Pharmaceutical Continuous Manufacturing Market Size 2024-2028

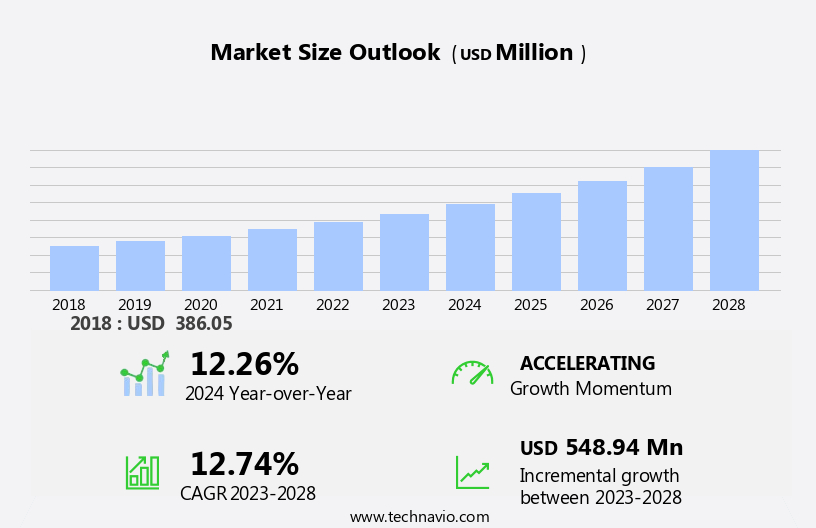

The pharmaceutical continuous manufacturing market size is forecast to increase by USD 548.94 million at a CAGR of 12.74% between 2023 and 2028. The pharmaceutical industry, like many others, is increasingly focused on sustainability, recognizing its importance in reducing environmental impacts, conserving resources, and meeting corporate responsibility goals. Sustainability initiatives include minimizing waste, reducing energy consumption, and implementing environmentally friendly production methods. Moreover, the integration of technologies like Artificial Intelligence (AI) and Machine Learning (ML) in continuous manufacturing However, continuous manufacturing methods not only enhance efficiency and product quality but also significantly reduce the environmental impact of pharmaceutical production. As the industry continues to prioritize sustainability, the global market for continuous manufacturing is expected to grow substantially during the forecast period.

The market is witnessing significant growth in various sectors, including tablets, capsules, coatings, and dosage forms. This manufacturing approach offers several advantages, such as increased productivity, improved product quality, and reduced production costs. The use of advanced technologies like Syntem and Caterpillar's Continuous Manufacturing Cell (CMC) is driving the market forward. The tablets segment is expected to dominate the market due to the high demand for oral solid dosage forms. The capsules segment is also gaining popularity due to their advantages over tablets, such as better bioavailability and patient compliance.

Consequently, coatings, another significant application area, are essential for improving the efficacy and stability of pharmaceutical products. The global market for Pharmaceutical Continuous Manufacturing is projected to grow at a steady pace, with key players focusing on innovation and collaboration to expand their offerings. The market is expected to face challenges such as regulatory compliance and high initial investment costs. However, the benefits of continuous manufacturing are expected to outweigh these challenges, making it a promising trend in the pharmaceutical industry.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

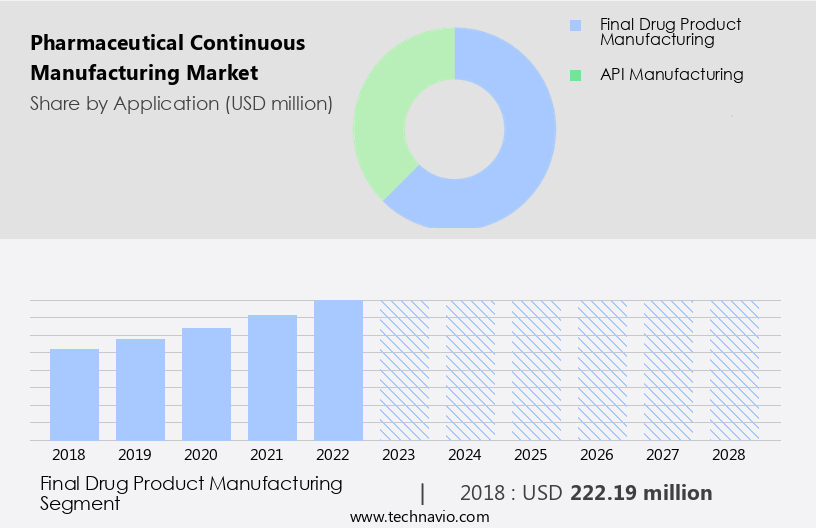

- Final drug product manufacturing

- API manufacturing

- Product

- Integrated systems

- Semi-continuous systems

- Controls or software

- Geography

- North America

- US

- Europe

- Germany

- UK

- Asia

- China

- Japan

- Rest of World (ROW)

- North America

By Application Insights

The final drug product manufacturing segment is estimated to witness significant growth during the forecast period. Continuous manufacturing streamlines the production process by integrating Upstream Bioprocessing and Downstream Bioprocessing, reducing timelines and increasing productivity. It ensures better control over critical process parameters, leading to improved product consistency and quality. Essential medicines, including small molecule drugs and their APIs, can be produced more efficiently and cost-effectively using this method. Continuous manufacturing minimizes variability and reduces the risk of defects, ensuring regulatory compliance. Operating costs are also reduced through labor savings, equipment maintenance, and energy consumption.

Get a glance at the market share of various segments Request Free Sample

The final drug product manufacturing segment was valued at USD 222.19 million in 2018 and showed a gradual increase during the forecast period.

Regional Insights

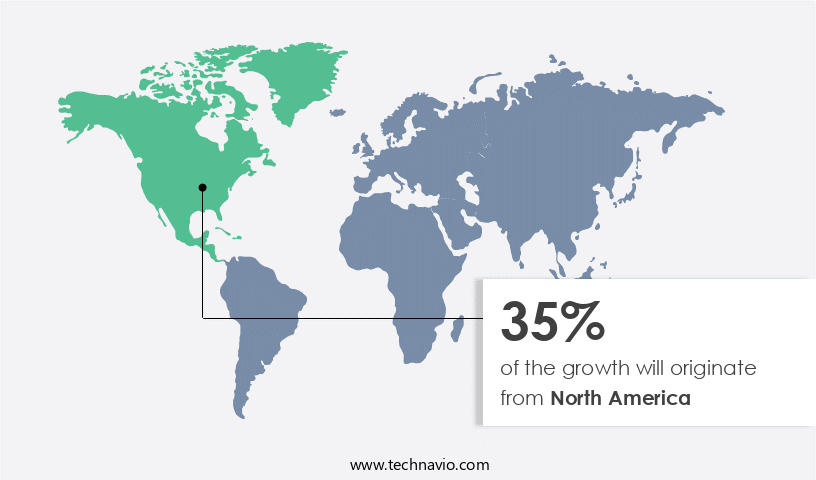

North America is estimated to contribute 35% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The Pharmaceuticals industry in North America utilizes continuous manufacturing to address drug shortages and patient demands for high-quality, affordable medicines. Technologies such as semi-continuous systems, continuous granulators, blenders, compressors, coaters, and dryers streamline the production of sterile injectables, oncology treatments, and biologics. Integrated continuous systems, including tablet and granulation processes, offer real-time monitoring, quality control, and material waste reduction. Untapped emerging markets and integrated process control enhance the production of pharmaceutical drug substances from raw materials to finished products, ensuring drug quality through active ingredient management and staff training. Other semi-continuous systems support solid and liquid dosage manufacturing.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The increasing prevalence of chronic diseases is the key driver of the market. The market is driven by the increasing production of small molecule drugs and Active Pharmaceutical Ingredients (APIs) in emerging economies. With preclinical and clinical trials leading to the approval of new drugs, the demand for finished dosage forms is surging.

Further, this trend is particularly noticeable in countries like India and China, where urbanization and rising disposable incomes are fueling pharmaceutical industry growth. To meet this demand, manufacturers are expanding their production capacity for essential medicines, focusing on both upstream bioprocessing and downstream bioprocessing. This growth is anticipated to continue during the forecast period.

Market Trends

The growing digitalization and integration of Industry 4.0 in continuous manufacturing is the upcoming trend in the market. The trend towards lightweighting in the automotive industry is mirrored in the pharmaceutical sector with the continuous manufacturing market for small molecule drugs. The use of lighter materials, such as titanium and advanced alloys, in the production of Active Pharmaceutical Ingredients (APIs) and Finished Dosage Forms (FDFs) is encouraged.

Further, this approach reduces the overall weight of pharmaceutical products without compromising performance, contributing to improved fuel efficiency and reduced emissions, similar to the automotive industry. Upstream bioprocessing and downstream bioprocessing are being optimized through the development of novel designs, utilizing lightweight materials to enhance endurance and performance. This focus on lightweighting aligns with the broader pharmaceutical industry goals of sustainability and enhanced performance, driving the growth of continuous manufacturing technology for essential medicines and small molecule drugs.

Market Challenge

The regulatory complexity in the pharmaceutical industry is a key challenge affecting the market growth. In the pharmaceutical industry, the production of small molecule drugs and active pharmaceutical ingredients (APIs) for finished dosage forms must adhere to stringent environmental regulations. The upstream bioprocessing and downstream processing of pharmaceutical ingredients, including essential medicines, are subject to scrutiny during preclinical and clinical stages. Traditional manufacturing methods may be reevaluated due to their energy-intensive nature and potential toxic emissions.

However, to minimize the carbon footprint, pharmaceutical companies are investigating alternative materials and processes, such as continuous manufacturing and the use of lightweight metals or composites in the production of APIs. Waste management is also a critical concern, as abandoned materials and byproducts must be disposed of properly. Sustainable manufacturing practices, including recycling and minimizing toxic emissions, are essential for meeting regulatory requirements and consumer expectations in the market.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Coperion GmbH - The company offers products such as pharma extruders, and process equipment.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Chemtrix BV

- Continuus Pharmaceuticals

- Corning Inc.

- Dr. Helmut Rothenberger Holding GmbH

- Eli Lilly and Co.

- Freund Vector Corp.

- GE Healthcare Technologies Inc.

- GEA Group AG

- Gebruder Lodige Maschinenbau GmbH

- Gericke AG

- Honeywell International Inc.

- Hosokawa Micron Corp.

- Hovione

- KORSCH AG

- L.B. Bohle Maschinen und Verfahren GmbH

- LMT Group

- Novartis AG

- Pfizer Inc.

- Siemens AG

- SK Inc.

- Syntegon Technology GmbH

- Thermo Fisher Scientific Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is experiencing significant growth due to the increasing demand for efficient and cost-effective production methods in the industry. Systems and technologies, such as Patents, Drugs, Shortages, Syntheses, Compressors, Oncology, Quality, Unprocessed, Producers, and Solids, play a crucial role in this market. Continuous manufacturing in pharmaceuticals involves the production of drugs without interruption, allowing for real-time monitoring and adjustment of the process. The Pharmaceutical Continuous Manufacturing Market is gaining significant traction due to its potential to address critical issues in the healthcare sector, including drug shortages and the production of essential medicines and drugs, particularly in areas like oncology and cancer treatments. Continuous manufacturing, which includes processes such as continuous blenders, compressors, coaters, and dryers, offers several advantages over traditional batch manufacturing methods. Continuous manufacturing streamlines the production of active pharmaceutical ingredients (APIs) and base ingredients, ensuring a consistent supply of molecules and biologics for health systems and patients. This integrated continuous system is particularly beneficial for sterile injectable medications, where manual handling is minimized, reducing the risk of contamination.

The pharmaceutical industry is increasingly adopting continuous manufacturing for solid dosage manufacturing, including tablet production and coating processes. Quality monitoring is ensured through real-time analysis, ensuring the production of finished dosage forms that meet regulatory requirements. The Drug Shortage Task Force has identified continuous manufacturing as a potential solution to address drug shortages, particularly for essential medicines. Continuous manufacturing systems, including semicontinuous systems, offer the flexibility to produce multiple products, reducing the risk of production downtime and ensuring a consistent supply of APIs and finished dosage forms. In the preclinical and clinical stages of drug development, continuous manufacturing can help streamline the production of drug molecules and APIs, reducing development timelines and costs. Overall, the Pharmaceutical Continuous Manufacturing Market is poised for significant growth, offering numerous benefits to the healthcare sector and patients.

In conclusion, this results in improved product quality, increased efficiency, and reduced costs. The processes further enhances their capabilities. These technologies enable predictive maintenance, real-time process optimization, and improved yield. The market for Pharmaceutical Continuous Manufacturing is expected to grow at a steady pace in the coming years, driven by the increasing adoption of these advanced technologies and the need for more efficient and cost-effective production methods in the industry.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

171 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 12.74% |

|

Market growth 2024-2028 |

USD 548.94 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

12.26 |

|

Regional analysis |

North America, Europe, Asia, and Rest of World (ROW) |

|

Performing market contribution |

North America at 35% |

|

Key countries |

US, Germany, UK, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Chemtrix BV, Continuus Pharmaceuticals, Coperion GmbH, Corning Inc., Dr. Helmut Rothenberger Holding GmbH, Eli Lilly and Co., Freund Vector Corp., GE Healthcare Technologies Inc., GEA Group AG, Gebruder Lodige Maschinenbau GmbH, Gericke AG, Honeywell International Inc., Hosokawa Micron Corp., Hovione, KORSCH AG, L.B. Bohle Maschinen und Verfahren GmbH, LMT Group, Novartis AG, Pfizer Inc., Siemens AG, SK Inc., Syntegon Technology GmbH, and Thermo Fisher Scientific Inc. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -