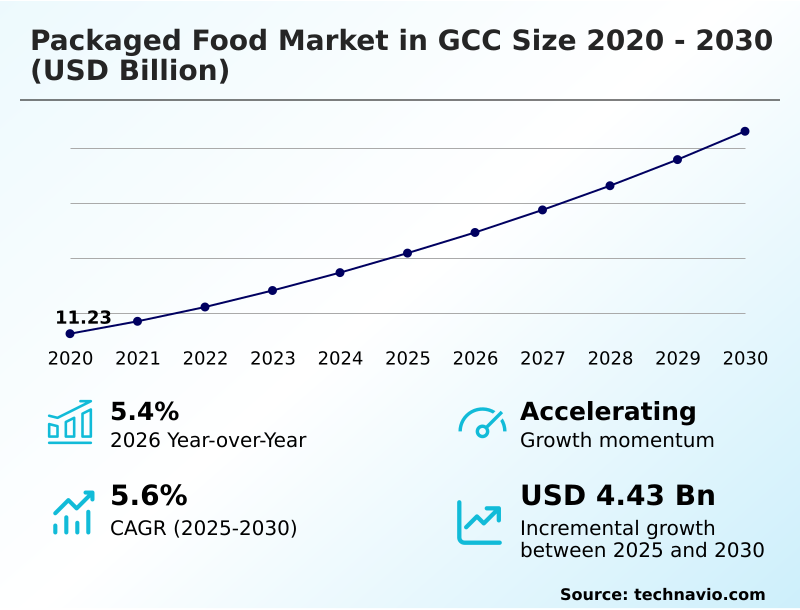

GCC Packaged Food Market Size 2026-2030

The gcc packaged food market size is valued to increase by USD 4.43 billion, at a CAGR of 5.6% from 2025 to 2030. Urbanization and changing lifestyles will drive the gcc packaged food market.

Major Market Trends & Insights

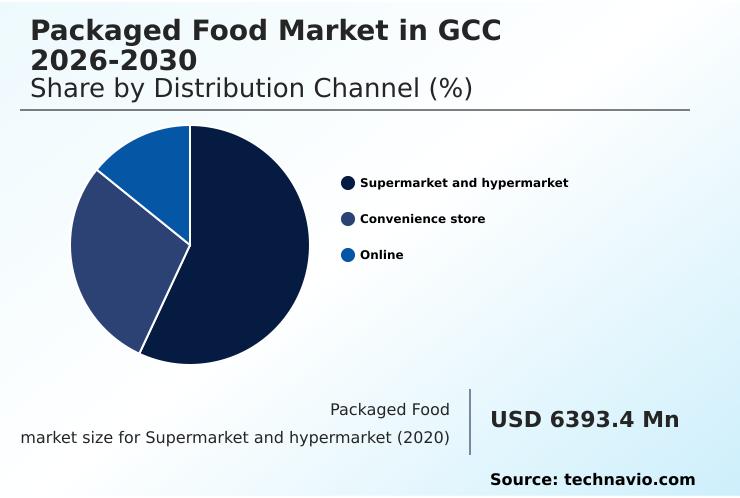

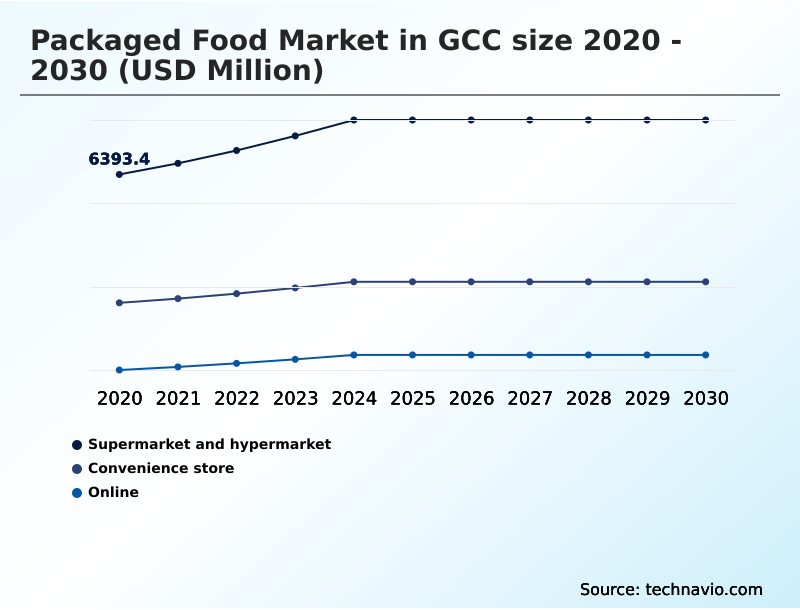

- By Distribution Channel - Supermarket and hypermarket segment was valued at USD 7.73 billion in 2024

