PD-1 And PD-L1 Inhibitors Market Size 2026-2030

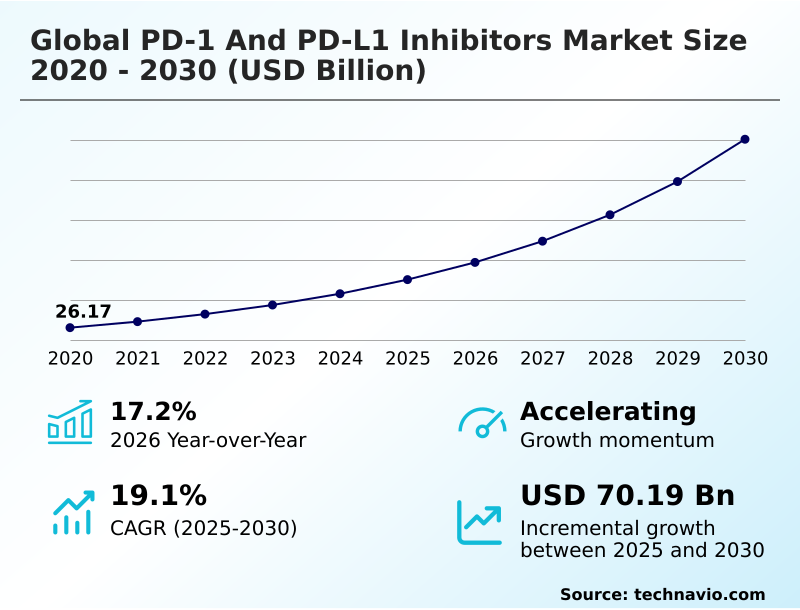

The pd-1 and pd-l1 inhibitors market size is valued to increase by USD 70.19 billion, at a CAGR of 19.1% from 2025 to 2030. Strategic expansion of therapeutic applications into earlier disease stages will drive the pd-1 and pd-l1 inhibitors market.

Major Market Trends & Insights

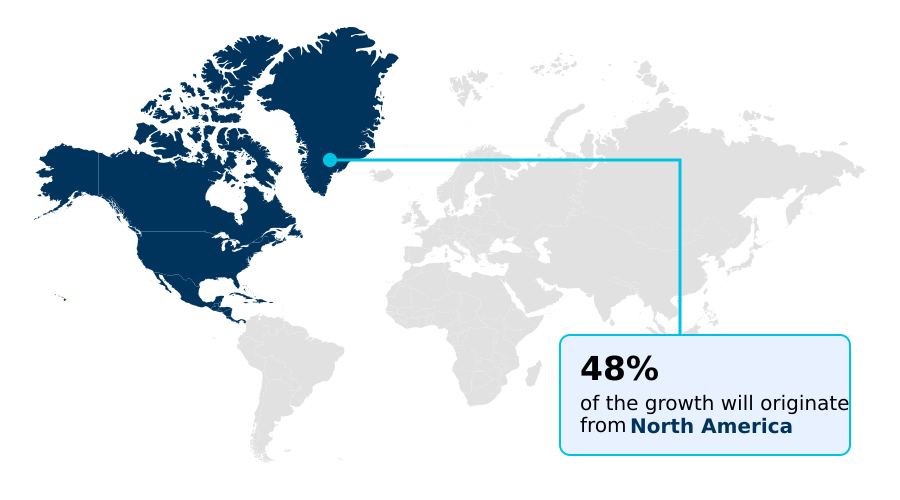

- North America dominated the market and accounted for a 48.1% growth during the forecast period.

