Nuclear Powered Naval Vessels Market Size 2024-2028

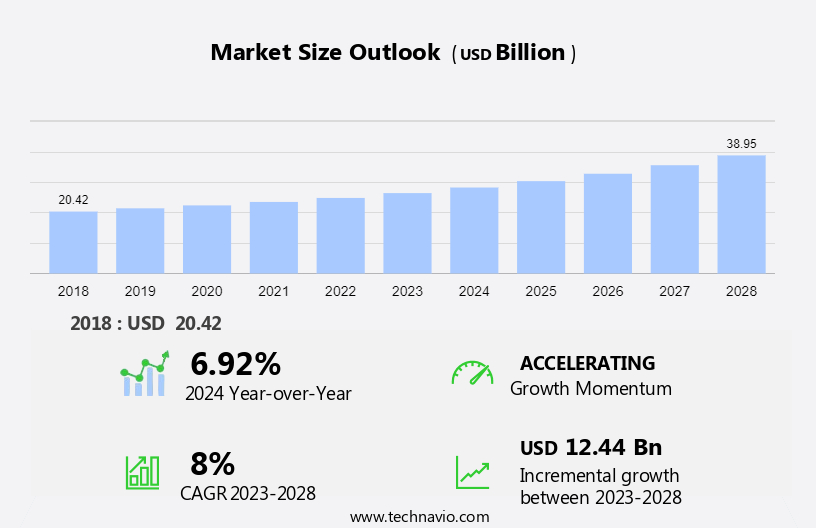

The nuclear powered naval vessels market size is forecast to increase by USD 12.44 billion at a CAGR of 8% between 2023 and 2028. The growth analysis of the market hinges on various factors, including the cost-effectiveness of nuclear power, the escalation in military spending, and efforts to enhance the stealth capabilities of submarines. These factors underscore the strategic investments and advancements in defense technologies aimed at achieving undetectability in naval operations. The cost-effectiveness of nuclear power plays a crucial role in shaping budget allocations and long-term defense strategies, influencing decisions on submarine capabilities and fleet modernization. As geopolitical tensions evolve, there is a heightened emphasis on enhancing submarine stealth to maintain tactical superiority and ensure national security. The synergy between these factors drives innovation and investment in submarine technologies, defining the competitive landscape and future prospects in naval defense markets worldwide.

Market Overview

Market Forecast 2024-2028

To learn more about this report, Request Free Sample

Market Dynamics

The market is pivotal in modern defense strategies, driven by advancements in warships equipped with anti-submarine capabilities and sophisticated armament systems like rocket launchers and vertical missile launchers. These vessels play critical roles in surveillance and operations in strategic regions such as the Black Sea amidst geopolitical tensions and sanctions. Mainstay vessels include main battle warships and large destroyers, bolstering naval capabilities for both offensive and defensive maneuvers. The deployment of amphibious assault ships underscores flexibility in military operations, ensuring readiness for diverse mission scenarios. As nations like Ukraine enhance their naval defenses, the demand for nuclear-powered vessels rises, emphasizing their role in maintaining maritime superiority and safeguarding national interests in challenging environments. Our researchers studied the market research and growth data for years, with 2023 as the base year and 2024 as the estimated year, and presented the key drivers, trends, and challenges for the market.

Key Driver- Rising military spending

The geopolitical tensions between countries have contributed to a significant increase in military spending worldwide, which is also a significant driver for defense equipment manufacturers. In 2023, the military expenditure of countries such as India, China, France, Saudi Arabia, and the US accounted for a major part of the overall defense market. These countries are modernizing their sea-based defense systems and militaries, which has propelled the demand for defense products.

For instance, in 2023, military spending in the US was announced to be USD 816.7 billion. In the fiscal year 2023-2024, the military budget allocated by the Government of India was around USD 50 billion, which is 13% of the entire budget. Thus, the increase in defense and military spending is likely to augment the deployment of nuclear-powered naval vessels, thus driving the growth of the market during the forecast period.

