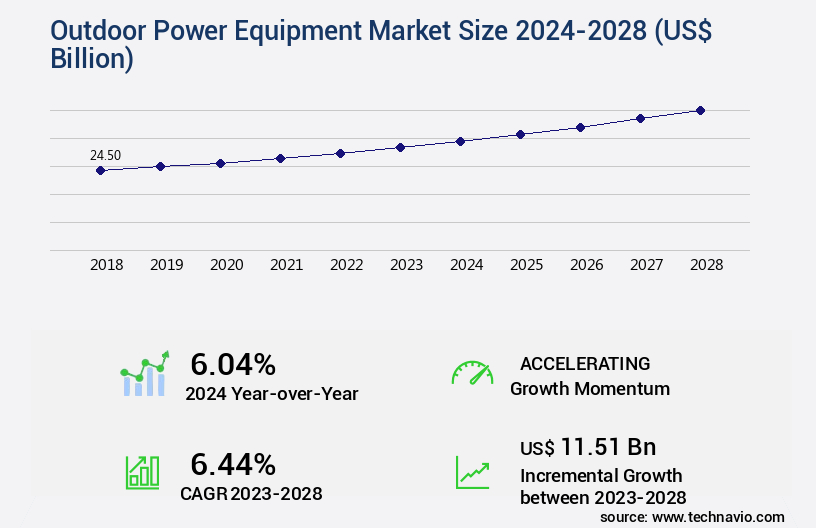

Outdoor Power Equipment Market Size 2024-2028

The outdoor power equipment market size is valued to increase USD 11.51 billion, at a CAGR of 6.44% from 2023 to 2028. Increasing demand for outdoor natural aesthetics will drive the outdoor power equipment market.

Major Market Trends & Insights

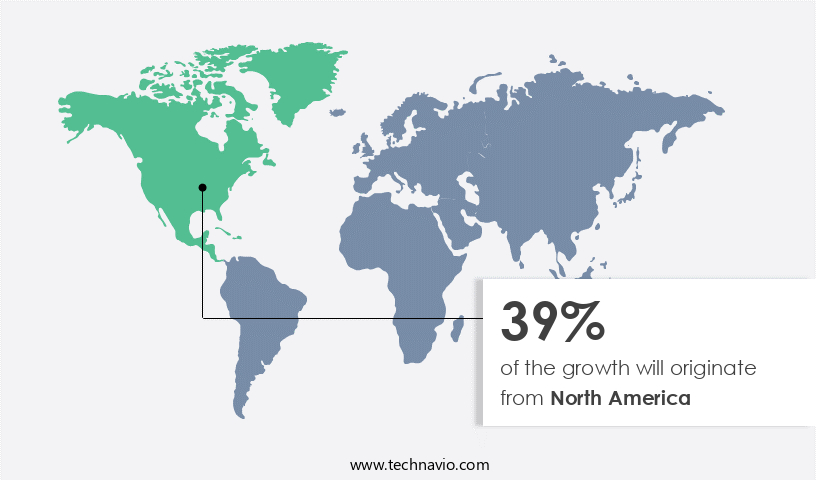

- North America dominated the market and accounted for a 39% growth during the forecast period.

