North America French Fries Market Size 2024-2028

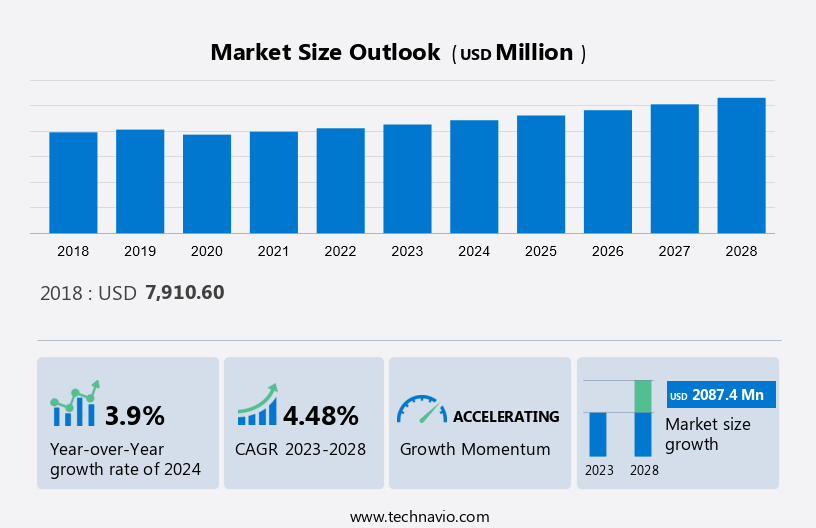

The North American French Fries Market size is projected to increase by USD 2.09 billion and the market size is estimated to grow at a CAGR of 4.48% between 2023 and 2028. The market in North America is experiencing significant growth due to several key factors. Firstly, the increased online presence of frozen variants is driving sales, as consumers turn to e-commerce platforms for convenience and accessibility. Secondly, the market is witnessing a surge in new product launches, with companies introducing innovative flavors and vegan options to cater to diverse consumer preferences. Lastly, the rising trend of veganism is fueling market growth, as more consumers seek plant-based alternatives to traditional animal-derived products. These factors collectively contribute to a dynamic and evolving market landscape in North America.

Market Overview

To get additional information about the market, Request Free Sample

Market Dynamics

In the market, fastfood chains continue to cater to the steady demand stream for their menu items, including staple side dishes. With health conscious trends on the rise, many chains are exploring baked or air fried options to offer healthier alternatives to their customers. Fastfood franchises and retail outlets, including drive-thru outlets, prioritize quality, speed, and convenience, ensuring a diverse and innovative food selection that appeals to a wide audience. Weather conditions and pests can pose challenges to the production and distribution of regular ones. To mitigate these risks, institutional buyers increasingly turn to frozen meals and snacks, which offer extended shelf life and consistency in taste and texture. The frozen snacks industry, including frozen ones, has seen steady growth due to smaller households' preference for convenient takeaway options. Menu items at fastfood chains and retail outlets, such as sandwiches and baked goods, also incorporate them as ingredients or side dishes. As the market evolves, fastfood franchises and retail outlets, including hotels, continue to offer diverse and innovative food options, ensuring a steady demand in North America.

Key Market Driver

Increased online presence of frozen french fries is driving the market growth. There has been an increasing preference by consumers to buy them through online platforms. One of the main reasons for this growing preference is the convenience the online platform offers its consumers. Another advantage is that online platforms often offer a broader range of frozen potato fry brands, flavors, and packaging sizes than physical or brick-and-mortar retail stores.

Furthermore, factors such as the online channel appeal to consumers with specific preferences, including in terms of different cuts, seasonings, or specialty options. Hence, such factors are expected to drive the growth of the market in North America during the forecast period. It also includes an in-depth analysis of drivers, trends, and challenges. Hence, such factors are driving the market growth during the forecast period.

Significant Market Trends

The rising demand for ready-to-cook (RTC) food options is expected to have a positive impact on the market in the coming years. There has been an increasing demand for ready-to-cook food due to the changing lifestyles and preferences of consumers globally. One of the main advantages is that offers convenience to busy individuals or families who may not have the time or inclination to cook a meal from scratch.

Factors such as hectic schedules and changing lifestyles are significantly contributing to the growth of ready-to-cook food product variants. These food variants typically come with pre-measured ingredients and easy-to-follow instructions, allowing consumers to prepare a meal quickly and easily. Furthermore, they offer the ultimate convenience as they are pre-cut, pre-cooked, and ready to be baked or fried and eliminate the need for meal planning, grocery shopping, and extensive preparatory work. Hence, these factors are expected to drive the growth of the market in North America during the forecast period.

Major Market Challenge

Growing demand for homemade and street potato fries decreases demand for packaged variants will be a major challenge for the market in North America during the forecast period. There is an increasing preference by consumers for potato-based snacks that are prepared at food service establishments. However, these types of food variants are also available as street food.

For instance, mashed potato cutlets and fries, which are made with potatoes and various other ingredients, are popular street foods in India that can be a potential alternative. Hence, these substitutes which are available at various street food joints and establishments are expected to negatively impact the market growth in North America during the forecast period.

Market Segmentation

By End-User

The growing number of QSRs and restaurants is expected to drive the growth of the food service segment of the market in North America during the forecast period. As many food service outlets offer a wide range of processed potato products, potato patties, and other related items which cater to a broad consumer segment, the demand will remain consistent in the steadily growing food service in North America. Additionally, the rapidly increasing quick-service restaurants (QSRs) are expected to significantly fuel the growth of the market as well. There has been an increasing demand for quick-service restaurants (QSRs) among consumers as it offer value-based menus and quick services. Hence, such factors are expected to drive the growth of this segment which in turn will drive the growth of the market in North America during the forecast period.

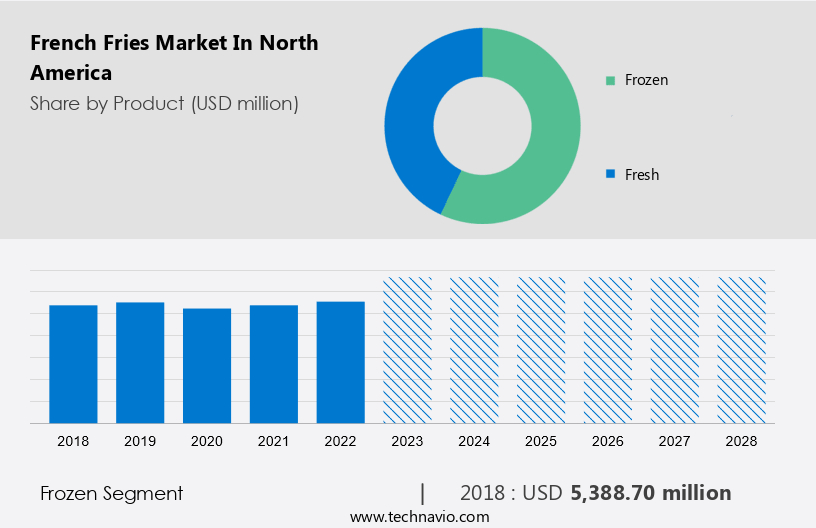

By Product

The market share growth by the frozen segment will be significant during the forecast period. There has been an increasing preference among consumers of all ages across the world due to factors such as they are easy to cook, involve less preparation time, and are cost-effective.

The Frozen Segment was valued at USD 5.39 billion in 2018 and continued to grow until 2022.

For a detailed summary of the market segments Request for Sample Report

Some of the main health benefits of consuming them include a high amount of vitamin C and starch, fibre, protein, iron, and other vitamins, such as folate and vitamin B6. In the food service sector, frozen French fries and other frozen potato products are one of the most sought after food items in quick-service restaurants (QSRs), such as McDonald's and Burger King, to serve fast food quickly to their customers. Hence, the availability of premium-category frozen variants with different storage types (freezing temperatures), sizes, and preparation methods from vendors is likely to drive the growth of this segment, which in turn will drive the market growth of frozen French fries in the region during the forecast period.

Company Overview

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

- Key Offering - AJC International Inc: The company offers french fries through its subsidiaries Del Campo, Garden Maid, Early Dawn.

- Key Offering - Cavendish Farms Corp: The company offers french fries such as Crispy Classic Straight Cut, Crispy Spicy Cracked Pepper Straight Cut, and Crispy Sweet Potato Straight Cut.

- Key Offering - Conagra Brands Inc: The company offers french fries under the brand Alexia Foods such as Organic sweet potato fries, Organic Yukon Select Fries, Organic Oven Crinkles With Sea Salt.

The market report also includes detailed analyses of the competitive landscape of the market and information about 15 market companies, including:

- Agristo NV

- AJC International Inc.

- Allied Potato

- B and G Foods Inc.

- Cavendish Farms Corp.

- Conagra Brands Inc.

- Cooperatie Koninklijke Cosun UA

- General Mills Inc.

- Himalaya Food International Ltd.

- Hormel Foods Corp.

- Inspire Brands Inc.

- J.R. Simplot Co.

- Lamb Weston Holdings Inc.

- McCain Foods Ltd.

- Red Robin Gourmet Burgers Inc.

- The Kraft Heinz Co.

- Trader Joes

- Walmart Inc.

- WH Group Ltd.

- Kroger Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Segment Overview

The market provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD Billion" for the period 2024 to 2028, as well as historical data from 2018 to 2022 for the following segments

- Product Outlook

- Frozen

- Food

- End-user Outlook

- Foodservice

- Retail

You may also interested in below market reports:

Frozen Potato Fries Market Research Report by Product, Application, and Geography - Forecast and Analysis

Processed Potatoes Market Analysis North America, Europe, APAC, South America, Middle East and Africa - US, UK, Japan, Germany, Canada - Size and Forecast

Potato Market Analysis APAC, Europe, North America, Middle East and Africa, South America - US, China, India, France, Germany - Size and Forecast

Market Analyst Overview

In the North American market, fast food chains and casual dining establishments continue to serve up popular staple side dishes, with seasoned fries being a top choice. French fries, available in various forms such as curly fries, are a significant convenience food and extend the shelf life of frozen snacks and meals in smaller and single-person households. The frozen food products sector, encompassing frozen ready-to-eat products, offers diverse flavors to cater to evolving consumer preferences. Health-conscious consumers seek low carbohydrate alternatives, leading to the rise of air-fried fries. Condiments, sauces, and dips are essential accompaniments, adding to the overall dining experience. With the increasing popularity of online shopping and home delivery services, consumers can easily access their favorite fast food outlets from the comfort of their homes. However, it is essential to consider the potential health impact of frequent consumption of fast food and convenience items.

In today's quick service restaurants, staple side dishes like regular French fries are evolving with health-conscious trends. Consumers are increasingly opting for baked or air-fried options over traditional conventional methods. Choices now include baked fries, crinkle-cut fries, and steak fries, catering to diverse tastes and snacking habits. With a growing demand for gluten-free, low-carb, and whole-grain alternatives, many establishments are adopting standardized cooking methods to ensure extended shelf-life and consistency across multiple locations. Home delivery service and online orders are boosting on-the-go consumption, while fast food vans meet the needs of millennials seeking convenient, organic diet products. Addressing health issues remains a priority, with options like fresh cut variety being a popular choice for dine-in and takeout.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

141 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.48% |

|

Market growth 2024-2028 |

USD 2.09 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.9 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Agristo NV, AJC International Inc., Allied Potato, B and G Foods Inc., Cavendish Farms Corp., Conagra Brands Inc., Cooperatie Koninklijke Cosun UA, General Mills Inc., Himalaya Food International Ltd., Hormel Foods Corp., Inspire Brands Inc., J.R. Simplot Co., Kroger Co., Lamb Weston Holdings Inc., McCain Foods Ltd., Red Robin Gourmet Burgers Inc., The Kraft Heinz Co., Trader Joes, Walmart Inc., and WH Group Ltd. |

|

Market dynamics |

Parent market analysis, Market forecasting, Market report, Market forecast, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, Market growth and Forecasting, COVID 19 impact and recovery analysis and future consumer dynamics, Market condition analysis for forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

BUY NOW Full Report and Discover more

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the growth of the market between 2024 and 2028

- Precise estimation of the size of the market size and its contribution of the market in focus to the parent market

- Accurate predictions about market research and growth, upcoming trends and changes in consumer behavior

- Market growth analysis across North America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of the market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -