Ophthalmic Handheld Surgical Instruments Market Size 2024-2028

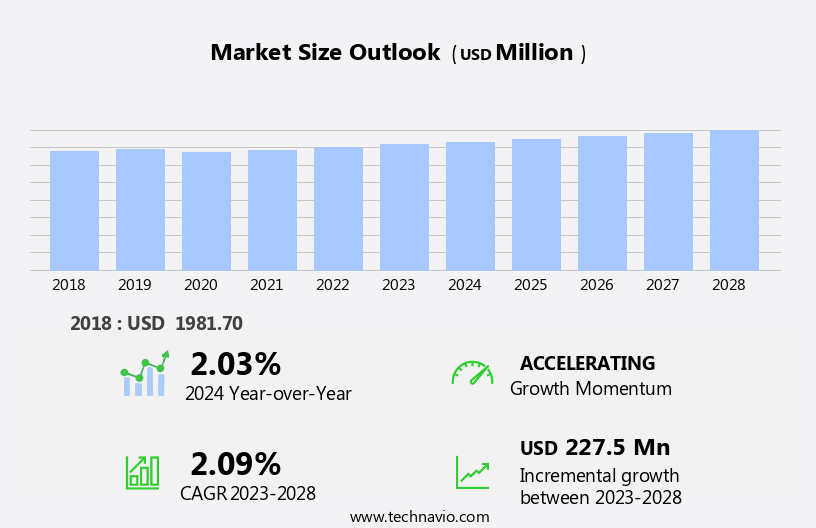

The ophthalmic handheld surgical instruments market size is forecast to increase by USD 227.5 billion at a CAGR of 2.09% between 2023 and 2028.

- The market is experiencing significant growth due to several key factors. The increasing prevalence of ophthalmic diseases, such as cataracts, glaucoma, and age-related macular degeneration, is driving market demand. Additionally, the rise of medical tourism for affordable ophthalmology surgeries in developing countries is expanding the market's reach. However, the shortage of skilled ophthalmologists poses a challenge to market growth, as the demand for these specialists continues to outpace supply. Overall, the market is expected to witness steady expansion In the coming years, with innovations in handheld surgical instruments and increasing awareness of eye health contributing to its growth trajectory.

What will be the Size of the Ophthalmic Handheld Surgical Instruments Market During the Forecast Period?

- The market In the US is experiencing significant growth due to the increasing prevalence of ocular conditions such as glaucoma, cataracts, refractive errors, and diabetic retinopathy. According to industry analysis, the market is driven by the rising number of ambulatory surgery centers and the growing preference for minimally invasive surgeries. The older population, which is more susceptible to visual impairments and blindness, also contributes to market expansion. Patient care and elective surgeries are key areas of focus, with a demand for instruments that ensure precise incisions and quick recovery periods. Ophthalmic knives, including disposable and diamond knives, are popular choices for surgeons due to their ability to provide the best correction for poor visions.

- Public awareness campaigns and routine healthcare services are further fueling the market, with a particular emphasis on reducing turnaround times for surgeries and improving visual acuity for patients with legal blindness.

How is this Ophthalmic Handheld Surgical Instruments Industry segmented and which is the largest segment?

The ophthalmic handheld surgical instruments industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2017-2022 for the following segments.