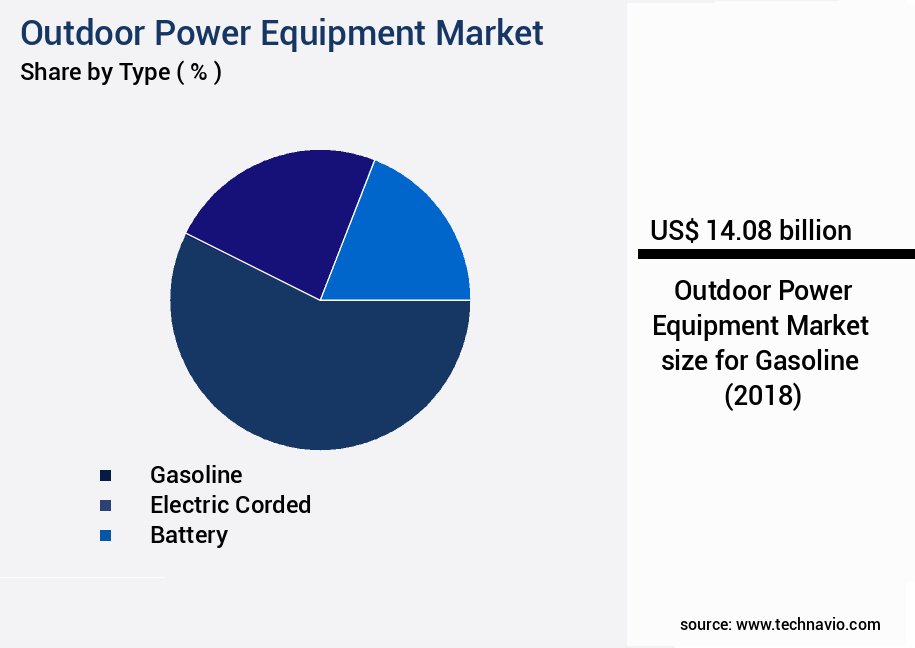

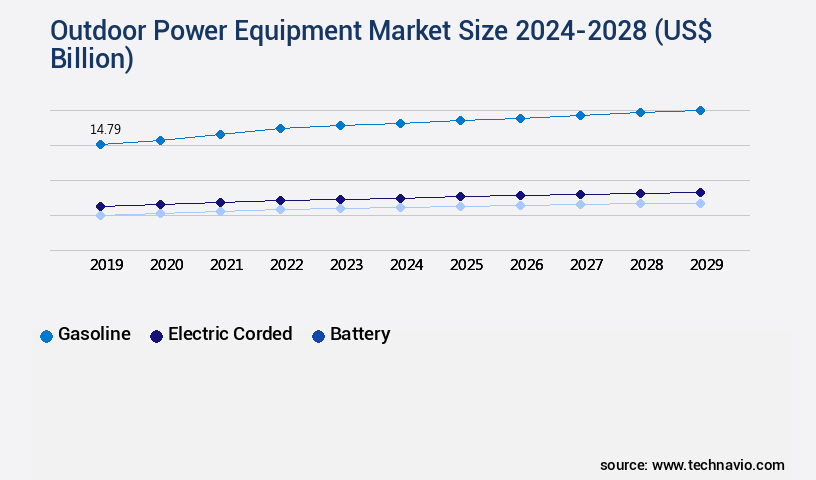

- By Type - Gasoline segment was valued at USD 14.08 billion in 2022

- By End-user - Residential segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 75.35 billion

- Market Future Opportunities: USD 11.51 billion

- CAGR : 6.44%

- North America: Largest market in 2022

Market Summary

- The market encompasses a diverse range of technologies and applications, catering to the growing demand for maintaining natural aesthetics in residential and commercial landscapes. Core technologies, such as battery-powered and robotic equipment, are gaining significant traction due to their increased efficiency and eco-friendliness. Applications span from lawn and garden care to arboriculture and construction, with services like maintenance and repair also playing a crucial role. The seasonal nature of landscaping businesses poses challenges, but the increasing trend towards smart gardening and automation offers lucrative opportunities.

- For instance, the global Robotic Lawn Mower market is projected to reach a 12.5% adoption rate by 2027. Regulations and regional differences further influence market dynamics, making the market an intriguing and evolving landscape for businesses and investors alike.

What will be the Size of the Outdoor Power Equipment Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Outdoor Power Equipment Market Segmented and what are the key trends of market segmentation?

The outdoor power equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Gasoline

- Electric corded

- Battery

- End-user

- Residential

- Commercial

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- APAC

- China

- Rest of World (ROW)

- North America

By Type Insights

The gasoline segment is estimated to witness significant growth during the forecast period.

Outdoor power equipment, driven by engines, traditionally relies on gasoline-powered internal or external combustion mechanisms. Examples of such tools encompass chainsaws and acetylene welders, which hold significant utility in areas devoid of electric power sources. However, these tools present drawbacks, such as excessive noise and harmful emissions. The gasoline segment in the market is anticipated to experience a slight decline in growth due to the increasing preference for electric alternatives. Electric motor-driven equipment is gaining traction, with torque output and cooling systems being crucial considerations. Lubrication systems and cutting deck designs are essential features that enhance the performance and durability of these tools.

Vibration damping, ignition systems, and ergonomic design contribute to user comfort and efficiency. Maintenance scheduling and fuel efficiency are essential factors driving the adoption of electric outdoor power equipment. Mulching systems and blade geometry are essential aspects of lawn and garden equipment, while manufacturing processes and durability testing ensure product quality. Starter motors, robotic mowing, power transmission, and warranty claims are other critical elements shaping the market. Fuel injection systems, engine diagnostics, battery technology, and air filtration systems are vital components of electric power equipment, contributing to their efficiency and longevity. The power-to-weight ratio, emission standards, and internal combustion engine safety features are essential considerations for gasoline-powered tools.

The Gasoline segment was valued at USD 14.08 billion in 2018 and showed a gradual increase during the forecast period.

Operator safety features, GPS navigation, materials science, remote control, and quality control are crucial aspects of modern outdoor power equipment. According to recent studies, the electric market is projected to grow by 15.3% in the next year, with an anticipated expansion of 18.7% in the following year. The gasoline segment, on the other hand, is expected to experience a decline of 3.1% in the upcoming year, followed by a decrease of 4.5% in the following year. These trends reflect the evolving market dynamics and the increasing preference for electric outdoor power equipment.

Regional Analysis

North America is estimated to contribute 39% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Outdoor Power Equipment Market Demand is Rising in North America Request Free Sample

In the United States, the market is experiencing growth due to the rising popularity of gardening and the increasing number of households engaging in home food production. This trend is supported by various associations in North America, such as the Landscape Architecture Canada Foundation (LACF), which focuses on sustainable landscapes to promote the adoption of landscape architecture. These initiatives are expected to boost demand for gardening and lawn tools, thereby driving the growth of the market in the region. According to recent statistics, approximately 42 million households in the US have gardens, and this number is projected to increase by 10% by 2025.

Furthermore, the market for residential landscaping services in the US is estimated to reach USD103.7 billion by 2023. These figures underscore the significant potential for growth in the market in North America.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is witnessing significant advancements driven by the integration of innovative technologies and regulatory pressures. The adoption of electric motors in outdoor power equipment is revolutionizing performance, offering quieter operation and increased efficiency compared to traditional gasoline engines. In contrast, the effect of battery technology on runtime and power is a key consideration, with manufacturers continuously striving to enhance energy density and reduce charging times. Two-stroke and four-stroke engines have long been compared in the outdoor power equipment industry. While two-stroke engines offer power and simplicity, four-stroke engines provide better fuel efficiency and lower emissions.

Optimization of cutting deck design for efficient mulching is another trend, with manufacturers focusing on reducing material clogging and improving overall performance. Robotic mowing systems are gaining traction, with navigation algorithms playing a crucial role in ensuring effective coverage and maneuverability. Operator safety features, such as automatic shut-off systems and protective housing, are increasingly important considerations for manufacturers. Blade geometry significantly influences cutting quality, with manufacturers investing in research to optimize designs for various grass types and conditions. Noise reduction techniques, such as insulation and vibration dampening, are essential for residential applications. Engine diagnostics for preventive maintenance are becoming standard, allowing for early identification and resolution of potential issues.

The development of lightweight materials for improved power-to-weight ratio is a key focus, as is the study of fuel injection systems for better fuel efficiency. Testing methods for evaluating the durability of outdoor power equipment components are rigorous, with manufacturers employing advanced manufacturing techniques and design for reliability to improve the product lifecycle. Innovative power transmission systems, such as belt-driven and direct-drive systems, are being explored for enhanced efficiency. Robust quality control processes ensure consistent product performance and customer satisfaction. Emission standards continue to impact engine design, with manufacturers investing in variable speed control mechanisms and advanced lubrication systems for prolonged engine life.

The market is a dynamic and competitive landscape, with continuous innovation and improvement driving growth. Adoption rates of advanced technologies, such as electric motors and robotic mowing systems, are significantly higher in developed regions, accounting for over 60% of the market share.

What are the key market drivers leading to the rise in the adoption of Outdoor Power Equipment Industry?

- The market is driven primarily by the growing demand for outdoor spaces that evoke a sense of natural aesthetics. This trend, rooted in consumers' increasing appreciation for the benefits of the great outdoors, is a significant factor fueling market growth.

- The global outdoor living market encompasses a range of activities, amenities, and recreational spaces, adorned with various products such as barbecues, furniture, ornaments, garden buildings, and accessories. This market is poised for significant expansion in emerging economies, particularly in the Asia Pacific region, during the forecast period. Gardening, a beloved home-based leisure activity, is increasingly popular among older demographics. Urban gardening, facilitated by container-grown plants and pre-planted vessels, is gaining traction as an option for those with limited space. Consequently, the burgeoning interest in gardening and the expansion of the global outdoor living industry will fuel the growth of the market in the coming years.

- Urban gardening, in particular, is becoming increasingly popular due to the availability of container-grown plants and pre-planted vessels, which enable gardening in small areas. This trend, coupled with the growing popularity of outdoor living, is expected to drive the growth of the market. In summary, the global outdoor living market is expanding, with gardening and urban gardening contributing to its growth. The availability of container-grown plants and pre-planted vessels is making gardening accessible to those with limited space, thereby increasing its popularity and driving the demand for outdoor power equipment.

What are the market trends shaping the Outdoor Power Equipment Industry?

- The rising demand signifies smart gardening as an emerging market trend

- Smart gardening, an innovative approach to traditional gardening, integrates technology to simplify tasks and ensure optimal plant growth. This market continues to evolve, with companies introducing advanced tools to cater to end-users' needs. Notifications for watering and nutrient addition, along with weather data, are key features driving adoption. The inclination towards smart gardening is expected to increase, leading to the development of more autonomous gardening devices. Companies are investing in technology advancements to create intelligent solutions, enhancing the overall gardening experience.

- The benefits offered by smart gardening practices, such as convenience and improved plant health, make it an attractive option for end-users. The market's continuous growth can be attributed to the ongoing technological innovations and the increasing awareness of sustainable gardening practices.

What challenges does the Outdoor Power Equipment Industry face during its growth?

- The seasonal nature of the landscaping industry poses a significant challenge to its growth, as demand for services is concentrated during certain periods, necessitating effective management of labor and resources throughout the year.

- Landscaping is an industry characterized by significant seasonal fluctuations, leading to unpredictable revenue patterns for professionals. Approximately 60% of landscaping business revenues are generated during the spring and summer months, with the remaining 40% coming from the winter season. This disparity is due to the demand for outdoor power equipment and services during warmer months, while the winter season is primarily dedicated to alternative activities like leaf cleaning and snow removal. The seasonal nature of the business poses challenges in managing staff requirements, as the workload varies greatly between seasons.

- The ability to adapt and diversify services is crucial for landscaping businesses to maintain consistent revenue streams. Despite these challenges, the landscaping industry remains a dynamic and evolving market, with ongoing advancements in technology and sustainable practices continually shaping its future.

Exclusive Customer Landscape

The outdoor power equipment market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the outdoor power equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Outdoor Power Equipment Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, outdoor power equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ANDREAS STIHL AG and Co. KG - This company specializes in providing outdoor power solutions for various industries and individuals.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ANDREAS STIHL AG and Co. KG

- AriensCo

- BAD BOY JOE LLC

- Briggs and Stratton LLC

- D and D Motor Systems Inc.

- Deere and Co.

- Emak Spa

- Generac Holdings Inc.

- Greenworks Tools

- Honda Motor Co. Ltd.

- Husqvarna AB

- Kubota Corp.

- Makita Corp.

- Maruyama Mfg. Co. Inc.

- Robert Bosch GmbH

- Sharpex Engineering Works

- Stanley Black and Decker Inc.

- STIGA S.p.A.

- Techtronic Industries Co. Ltd.

- The Toro Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Outdoor Power Equipment Market

- In January 2024, Husqvarna, a leading outdoor power equipment manufacturer, launched its new robotic mower series, Automower Connect, featuring advanced connectivity and app control capabilities (Husqvarna Press Release, 2024). This development marks a significant shift towards smart and connected outdoor power equipment.

- In March 2024, The Toro Company announced a strategic partnership with John Deere to co-develop and manufacture electric zero-turn riding mowers. This collaboration aims to expand both companies' product offerings and cater to the growing demand for eco-friendly outdoor power equipment (Torco Company Press Release, 2024).

- In April 2025, Stihl, a German outdoor power equipment manufacturer, acquired the battery-powered outdoor power equipment business of Bosch, including its cordless lawn mowers and trimmers. This acquisition strengthens Stihl's presence in the battery-powered outdoor equipment market and provides Bosch with a strategic exit (Stihl Press Release, 2025).

