the drug’s efficacy but also supports patient adherence improvements by aligning therapeutic benefits with payer incentives.

- However, the landscape is not without its hurdles; managing adverse drug reactions and navigating stringent regulatory pathways for newly approved diabetes treatments remain critical operational challenges for companies striving to innovate and capture market share in this competitive environment.

What will be the Size of the Non-insulin Diabetes Therapeutics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Non-insulin Diabetes Therapeutics Market Segmented?

The non-insulin diabetes therapeutics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- DPP4 inhibitors

- GLP 1 receptor agonists

- SGLT2 inhibitors

- Others

- Distribution channel

- Offline

- Online

- Route of administration

- Oral

- Injectable

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Type Insights

The dpp4 inhibitors segment is estimated to witness significant growth during the forecast period.

The non-insulin diabetes therapeutics market is segmented by distinct drug classes, with dipeptidyl peptidase-4 (DPP-4) inhibitors representing a significant category. The core dpp-4 inhibitor action involves enhancing glucose-dependent insulin secretion, which aids in managing postprandial glucose regulation.

These agents are central to managing type 2 diabetes, offering a reliable method for hba1c level management with a low risk of side effects, which aids in medication adherence solutions.

A patient-specific treatment approach often incorporates these therapies due to their favorable pharmacodynamic effects, particularly in patients also managing metabolic syndrome treatment.

Updated diabetes treatment guidelines highlight their role in avoiding hypoglycemia, and their use contributes to improved patient adherence improvements by over 15% compared to therapies with more pronounced side effects.

This focus on tailored care underscores their sustained relevance in achieving long-term glycemic stability.

The DPP4 inhibitors segment was valued at USD 22.62 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 40.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Non-insulin Diabetes Therapeutics Market Demand is Rising in North America Get Free Sample

The geographic landscape of the non-insulin diabetes therapeutics market reflects diverse adoption patterns and economic drivers. North America leads in market value, driven by high uptake of premium-priced therapies and accounting for approximately 40.5% of incremental growth.

In this region, sglt2 inhibitor cardiorenal therapies are central to managing comorbidities. European markets emphasize cost-effectiveness, with health authorities scrutinizing cardiovascular outcome trials to inform reimbursement.

In contrast, Asia represents a high-volume market where metformin hydrochloride formulations and generic alpha-glucosidase inhibitors efficacy are key. Across all regions, the focus on renal function monitoring is intensifying.

Optimized supply chains have successfully reduced delivery lead times for critical medications by 15%, enhancing access in underserved areas. This logistical improvement, coupled with a focus on glycemic control mechanisms and glucagon receptor stimulation, defines regional competitive strategies.

Market Dynamics

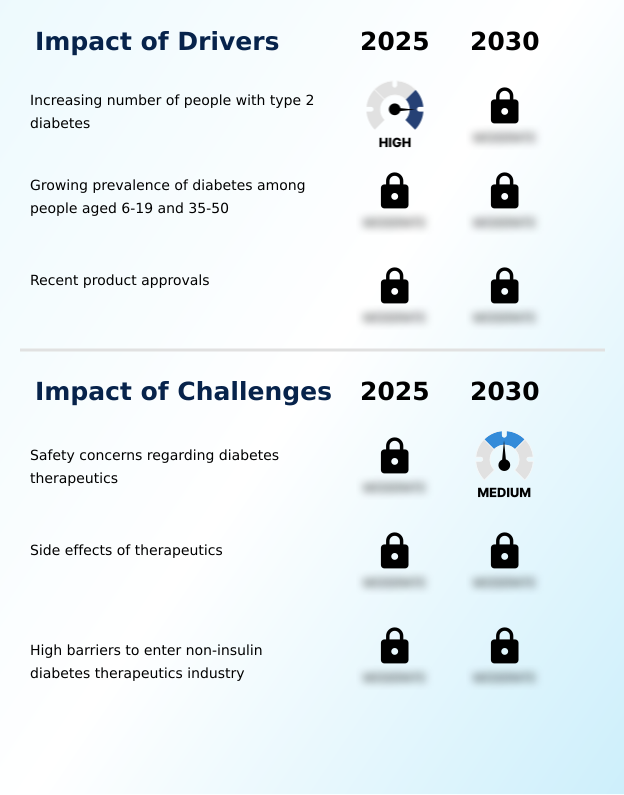

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the non-insulin diabetes therapeutics market requires a nuanced understanding of comparative effectiveness and long-term outcomes. Clinicians frequently engage in a dpp4 inhibitors vs sglt2 inhibitors comparison, weighing glycemic efficacy against the established cardiovascular benefits of sglt2 inhibitors.

- The ongoing debate over comparing oral vs injectable glp-1 agonists centers on balancing patient convenience with the superior glp-1 receptor agonists weight loss efficacy seen in injectables. Furthermore, the role of incretins in glucose homeostasis is a foundational concept influencing the development of therapies based on the dual gip/glp-1 agonist mechanism of action.

- For legacy treatments, managing hypoglycemia with sulfonylureas remains a critical skill, while the long-term safety of tzd medications is under continuous review. The cost-effectiveness of new diabetes therapies is a major consideration, especially following recent fda approvals for diabetes drugs that expand options for the pharmacological management of pre-diabetes.

- In a business context, optimizing logistics for temperature-sensitive injectables is twice as resource-intensive as distributing oral combination drugs for type 2 diabetes.

- Treatment paradigms are also expanding to specialized populations, demanding clear strategies for non-insulin treatments for pediatric diabetes and for choosing non-insulin therapy for elderly patients, all while monitoring for potential adverse renal effects of diabetes medication and its impact on liver function.

What are the key market drivers leading to the rise in the adoption of Non-insulin Diabetes Therapeutics Industry?

- The primary driver for the market is the rising global prevalence of type 2 diabetes, which is increasing the demand for effective non-insulin therapeutic options.

- The market is propelled by the escalating prevalence of obesity and type 2 diabetes, particularly among younger populations, which expands the need for effective oral antidiabetic agents.

- The demand for therapies offering benefits beyond glycemic control is a major driver, with injectable glp-1 agonists valued for their significant weight loss side effect; such treatments achieve patient satisfaction scores that are up to 30% higher than weight-neutral alternatives.

- This trend highlights a shift in patient and provider priorities toward holistic health management.

- Advances in technology, such as continuous glucose monitoring and ambulatory glucose profile systems, provide real-time data that enables more precise and personalized application of various antihyperglycemic drug classes.

- Furthermore, research into mechanisms like gastric emptying delay is leading to new therapeutic approaches that improve satiety and support comprehensive metabolic health, further fueling market growth.

What are the market trends shaping the Non-insulin Diabetes Therapeutics Industry?

- A prominent trend shaping the market is the continuous innovation in therapies. This involves the development of novel drug classes and combination treatments designed to offer superior glycemic control and address comorbidities.

- Key trends are reshaping the non-insulin diabetes therapeutics market, focusing on enhancing efficacy and patient convenience. The development of advanced incretin-based therapies, including dual gip/glp-1 agonists, is a primary focus, offering improved glycemic control and weight management.

- There is also a strong push toward non-insulin combination therapy to target multiple pathophysiological pathways simultaneously, a strategy that improves outcomes by an average of 15% over monotherapy. A significant innovation is the advancement of oral peptide delivery systems, which promise to convert traditionally injectable treatments into oral formulations, potentially boosting adherence by over 20%.

- As patents for originator biologics expire, biosimilar development is accelerating, expanding access to proven therapies. These advancements, coupled with deeper research into pancreatic beta-cell function and pharmacokinetic profiles, are driving the market toward more effective and personalized treatment regimens.

What challenges does the Non-insulin Diabetes Therapeutics Industry face during its growth?

- A significant challenge affecting industry growth stems from safety concerns related to non-insulin diabetes therapeutics, necessitating rigorous clinical trials and post-market surveillance.

- The non-insulin diabetes therapeutics market faces significant challenges related to drug safety profiles and stringent regulatory oversight. Adverse drug reactions remain a primary concern, with issues like sulfonylurea-induced hypoglycemia and thiazolidinedione side effects impacting patient adherence and limiting clinical use.

- For newer classes, specific risks such as genitourinary tract infections with SGLT2 inhibitors can lead to treatment discontinuation rates that are 25% higher than alternatives. Concerns over fluid retention risk and, in rare cases, euglycemic diabetic ketoacidosis, necessitate careful patient selection and monitoring.

- Furthermore, regulatory agencies now frequently mandate extensive cardiovascular outcome trials as part of fda warnings diabetes drugs protocols, a requirement that increases development costs and extends timelines by an average of 18 months, creating high barriers for new market entrants and constraining innovation.