- By Product - Bakery and cereals segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 7.36 billion

- Market Future Opportunities: USD 4.43 billion

- CAGR from 2025 to 2030 : 5.6%

Market Summary

- The packaged food market in GCC is characterized by its dynamic response to shifting demographics and economic diversification efforts. Growth is underpinned by the rising demand for convenience, which has propelled the adoption of ready-to-eat meals and value-added processed food.

- Innovations in thermal processing technology and aseptic packaging solutions are critical in extending shelf life and ensuring product safety, addressing consumer concerns and regulatory mandates.

- A key operational focus is optimizing the cold chain infrastructure to manage the distribution of frozen and dairy products efficiently across vast distances, a scenario where a 15% improvement in logistical efficiency can significantly reduce spoilage and operational costs.

- Furthermore, the emphasis on food security is encouraging investment in local production, reducing reliance on imports and fostering a more resilient supply chain. Companies are increasingly adopting clean label formulations and sustainable packaging materials, aligning with consumer preferences for health and environmental responsibility.

- This evolution requires constant adaptation in product development, marketing, and supply chain management to maintain competitiveness in a crowded marketplace.

What will be the Size of the GCC Packaged Food Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the GCC Packaged Food Market Segmented?

The gcc packaged food industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- Supermarket and hypermarket

- Convenience store

- Online

- Product

- Bakery and cereals

- Dairy products

- Processed and canned Food

- Meat and fish

- Others

- Category

- Conventional

- Organic

- Geography

- GCC

By Distribution Channel Insights

The supermarket and hypermarket segment is estimated to witness significant growth during the forecast period.

Supermarkets and hypermarkets are the primary distribution channel, commanding over 55% of sales volume. This channel's dominance is sustained by its extensive cold chain infrastructure and capacity for high-volume turnover of products like shelf-stable dairy products.

These outlets are crucial for achieving broad geographic coverage and ensuring food safety compliance for both staple food products and premium packaged goods.

The competitive landscape necessitates strong retail partnerships, which influence everything from shelf positioning to promotional strategies for ready-to-consume meals.

Companies leverage these large-format stores to maintain brand visibility and manage automated inventory management, which is essential for handling both high-demand items and introducing niche clean label formulations. This channel effectively supports both mass-market and health-conscious consumers' needs.

The Supermarket and hypermarket segment was valued at USD 7.73 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

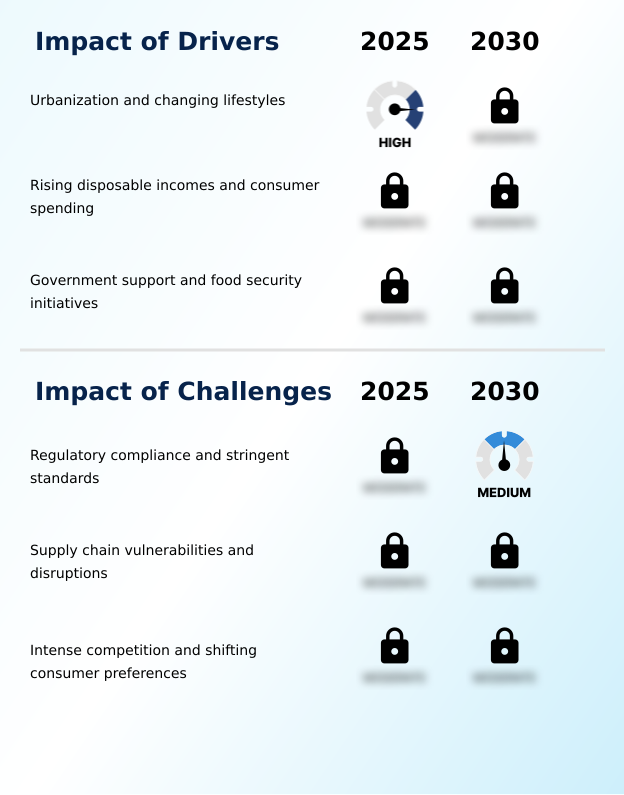

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic direction of the packaged food market is increasingly shaped by the impact of urbanization on packaged food demand, which has accelerated the need for convenient, high-quality options. A pivotal element in this shift is the role of e-commerce in GCC food retail, which has lowered barriers to entry and intensified competition.

- In response, established companies are focusing on strategies for sustainable packaging in food to align with both regulatory pressures and consumer sentiment. This pivot introduces new complexities, particularly around the challenges of cold chain logistics management, where maintaining integrity from plant to consumer is paramount.

- Simultaneously, consumer trends in healthy packaged snacks continue to influence product innovation, with a marked preference for clean-label and fortified items. Government policies for food security enhancement are a powerful driver, encouraging domestic production and investment in technology adoption in food processing plants to mitigate supply chain vulnerability to geopolitical risks.

- Premiumization trends in the dairy category and the growth of the ready-to-eat meal segment reflect rising disposable incomes. However, navigating packaged food import regulations and ensuring nutritional labeling compliance requirements remain critical hurdles. The importance of halal certification for market access cannot be overstated.

- Furthermore, the demand for plant-based packaged foods and opportunities in functional beverages are creating new avenues for growth, while the competitive landscape of private label foods and managing raw material price fluctuations require sophisticated processed food consumption patterns analysis.

- Businesses that master these dynamics, including strategies for reducing food processing waste, are better positioned for success, often outperforming peers in operational efficiency by a notable margin.

What are the key market drivers leading to the rise in the adoption of GCC Packaged Food Industry?

- The key market driver is the convergence of rapid urbanization and changing lifestyles, which accelerates demand for convenient packaged food products.

- Market expansion is fueled by strong socioeconomic drivers, primarily rapid urbanization and rising disposable incomes. These factors heighten demand for convenient food options, as seen in the double-digit growth of the ready-to-eat meals category in major urban centers.

- Government-led food security initiatives and import substitution policies are also critical, encouraging investment in local manufacturing and enhancing food processing efficiency.

- These programs often include incentives for adopting advanced thermal processing technology, which has helped certain producers increase output by up to 15%.

- The expansion of modern retail channels and the growth of e-commerce platforms further stimulate the market by improving access to a diverse range of packaged food, including processed meat and seafood, and bolstering consumer brand recognition across multiple touchpoints.

What are the market trends shaping the GCC Packaged Food Industry?

- A prominent market trend is the increasing health and wellness orientation among consumers. This shift is driving demand for nutritious and functional packaged food options.

- Key market trends are redefining product development and consumer engagement. The shift toward health and wellness is pronounced, with a growing number of health-conscious consumers seeking out functional ingredients and fortified dairy products. This has led to the adoption of technologies like probiotic enrichment, with sales in this sub-segment growing at nearly double the rate of conventional counterparts.

- Sustainability is also a major influence, driving demand for eco-friendly packaging and creating new opportunities for on-the-go consumption formats. Consequently, companies are investing in modified atmosphere packaging and other innovations. Premiumization is another significant trend, as rising incomes fuel demand for gourmet and value-added processing, particularly in indulgent snack offerings and ready-to-cook formats, where brands differentiate through quality and innovation.

What challenges does the GCC Packaged Food Industry face during its growth?

- A key challenge affecting industry growth is the need for strict regulatory compliance with stringent food safety and quality standards.

- The market faces several structural challenges, led by the complexities of regulatory compliance and the need for rigorous food safety protocols. Adherence to evolving nutritional labeling regulations and portion control packaging guidelines can increase operational costs by over 10% for some manufacturers.

- Supply chain vulnerabilities present another significant hurdle, with geopolitical tensions and logistical bottlenecks impacting the consistent availability of raw materials and finished goods. This necessitates greater investment in supply chain resilience and local sourcing. Intense competition, coupled with rapidly shifting consumer preferences toward healthier, less-processed options, forces companies to innovate continuously.

- Balancing competitive pricing strategies with the high cost of R&D for new formulations and controlled atmosphere packaging presents a persistent challenge for maintaining profitability and market share in a crowded field.

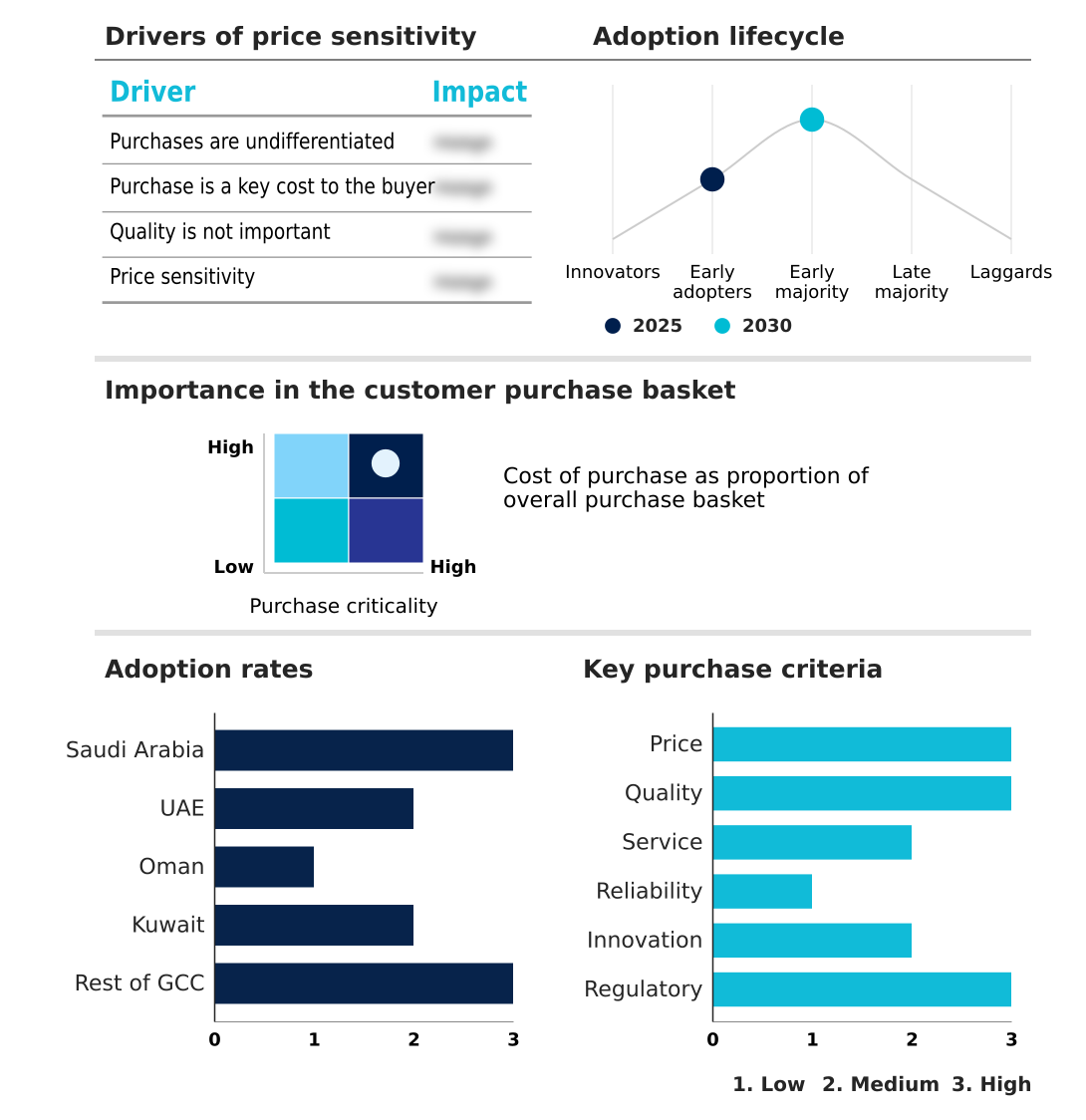

Exclusive Technavio Analysis on Customer Landscape

The gcc packaged food market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the gcc packaged food market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of GCC Packaged Food Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, gcc packaged food market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Al Ain Farms - Offerings are centered on frozen and processed foods, including ready-to-cook meals, meats, and snacks, designed to meet the demands of convenience-driven consumers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Al Ain Farms

- Al Kabeer Group ME

- Al Rawabi Dairy Co L.L.C.