Significant Trends- Indigenous development of nuclear-powered naval vessels

The development of a nuclear-powered naval vessel requires an efficient in-house technical team supported by exclusive technologies and domain expertise, along with large funding. Nowadays, the military equipment procurement pattern has evolved, and countries are now indigenously manufacturing nuclear-powered naval vessels. For instance, India's first nuclear-powered ballistic missile submarine, Arihant class, INS Arihant (S73), was built indigenously by the Indian Navy's Ship Building Centre in the port city of Visakhapatnam, India. INS Vindhyagiri, after its successful sea trials in February 2016, was confirmed and was commissioned in August 2023.

Furthermore, India domestically built its second nuclear-powered ballistic missile submarine, INS Aridhaman, at a fully enclosed dry dock at Vishakhapatnam. INS Aridhaman has one seven-blade propeller powered by a pressurized water reactor (PWR) and a maximum speed of 12-15 knots when on the surface and 24 knots when submerged. Such factors will boost the growth of the market during the forecast period.

Major Challenge- High cost and incorporation of AIP systems

The initial cost of construction of a nuclear-based propulsion system is twice the cost of other kinds of energy propulsion systems. Furthermore, the reactor requires specialist personnel to maintain and operate the nuclear plant, turbine, and generators, while diesel-electric generators and turbines require just a good motor mechanic. Additionally, air-independent propulsion (AIP) is a marine propulsion technology that allows non-nuclear submarines to operate without accessing atmospheric air/oxygen (by surfacing or using a snorkel). AIP can augment or replace both the diesel-electric propulsion system and the nuclear-powered naval vessels.

Moreover, the introduction of AIP has largely improved the underwater endurance of these submarines and has given them a distinct advantage. One of the main advantages of AIP technology is that it can be installed on existing generation submarines by inserting a new hull section during a retrofit. Therefore, navies across the globe are seen queuing up to buy or build submarines with AIP systems. Thus, such factors will impede market growth during the forecast period.

Market Segmentation by Product, Application, and Geography

Product Segment Analysis:

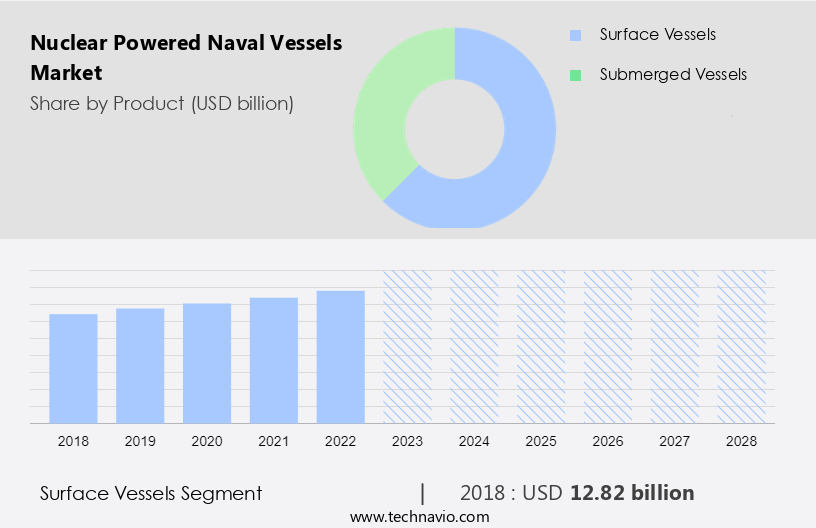

The surface vessels segment will account for a major share of the market's growth during the forecast period.?The surface vessels segment includes a variety of surface-based products, such as aircraft carriers, surface-based cruisers, surface-based destroyers, surface-based frigates, and more. Each surface vessel fulfills a unique purpose and reflects the changing strategic priorities and capacities of naval forces around the world. One of the main categories of surface vessels powered by nuclear is aircraft carriers, often referred to as the flagship of the naval fleet. These gigantic aircraft carriers act as mobile bases of operations, projecting power and power across vast sea areas.

Customised Report as per your requirements!

The surface vessels segment was valued at USD 12.82 billion in 2018. With the use of nuclear power, surface vessels can operate for extended periods of time without refueling, allowing for long-term and long-lasting deployments. For instance, aircraft carriers are powerful power projection platforms and mobile airbases that can carry and launch a wide variety of aircraft. Examples include the United States Navy's Gerald R. Ford class carrier and the Royal Navy's Queen Elizabeth-class carrier. These factors under the surface vessels segment will drive the growth of the market during the forecast period.

Application?Segment Analysis:

Based on application, the market has been segmented into defense and transportation. The defense segment will account for the largest share of this segment.?Nuclear-powered naval vessels are used for a variety of defense applications. There are several different types of vessels in the market, such as aircraft carriers, nuclear-powered submarines, and surface combatants. Aircraft carriers are an essential part of naval defense because they can project power over vast distances. In addition, the defense segment is also characterized by constant technological innovation. The development of reactor designs, propulsion systems, and stealth technologies has enabled the development of more advanced and efficient vessels. Thus, such factors under the defense segment will drive the growth of the market during the forecast period.

Regional Analysis

For more insights on the market share of various regions Download Sample PDF now!

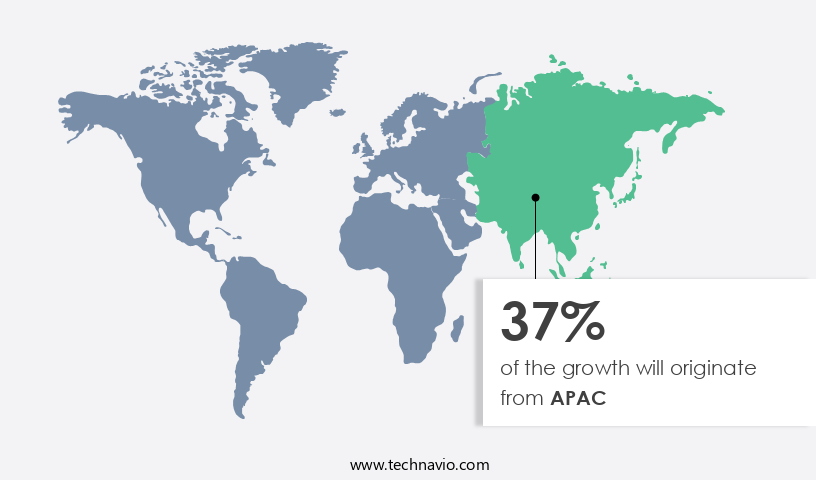

APAC is estimated to contribute 37% to the growth by 2028. Technavio's analysts have provided extensive insight into the market forecasting, detailing the regional trends and drivers influencing the market's trajectory throughout the forecast period. Another region offering significant growth opportunities to companies is North America. The high defense budget of the US is approximately 3.1% of the total country's budget in 2023 and makes it the leading region in the global market. The increasing spending from the defense department on the construction of nuclear-powered naval ships is likely to drive the growth of the market in the region. There are only three major naval forces (The US Navy, Royal Canadian Navy, and Mexican Navy) in North America, however, the US Nuclear Navy is one of the oldest and largest nuclear organizations in the world, Furthermore, the two primary reasons contributing to the adoption of nuclear-powered propulsion are the cost-benefit derived from the system and the time involved in replacing the core. Hence, such factors are expected to drive market growth in this region during the forecast period.

Who are the Major Market Companies?

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

- Austal Ltd.: The company offers nuclear-powered naval vessel components for US Navy Virginia class and Columbia class nuclear-powered submarine fleets.