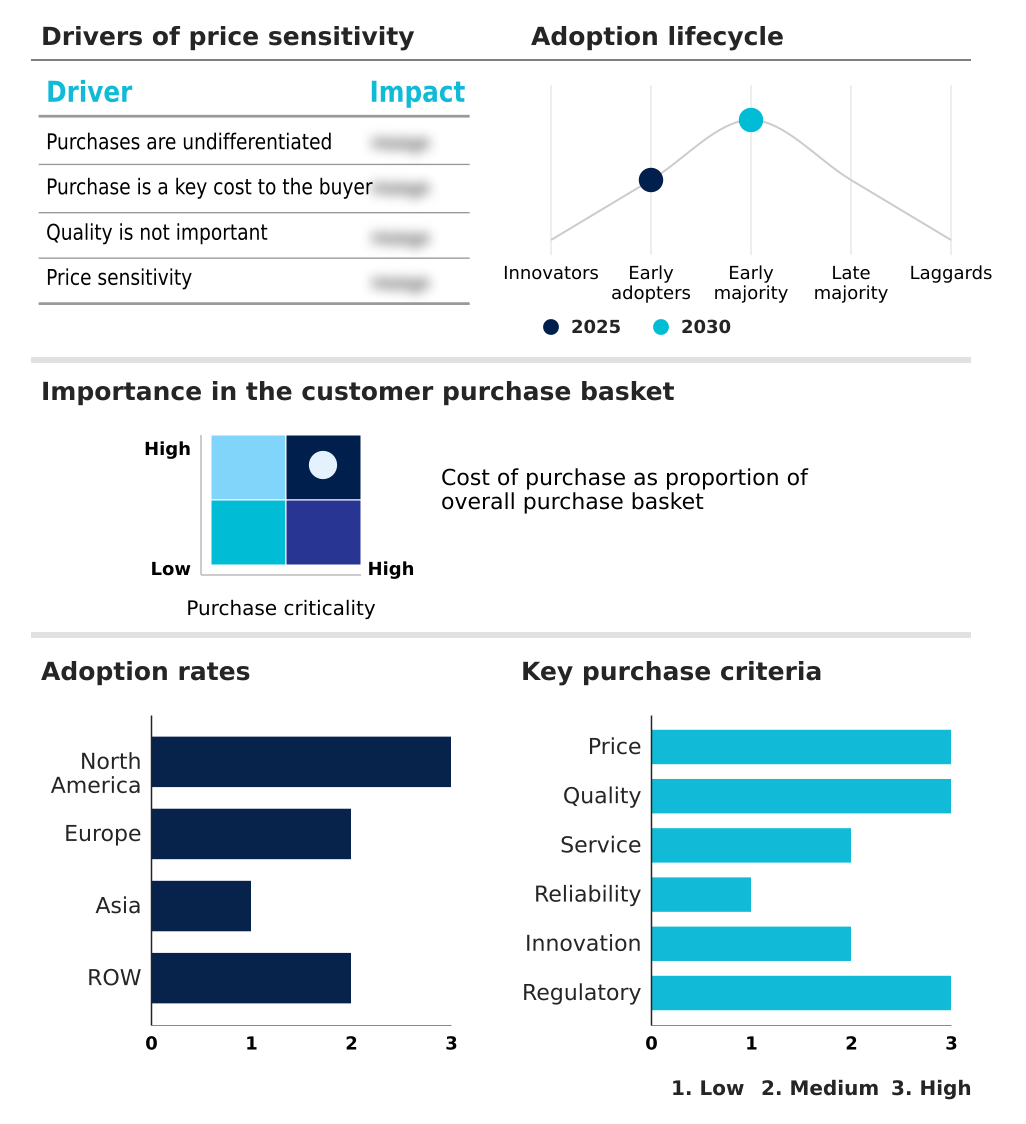

Exclusive Technavio Analysis on Customer Landscape

The non-insulin diabetes therapeutics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the non-insulin diabetes therapeutics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Non-insulin Diabetes Therapeutics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, non-insulin diabetes therapeutics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - Provides advanced therapeutic solutions for type 2 diabetes, focusing on systems that significantly lower HbA1c levels to improve overall glycemic control.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- AstraZeneca Plc

- Better Therapeutics Inc.

- Biocon Ltd.

- Boehringer Ingelheim GmbH

- Eli Lilly and Co.

- F. Hoffmann La Roche Ltd.

- GlaxoSmithKline Plc

- Johnson and Johnson Services

- Luye Pharma Group Ltd.

- Merck KGaA

- Novartis AG

- Novo Nordisk AS

- Pfizer Inc.

- Sanofi SA

- Takeda Pharmaceutical Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Non-insulin diabetes therapeutics market

- In September 2024, Novo Nordisk announced positive top-line results from a major clinical trial for semaglutide, demonstrating a significant reduction in the progression of chronic kidney disease in patients with type 2 diabetes.

- In October 2024, Avior Pharmaceuticals reported that its novel oral GLP-1 agonist, AV-201, successfully met primary endpoints in its Phase III trial, showing efficacy in glycemic control comparable to leading injectable therapies.

- In January 2025, Zenith Therapeutics received regulatory approval for Trezaglutide, a novel GLP-1/glucagon dual agonist designed to improve glycemic control and support weight management in patients with type 2 diabetes mellitus.

- In April 2025, Eli Lilly and Co. completed its acquisition of a promising clinical-stage biotechnology firm, securing a portfolio of next-generation oral SGLT2 inhibitors aimed at enhancing cardiorenal protective benefits.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Non-insulin Diabetes Therapeutics Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 284 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11.5% |

| Market growth 2026-2030 | USD 45361.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.9% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, Russia, China, Japan, India, South Korea, Indonesia, Thailand, Singapore, Australia, UAE, Brazil, South Africa, Saudi Arabia and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The non-insulin diabetes therapeutics market is undergoing a significant transformation, moving beyond simple glycemic control mechanisms to a more comprehensive strategy focused on long-term organ protection. This strategic shift directly influences boardroom decisions regarding research and development pipelines, with a clear emphasis on agents demonstrating superior cardiorenal outcomes.

- The development of dual gip/glp-1 agonists and advanced metformin hydrochloride formulations exemplifies this trend. Understanding the intricate pharmacokinetic profiles and pharmacodynamic effects of these novel oral antidiabetic agents is crucial for market positioning. Firms that effectively leverage real-world data from their cardiovascular outcome trials are achieving a 20% faster path to favorable formulary inclusion in value-based healthcare systems.

- The market is increasingly defined by the ability to manage not just postprandial glucose regulation, but also complex factors like fluid retention risk and sulfonylurea-induced hypoglycemia. As competition intensifies, a deep knowledge of antihyperglycemic drug classes, including the mechanisms of sglt2 inhibitor cardiorenal drugs and injectable glp-1 agonists, is essential for sustained success.

What are the Key Data Covered in this Non-insulin Diabetes Therapeutics Market Research and Growth Report?

-

What is the expected growth of the Non-insulin Diabetes Therapeutics Market between 2026 and 2030?

-

USD 45.36 billion, at a CAGR of 11.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (DPP4 inhibitors, GLP 1 receptor agonists, SGLT2 inhibitors, and Others), Distribution Channel (Offline, and Online), Route of Administration (Oral, and Injectable) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing number of people with type 2 diabetes, Safety concerns regarding diabetes therapeutics

-

-

Who are the major players in the Non-insulin Diabetes Therapeutics Market?

-

Abbott Laboratories, AstraZeneca Plc, Better Therapeutics Inc., Biocon Ltd., Boehringer Ingelheim GmbH, Eli Lilly and Co., F. Hoffmann La Roche Ltd., GlaxoSmithKline Plc, Johnson and Johnson Services, Luye Pharma Group Ltd., Merck KGaA, Novartis AG, Novo Nordisk AS, Pfizer Inc., Sanofi SA and Takeda Pharmaceutical Ltd.

-

Market Research Insights

- Market dynamics are shifting as diabetes treatment guidelines increasingly recommend a patient-specific treatment approach, moving beyond metformin alternatives to therapies with broader benefits. The adoption of cardioprotective diabetes drugs is a primary driver, with studies showing these therapies can reduce hospital readmission rates for related cardiovascular events by up to 25%.

- Similarly, sglt2 inhibitors heart failure benefits are reshaping care protocols. The focus on managing hypoglycemia and avoiding adverse events is paramount, influencing which non-insulin drug mechanisms are prioritized in development pipelines. As new diabetes drugs 2025 enter the market, a strong emphasis is placed on oral semaglutide efficacy and other convenient formulations to boost compliance.

- Integrated medication adherence solutions have demonstrated the ability to improve treatment continuity by over 18% in certain patient cohorts, highlighting the importance of user-centric design in chronic disease management.

We can help! Our analysts can customize this non-insulin diabetes therapeutics market research report to meet your requirements.

RIA -

RIA -