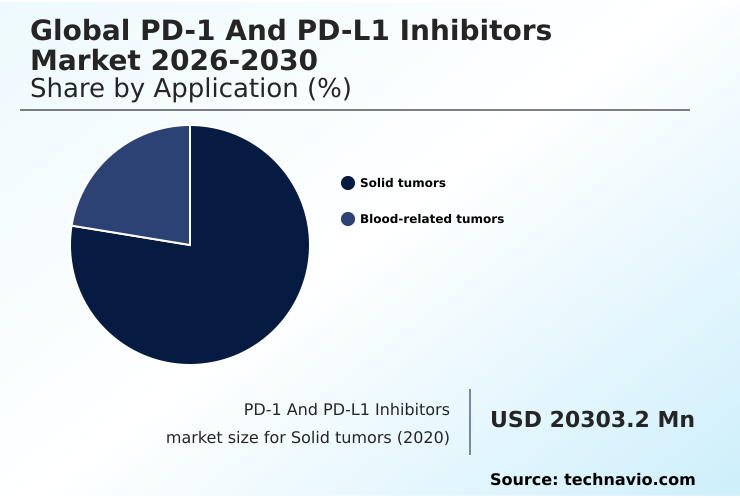

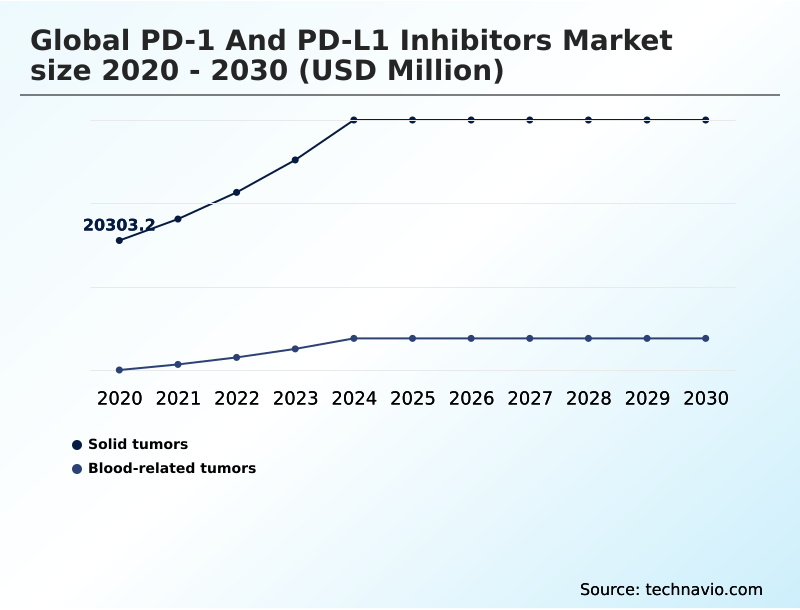

- By Application - Solid tumors segment was valued at USD 33.74 billion in 2024

- By Type - PD-1 segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 94.21 billion

- Market Future Opportunities: USD 70.19 billion

- CAGR from 2025 to 2030 : 19.1%

Market Summary

- The PD-1 and PD-L1 inhibitors market is fundamentally reshaping cancer immunotherapy by leveraging the immune checkpoint pathway to restore T-cell activation against malignancies. The core of this market revolves around sophisticated monoclonal antibody therapy designed to block inhibitory signals within the tumor microenvironment, thereby unleashing anti-tumor immunity.

- A key dynamic is the relentless push toward combination therapies, where these inhibitors are paired with other agents to overcome resistance and improve outcomes. For instance, a hospital system implementing a new protocol for neoadjuvant therapy in non-small cell lung cancer would integrate checkpoint inhibitors with chemotherapy.

- This requires deploying advanced companion diagnostics to assess biomarker expression and training clinical staff to proactively manage potential immune-related adverse events. This strategic integration of immuno-oncology into earlier treatment stages aims to improve long-term metrics like overall survival benefit, representing a paradigm shift in oncological care and driving sustained innovation in the field.

What will be the Size of the PD-1 And PD-L1 Inhibitors Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the PD-1 And PD-L1 Inhibitors Market Segmented?

The pd-1 and pd-l1 inhibitors industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Solid tumors

- Blood-related tumors

- Type

- PD-1

- PD-L1

- Distribution channel

- Hospital

- Retail

- Online pharmacies

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Application Insights

The solid tumors segment is estimated to witness significant growth during the forecast period.

The market's solid tumors segment is defined by therapies targeting a range of malignancies. A primary focus is on activating anti-tumor immunity through immuno-oncology strategies.

The application of neoadjuvant therapy and adjuvant treatment is transforming oncological intervention strategies from late-stage to early-stage disease management, a shift that has improved event-free survival by over 15% in certain trial cohorts.

The development of advanced combination therapies, including those with antibody-drug conjugates (ADCs), aims to enhance PD-1 inhibitor mechanism efficacy.

Furthermore, the use of companion diagnostics to measure biomarker expression is critical for guiding patient selection in precision immuno-oncology, ensuring that PD-L1 inhibitor efficacy is maximized. This approach refines treatment for various solid tumor indications.

The Solid tumors segment was valued at USD 33.74 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 48.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How PD-1 And PD-L1 Inhibitors Market Demand is Rising in North America Get Free Sample

North America continues to lead the market, accounting for over 48% of activity due to its advanced research infrastructure and high adoption rates of novel oncological intervention strategies.

The region's leadership is reinforced by a robust regulatory approval process that accelerates market access. In Europe, a key focus is managing biosimilar competition, which has driven manufacturers to innovate.

This competitive pressure has helped streamline clinical pathways, reducing average patient wait times for initial therapy by 10% in some national health systems.

Meanwhile, the market in Asia is expanding rapidly, fueled by rising healthcare investment and a growing focus on immuno-oncology drug development, particularly around pembrolizumab indications and nivolumab mechanism of action.

The increasing number of clinical trials for durvalumab and atezolizumab side effects management highlights the region's growing role in global research.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the oncology sector increasingly involves comparing pd-1 and pd-l1 inhibitors to determine the optimal therapeutic approach for specific patient populations. The cost-effectiveness of pd-1 inhibitors remains a central topic in health economics, influencing formulary decisions and reimbursement policies globally.

- As the market matures, the biosimilar landscape for checkpoint inhibitors is becoming a critical factor, with a potential to increase patient access but also intensify price competition. This has spurred innovation, with a significant focus on the future of bispecific antibody therapies, which promise enhanced efficacy.

- A primary driver of market expansion is the use of checkpoint blockade in early-stage cancers, particularly through adjuvant immunotherapy in resectable cancer and neoadjuvant treatment for breast cancer. The impact of pd-1 inhibitors on survival rates is well-documented, yet overcoming resistance to checkpoint inhibitors remains a key research frontier.

- The role of companion diagnostics in immunotherapy is indispensable for patient selection for pd-l1 therapy, often guided by pd-l1 expression as a biomarker. Managing immune-related adverse events is a crucial aspect of clinical practice, with specialized protocols showing the ability to reduce average hospital stays by more than a full day compared to institutions without such measures.

- The development of subcutaneous vs intravenous checkpoint inhibitors addresses patient convenience and healthcare system efficiency. As therapies expand to include pd-1 inhibitors in hematological malignancies, navigating the diverse regulatory pathways for immunotherapy drugs becomes increasingly complex, highlighting the economic burden of immunotherapy treatments and the need for robust real-world evidence for checkpoint inhibitors.

What are the key market drivers leading to the rise in the adoption of PD-1 And PD-L1 Inhibitors Industry?

- A key market driver is the strategic expansion of therapeutic applications into earlier disease stages, broadening the patient population and enhancing treatment outcomes.

- Market growth is significantly propelled by the strategic therapeutic expansion of checkpoint inhibitors into earlier stages of cancer care. The integration of neoadjuvant immunotherapy and adjuvant checkpoint blockade into treatment protocols for resectable tumors is broadening the addressable patient population.

