North America Building Automation Systems Market Size 2024-2028

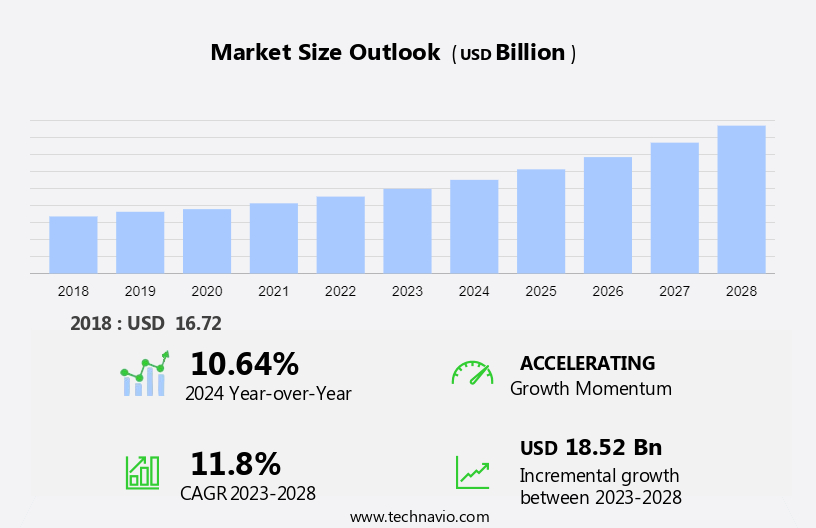

The North America building automation systems market size is forecast to increase by USD 18.52 billion billion at a CAGR of 11.8% between 2023 and 2028.

- The market in North America is witnessing significant growth due to several key trends. The increasing focus on sustainability and green building practices is driving the adoption of BAS, as these systems enable energy efficiency and reduce carbon footprint. Furthermore, the integration of predictive analytics and artificial intelligence in BAS is revolutionizing the way buildings are managed and maintained, leading to improved operational efficiency and reduced downtime. However, the market also faces challenges, including cybersecurity risks and vulnerabilities associated with BAS. As buildings become increasingly connected, securing these systems against cyber threats is becoming a top priority for building owners and operators. Despite these challenges, the future of the BAS market in North America looks promising, with continued innovation and advancements in technology expected to drive growth.

What will be the size of the North America Building Automation Systems Market during the forecast period?

- The North American building automation systems market is experiencing significant growth, driven by the increasing adoption of smart buildings and the integration of advanced technologies. These systems enable the automation and optimization of various building functions, including HVAC, lighting, security, access control, and energy management. Sensors and actuators, coupled with networking technologies such as IoT and 5G, facilitate real-time monitoring and control of building systems, enhancing efficiency, safety, and energy consumption. Building automation solutions encompass a range of electronic, mechanical, and electrical systems, including semiconductor chips, lighting controls, fire detection, and HVAC controls.

- The market's expansion is fueled by the demand for energy-efficient buildings, integrated systems, and the ongoing digitization of construction activities. Overall, the North American building automation systems market is poised for continued growth, offering opportunities for innovation and improvement in building control and management systems.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Commercial

- Industrial

- Residential

- Technology

- Wired

- Wireless

- Geography

- North America

- US

- Canada

- Mexico

- North America

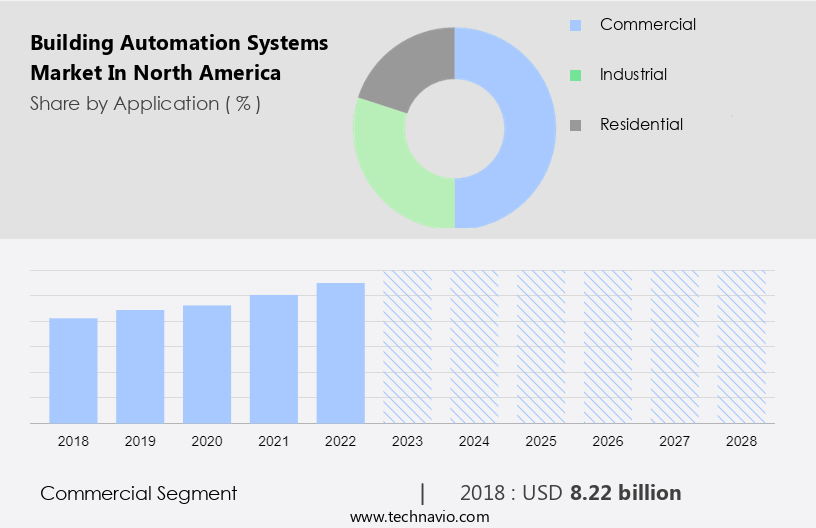

By Application Insights

The commercial segment is estimated to witness significant growth during the forecast period. The North American market for Building Automation Systems (BAS) is experiencing significant growth due to the increasing adoption of smart buildings. These intelligent structures prioritize data-driven building management solutions to optimize occupant comfort, boost operational efficiency, and promote sustainability. Urbanization and commercial construction projects, such as offices, retail spaces, hospitality venues, and healthcare facilities, present ample opportunities for BAS implementation in both new builds and retrofits. Financial incentives, including government grants, utility rebates, tax credits, and financing programs, encourage building owners to invest in energy-efficient technologies, including BAS. These incentives help offset upfront costs and expedite the adoption of BAS In the commercial sector.

Get a glance at the market share of various segments Request Free Sample

The commercial segment was valued at USD 8.22 billion in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of North America Building Automation Systems Market?

- Growing focus on sustainability and green building practices is the key driver of the market. Sustainability regulations, energy codes, and green building certifications, including LEED, fuel the demand for Building Automation Systems (BAS) in North America. These solutions optimize energy usage and reduce carbon emissions by providing precise control and monitoring of building systems such as HVAC, lighting, and ventilation. The integration of renewable energy sources like solar PV and wind power is a key aspect of green building practices, and BAS plays a pivotal role in managing and optimizing their generation, storage, and distribution. Smart control strategies enable BAS to balance energy supply and demand, maximize self-consumption of renewable energy, and support grid interaction.

- Additionally, sensors, actuators, and networking technologies facilitate the integration of IoT, IP-based devices, and SaaS platforms, enhancing building efficiency and enabling real-time monitoring and analysis of energy usage. Safety concerns, including security breaches, employee tampering, and safety issues such as gas leaks, fires, and air quality, are addressed through advanced safety systems, access control management, and machine learning algorithms. BAS solutions encompass a range of systems, including HVAC, lighting, security, access control, and energy management, and are essential for facility management in commercial, industrial, and residential buildings. The adoption of 5G technology and integrated systems further enhances the capabilities of energy-efficient buildings, enabling seamless communication between various building systems and improving overall building performance.

What are the market trends shaping the North America Building Automation Systems Market?

- Integration of predictive analytics and AI with BAS is the upcoming trend In the market. Building Automation Systems (BAS) in North America leverage predictive analytics and artificial intelligence (AI) algorithms to optimize building performance and energy consumption. These technologies analyze historical data from sensors, equipment, and IT data to identify patterns and predict potential issues, enabling proactive maintenance and extending asset lifespan. BAS can optimize energy usage by analyzing building usage patterns, weather forecasts, and energy demand data, dynamically adjusting HVAC settings, lighting controls, and other systems to minimize energy waste while maintaining comfort levels. This results in significant cost savings and reduced environmental impact for various building types, including commercial, industrial, and residential structures.

- Additionally, BAS can enhance safety by integrating with security systems, access control, fire systems, and environmental systems to mitigate risks related to employee tampering, security breaches, gas leaks, fires, and air quality concerns. The Internet of Things (IoT) and network-connected devices, such as IP-based sensors and actuators, enable remote monitoring and management of BAS, further enhancing efficiency and waste minimization. The integration of 5G technology and SaaS solutions offers opportunities for real-time data processing and advanced analytics, driving the growth of the BAS market in North America.

What challenges does North America Building Automation Systems Market face during the growth?

- Cybersecurity risks and vulnerabilities associated with BAS is a key challenge affecting the market growth. Building Automation Systems (BAS) in North America are essential for optimizing construction activities in commercial, industrial, and residential buildings. These systems utilize sensors, actuators, and networking technologies to manage HVAC, lighting, security, access control, energy management, and building efficiency. IoT and IP-based devices enable remote monitoring and SaaS solutions, while machine learning enhances building systems' interface and performance. However, BAS systems face cybersecurity challenges. Malicious actors can exploit vulnerabilities in network infrastructure, software applications, and communication protocols, leading to unauthorized access and control, system manipulation, and operational disruptions.

- Malware, ransomware, and Denial-of-Service (DoS) attacks pose significant risks, compromising system functionality, encrypting critical data, and causing downtime, resulting in financial losses. Building owners and operators must prioritize cybersecurity measures to protect against these threats and ensure building safety and efficiency.

Exclusive North America Building Automation Systems Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Carrier Global Corp

- Emerson Electric Co.

- Honeywell International Inc.

- Hubbell Inc.

- Johnson Controls

- Legrand

- Mitsubishi Electric Corp.

- OMRON Corp.

- Robert Bosch GmbH

- Schneider Electric SE

- Siemens AG

- Texas Instruments Inc.

- Trane Technologies plc

- Rockwell Automation Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is experiencing significant growth due to the increasing adoption of smart buildings and the integration of various technologies. These systems enable the optimization of various building functions, including HVAC, lighting, security, and access control, among others. Sensors and actuators play a crucial role in building automation, allowing for real-time monitoring and control of various environmental and operational conditions. Networking technologies, such as IoT and IP-based devices, facilitate the communication and integration of these systems, enabling remote monitoring and management. Energy management is a key focus area for building automation, with systems designed to optimize energy usage and improve building efficiency.

In addition, building efficiency is becoming increasingly important as energy consumption continues to rise, and the need to minimize waste and reduce environmental impact becomes more pressing. Facility management is another area where building automation is making a significant impact. By automating various building functions, facility managers can more easily monitor and control systems, reducing the need for manual intervention and improving overall operational efficiency. The integration of various building systems, including electrical, electronic, and mechanical systems, is a major trend in building automation. Integrated systems enable more efficient and effective building management, reducing energy consumption and improving safety and security.

Moreover, building automation systems also offer various safety features, such as fire detection and safety systems, ensuring the safety of building occupants and minimizing potential risks. Access control systems and security systems are also important components, providing building owners and managers with greater control over access to their properties and protecting against potential threats, including employee tampering and cyberattacks. The building automation market in North America is expected to continue growing, driven by the increasing adoption of smart buildings and the need to improve building efficiency and safety. The integration of various technologies, including IoT, machine learning, and 5G technology, is also expected to drive growth, enabling more advanced building automation solutions and improving the overall user experience.

Furthermore, building automation systems are being adopted across various sectors, including commercial, industrial, and residential buildings. In the commercial segment, office buildings, institutional facilities, healthcare facilities, hotels and restaurants, retail stores, and IT tech parks are all adopting building automation systems to improve operational efficiency and reduce energy consumption. In the industrial sector, building automation is being used to optimize manufacturing processes and improve safety, while In the residential sector, apartment dwellers are adopting smart door locks, wireless intercom devices, and other network-connected devices to enhance security and convenience. Despite the many benefits of building automation, there are also challenges, including the need for cybersecurity measures to protect against potential cyberattacks and the need for regular system updates and maintenance to ensure optimal performance.

In addition, sanitization systems are also becoming increasingly important, particularly In the wake of the COVID-19 pandemic, to ensure the health and safety of building occupants. The integration of various technologies, including IoT, machine learning, and 5G technology, is enabling more advanced building automation solutions and improving the overall user experience. However, there are also challenges that must be addressed, including cybersecurity and regular system maintenance, to ensure the optimal performance of building automation systems.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

153 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 11.8% |

|

Market growth 2024-2028 |

USD 18.52 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

10.64 |

|

Competitive landscape |

Leading Companies, Market Report, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -