Polar Polymers Market Size 2026-2030

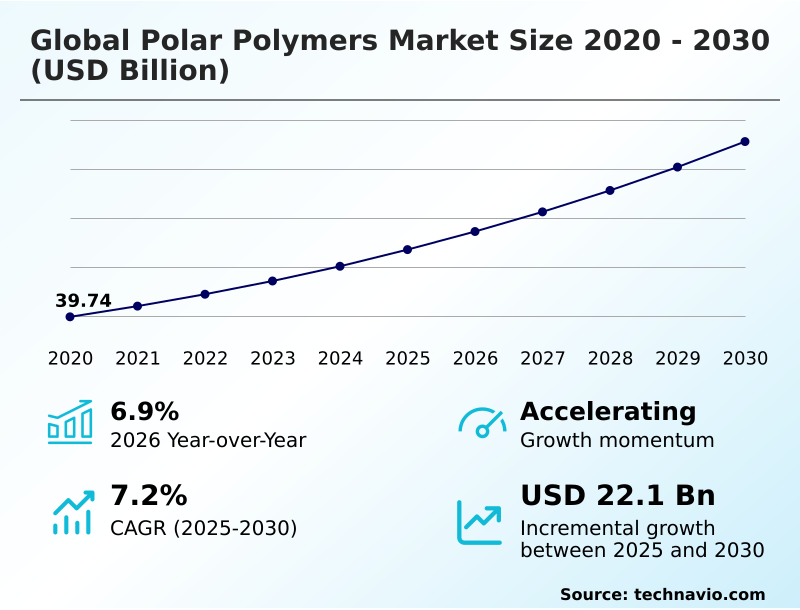

The polar polymers market size is valued to increase by USD 22.10 billion, at a CAGR of 7.2% from 2025 to 2030. Surging adoption of electric vehicles and advanced electronics propelling demand will drive the polar polymers market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 49.9% growth during the forecast period.

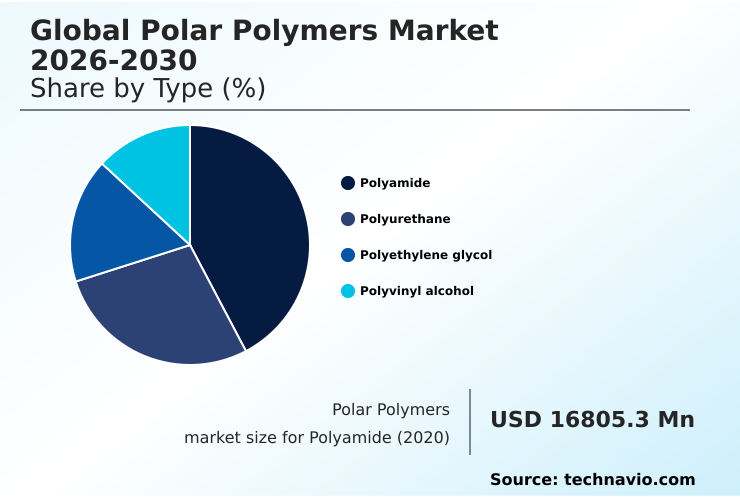

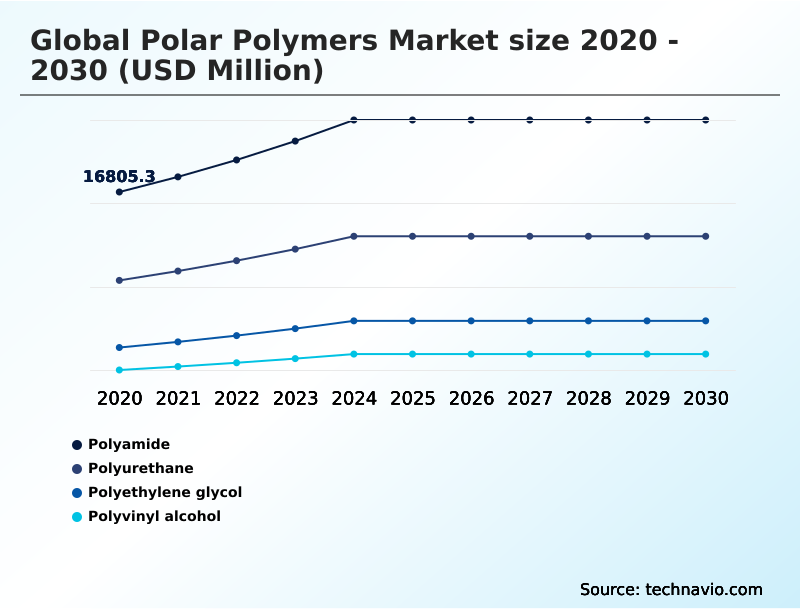

- By Type - Polyamide segment was valued at USD 21.49 billion in 2024

- By Application - Films segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 35.85 billion

- Market Future Opportunities: USD 22.10 billion

- CAGR from 2025 to 2030 : 7.2%

Market Summary

- The polar polymers market is defined by materials exhibiting distinct properties like adhesion and chemical resistance, stemming from their molecular structure. This makes them indispensable in high-performance applications. Key drivers include the global transition to electric mobility and the expansion of the healthcare sector, which demand materials with superior thermal and mechanical characteristics.

- A major trend is the industry's pivot toward sustainability, with a focus on bio-based feedstocks and establishing circular economies to address regulatory pressures and consumer preferences. For instance, an automotive original equipment manufacturer must now evaluate material substitutions, balancing the performance of an advanced polyamide against the cost benefits of a modified non-polar alternative to meet new recycled-content mandates.

- This scenario directly impacts its supply chain and compliance strategy. However, the market faces challenges from volatile feedstock prices and intense competition from alternative materials, which can narrow profit margins and influence material selection in cost-sensitive applications. The interplay of these dynamics shapes a market characterized by continuous innovation in material science.

What will be the Size of the Polar Polymers Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Polar Polymers Market Segmented?

The polar polymers industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Polyamide

- Polyurethane

- Polyethylene glycol

- Polyvinyl alcohol

- Application

- Films

- Coatings

- Adhesives

- Others

- End-user

- Electronics

- Consumer goods

- Automotive

- Medical

- Geography

- APAC

- China

- Japan

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Type Insights

The polyamide segment is estimated to witness significant growth during the forecast period.

The polyamide segment is foundational to the market for engineering plastics, driven by the unique properties derived from its molecular structure.

This class of polymers is indispensable in demanding sectors such as automotive components and e-mobility applications, where its high mechanical strength and thermal stability are critical for under-the-hood parts and battery systems.

The market is also heavily influenced by the adoption of circular economy models, pushing for innovations in advanced polymer science to improve the recyclability of materials used in consumer goods packaging and medical device manufacturing.

With a demonstrated year-over-year expansion of 6.9%, the segment's trajectory is tied to its role in producing lightweighting materials and its electrical insulation properties, which are essential for textile fibers and modern construction materials.

The Polyamide segment was valued at USD 21.49 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 49.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Polar Polymers Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the market is increasingly dominated by the APAC region, which is projected to contribute nearly 50% of incremental growth.

This is driven by its role as a global manufacturing hub for electronics and automotive sectors, creating massive demand for polar polymer chemistry.

In contrast, the markets in North America and Europe are characterized by technological maturity and a strong focus on sustainability.

Europe's stringent regulations, which mandate a significant reduction in packaging waste, are accelerating the adoption of materials with high surface energy and recyclability. The use of waterborne polyurethane dispersions and structural adhesives is expanding due to environmental compliance needs.

These regional differences require producers to tailor their polymer formulations, leveraging properties like dipole-dipole interactions to meet diverse performance and regulatory standards across the globe.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions within the global polar polymers market 2026-2030 are increasingly shaped by nuanced material trade-offs. The impact of polar polymers in EVs is profound, with PVDF binders for lithium-ion batteries becoming a critical component for enhancing energy density and lifespan. In parallel, polyurethane foam for building insulation addresses energy efficiency mandates.

