Penicillin Market Size 2024-2028

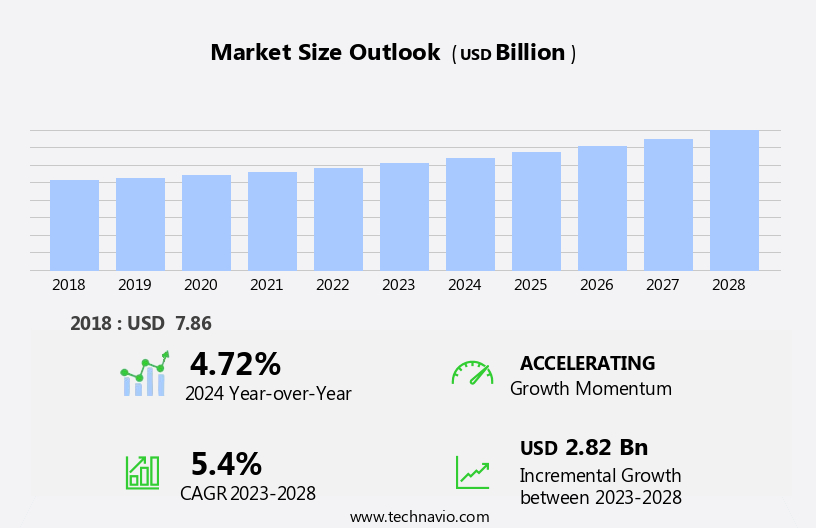

The penicillin market size is forecast to increase by USD 2.82 billion at a CAGR of 5.4% between 2023 and 2028.

- The market is experiencing significant growth driven by the rising prevalence of infectious diseases worldwide. According to the World Health Organization, infectious diseases account for approximately 15 million deaths annually, making it a major public health concern. Penicillin, as the world's first antibiotic, remains a cornerstone in infectious disease treatment. However, market growth is not without challenges. Strategic alliances and mergers and acquisitions among penicillin companies are transforming the competitive landscape. These collaborations aim to expand market reach, enhance product portfolios, and improve operational efficiencies. Furthermore, the increasing use of alternative therapies, such as biologics and antimicrobial peptides, is resulting in decreased purchase of penicillin.

- Companies must navigate this shift by investing in research and development to innovate and differentiate their offerings. In summary, the market presents both opportunities and challenges for stakeholders. Companies seeking to capitalize on market opportunities must stay abreast of emerging trends, collaborate effectively, and invest in research and development to maintain a competitive edge.

What will be the Size of the Penicillin Market during the forecast period?

- The market is experiencing significant shifts due to the impact of generic medications and disruptions in supply chains caused by lockdowns. The demand for narrow spectrum penicillin, such as generic penicillin medication, remains strong for treating bacterial infections caused by Neisseria meningitidis and respiratory tract infections. The source of penicillin includes finished products derived from natural penicillin and R&D efforts for semisynthetic penicillin like aminopenicillin and ampicillin. The spectrum of activity for penicillin extends to various bacterial infections, including those caused by Streptococcus pyogenes, pneumonia, and penicillinase-resistant penicillin for combating Streptococcus pneumoniae. Travel restrictions have influenced the market dynamics, leading to increased demand for brand-name counterparts of broad spectrum penicillin.

- Raw materials and production processes are undergoing continuous improvements to address antimicrobial resistance (AMR). The market is seeing a shift towards capsules and injections for better patient compliance and treatment efficacy. Key players are investing in R&D to develop penicillinase-resistant penicillin and broad spectrum penicillin to cater to the evolving needs of the healthcare industry. In summary, the market is adapting to the challenges posed by the global health crisis and the increasing prevalence of bacterial infections. Players are focusing on innovation and improving production processes to cater to the growing demand for effective penicillin-based treatments.

How is this Penicillin Industry segmented?

The penicillin industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Source

- Semisynthetic

- Natural

- Type

- Oral

- Parenteral

- Geography

- North America

- US

- Canada

- Europe

- Germany

- UK

- Middle East and Africa

- APAC

- China

- South America

- Rest of World (ROW)

- North America

By Source Insights

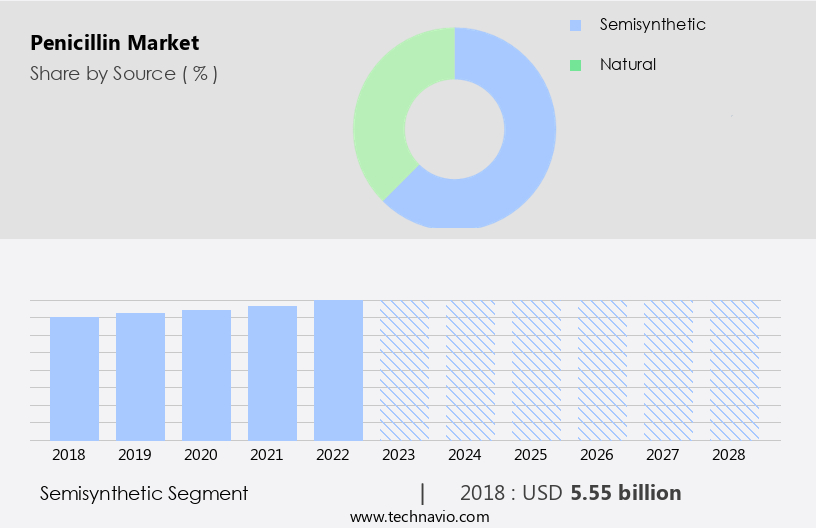

The semisynthetic segment is estimated to witness significant growth during the forecast period.

Semisynthetic penicillin, derived from naturally occurring antibiotics through hydrolysis and further synthesis, offers expanded coverage against a broad spectrum of organisms, including streptococci, staphylococci, aerobic Gram-negative bacteria, and anaerobes. This class of antibiotics can be administered orally and parenterally, making it a cost-effective alternative to other antibiotics. In most instances, semisynthetic penicillin can be used alone for treating various bacterial infections, such as ear infections, respiratory tract infections, and urinary tract infections. However, for highly resistant organisms, like Pseudomonas aeruginosa, combination therapy with aminoglycosides may be required. The development of penicillinase-resistant penicillin and semisynthetic penicillin has significantly impacted the treatment landscape for various bacterial infections, including meningococcal meningitis, pneumonia, and gonorrhea.

These advancements have been crucial in addressing the growing concern of antimicrobial resistance (AMR) and the need for novel antibacterials. Semisynthetic penicillin is produced using raw materials sourced globally, with significant manufacturing capacity in Europe. The market for semisynthetic penicillin is diverse, with various players, including brand-name counterparts, generic medications, and online providers, catering to the needs of various stakeholders, such as hospitals, retail pharmacies, and individual consumers. The aging demographic and the increasing prevalence of bacterial infections are key drivers for the growth of the semisynthetic the market.

Get a glance at the market report of share of various segments Request Free Sample

The Semisynthetic segment was valued at USD 5.55 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

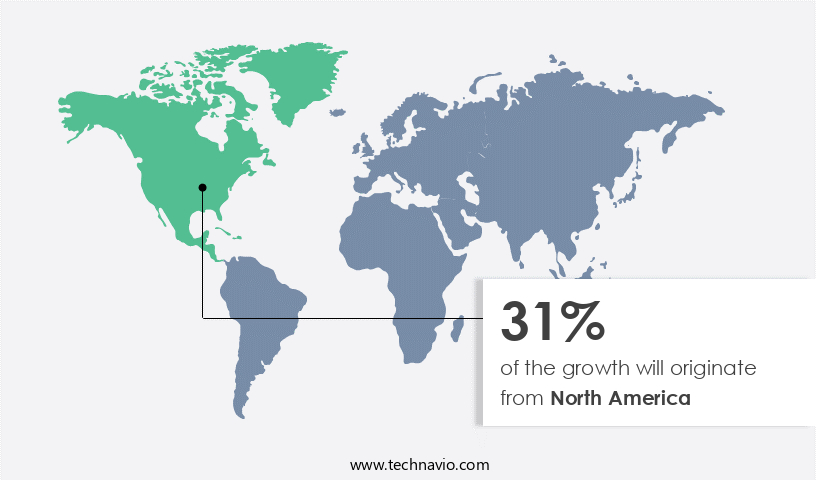

North America is estimated to contribute 31% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The Penicillin drug market experiences a complex landscape shaped by various factors. Reimbursement policies and co-pay assistance programs in developed regions enable individuals to access medical treatment, yet the increasing availability of generic drugs partially offsets growth. Cost containment strategies have led some manufacturers to explore new markets such as Brazil, China, and India for better business opportunities. Favorable regulatory initiatives for antibiotic approvals encourage drug developers to innovate, despite a decreasing consumption trend in the US due to heightened awareness and the growing adoption of generics. Infectious diseases continue to pose a significant challenge, with respiratory tract infections, scarlet fever, and meningococcal meningitis among the most common.

Penicillin and its derivatives, including broad and narrow spectrum penicillins, remain crucial in treating various bacterial infections, including those caused by Streptococcus pneumoniae, Streptococcus pyogenes, and Neisseria meningitidis. However, the emergence of antimicrobial resistance (AMR) and the need for novel antibacterials is a pressing concern. Semisynthetic penicillins and beta-lactamase inhibitors, such as xeruborbactam, are essential tools in combating AMR. These advanced treatments, along with combination medications and brand-name counterparts, are increasingly being used to address the threat of antibiotic resistance. Ampicillin, amoxicillin, and other antibiotics continue to be popular choices for treating various bacterial infections, including urinary tract infections, ear infections, pneumonia, and gonorrhea.

The market for antibiotics is influenced by various factors, including the spectrum of activity, route of administration, and the presence of gram-positive and gram-negative bacteria. Injections, capsules, and oral medications are the primary delivery systems, with finished products and drug formulations playing a significant role in the market's dynamics. The aging demographic and the rising prevalence of bacterial infections, particularly in developing regions, further contribute to the market's growth. Despite the challenges, the market for antibiotics remains a critical component of global healthcare systems. The ongoing R&D efforts to develop new antibiotics and delivery systems, as well as the increasing focus on AMR, ensure that the market remains dynamic and evolving.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Penicillin Industry?

- Rising prevalence of infectious diseases is the key driver of the market.

- The global health landscape has been significantly impacted by the rise in infectious diseases, with the World Health Organization reporting over 14.9 million deaths associated with such diseases in 2020 and 2021. Infectious diseases are caused by pathogens and can be transmitted through direct or indirect contact. Demographic changes, particularly urbanization, have emerged as major contributors to the global proliferation of these diseases. Urbanization has led to overcrowding, increasing the likelihood of disease transmission. As globalization continues to expand, international travel and trade facilitate the spread of pathogens across borders. These factors underscore the importance of effective treatments and preventative measures in mitigating the impact of infectious diseases.

- Penicillin, a widely-used antibiotic, plays a crucial role in treating various bacterial infections. Its antimicrobial properties make it an essential tool in the fight against infectious diseases. The market for penicillin is driven by the growing prevalence of infectious diseases and the increasing demand for effective treatments. The market is expected to grow steadily in the coming years, as the global population continues to grapple with the challenges posed by these diseases.

What are the market trends shaping the Penicillin Industry?

- Strategic alliances and M and A among penicillin vendors is the upcoming market trend.

- Strategic alliances and collaborations play a significant role in the pharmaceutical industry, particularly in the development and commercialization of drugs across various regions. Co-development agreements between pharmaceutical companies enable the sharing of technical expertise, regulatory experience, and development costs, reducing liability risks and attracting venture investments. Mergers and acquisitions (M&A) are another common strategy, aimed at increasing market penetration or enhancing the product portfolio of the parent company. These activities foster innovation and competition in the industry, ultimately benefiting consumers and driving market growth.

- As a professional assistant, I am committed to providing you with accurate and up-to-date information on market dynamics in the pharmaceutical sector. If you require further insights or have specific questions, please do not hesitate to ask.

What challenges does the Penicillin Industry face during its growth?

- Increasing use of alternative therapies resulting in decreased purchase of penicillin is a key challenge affecting the industry growth.

- The market faces challenges due to the increasing preference for alternative medical interventions for treating various infections. For instance, in the case of sinusitis, the choice of antibiotic depends on the severity of the condition. However, the availability of alternative therapies, such as antimicrobial therapy, has led to a decrease in the demand for penicillin and its derivatives. According to the US Department of Health and Human Services, approximately 10% of the US population reported allergies to penicillin in 2022, which is higher among hospital inpatients and residents in healthcare-related facilities. This prevalence of allergies further increases the usage of alternative therapies, thereby impeding the growth of the market.

- Despite these challenges, ongoing research and development efforts in the antibiotics industry are expected to provide opportunities for market growth. The market dynamics are influenced by various factors, including the prevalence of infections, the efficacy of alternative therapies, and the incidence of antibiotic resistance.

Exclusive Customer Landscape

The penicillin market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the penicillin market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, penicillin market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - The company supplies a diverse array of penicillin products, including Abbott Penicillin G Potassium tablets, addressing a broad spectrum of bacterial infections. These effective solutions contribute significantly to the global healthcare landscape, enhancing treatment options for various bacterial afflictions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- AdvaCare Pharma

- Aenova Holding GmbH

- Astellas Pharma Inc.

- Canvax Biotech SL

- Cipla Ltd.

- F. Hoffmann La Roche Ltd.

- Fermenta Biotech Ltd.

- Focus Technology Co. Ltd.

- FUJIFILM Corp.

- GlaxoSmithKline Plc

- Glenmark Pharmaceuticals Ltd.

- Lupin Ltd.

- Merck KGaA

- Novartis AG

- Pfizer Inc.

- Recipharm AB

- Sanofi SA

- Viatris Inc.

- Wellona Pharma

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The Penicillin Drug Market encompasses a broad spectrum of antibacterial agents, with Penicillin being a prominent antibiotic in the arsenal against various bacterial infections. This market is characterized by a complex global supply chain, with numerous players involved in the production of raw materials, manufacturing, and distribution of finished products. Sandoz, a leading global company, plays a significant role in the Penicillin Drug Market by providing a wide range of Penicillin-based products. Online providers have emerged as a key distribution channel, offering convenience and accessibility to consumers. Respiratory tract infections, including scarlet fever, are among the common indications for Penicillin use.

R&D efforts are ongoing to develop Penicillinase-resistant Penicillin and other beta-lactam antimicrobials to combat the growing threat of Antimicrobial Resistance (AMR). Raw materials, such as penicillin G and V, are sourced from various suppliers and undergo extensive purification processes before being used in the manufacturing of Penicillin-based drugs. Lockdowns and travel restrictions have impacted the Penicillin Drug Market, disrupting global supply chains and leading to increased demand for local manufacturing in developing regions. Ear infections, pneumonia, and urinary tract infections are among the most common indications for Penicillin use. Manufacturing investments have been made to increase European manufacturing capacity, with a focus on producing broad-spectrum Penicillin and Semisynthetic Penicillin.

Infectious diseases, including meningitis, syphilis, and gonorrhea, continue to be major indications for Penicillin use. The Penicillin Drug Market is segmented into various forms, including tablets, capsules, and injectables. Brand-name counterparts and generic medications are available for most Penicillin-based drugs, with the latter offering cost advantages. Beta-lactamase inhibitors, such as Xeruborbactam, are used to enhance the activity of Penicillin against gram-negative bacteria. The market for Penicillin and other antibiotics is influenced by various factors, including the spectrum of activity, route of administration, and patient demographics. Aging demographics and the increasing prevalence of bacterial infections are expected to drive demand for Penicillin and other antibiotics.

Qpex Biopharma Inc. And Microbiology Insights are among the companies focused on developing novel antibacterials to address the growing threat of AMR. Combination medications and delivery systems are also being explored to improve the efficacy and safety of Penicillin-based drugs. In conclusion, the Penicillin Drug Market is a dynamic and evolving industry, with ongoing efforts to address the challenges posed by AMR and meet the growing demand for effective antibacterial agents. The market is characterized by a complex global supply chain, with numerous players involved in various stages of production and distribution. Penicillin remains a cornerstone of antibacterial therapy, with ongoing R&D efforts focused on developing new formulations and addressing the growing threat of AMR.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

165 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.4% |

|

Market growth 2024-2028 |

USD 2.82 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.72 |

|

Key countries |

US, Canada, UK, Germany, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Penicillin Market Research and Growth Report?

- CAGR of the Penicillin industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the penicillin market growth of industry companies

We can help! Our analysts can customize this penicillin market research report to meet your requirements.

RIA -

RIA -