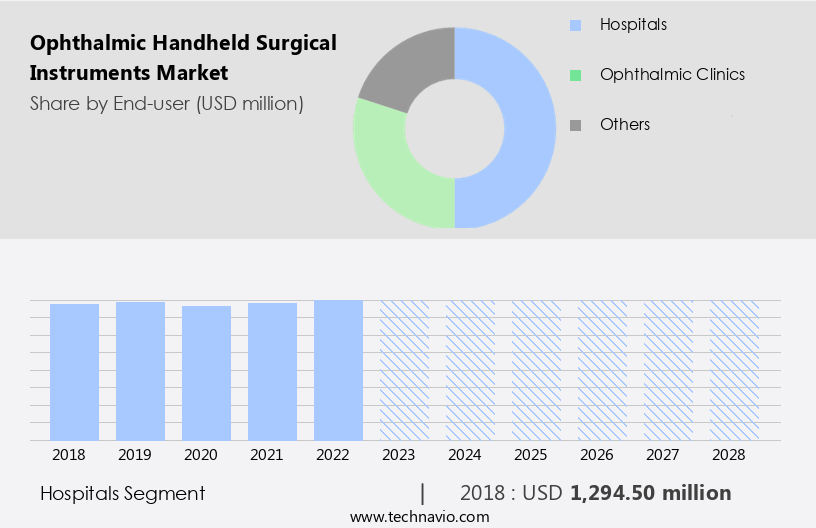

- End-user

- Hospitals

- Ophthalmic clinics

- Others

- Product

- Ophthalmic knives

- Forceps

- Scissors and others

- Geography

- North America

- Canada

- US

- Europe

- Germany

- UK

- Asia

- China

- Rest of World (ROW)

- North America

By End-user Insights

- The hospitals segment is estimated to witness significant growth during the forecast period.

The market experienced significant growth in 2023, with hospitals being a major end-user. Hospitals utilize Ophthalmic Handheld Surgical Instruments (OHSI) for various ophthalmic procedures, including cataracts, glaucoma, and corneal surgeries. The presence of specialized ophthalmology departments in hospitals, equipped with advanced surgical tools, enables them to offer comprehensive eye care services. The aging population and the increasing prevalence of ocular disorders have fueled the demand for OHSI in hospitals. Additionally, the availability of minimally invasive surgical methods and technological advancements have further boosted the adoption of these instruments. As a result, the market for OHSI is anticipated to expand further during the forecast period.

Get a glance at the Ophthalmic Handheld Surgical Instruments Industry report of share of various segments Request Free Sample

The Hospitals segment was valued at USD 0.00 billion in 2017 and showed a gradual increase during the forecast period.

Regional Analysis

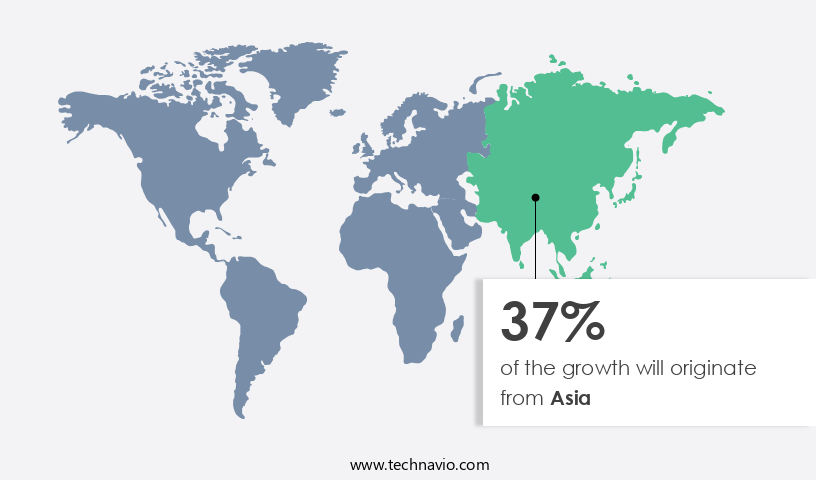

- Asia is estimated to contribute 37% to the growth of the global market during the forecast period.

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The North American market for ophthalmic handheld surgical instruments experiences significant growth due to increasing healthcare expenditure on ocular diseases and the approval of new handheld ophthalmology surgical devices. Prevalent eye conditions such as cataracts, glaucoma, diabetic retinopathy, AMD, and refractive errors, coupled with an aging population, contribute to the market expansion. In the US and Canada, the high volume of ophthalmology surgeries further bolsters the regional market growth. These factors collectively drive the market in North America during the forecast period.

Market Dynamics

Our ophthalmic handheld surgical instruments market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Ophthalmic Handheld Surgical Instruments Industry?

Increasing prevalence of ophthalmic diseases is the key driver of the market.

