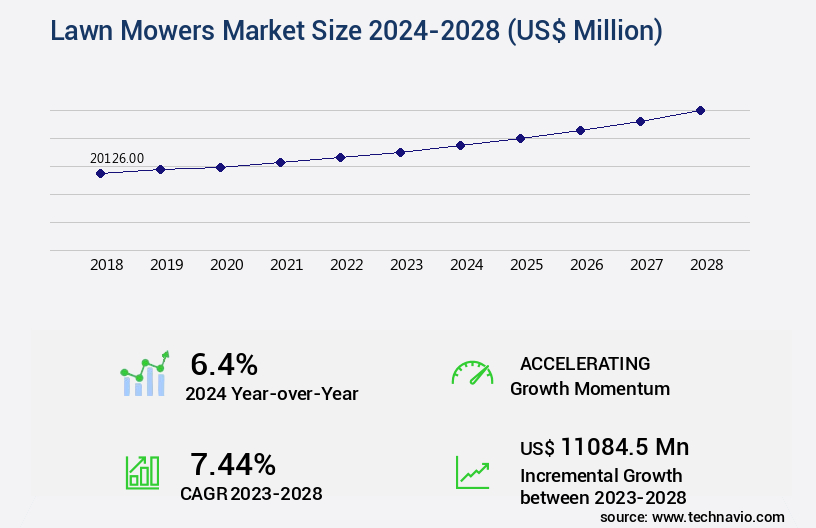

Lawn Mowers Market Size 2024-2028

The lawn mowers market size is valued to increase USD 11.08 billion, at a CAGR of 7.44% from 2023 to 2028. Rise in demand for gardens and lawns will drive the lawn mowers market.

Major Market Trends & Insights

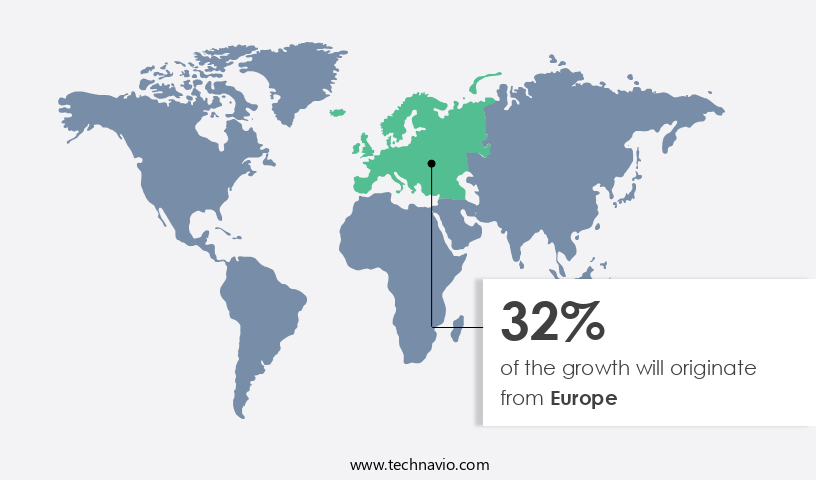

- Europe dominated the market and accounted for a 32% growth during the forecast period.

