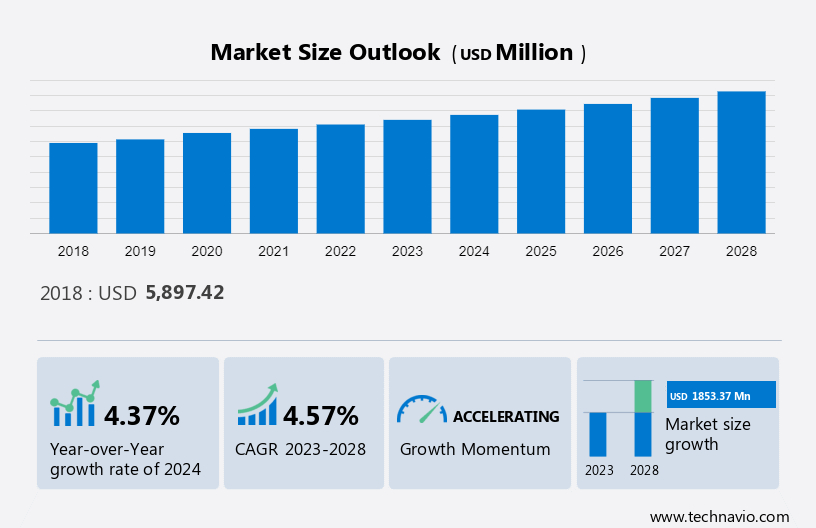

Packaged Croissant Market Size 2024-2028

The Packaged Croissant Market size is projected to increase by USD 1.85 billion, at a CAGR of 4.57% between 2023 and 2028. The market is influenced by several key factors driving its growth trajectory. With a surge in urbanization and evolving lifestyles, there's a noticeable shift towards convenience foods, elevating the demand for packaged croissants. This trend is further propelled by the innovation witnessed in bakery product offerings across different cafes, where consumers seek diverse and enticing options. As the market continues to evolve, manufacturers are tapping into this demand, introducing new flavors, fillings, and variations to cater to changing consumer preferences. Additionally, the convenience factor of packaged croissants aligns well with the fast-paced lifestyles of modern consumers, contributing to their popularity in the market. Overall, these dynamics highlight the resilience and adaptability of the Packaged Croissant Market amidst changing consumer needs and preferences.

The market shows an Accelerated CAGR during the forecast period.

To get additional information about the market, Request Free Sample

Market Segmentation by Distribution Channel

The largest distribution channel is offline sales. In offline sales, the customer purchases products from a physical store, such as a grocery store or convenience store. Offline distribution channels deliver consumers a variety of purchasing options. Most supermarkets and retail stores in the GCC packaged food market have a section dedicated to baked goods, prominently displayed. Another important component of offline distribution is the convenience store. Convenience stores are a great option for people who want to make an impulse purchase while on the go. Thus, such factors under the offline segment of the distribution channel will drive the GCC packaged food market during the forecast period. These offline channels cater to diverse consumer preferences and contribute significantly to the accessibility and availability of packaged food products across the GCC region.

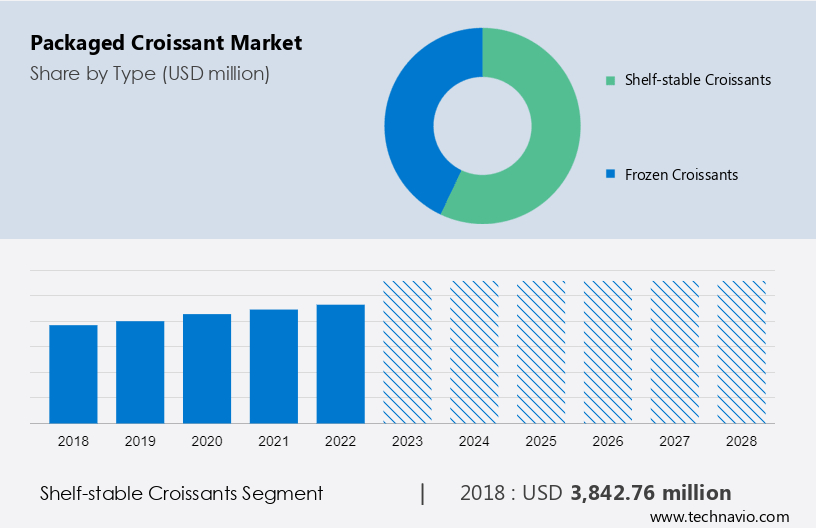

Market Segmentation by Type

The market share growth by the shelf-stable croissants segment will be significant during the forecast period. Shelf-stable croissants are suitable for long-term storage and consumption without the need for refrigeration. This segment is intended for consumers who are looking for convenience, long-term shelf life, and availability in their daily croissant consumption. Croissants that are shelf-stable provide a few benefits for both producers and consumers.

The shelf-stable croissants segment was valued at USD 3.84 billion in 2017.

For a detailed summary of the market segments Request for Sample Report

Shelf-stable croissants, like many bakery products, come in a variety of flavors, fillings, and shapes. To meet the needs of different tastes, manufacturers often experiment with different fillings, such as chocolate-flavored, almond-flavored, vanilla-flavored, or fruit-flavored fillings. There is also a focus on keeping the flaky, buttery texture of the croissant, even with a longer shelf life. Thus, such factors under the shelf-stable croissants segment will drive the growth of bakery products during the forecast period. These innovations in croissant production cater to consumer preferences for convenience without compromising on taste or quality. The versatility of shelf-stable bakery products like croissants enhances their appeal across various retail channels, including supermarkets, convenience stores, and online platforms, contributing to the overall growth of the bakery products market.

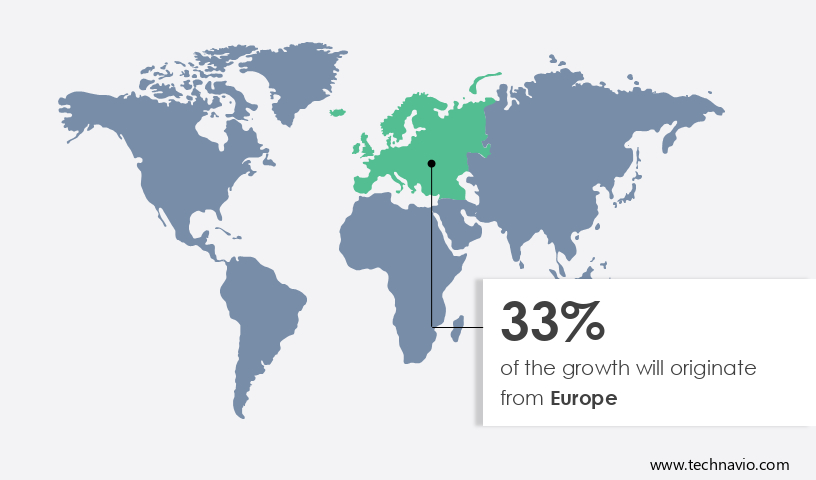

Key Regions for the Market

Europe is estimated to contribute 33% to the growth of the global market during the forecast period

Get a glance at the market share of various regions View PDF Sample

Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period. Europe has many established bakery shops and chains, and the market in this region is well-established in terms of innovation, consumer preferences, and distribution channels. Moreover, the demand for packaged croissants is increasing at a faster rate than other bakery items because of their easy-to-eat nature and excellent sweet taste.

Furthermore, the regional market, particularly in the India frozen food market, is fueled by growing disposable income, high demand for convenience foods, and increasing interest in healthier products. In addition, there is a rising demand for multicultural flavors and designs, as well as preferences for reduced sugar, low-calorie, and low-fat packaged croissants. These factors are expected to drive significant growth in the India frozen food market during the forecast period. Manufacturers are innovating to meet these consumer preferences, offering a variety of shelf-stable croissants that cater to diverse tastes and dietary needs. The convenience and versatility of frozen bakery products like croissants make them popular choices among consumers seeking convenient yet wholesome food options. As consumer lifestyles evolve and preferences for convenient, healthier foods increase, the demand for frozen bakery products, including croissants, is set to rise in the India market.

Market Dynamics and Customer Landscape

The market is experiencing significant growth, with French & Austrian varities leading the trend. As metropolitan areas expand, consumers are increasingly aware of the adverse health effects of saturated fats, driving demand for healthier options that support heart health. Brands like Bridor offer a diverse range of products, including Mini Filled Croissants, which cater to changing consumer preferences. However, occasional product recalls underscore the importance of stringent regulations in ensuring product safety and quality. Both online and independent retailers play a crucial role in distributing these pastries, known for their flaky texture and buttery flavor. From plain to chocolate-filled, packaged croissants continue to captivate consumers and dominate retail establishments worldwide.

Key Market Drivers

The market witnesses growth propelled by increasing demand for convenience foods such as Croissant Products and Ready-to-Eat Croissants. Busy lifestyles drive preference for Breakfast Items and Bakery Goods requiring minimal preparation, fostering market growth. Product Innovation and Quality Assurance are crucial in meeting consumer needs and ensuring satisfaction in the Baked Goods Industry.

In addition, the market research forecasts continued expansion, aiding Croissant Suppliers and Retailers in anticipating demand and adapting strategies. The evolution of Croissant Preservation Techniques enhances product quality, contributing to sustained market growth.

Significant Market Trends

Rising disposable income among people is the primary trend shaping market growth. Due to packaged croissants being ready to eat and convenient, they are evolving into a popular option for people who are on the go and want a tasty and quick breakfast or snack. Customer tastes have also evolved as a result of rising disposable money, as individuals now prioritize convenience over quality. Packaged croissants are made by a number of international and local producers and are a desirable substitute for freshly baked croissants due to their uniform taste and texture.