- The market In the US is witnessing significant growth due to the increasing prevalence of various ocular conditions, such as refractive errors, cataracts, glaucoma, and diabetic retinopathy. According to the World Health Organization (WHO), approximately 2.2 billion people worldwide have a vision impairment or blindness, with uncorrected refractive errors and cataracts being the leading causes. The older population is particularly at risk, as aging increases the likelihood of developing these conditions. Globally, an estimated 400 out of every 1,000 people and 50 out of every 1,000 people will develop cataracts and glaucoma, respectively, during their lifetime. Ophthalmic clinics and ambulatory surgery centers are increasingly offering elective surgeries to address these conditions, driven by patient preferences for improved visual acuity and reduced recovery periods.

- Ophthalmic handheld surgical instruments, including ophthalmic knives (such as disposable and diamond knives), scissors (including conjunctival, corneal, IOL, iris, stitch, tenotomy, and Vannas scissors), and forceps (made of materials like titanium and stainless steel), play a crucial role In these surgeries. These instruments enable precise incisions and facilitate the successful completion of procedures. The market for these instruments is further driven by the increasing availability of cutting-edge surgical devices, research centers, academics, and mobile ophthalmic units. Public awareness campaigns and the integration of ophthalmic services into routine healthcare services have also contributed to the market's growth. The focus on patient care and reducing turnaround times further underscores the importance of these instruments In the healthcare industry.

What are the market trends shaping the Ophthalmic Handheld Surgical Instruments Industry?

Increasing medical tourism for low-cost ophthalmology surgeries is the upcoming market trend.

- The market caters to the growing demand for advanced surgical devices to address various ocular conditions, including glaucoma, cataracts, and refractive errors. Ambulatory surgery centers and ophthalmic clinics are major segments driving market growth due to patient preferences for convenient and efficient care. Ophthalmic services, such as cataract surgery, are increasingly utilizing cutting-edge surgical devices, like precision ophthalmic knives (diamond and disposable), scissors (conjunctival, corneal, IOL, iris, stitch, tenotomy, Vannas, and strabismus), and forceps (titanium and stainless steel). Visual impairments and blindness, particularly among the older population and those with diabetic retinopathy, are significant drivers for elective surgeries. The market benefits from patient care priorities, research centers, academics, and mobile ophthalmic units.

- Short recovery periods and turnaround times, public awareness, and routine healthcare services further fuel market growth. Market dynamics are influenced by patient preferences for the best correction and poor visions, as well as the increasing incidence of ocular conditions. The industry's focus on innovation and minimally invasive procedures continues to shape the market landscape.

What challenges does the Ophthalmic Handheld Surgical Instruments Industry face during its growth?

Shortage of skilled ophthalmologists is a key challenge affecting the industry growth.

- The market is witnessing significant growth due to the increasing prevalence of ocular conditions such as glaucoma, cataracts, and refractive errors. According to the National Eye Institute, over 2.5 million Americans have diabetic retinopathy, a leading cause of blindness in working-age adults. Ambulatory surgery centers and ophthalmic clinics are increasingly adopting advanced surgical devices for elective surgeries, including MicroSurgical Technology's diamond knives for precision incisions and disposable knives for improved patient safety. Patient preferences for minimally invasive procedures and shorter recovery periods are driving the demand for cutting-edge surgical devices. The older population, which is more susceptible to visual impairments and blindness, is a significant market segment.

- The market faces challenges such as insufficient human resources, long turnaround times, and poor coordination between hospitals and ophthalmologists. Ophthalmic services, including routine healthcare services and research centers, are investing In the latest technologies to improve patient care. The use of titanium and stainless steel instruments in surgeries, such as conjunctival scissors, corneal scissors, and IOL scissors, ensures the best correction for poor visions. The market is expected to grow further due to increasing public awareness and the availability of mobile ophthalmic units for patient convenience. In conclusion, the market is evolving to meet the growing demand for advanced surgical procedures.

- The market dynamics include the increasing prevalence of ocular conditions, patient preferences, and the availability of new technologies. However, challenges such as insufficient human resources and poor coordination between hospitals and ophthalmologists remain. The market is expected to continue growing due to the increasing demand for minimally invasive procedures and the availability of mobile ophthalmic units.

Exclusive Customer Landscape

The ophthalmic handheld surgical instruments market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ophthalmic handheld surgical instruments market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, ophthalmic handheld surgical instruments market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

AddVision - Vision Pharmaceuticals Ltd., a subsidiary of our company, provides a range of ophthalmic handheld surgical instruments for the US market. These instruments include the advanced dual lumen cannulas, which are essential tools for ophthalmic surgeries. Our commitment to innovation and quality ensures that these instruments meet the highest standards for precision and safety. By offering these instruments, we aim to support ophthalmic surgeons in delivering optimal patient outcomes.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AddVision

- Appasamy Associates Pvt. Ltd.

- Aspen Surgical Products Inc.

- Bausch Health Companies Inc.

- BVI Holdings Ltd.

- Carl Zeiss Stiftung

- Corza Medical

- Devine Meditech

- Duckworth and Kent Ltd.

- Halma Plc

- INKA

- Iscon Surgicals Ltd.

- Lombart Instrument Inc.

- Mani Inc.

- Metall Zug AG

- Millennium Surgical Corp.

- P.W. Coole and Son Ltd.

- Pelion Surgical

- Precipart

- Prkamya Visions

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Ophthalmic Handheld Surgical Instruments: Market Dynamics and Trends the market is witnessing significant growth due to the increasing prevalence of various ocular conditions that necessitate surgical interventions. These instruments play a crucial role in performing precise and efficient surgeries, contributing to improved patient outcomes and reduced recovery periods. Ophthalmic handheld surgical instruments are essential tools In the healthcare industry, catering to a wide range of surgical procedures. These instruments include ophthalmic knives, scissors, and forceps, designed to ensure optimal precision and accuracy during surgeries. Ophthalmic knives, available in various materials like stainless steel and titanium, are used for making incisions during surgeries.

Disposable knives and diamond knives are popular choices due to their sterility and ability to provide precise incisions. The demand for these instruments is driven by the growing number of surgeries performed for conditions such as glaucoma, cataracts, and diabetic retinopathy. Scissors are another essential category of ophthalmic handheld surgical instruments. Conjunctival scissors, corneal scissors, general ophthalmic scissors, iol scissors, iris scissors, stitch scissors, tenotomy scissors, and Vannas scissors are some of the commonly used types. These scissors are designed to cater to the unique requirements of various ophthalmic surgeries, ensuring minimal damage to surrounding tissues and optimal surgical outcomes.

The use of microsurgical technology In the production of these instruments has revolutionized ophthalmic surgeries. This technology allows for smaller incisions, reduced trauma, and faster recovery times. Research centers and academics are continually exploring new ways to improve the design and functionality of these instruments to cater to the evolving needs of the healthcare industry. The ophthalmic services segment, including ambulatory surgery centers and ophthalmic clinics, is a significant consumer of ophthalmic handheld surgical instruments. The increasing popularity of elective surgeries and routine healthcare services has led to a surge in demand for these instruments. Patient preferences for minimally invasive procedures and shorter turnaround times further fuel the market growth.

Public awareness about visual impairments and blindness has also contributed to the growth of the market. Early detection and timely intervention for various ocular conditions have become a priority, leading to an increase In the number of surgeries performed. The older population is another significant demographic driving market growth. Age-related ocular conditions such as cataracts, glaucoma, and diabetic retinopathy are common among the elderly, necessitating the use of advanced ophthalmic handheld surgical instruments for accurate and efficient surgeries. In conclusion, the market is poised for continued growth due to the increasing prevalence of various ocular conditions, the aging population, and the advancements in microsurgical technology.

These instruments play a crucial role in ensuring optimal surgical outcomes, reduced recovery periods, and improved patient care.

|

Ophthalmic Handheld Surgical Instruments Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

154 |

|

Base year |

2023 |

|

Historic period |

2017-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 2.09% |

|

Market growth 2024-2028 |

USD 227.5 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

2.03 |

|

Key countries |

US, China, Germany, Canada, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Ophthalmic Handheld Surgical Instruments Market Research and Growth Report?

- CAGR of the Ophthalmic Handheld Surgical Instruments industry during the forecast period

- Detailed information on factors that will drive the Ophthalmic Handheld Surgical Instruments growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the ophthalmic handheld surgical instruments market growth of industry companies

We can help! Our analysts can customize this ophthalmic handheld surgical instruments market research report to meet your requirements.

RIA -

RIA -