We also have detailed analyses of the market’s competitive landscape and offer information on 20 market companies, including Babcock International Group Plc, BAE Systems Plc, Bechtel Corp., BWX Technologies Inc., Curtiss Wright Corp., General Dynamics Corp., Huntington Ingalls Industries Inc., Kongsberg Gruppen ASA, Lockheed Martin Corp., Naval Group, Northrop Grumman Corp., Rolls Royce Holdings Plc, and Thales Group

Technavio market forecast the an in-depth analysis of the market and its players through combined qualitative and quantitative data. The analysis classifies companies into categories based on their business approaches, including pure-play, category-focused, industry-focused, and diversified. Companies are specially categorized into dominant, leading, strong, tentative, and weak, based on their quantitative data analysis.

Segment Overview

The market research report provides comprehensive data (region wise segment analysis), with forecasts and estimates in "USD Billion" for the period 2024 to 2028, as well as historical data from 2018 to 2022 for the following segments.

- Product Outlook

- Surface vessels

- Submerged vessels

- Application Outlook

- Defense

- Transportation

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- The U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- South America

- Chile

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- North America

You may also interested in below market reports:

- Naval Vessels Maintenance, Repair, and Overhaul (MRO) Market - Naval Vessels Maintenance, Repair, and Overhaul (MRO) Market Analysis North America, APAC, Europe, South America, Middle East and Africa - US, China, India, Russia, UK - Size and Forecast

- Submarine Market - Submarine Market Analysis North America, APAC, Europe, Middle East and Africa, South America - US, China, Russia, Japan, South Korea - Size and Forecast

- Fuel Cells for Marine Vessels Market - Fuel Cells for Marine Vessels Market Analysis North America, APAC, Europe, Middle East and Africa, South America - US, China, Japan, Germany, UK - Size and Forecast

Market Analyst Overview

The market is at the forefront of global defense strategies, encompassing large destroyers and amphibious assault ships designed for complex missions in regions like the Black Sea. As Western countries and the international community emphasize security, the defense industry and shipbuilding sectors innovate with advanced technologies including 3D printers for metal pipes, cylinders, and plates of varied shapes. These vessels feature integrated electric propulsion and may explore renewable energy sources like solar and wind power. Cutting-edge materials such as buckypaper enhance durability, while robotics revolutionize combat management and search and rescue operations. The market faces challenges such as high development costs but remains crucial with robust weapon launch, sensor, and communication systems for effective combat operations and maritime missions worldwide.

In addition, the market is pivotal in global defense, featuring large destroyers and amphibious assault ships crucial for operations in strategic areas like the Black Sea. These vessels utilize advanced metal plates tailored for curved & hilly shapes, enhancing durability and maneuverability. Innovations such as solar and wind-powered ships and materials like buckypaper address sustainability and resilience challenges despite high development costs. They integrate sophisticated sensor, weapon launch, and combat management systems to ensure operational readiness. The market also caters to diverse needs with corvettes, amphibious ships, and auxiliary vessels, offering flexibility in missions. With a focus on replacement parts and retrofit solutions for marine engine, control, and electrical systems, nuclear-powered vessels maintain their relevance in modern naval fleets, aligning with stringent defense requirements worldwide.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

168 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8% |

|

Market Growth 2024-2028 |

USD 12.44 billion |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

6.92 |

|

Regional analysis |

North America, APAC, Europe, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 37% |

|

Key countries |

US, China, India, Russia, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Austal Ltd., Babcock International Group Plc, BAE Systems Plc, Bechtel Corp., BWX Technologies Inc., Curtiss Wright Corp., General Dynamics Corp., Huntington Ingalls Industries Inc., Kongsberg Gruppen ASA, Lockheed Martin Corp., Naval Group, Northrop Grumman Corp., Rolls Royce Holdings Plc, and Thales Group |

|

Market dynamics |

Parent market growth analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and Market condition analysis for the forecast period. |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the growth of the market between 2024 and 2028

- Precise estimation of the market growth and trends and its contribution to the market in focus on the parent market

- Accurate predictions about upcoming market trends and analysis and changes in consumer behavior

- Market growth and forecasting across North America, APAC, Europe, Middle East and Africa, and South America

- A thorough market analysis and report of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -