Europe Optometry Software Market Size 2026-2030

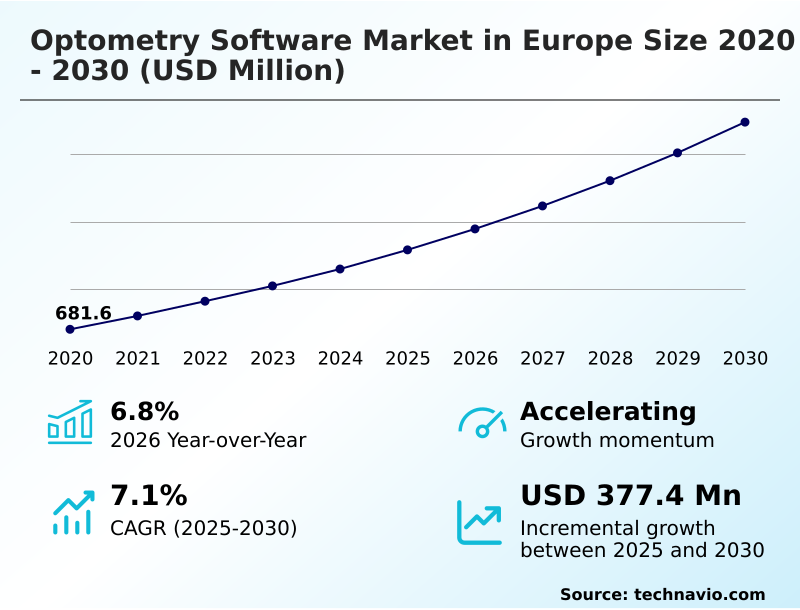

The europe optometry software market size is valued to increase by USD 377.4 million, at a CAGR of 7.1% from 2025 to 2030. Integration of AI and cloud-based diagnostic ecosystems will drive the europe optometry software market.

Major Market Trends & Insights

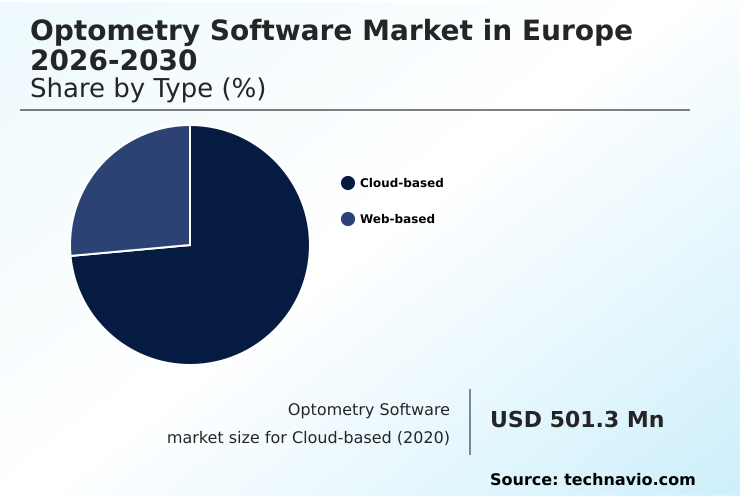

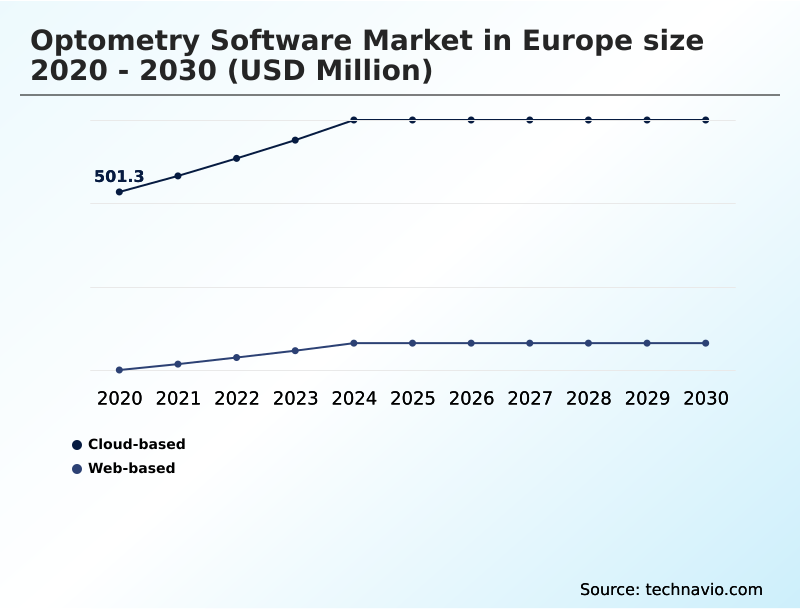

- By Type - Cloud-based segment was valued at USD 631 million in 2024

- By End-user - Hospitals segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 612.1 million

- Market Future Opportunities: USD 377.4 million

- CAGR from 2025 to 2030 : 7.1%

Market Summary

- The optometry software market in Europe is evolving from standalone administrative tools to integrated ecosystems that merge clinical diagnostics with retail operations. This transition is fueled by the need for enhanced operational efficiency and improved patient outcomes in the face of an aging population with a higher prevalence of ocular diseases.

- A key trend is the accelerated adoption of cloud-based platforms and AI-powered diagnostic support, which enable earlier detection of conditions like glaucoma and diabetic retinopathy.

- For instance, a multi-location practice can deploy a unified system where an AI algorithm flags a high-risk retinal scan from a remote clinic, automatically updating the patient's electronic health record and scheduling a tele-consultation with a specialist. Simultaneously, the platform manages optical inventory and point-of-sale transactions, creating a seamless patient journey.

- However, the market faces challenges related to data interoperability between disparate systems and ensuring strict compliance with GDPR for patient data privacy. The drive toward standardized, secure, and intelligent software solutions remains central to modernizing eye care delivery across the continent and is a key factor in the optometry software market in Europe.

What will be the Size of the Europe Optometry Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Europe Optometry Software Market Segmented?

The europe optometry software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Cloud-based

- Web-based

- End-user

- Hospitals

- Nursing homes

- Others

- Application

- Patient records

- Billing and scheduling

- Optical inventory management

- E-prescribing

- Others

- Geography

- Europe

- Germany

- UK

- France

- Europe

By Type Insights

The cloud-based segment is estimated to witness significant growth during the forecast period.

The cloud-based segment is defined by its scalability and subscription-based model, offering enterprise-grade technology without significant upfront capital.

This model is driving a shift away from legacy on-premises systems, enabling real-time data synchronization for functions like cloud-based practice management and practice and retail management.

These platforms facilitate seamless clinic workflow automation by integrating diagnostic tools, electronic eyewear measurement, and patient engagement features. Advanced functionalities such as predictive analytics for appointment scheduling, retinal decision support, and digital vision therapy are increasingly standard.

Cloud-native platforms facilitate real-time data synchronization using technologies like radio-frequency identification (rfid), improving inventory accuracy by over 95%. This architecture supports dispensing and lens demonstration alongside vision therapy software, creating a unified ecosystem for modern eye care.

The Cloud-based segment was valued at USD 631 million in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic adoption of specialized software is reshaping European eye care, with solutions tailored to specific operational needs. For instance, cloud-based optometry software for multi-location practices is becoming essential for centralizing data and standardizing workflows. A critical advancement is the use of ai for early glaucoma risk analysis, which integrates directly into clinical routines.

- Ensuring gdpr compliance in eye care software is a non-negotiable factor driving investment in secure platforms. The capability for integrating diagnostic imaging with patient records is now a standard expectation, enhancing longitudinal care. In parallel, tele-optometry platforms for rural areas are expanding access to specialist consultations.

- On the administrative side, automated billing for optometry practices and tools for improving accuracy with automated claim scrubbing are streamlining revenue cycles. The challenge of achieving interoperability between diagnostic hardware and software is being addressed by unified ecosystems. For retail operations, optical inventory management with rfid and point-of-sale execution for optical retail are optimizing stock control and sales processes.

- The implementation of secure e-prescribing for spectacle lenses and clinical decision support for therapeutic agents enhances patient safety. Furthermore, software for managing age-related eye diseases is critical for an aging population. Practices implementing such systems report patient recall compliance rates up to 40% higher than those using manual methods.

- Digital patient portals for appointment management empower patients, while implementing ehr for optometry clinic efficiency optimizes internal processes. Solutions offering ai-guided retinal therapy planning support and tools for reducing patient no-shows with automated reminders are improving clinical outcomes.

- Finally, dedicated practice management for independent optometrists and software supporting hl7 fhir standards are ensuring even smaller clinics can participate in the digital health landscape, while platforms adept at managing complex reimbursement landscapes in software provide crucial financial stability.

What are the key market drivers leading to the rise in the adoption of Europe Optometry Software Industry?

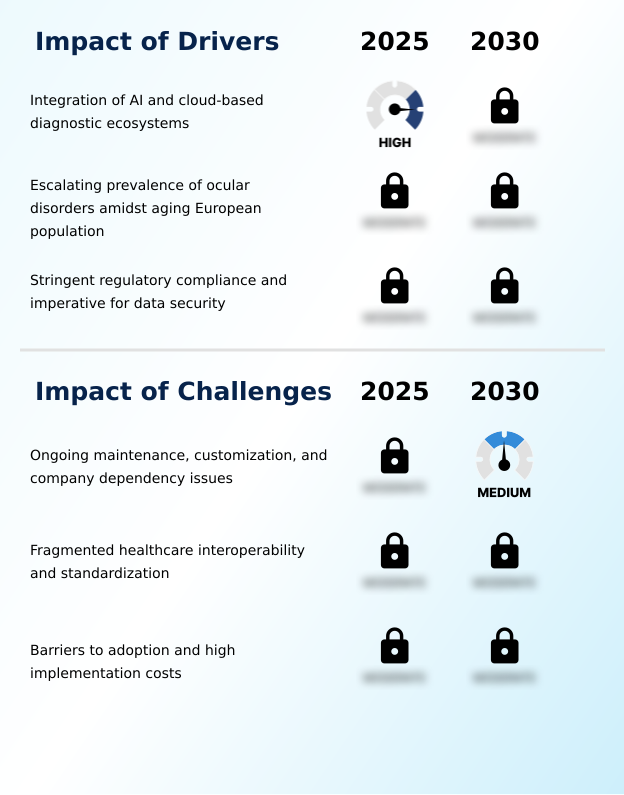

- The integration of AI and cloud-based diagnostic ecosystems is a primary driver for the optometry software market in Europe.

- Market growth is significantly driven by regulatory mandates and new care delivery models.

- The establishment of the European Health Data Space (EHDS) and standards like HL7 FHIR and SNOMED CT compels investment in interoperable, GDPR-compliant digital platforms that ensure patient data privacy and secure data handling.

- This regulatory push supports the expansion of shared-care schemes and community-based triaging services, which rely on software to connect different healthcare providers. The demand for automated recall systems is also rising to manage chronic conditions in an aging population.

- These drivers have led to a 35% increase in follow-up appointment adherence where automated systems are used.

- Furthermore, the need to manage complex billing and reimbursement structures is fueling the adoption of specialized software, particularly for tele-expertise platforms and tele-ophthalmology booths.

What are the market trends shaping the Europe Optometry Software Industry?

- The growth of advanced imaging software is a significant trend, embedding high-resolution scanning and AI-powered analysis into clinical workflows.

- Key market trends are centered on the adoption of cloud-native solutions that enable sophisticated AI-powered diagnostic support and create interoperable device-software ecosystems. The growth in high-resolution retinal scanning and multimodal imaging technologies is driving demand for platforms capable of asynchronous remote monitoring and end-to-end optician management. This allows for earlier ocular pathology detection and better practice workflow integration.

- Tele-optometry platforms are becoming standard, supported by digital patient portals that improve the patient engagement platform. These advanced systems are showing tangible results, with AI-driven screening tools reducing initial diagnostic times by over 25% and integrated patient portals leading to a 40% increase in patient self-scheduling, optimizing clinic resources and improving access to care.

What challenges does the Europe Optometry Software Industry face during its growth?

- Ongoing maintenance, customization requirements, and dependency on software companies present key challenges affecting industry growth.

- Significant challenges persist around system integration and implementation costs. Achieving seamless cross-platform compatibility between legacy systems and modern remote diagnostic software remains a primary hurdle, particularly for vertically integrated business models that combine clinical services with omnichannel retail capabilities. The complexity of integrating e-prescribing systems, clinical decision support systems, and point-of-sale (POS) execution tools requires substantial investment.

- The initial cost of data migration and staff training can constitute up to 30% of the total implementation expense for a new platform. Moreover, a lack of interoperability often leads to workflow inefficiencies, increasing administrative tasks by as much as 20% and hindering efforts to achieve true supply chain transparency and facilitate cross-border healthcare services.

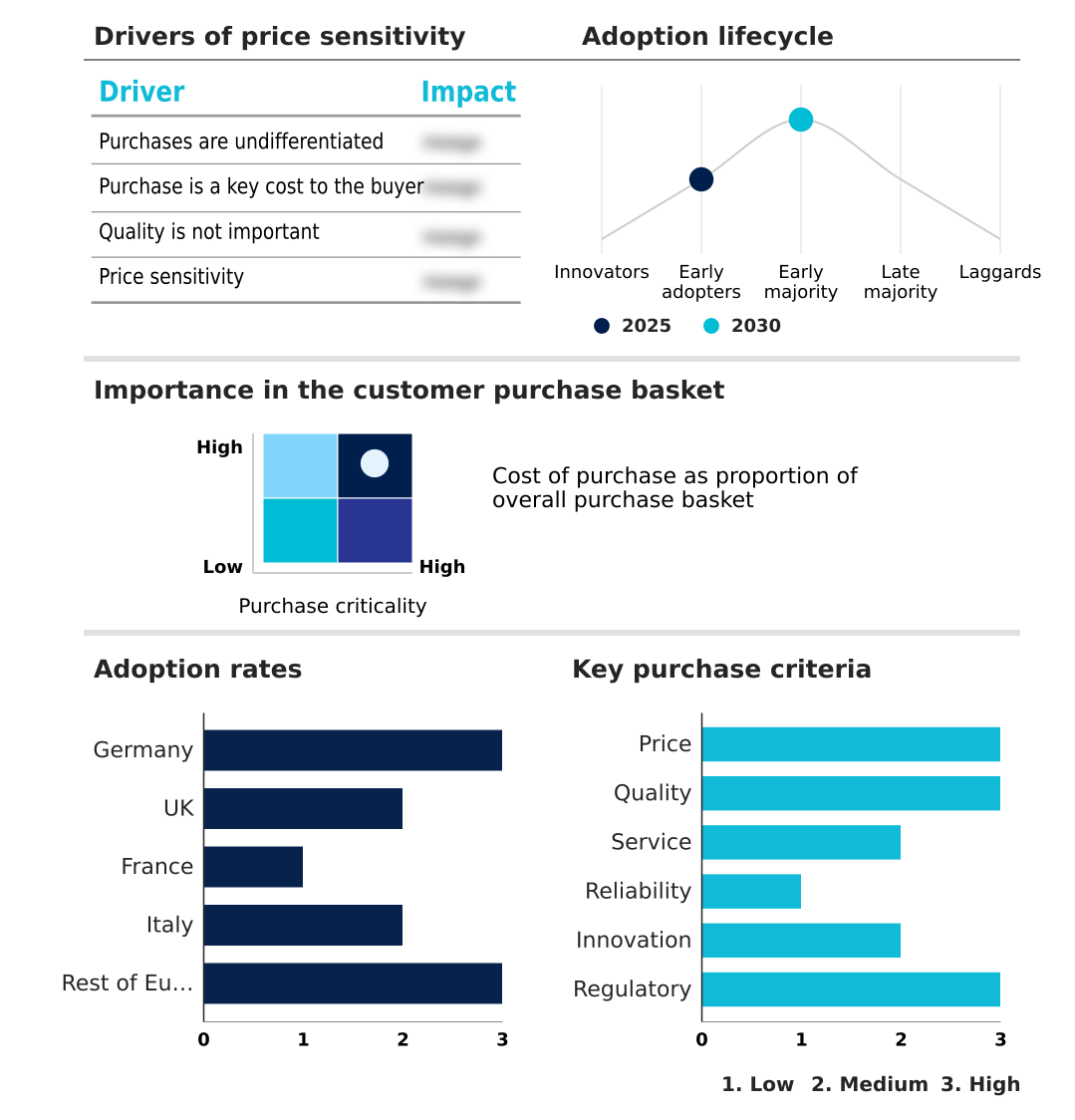

Exclusive Technavio Analysis on Customer Landscape

The europe optometry software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the europe optometry software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Europe Optometry Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, europe optometry software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Altris Inc. - Delivers integrated software for practice management, clinical diagnostics, and optical retail, focusing on AI-driven efficiency and workflow automation.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Altris Inc.

- Blink OMS

- Cosium

- DoctorConnect

- Eyefinity Inc.

- iTRUST.IO LLC

- LitGrey Technologies

- Medesk Ltd.

- Ocuco Ltd.

- Opticabase

- Optikam Tech Inc.

- Optinet Ltd.

- Optix Software Ltd.

- Smart Optometry Ltd.

- Thomson Software Solutions

- Vision Plus PMS Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Europe optometry software market

- In August, 2024, Icare Finland Oy acquired Thirona Retina, an artificial intelligence software company, to strengthen the capabilities of portable screening devices by embedding AI algorithms for detecting retinal disease.

- In October, 2024, EssilorLuxottica completed its acquisition of an 80% majority stake in Heidelberg Engineering, a Germany-based provider of diagnostic solutions and digital surgical technologies for clinical ophthalmology.

- In April, 2025, Ocuco entered into a strategic partnership with Nextech to integrate its omnichannel retail capabilities with Nextech's clinical ophthalmology platform, aiming for an end-to-end eye care solution.

- In May, 2025, Topcon Healthcare announced a strategic partnership with Microsoft to leverage cloud and artificial intelligence technologies, aiming to enhance the efficiency of ocular data management systems.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Europe Optometry Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 208 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.1% |

| Market growth 2026-2030 | USD 377.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.8% |

| Key countries | Germany, UK, France, Italy and Rest of Europe |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is rapidly evolving toward interconnected, intelligent ecosystems where AI-powered OCT analysis and AI-guided retinal therapy are becoming integral to clinical practice. This shift is underpinned by the widespread adoption of cloud-based practice management and integrated EHR and practice management platforms, which unify patient data and clinical workflows.

- Solutions now offer end-to-end optician management, combining high-resolution retinal scanning and multimodal imaging with optical inventory management and electronic eyewear measurement tools. The regulatory landscape, particularly the European Health Data Space (EHDS) and GDPR-compliant digital platforms, mandates adherence to standards like HL7 FHIR and SNOMED CT, driving demand for secure and interoperable systems.

- Advanced features such as automated recall systems, digital vision therapy, and sophisticated clinical workflow automation are no longer niche offerings. As tele-optometry platforms and tele-ophthalmology booths expand, so does the need for robust software. The integration of digital surgical technologies, tele-referto (remote reporting), and portable screening devices is creating a cohesive care continuum.

- Platforms offering asynchronous review are enabling greater efficiency, with some systems demonstrating a 25% reduction in diagnostic interpretation times. This comprehensive digitization extends from community urgent eye care services to specialized needs like Hebergeur de Donnees de Sante (HDS) compliance, transforming both practice efficiency and patient outcomes.

What are the Key Data Covered in this Europe Optometry Software Market Research and Growth Report?

-

What is the expected growth of the Europe Optometry Software Market between 2026 and 2030?

-

USD 377.4 million, at a CAGR of 7.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Cloud-based, and Web-based), End-user (Hospitals, Nursing homes, and Others), Application (Patient records, Billing and scheduling, Optical inventory management, E-prescribing, and Others) and Geography (Europe)

-

-

Which regions are analyzed in the report?

-

Europe

-

-

What are the key growth drivers and market challenges?

-

Integration of AI and cloud-based diagnostic ecosystems, Ongoing maintenance, customization, and company dependency issues

-

-

Who are the major players in the Europe Optometry Software Market?

-

Altris Inc., Blink OMS, Cosium, DoctorConnect, Eyefinity Inc., iTRUST.IO LLC, LitGrey Technologies, Medesk Ltd., Ocuco Ltd., Opticabase, Optikam Tech Inc., Optinet Ltd., Optix Software Ltd., Smart Optometry Ltd., Thomson Software Solutions and Vision Plus PMS Ltd.

-

Market Research Insights

- The market is characterized by a dynamic shift toward comprehensive patient engagement platforms and enhanced clinic workflow automation. This evolution prioritizes the integration of omnichannel retail capabilities with clinical care, supported by robust device-software ecosystems. The adoption of advanced patient communication tools has demonstrated a capacity to reduce appointment no-show rates by up to 30%, directly impacting practice revenue.

- Furthermore, practices leveraging fully integrated platforms for practice workflow integration and optical retail management report an average 15% improvement in diagnostic throughput and staff efficiency.

- This move toward cloud-native solutions is not just about technological upgrades but is a strategic response to demands for more efficient, patient-centric care models that require secure data handling and seamless supply chain transparency across the entire service delivery chain.

We can help! Our analysts can customize this europe optometry software market research report to meet your requirements.

RIA -

RIA -