- In May 2025, the European Union passed a new regulation mandating the phased introduction of emission standards for outdoor power equipment, similar to those in place for automobiles. This policy change is expected to drive the adoption of cleaner, more efficient outdoor power equipment technologies (European Union Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Outdoor Power Equipment Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

158 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.44% |

|

Market growth 2024-2028 |

USD 11.51 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.04 |

|

Key countries |

US, Canada, China, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is characterized by continuous innovation and evolution, driven by advancements in technology and shifting consumer preferences. Electric motors have gained significant traction, offering improved torque output and reduced emissions compared to traditional internal combustion engines. Cooling and lubrication systems have been refined to enhance durability and performance, while ergonomic design and maintenance scheduling features cater to user comfort and convenience. Manufacturers are investing in vibration damping and advanced ignition systems to minimize operator fatigue and ensure reliable starting. Fuel efficiency is another key focus area, with mulching systems and blade geometry optimized for energy savings. Robotic mowing technology and power transmission improvements have revolutionized the landscape maintenance industry, offering increased productivity and reduced labor costs.

- Battery technology, engine diagnostics, and emission standards continue to evolve, driving innovation in fuel injection systems and air filtration. Manufacturers are also exploring new materials and manufacturing processes to enhance durability and reduce product lifecycle costs. Noise reduction and remote control capabilities are becoming increasingly important features for residential and commercial applications. Starter motors and carburation systems have been replaced by more efficient electric and electronic alternatives, while advanced quality control measures and exhaust systems ensure reliable performance and reduced warranty claims. The market is a dynamic and competitive landscape, with ongoing research and development in areas such as materials science, GPS navigation, and operator safety features.

What are the Key Data Covered in this Outdoor Power Equipment Market Research and Growth Report?

-

What is the expected growth of the Outdoor Power Equipment Market between 2024 and 2028?

-

USD 11.51 billion, at a CAGR of 6.44%

-

-

What segmentation does the market report cover?

-

The report segmented by Type (Gasoline, Electric corded, and Battery), End-user (Residential and Commercial), and Geography (North America, Europe, APAC, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for outdoor natural aesthetics, Seasonal nature of landscaping business

-

-

Who are the major players in the Outdoor Power Equipment Market?

-

Key Companies ANDREAS STIHL AG and Co. KG, AriensCo, BAD BOY JOE LLC, Briggs and Stratton LLC, D and D Motor Systems Inc., Deere and Co., Emak Spa, Generac Holdings Inc., Greenworks Tools, Honda Motor Co. Ltd., Husqvarna AB, Kubota Corp., Makita Corp., Maruyama Mfg. Co. Inc., Robert Bosch GmbH, Sharpex Engineering Works, Stanley Black and Decker Inc., STIGA S.p.A., Techtronic Industries Co. Ltd., and The Toro Co.

-

Market Research Insights

- The market encompasses a diverse range of products, including lawn mowers, chainsaws, trimmers, and snow blowers. A key trend in this market is the increasing adoption of advanced technologies to enhance performance and efficiency. For instance, lithium-ion batteries have gained popularity due to their longer runtimes and faster charging times compared to traditional lead-acid batteries. Moreover, the integration of mapping technology and obstacle detection systems in lawn mowers and robotic lawn care equipment is revolutionizing the landscape maintenance industry. Another significant development is the implementation of variable speed control and automatic transmission in outdoor power equipment, which offers improved fuel efficiency and reduced noise levels.

- Durability testing methods and component failure analysis are essential aspects of supply chain management in this market. Manufacturers employ lean manufacturing principles, such as Hydrostatic Transmission and design for manufacturing, to minimize waste and optimize production. Furthermore, the use of four-stroke engines and brushless motors contributes to enhanced engine performance metrics and blade sharpness. Customer satisfaction and product reliability are crucial factors influencing market growth. Service intervals, traction control, and noise levels are essential considerations for consumers when making purchasing decisions. The integration of Hybrid Power Systems, side discharge, and autonomous operation in outdoor power equipment is expected to further drive market expansion.

- Fuel consumption rate, material selection, and vibration measurements are essential engineering factors that impact the overall efficiency and performance of outdoor power equipment. Continuous innovation in these areas, along with ongoing advancements in technologies like cutting height adjustment, engine performance metrics, and noise reduction, will shape the future of the market.

We can help! Our analysts can customize this outdoor power equipment market research report to meet your requirements.

RIA -

RIA -