Additionally, packaged croissants are more appealing because they are easy for customers to include in their regular routines when purchased from nearby retail locations or online. Besides, people who are strapped for time and prefer packaged croissants for a quick breakfast or on-the-go snack are becoming more and more common. Thus, such factors will drive the growth of the global packaged croissant market during the forecast period, with market trends and market growth analysis indicating sustained momentum. Moreover, advancements in Croissant Packaging and manufacturing processes contribute to the expansion of the Packaged Bakery Goods sector, further enhancing market growth. Additionally, continuous innovation in Croissant Ingredients ensures product quality and appeals to evolving consumer preferences, fostering market development.

Major Challenges

Unpleasant health effects of bakery items due to high calories and fat is a challenge that affects market growth. Butter is commonly used to make these flaky pastries, which adds to their rich flavor but also raises their calorie and fat content. Frequent intake of these high-calorie croissants may result in weight gain and an increased risk of developing health problems associated with obesity, such as diabetes and heart disease.

Moreover, overindulging in added sugars can raise the risk of obesity, chronic illnesses like type 2 diabetes, and dental issues. Commonly employed to prolong the shelf life of packaged croissants, artificial preservatives have been linked to negative health outcomes, including allergic responses and gastrointestinal problems in certain people. Thus, such factors may impede the market during the forecast period.

Company Overview

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

- Key Offering- Bauli S.p.A.: The company offers products such as vanilla cream filled croissants and chocolate filled croissants, under the brand called BAULI MOONFILS.

- Key Offering- Corporativo Bimbo SA de CV: The company offers products such as mouthwatering croissants with toppings, under the brand called Cuernitos.

- Key Offering- Edita Food Industries: The company offers products, such as chocolate and strawberry, under the brand Molto.

The market growth and forecasting report also includes detailed analyses of the competitive landscape of the market and information about 20 market companies, including:

- Boulangerie Solignac

- Britannia Industries Ltd.

- FRESH SNACK

- General Mills Inc.

- Lantmannen ekonomisk forening

- McCain Foods Ltd.

- Mondelez International Inc.

- Pizzo and Crozzo

- Rademaker BV

- San Giorgio Spa

- Spanish Market doo

- Starbucks Corp.

- Sydney Cake House Sdn Bhd

- Tata Sons Pvt. Ltd.

- Upper Crust

- Vancouver Croissant Enterprises Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Segment Overview

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD Billion" for the period 2024 to 2028, as well as historical data from 2018 to 2022 for the following segments.

- Type Outlook

- Shelf-stable croissants

- Frozen croissants

- Distribution Channel Outlook

- Offline

- Online

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- The U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- South America

- Chile

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- North America

You may also interested in below market reports:

- GCC - Packaged Food Market - GCC - Packaged Food Market by Distribution Channel, and Product - Forecast and Analysis

- Bakery Products Market - Bakery Products Market Analysis APAC, Europe, North America, South America, Middle East and Africa - US, China, Japan, India, Germany - Size and Forecast

- India Frozen Food Market - India Frozen Food Market by Product and Distribution Channel - Forecast and Analysis

Market Analyst Overview

The market presents a dynamic landscape influenced by various factors. The sector's growth is not only driven by traditional European-style pastries like the Danish pastry but also by evolving consumer preferences for almond-filled and savory options. With hectic schedules, consumers seek convenient snack options, and packaged croissants offer indulgent taste in the breakfast foods segment. Online retailers play a significant role in catering to these demands, enabling consumers to access a wide range of products. To stay competitive, market participants must innovate and broaden their product offerings, satisfying customer needs for healthier indulgence with lower fat content and multigrain options. Furthermore, embracing global flavors while incorporating familiar local ingredients ensures appeal to adventurous palates, fostering comfort and familiarity.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

152 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.57% |

|

Market Growth 2024-2028 |

USD 1.85 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.37 |

|

Regional analysis |

Europe, North America, APAC, South America, and Middle East and Africa |

|

Performing market contribution |

Europe at 33% |

|

Key countries |

US, China, Germany, France, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Bauli S.p.A., Boulangerie Solignac, Britannia Industries Ltd., Corporativo Bimbo SA de CV, Edita Food Industries, FRESH SNACK, General Mills Inc., Lantmannen ekonomisk forening, McCain Foods Ltd., Mondelez International Inc., Pizzo and Crozzo, Rademaker BV, San Giorgio Spa, Spanish Market doo, Starbucks Corp., Sydney Cake House Sdn Bhd, Tata Sons Pvt. Ltd., Upper Crust, and Vancouver Croissant Enterprises Ltd. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and Market condition analysis for the market forecast period. |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

BUY NOW Full Report and Discover more

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the growth of the market between 2024 and 2028

- Precise estimation of the market size and its contribution to the market in focus on the parent market

- Accurate predictions about upcoming trends and changes in consumer behavior

- Growth of the market across Europe, North America, APAC, South America, and Middle East and Africa

- A thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market forecasting companies

We can help! Our analysts can customize this market research and growth report to meet your requirements. Get in touch

RIA -

RIA -