- Clinical trials have demonstrated that this early intervention can improve event-free survival by more than 20% in certain cancers, such as metastatic melanoma.

- This success is driving further research into the overall survival benefit across a wider range of solid tumor indications and hematological malignancies. The robust immuno-oncology drug development pipeline, focused on creating effective checkpoint inhibitor combinations, continues to fuel this expansion.

- Exploring cemiplimab uses and other novel agents in these settings is a primary focus of ongoing research.

What are the market trends shaping the PD-1 And PD-L1 Inhibitors Industry?

- A significant market trend is the transition toward subcutaneous formulations. This shift aims to enhance the convenience and efficiency of administration for patients and healthcare providers.

- Key trends are reshaping the market, with a notable shift toward developing bispecific antibodies and advanced subcutaneous formulations. These innovations are critical elements of checkpoint inhibitor lifecycle management, designed to offer superior efficacy and patient convenience. The move to subcutaneous delivery, for example, has been shown to reduce patient chair time by over 80% compared to standard intravenous infusion.

- This transition not only improves the patient experience but also optimizes clinical resources. As the immuno-oncology pipeline matures, the focus on atezolizumab side effects and the management of irAEs becomes increasingly important for long-term treatment success. The development of sophisticated therapies like bispecific checkpoint inhibitors represents the next frontier in cancer treatment.

What challenges does the PD-1 And PD-L1 Inhibitors Industry face during its growth?

- High treatment costs and complex reimbursement landscapes present a significant challenge to industry growth and patient access.

- Significant challenges constrain market access, primarily related to the high costs of programmed cell death protein 1 therapies and complex oncology drug reimbursement pathways. The financial burden on healthcare systems and patients can be substantial, with out-of-pocket costs contributing to treatment discontinuation rates of up to 15% in certain underinsured populations.

- This issue is compounded by the need for a robust regulatory approval process for new indications and combinations, which can be lengthy and expensive. Furthermore, navigating PD-1 vs PD-L1 inhibitors for specific indications requires clear clinical guidelines and a strong evidence base.

- As classical hodgkin lymphoma and HER2+ gastric cancer treatments evolve, ensuring equitable access remains a critical hurdle for the industry.

Exclusive Technavio Analysis on Customer Landscape

The pd-1 and pd-l1 inhibitors market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the pd-1 and pd-l1 inhibitors market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of PD-1 And PD-L1 Inhibitors Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, pd-1 and pd-l1 inhibitors market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agenus Inc. - The portfolio includes advanced PD-1 and PD-L1 inhibitors, focusing on the development and commercialization of transformative treatments for various oncological indications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agenus Inc.

- AnaptysBio Inc.

- AstraZeneca Plc

- BeiGene Ltd.

- Bristol Myers Squibb Co.

- Coherus Oncology Inc

- CStone Pharmaceuticals

- F. Hoffmann La Roche Ltd.

- GlaxoSmithKline Plc

- Incyte Corp.

- Innovent Biologics Inc.

- Jiangsu Hengrui Pharmaceuticals

- MacroGenics Inc.

- Merck and Co. Inc.

- Merck KGaA

- Merus N.V.

- Pfizer Inc.

- Regeneron Pharmaceuticals Inc.

- Sanofi SA

- Shanghai Henlius Biotech Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Pd-1 and pd-l1 inhibitors market

- In January 2025, Pfizer Inc. announced positive topline results from its pivotal Phase III CREST trial, which evaluated sasanlimab in combination with Bacillus Calmette-Guerin for treating non-muscle invasive bladder cancer.

- In February 2025, Shanghai Henlius Biotech Inc. announced that its PD-L1 antibody-drug conjugate, HLX43, had successfully completed the first patient dosing in a Phase II clinical trial for advanced solid tumors.

- In March 2025, the U.S. Food and Drug Administration granted traditional approval to Merck and Co. Inc.'s Pembrolizumab, used in combination with trastuzumab and chemotherapy, for treating HER2-positive gastric or gastroesophageal junction adenocarcinoma that expresses PD-L1.

- In September 2025, the U.S. Food and Drug Administration approved the subcutaneous injection formulation of Merck and Co. Inc.'s pembrolizumab for all previously approved adult solid tumor indications, streamlining administration.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled PD-1 And PD-L1 Inhibitors Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 284 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 19.1% |

| Market growth 2026-2030 | USD 70194.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 17.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Indonesia, Thailand, Brazil, Saudi Arabia, UAE, Turkey, Argentina, Chile, South Africa and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The PD-1 and PD-L1 inhibitors market is characterized by rapid therapeutic expansion, where monoclonal antibody therapy targets the immune checkpoint pathway to restore T-cell activation. The focus on enhancing anti-tumor immunity is driving the evolution of cancer immunotherapy from late-stage to perioperative settings, including neoadjuvant therapy and adjuvant treatment.

- This strategic shift addresses a wider range of solid tumor indications and hematological malignancies. The development of novel combination therapies, including those with antibody-drug conjugates (ADCs) and bispecific antibodies, is crucial for overcoming resistance. Innovation in administration is also a key theme, with a move toward subcutaneous formulations over traditional intravenous infusion.

- Within this landscape, the tumor microenvironment and biomarker expression levels are central to research. The adoption of standardized companion diagnostics to guide treatment for conditions like platinum-resistant ovarian cancer and non-small cell lung cancer has improved patient stratification, leading to a 30% increase in clinical trial enrollment efficiency for specific indications.

- Managing immune-related adverse events (irAEs) and navigating biosimilar competition are critical operational challenges for stakeholders in the immuno-oncology field.

What are the Key Data Covered in this PD-1 And PD-L1 Inhibitors Market Research and Growth Report?

-

What is the expected growth of the PD-1 And PD-L1 Inhibitors Market between 2026 and 2030?

-

USD 70.19 billion, at a CAGR of 19.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Solid tumors, and Blood-related tumors), Type (PD-1, and PD-L1), Distribution Channel (Hospital, Retail, and Online pharmacies) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Strategic expansion of therapeutic applications into earlier disease stages, High treatment costs and reimbursement complexities

-

-

Who are the major players in the PD-1 And PD-L1 Inhibitors Market?

-

Agenus Inc., AnaptysBio Inc., AstraZeneca Plc, BeiGene Ltd., Bristol Myers Squibb Co., Coherus Oncology Inc, CStone Pharmaceuticals, F. Hoffmann La Roche Ltd., GlaxoSmithKline Plc, Incyte Corp., Innovent Biologics Inc., Jiangsu Hengrui Pharmaceuticals, MacroGenics Inc., Merck and Co. Inc., Merck KGaA, Merus N.V., Pfizer Inc., Regeneron Pharmaceuticals Inc., Sanofi SA and Shanghai Henlius Biotech Inc.

-

Market Research Insights

- The market is shaped by a deep understanding of the PD-1 inhibitor mechanism and the ongoing effort to overcome immunotherapy resistance mechanisms. Checkpoint inhibitor lifecycle management is a key strategic focus, with companies exploring novel formulations and combinations to extend product viability.

- This competitive environment is fostering the integration of value-based oncology care models, where reimbursement is increasingly tied to patient outcomes. These models have demonstrated an ability to reduce non-essential expenditures by over 10% in accountable care organizations.

- Concurrently, the refinement of PD-L1 testing methods and companion diagnostics for PD-L1 has improved patient stratification, leading to response rate improvements of up to 20% in select patient cohorts with refractory cancer immunotherapy needs. This data-driven approach is critical for justifying treatment decisions and navigating complex payer requirements.

We can help! Our analysts can customize this pd-1 and pd-l1 inhibitors market research report to meet your requirements.

RIA -

RIA -