- Almarai Co.

- Americana Foods Inc.

- Arla Foods amba

- Balade Farms Food Industries LLC

- Baladna

- Danone S.A.

- Emirates Food Industries

- Forsan Foods and Consumer Products Ltd.

- General Mills Inc.

- Global Food Industries LLC

- IFFCO Group

- Mondelez International Inc.

- Nestle SA

- Reesha General Trading L.L.C.

- Saudia Dairy and Foodstuff Co.

- Savola Group

- Unikai Foods PJSC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Gcc packaged food market

- In November 2024, Almarai selected a strategic partner for its five-year expansion plan, which is aimed at increasing production capacity to support national food security objectives.

- In January 2025, Almarai deployed advanced digital solutions to power its expansion, improving operational efficiency and contributing to the goal of greater self-reliance in food production.

- In April 2025, Carrefour expanded its online grocery and quick commerce services across the UAE and Saudi Arabia, enhancing the availability and delivery speed of packaged food.

- In September 2025, Almarai finalized its acquisition of Pure Beverage Industry Company, marking its entry into the bottled water market to diversify its portfolio and meet premium hydration trends.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled GCC Packaged Food Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 214 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.6% |

| Market growth 2026-2030 | USD 4430.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.4% |

| Key countries | Saudi Arabia, UAE, Oman, Kuwait and Rest of GCC |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The packaged food market is undergoing a significant transformation, driven by a convergence of consumer, regulatory, and technological forces. The adoption of advanced packaging solutions and high-pressure processing (HPP) is becoming standard for ensuring product integrity and extending shelf life.

- A core boardroom-level focus is aligning product portfolios with the demand for clean label formulations and functional ingredients, which directly impacts R&D budgeting and ingredient sourcing transparency. For example, a focus on retort processing for ready-to-eat meals can improve production output by over 10%.

- Emphasis is placed on vertical integration operations and food processing automation to enhance efficiency and maintain stringent food safety compliance. Moreover, companies are leveraging digital grocery platforms and sophisticated supply chain traceability systems to navigate the complexities of both local and international distribution.

- Success hinges on mastering everything from UHT processing for dairy to the nuances of halal certification standards and sustainable packaging materials.

What are the Key Data Covered in this GCC Packaged Food Market Research and Growth Report?

-

What is the expected growth of the GCC Packaged Food Market between 2026 and 2030?

-

USD 4.43 billion, at a CAGR of 5.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Supermarket and hypermarket, Convenience store, and Online), Product (Bakery and cereals, Dairy products, Processed and canned food, Meat and fish, and Others), Category (Conventional, and Organic) and Geography (GCC)

-

-

Which regions are analyzed in the report?

-

GCC

-

-

What are the key growth drivers and market challenges?

-

Urbanization and changing lifestyles, Regulatory compliance and stringent standards

-

-

Who are the major players in the GCC Packaged Food Market?

-

Al Ain Farms, Al Kabeer Group ME, Al Rawabi Dairy Co L.L.C., Almarai Co., Americana Foods Inc., Arla Foods amba, Balade Farms Food Industries LLC, Baladna, Danone S.A., Emirates Food Industries, Forsan Foods and Consumer Products Ltd., General Mills Inc., Global Food Industries LLC, IFFCO Group, Mondelez International Inc., Nestle SA, Reesha General Trading L.L.C., Saudia Dairy and Foodstuff Co., Savola Group and Unikai Foods PJSC

-

Market Research Insights

- The market's dynamic is shaped by a convergence of forces, including evolving dietary preferences and the expansion of modern retail channels. A notable shift toward health-conscious consumption has led to a greater emphasis on plant-based nutrition and functional foods, with some brands achieving up to a 10% sales lift in fortified product lines.

- The rise of e-commerce platforms has also been transformative, providing consumers with greater choice and intensifying competition. This digital shift has made supply chain resilience a critical success factor, as companies that optimize logistics can reduce delivery times by 20%.

- As consumer spending power grows, there is an increasing appetite for premium lifestyle products and indulgent snack offerings, encouraging product diversification. Consequently, firms are navigating this landscape by balancing competitive pricing strategies with investments in innovation and brand equity to capture discerning consumers.

We can help! Our analysts can customize this gcc packaged food market research report to meet your requirements.

RIA -

RIA -