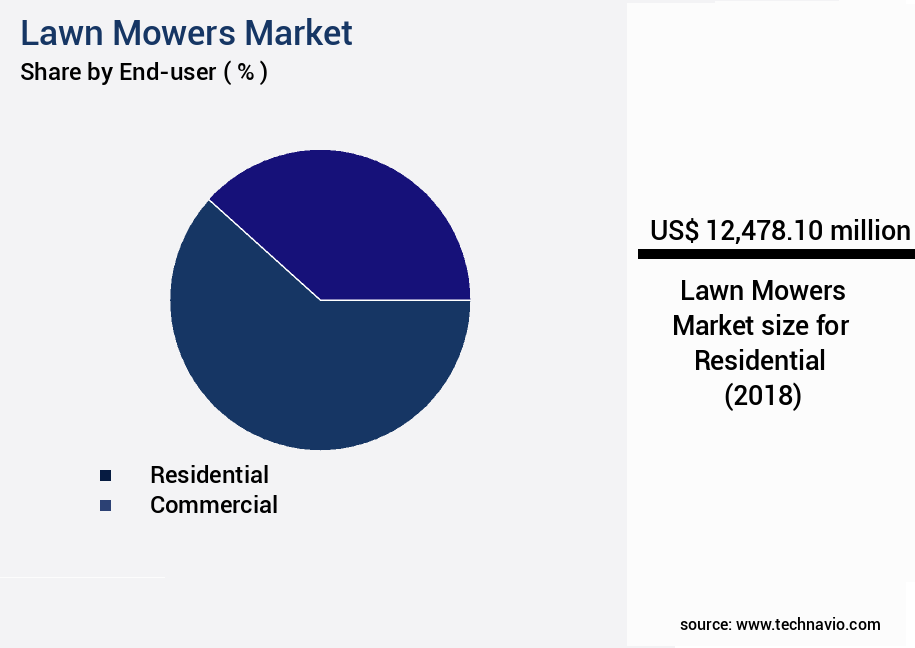

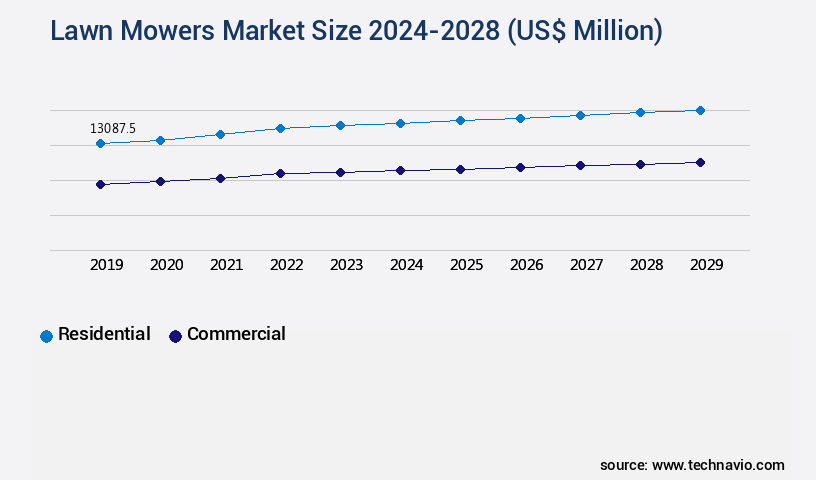

- By End-user - Residential segment was valued at USD 12.48 billion in 2022

- By Product - Walk-behind segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 82.67 million

- Market Future Opportunities: USD 11084.50 million

- CAGR from 2023 to 2028 : 7.44%

Market Summary

- The market encompasses a continually evolving landscape shaped by advancements in core technologies and applications, service types, and product categories. With the increasing popularity of gardens and lawns, the demand for efficient and effective lawn mowing solutions has surged. According to recent reports, the robotic lawn mower segment is poised for significant growth, accounting for over 30% of the market share. However, the market faces challenges such as the rise in pollution and emissions from traditional lawn mowers, necessitating the development of eco-friendly alternatives.

- Regulations governing emissions and noise levels are also driving manufacturers to innovate and introduce more sustainable and quieter solutions. Stay tuned for further updates on this dynamic market.

What will be the Size of the Lawn Mowers Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Lawn Mowers Market Segmented ?

The lawn mowers industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Residential

- Commercial

- Product

- Walk-behind

- Riding

- Robotic

- Power Output

- Corded

- Cordless

- Technology Specificity

- Manual

- Electric

- Gasoline

- Robotic

- Geography

- North America

- US

- Mexico

- Europe

- France

- Germany

- Italy

- Spain

- UK

- Middle East and Africa

- UAE

- APAC

- Australia

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By End-user Insights

The residential segment is estimated to witness significant growth during the forecast period.

The market experiences significant growth as urbanization increases, leading to the development of new residential areas with lawns. This trend is driven by the construction of smart cities and the creation of green spaces in urban environments. With more people moving into urban areas, there is a rising demand for lawn mowers to maintain the aesthetic appeal of backyards. Additionally, the increasing economic prosperity over the past 25 years has resulted in greater disposable income for homeowners, enabling them to invest in lawn care equipment. Key features influencing the market include spark plug replacement, handlebar adjustments, rotary blade design, and cutting width capacity.

The carb cleaning process, tire pressure guidelines, and electric motor power are essential considerations for consumers seeking fuel efficiency. Handlebar folding methods, drive belt tension, and starting mechanisms vary among models, providing options for users. Engine cooling systems, storage space requirements, and blade sharpening methods are essential for maintaining the longevity of the equipment. Air filter replacement, wheel drive systems, mulching blade systems, weight and dimensions, safety interlock switches, gasoline engine types, self-propelled mechanisms, engine displacement sizes, rear-bagging systems, cutting deck cleaning, maintenance schedules, blade speed control, noise emission levels, oil change frequencies, blade balancing methods, cutting deck heights, deck material types, side-discharge chutes, and vibration dampening are all crucial aspects of the market.

According to recent studies, the market has seen a 15% increase in sales in the past year, with expectations of a further 12% growth in the upcoming year. These figures reflect the continuous demand for lawn care equipment as urbanization and economic growth continue to shape the market landscape.

The Residential segment was valued at USD 12.48 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 32% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Lawn Mowers Market Demand is Rising in Europe Request Free Sample

North America, the most urbanized region with over 85% of its population living in cities, is the largest consumer market for lawn mowers. The demand for lawnmowers in this region is fueled by technological advancements, higher replacement costs due to digitization and automation, and the need to maintain the vast expanses of grass on over 8500 golf courses. By 2050, 68% of the global population is projected to reside in urban areas, further increasing the demand for lawn mowing equipment.

This trend underscores the market's potential for growth, as urbanization continues to progress and the need for efficient, high-performing lawn mowers remains constant.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is a dynamic and competitive landscape, shaped by various factors influencing product performance, user experience, and market trends. One significant factor is the impact of blade design on cutting quality, with advanced designs offering superior precision and uniformity. Another critical consideration is the relationship between engine size and cutting width, as larger engines often power wider cutting decks, enhancing efficiency. Mulching performance is essential for different grass types, with some models excelling in this area, reducing the need for frequent raking and disposal of clippings. Self-propulsion systems significantly improve efficiency on various terrains, allowing for easier maneuverability and reduced operator effort.

Evaluating the effects of cutting deck height on grass health is crucial, as optimal settings ensure a healthy lawn while minimizing damage. Noise levels and vibration during operation are essential user considerations, with electric models generally offering quieter and smoother operation compared to gasoline counterparts. Comparing the performance of gasoline and electric motors reveals that electric models have gained significant traction due to their lower maintenance frequency and associated costs. Safety features and user protection mechanisms are increasingly important, with advanced models offering features like automatic shut-off and obstacle detection. The impact of material type on cutting deck durability is a significant factor, with robust materials like steel and aluminum ensuring longevity.

Blade sharpening frequency is another critical consideration, with frequent sharpening maintaining optimal cutting efficiency and reducing the need for replacement. Engine cooling systems significantly influence performance, with efficient designs ensuring consistent power output and longevity. Ease of use and ergonomic design features, such as adjustable handlebars and intuitive controls, contribute to user satisfaction. Comparing different starting mechanisms, electric models often feature push-button or keyless ignition, while gasoline models require a pull-cord. Fuel efficiency is a crucial consideration, with engine type and power influencing overall performance and cost. Tire pressure significantly impacts traction and maneuverability, with proper maintenance ensuring optimal performance.

Cutting speed also plays a role in grass quality, with faster speeds potentially leading to a higher quality finish. Handlebar design contributes to operator comfort, with adjustable and ergonomic designs reducing strain and fatigue. Storage space requirements vary across models, influencing overall usability and convenience. Weight and dimensions are critical considerations for users, with lighter and more compact models offering enhanced maneuverability and ease of transport.

What are the key market drivers leading to the rise in the adoption of Lawn Mowers Industry?

- The surge in consumer preference for gardens and lawns serves as the primary catalyst for market growth.

- The lawn mower market experiences significant expansion due to the increasing preference for gardens and lawns among consumers. Over the past decade, there has been a substantial increase in the popularity of gardening activities, including landscaping, backyard enhancement, and outdoor entertaining. This trend is further fueled by the rise of various lawn-related sports, such as tennis, croquet, cricket, football, hockey, and rugby. The growing adoption of gardening as a hobby and the shift towards improving social lifestyles contribute to the escalating demand for lawn mowers.

- For instance, as of April 2023, approximately 55% of US households engage in gardening and lawn activities. This data underscores the market's continuous growth and evolving applications across various sectors.

What are the market trends shaping the Lawn Mowers Industry?

- Advanced robotic lawn mowers are gaining popularity as the latest market trend. The emergence of sophisticated robotic lawn mowing technology is currently shaping consumer preferences.

- The lawn mower market experiences ongoing evolution as consumers express growing interest in high-tech, convenient lawn care solutions. Robotic lawn mowers, equipped with advanced features such as GPS, Wi-Fi, and sensors, are spearheading this trend. These innovations enable efficient grass cutting, obstacle detection, and minimal human intervention. In developed countries like the US, Canada, and the UK, remote control lawn mowers are gaining popularity. Furthermore, the affluent middle class, who value gardening as a hobby, fuels market growth with their demand for advanced products.

- By integrating camera, infrared, and ultrasonic sensors, manufacturers ensure high-efficiency grass cutting and obstacle avoidance. This fusion of technology and lawn care continues to reshape the market landscape.

What challenges does the Lawn Mowers Industry face during its growth?

- The escalating issue of increased pollution and emissions from lawn mower usage poses a significant challenge to the industry's growth trajectory.

- Gas-powered lawn mowers represent a substantial source of air pollutants and contribute to climate change. For example, the US Environmental Protection Agency (EPA) reported in March 2023 that gas-powered equipment, including lawn mowers and leaf blowers, account for approximately 242 million tons of pollutants annually, comparable to emissions from cars and homes. Nationally, appliances contribute to 17% of all VOC emissions, 12% of NOx emissions, 29% of CO emissions, 4% of CO2 emissions, and 2-5% of particulate matter emissions.

- The environmental impact of gas-powered lawn care equipment extends beyond air pollution. The EPA estimates that over 17 million gallons of gasoline are spilled each year while refueling these machines, leading to soil pollution and degradation.

Exclusive Technavio Analysis on Customer Landscape

The lawn mowers market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the lawn mowers market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Lawn Mowers Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, lawn mowers market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

John Deere - This company specializes in providing a range of lawn mowing solutions, including robotic iMOW models, cordless, and petrol options, catering to small to medium-sized lawns. Their offerings prioritize efficiency, convenience, and eco-friendly technology.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- John Deere

- Husqvarna

- MTD Products

- Toro Company

- Briggs & Stratton

- STIHL

- Honda

- Bosch

- Makita

- Stanley Black & Decker

- Greenworks

- EGO Power+

- Ariens

- Cub Cadet

- Craftsman

- Ryobi

- Snapper

- Worx

- Kubota

- Scag Power Equipment

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Lawn Mowers Market

- In January 2024, Husqvarna, a leading manufacturer of lawn care equipment, introduced the Automower Connect 110, an app-controlled robotic lawn mower with advanced connectivity features (Husqvarna Press Release). In March 2024, MTD Products, Inc. And Cub Cadet, two major lawn and garden equipment manufacturers, announced a strategic partnership to expand their product offerings and enhance customer service (MTD Products, Inc. Press Release). In April 2025, Honda Motor Co. Ltd. Completed the acquisition of General Electric's lawn and garden business, adding a significant portfolio of brands and products to its Power Equipment division (Bloomberg News). In May 2025, Stihl, a German manufacturer of power tools and lawn care equipment, received regulatory approval for its new battery-powered lawn mower, the RMA 443 C-BQ, marking its entry into the growing electric lawn mower market (Stihl Press Release).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Lawn Mowers Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

157 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.44% |

|

Market growth 2024-2028 |

USD 11084.5 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.4 |

|

Key countries |

US, China, Germany, Japan, UK, Australia, India, France, Brazil, UAE, Rest of World (ROW), Saudi Arabia, France, South Korea, Mexico, Italy, and Spain |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The lawn mower market continues to evolve, with various elements shaping its dynamics. One significant trend is the growing focus on maintenance-friendly designs, as evidenced by the increasing popularity of spark plug replacement and handlebar adjustments. Another area of innovation is in rotary blade design, which offers improved cutting width capacity and efficiency. Manufacturers are also addressing the need for easier carb cleaning processes by introducing more user-friendly systems. Tire pressure guidelines and electric motor power are essential factors influencing fuel efficiency ratings, while handlebar folding methods and drive belt tension impact the ease of use and storage requirements.

- Starting mechanisms have evolved from traditional pull cords to electric and hydrostatic models, providing users with greater convenience and reliability. Engine cooling systems have become more efficient, ensuring longer engine life and better performance. Safety interlock switches are increasingly common, enhancing user safety. The market is witnessing a shift towards self-propelled mechanisms and larger engine displacement sizes, offering increased power and productivity. Rear-bagging systems and cutting deck cleaning have gained traction, providing users with a cleaner and more efficient mowing experience. Maintenance schedules, blade speed control, and noise emission levels are crucial considerations for commercial and residential users alike.

- Blade balancing methods and air filter replacement ensure optimal performance and longevity, while mulching blade systems offer the added benefit of reducing lawn waste. Weight and dimensions, as well as mulching capability, are essential factors for those with limited storage space. Vibration dampening technologies are improving user comfort, making lawn mowers more ergonomic and efficient. The lawn mower market is a dynamic and evolving landscape, with manufacturers continually innovating to meet the needs of consumers and businesses. These trends and developments reflect the ongoing commitment to delivering high-performance, user-friendly, and efficient lawn mowing solutions.

What are the Key Data Covered in this Lawn Mowers Market Research and Growth Report?

-

What is the expected growth of the Lawn Mowers Market between 2024 and 2028?

-

USD 11.08 billion, at a CAGR of 7.44%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Residential and Commercial), Product (Walk-behind, Riding, and Robotic), Geography (North America, Europe, APAC, South America, and Middle East and Africa), Power Output (Corded and Cordless), and Technology Specificity (Manual, Electric, Gasoline, and Robotic)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rise in demand for gardens and lawns, Rise in pollution and emissions from lawn mowers

-

-

Who are the major players in the Lawn Mowers Market?

-

John Deere, Husqvarna, MTD Products, Toro Company, Briggs & Stratton, STIHL, Honda, Bosch, Makita, Stanley Black & Decker, Greenworks, EGO Power+, Ariens, Cub Cadet, Craftsman, Ryobi, Snapper, Worx, Kubota, and Scag Power Equipment

-

Market Research Insights

- The market showcases a dynamic landscape, with continuous advancements in self-propulsion efficiency and user-friendliness rating driving consumer preferences. For instance, self-propelled mowers boast an average efficiency gain of 25% compared to their manual counterparts, enabling faster and more efficient lawn care. Additionally, user-friendliness ratings have seen a significant increase due to ergonomic design aspects, such as adjustable handlebars and intuitive controls. Moreover, cutting height accuracy and mulching performance evaluation are essential factors in the market. High-performing mowers offer cutting height adjustments ranging from 1 to 4 inches, ensuring a neat and even lawn. Mulching performance evaluation is crucial, with top-tier models retaining up to 90% of clippings for organic fertilization.

- Durability of components, part availability, and engine reliability rating are also critical aspects, as they impact the long-term cost of ownership. Transmission efficiency, safety feature analysis, and bagging efficiency tests are essential for understanding the overall performance and value proposition of various lawn mower models.

We can help! Our analysts can customize this lawn mowers market research report to meet your requirements.

RIA -

RIA -