- The choice between polyamide versus polypropylene in automotive interiors often hinges on balancing scratch resistance with cost. For high-frequency electronics, selecting advanced materials for 5G infrastructure can reduce signal loss by a factor of two compared to standard options. The trend towards polar polymers for medical device manufacturing is driven by biocompatibility and sterilization needs, particularly for single-use devices.

- In packaging, the debate around bio-based polar polymers in packaging and recycled PET in food-grade packaging is guided by circular economy goals. At the same time, advancements in polar polymer films for flexible displays are enabling new product form factors.

- Innovations in waterborne coatings for VOC reduction and polar polymers in structural adhesives for lightweighting reflect responses to regulatory pressures and performance demands, while PFAS restrictions on fluoropolymer usage present significant challenges for certain high-performance applications.

What are the key market drivers leading to the rise in the adoption of Polar Polymers Industry?

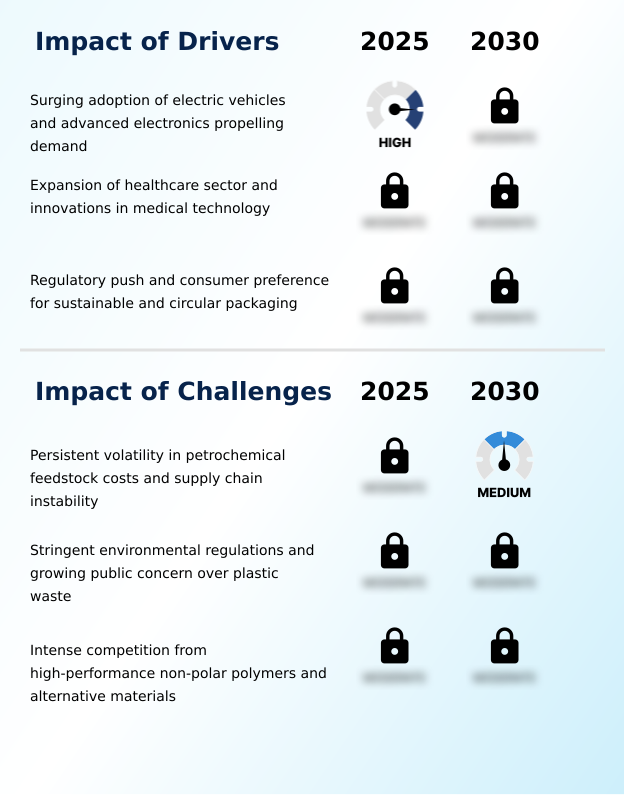

- The surging adoption of electric vehicles and the continuous advancement of electronic devices are key drivers propelling demand in the market.

- Demand is being significantly propelled by the growth of electric vehicles and advanced electronics. These sectors require high-performance polyamides and flame-retardant polymers for critical applications like thermal management systems and electronic device housings, where safety and reliability are paramount.

- In EV batteries, polyvinylidene fluoride (PVDF) is a key material, while low-dielectric-loss materials are essential for 5G telecommunications infrastructure and advanced driver-assistance systems. Lightweighting with polar polymers in EVs can improve battery range by up to 8%.

- The healthcare industry also contributes, with a rising need for single-use medical devices and in-vitro diagnostic platforms. This, coupled with extended producer responsibility regulations, fuels demand for materials suitable for food-grade containers and advanced composite material bonding.

What are the market trends shaping the Polar Polymers Industry?

- The proliferation of bio-based and circular polar polymers represents a significant market trend. This shift is primarily driven by mounting regulatory requirements and increasing consumer demand for sustainable materials.

- A dominant trend is the accelerated shift toward sustainability, driven by corporate ESG mandates and stringent environmental compliance. This is materializing through the development of bio-based polar polymers and robust circular supply chains, with chemical recycling technologies enabling the reuse of materials like recycled polyethylene terephthalate.

- The industry is moving toward mono-material solutions to enhance recyclability, supported by innovative polymer formulations. New thermoplastic polymers derived from renewable feedstocks offer a carbon footprint reduction of up to 40% compared to fossil-based counterparts.

- This pivot is critical in advanced electronics and for lightweighting in transportation, where sustainable packaging solutions are no longer a niche but a core requirement, compelling rapid innovation across the sector.

What challenges does the Polar Polymers Industry face during its growth?

- Persistent volatility in petrochemical feedstock costs, compounded by ongoing supply chain instability, presents a key challenge to industry growth.

- The market faces considerable headwinds from volatile petrochemical feedstocks, where price swings have caused manufacturing costs to fluctuate by as much as 25% quarter-over-quarter, creating significant supply chain instability.

- Compounding this is the intense regulatory scrutiny on substances like per- and polyfluoroalkyl substances (PFAS) and volatile organic compounds (VOCs), which threatens the use of some high-performance fluoropolymers and traditional solvent-based systems. There is also persistent alternative material competition from non-polar polymers and advanced composites, particularly in multi-material assemblies where cost is a primary factor.

- Innovators must focus on properties unique to polar polymers, such as hydrogen bonding, and promote sustainable options like bio-based sourcing and waterborne systems to defend their value proposition against these challenges.

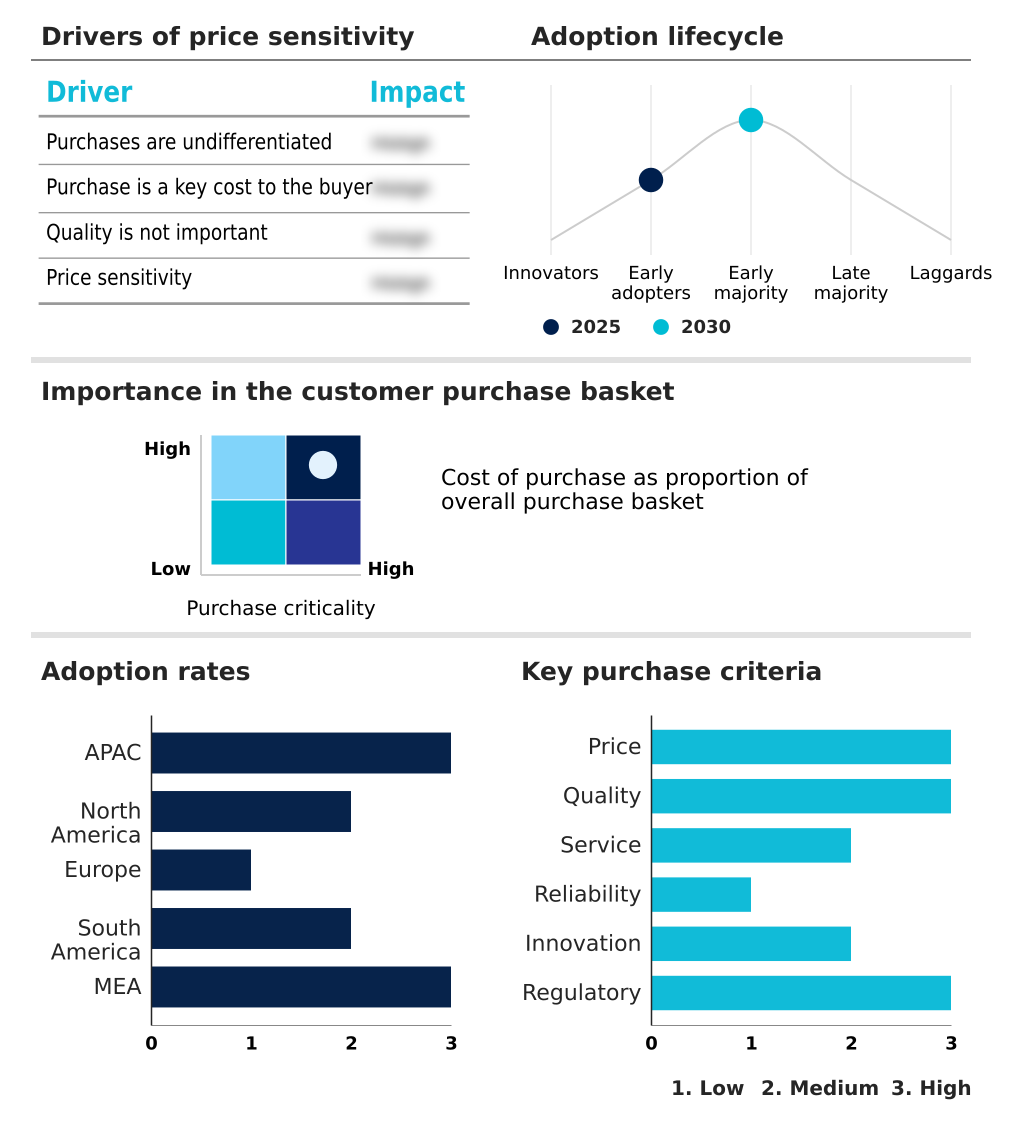

Exclusive Technavio Analysis on Customer Landscape

The polar polymers market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the polar polymers market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Polar Polymers Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, polar polymers market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Arkema Group - The firm's offerings center on high-performance specialty polymers, including advanced materials, adhesives, and coating solutions for demanding industrial applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Arkema Group

- Asahi Kasei Corp.

- BASF SE

- Celanese Corp.

- Covestro AG

- Dow Chemical Co.

- DuPont de Nemours Inc.

- Eastman Chemical Co.

- Evonik Industries AG

- Formosa Plastics Corp.

- Huntsman International LLC

- Lanxess AG

- LG Chem Ltd.

- LyondellBasell Industries NV

- Mitsubishi Chemical Grp.

- Saudi Basic Industries

- Shin Etsu Chemical Co. Ltd.

- Solvay SA

- Sumitomo Chemical Co. Ltd.

- Toray Industries Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Polar polymers market

- In September, 2024, a leading European chemical firm announced the successful commercial-scale production of a new bio-based polyamide derived from non-food agricultural waste, targeting automotive and textile applications.

- In November, 2024, a major Asia-based materials supplier launched a next-generation PVDF binder for EV battery cathodes, promising a 10% increase in charging speeds and cycle life.

- In February, 2025, a North American consortium of polymer manufacturers and automotive OEMs initiated a large-scale pilot program for the chemical recycling of end-of-life vehicle components back into virgin-quality engineering plastics.

- In April, 2025, an American adhesives specialist received aerospace certification for a new structural adhesive designed for bonding dissimilar composite materials, enabling further lightweighting in next-generation aircraft.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Polar Polymers Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 322 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.2% |

| Market growth 2026-2030 | USD 22104.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.9% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The polar polymers market is advancing through continuous material innovation tailored for high-stakes industries. Its trajectory is defined by the development of engineered plastics and specialty polyesters with superior thermal management systems and electrical insulation properties. The adoption of these materials is not merely a technical upgrade but a strategic imperative.

- For instance, boardroom decisions are now heavily influenced by the regulatory landscape surrounding per- and polyfluoroalkyl substances; choosing to invest in PFAS-free alternatives versus risking future market access has profound budgetary and product strategy implications.

- With the market demonstrating a year-over-year expansion of 6.9%, the emphasis is on creating advanced polymer science solutions, including polymer matrix composites and lightweighting materials, that deliver performance while navigating complex compliance frameworks. This involves a deep understanding of polar polymer chemistry to create formulations that meet the demands of applications from single-use medical devices to durable food-grade containers.

What are the Key Data Covered in this Polar Polymers Market Research and Growth Report?

-

What is the expected growth of the Polar Polymers Market between 2026 and 2030?

-

USD 22.10 billion, at a CAGR of 7.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Polyamide, Polyurethane, Polyethylene glycol, and Polyvinyl alcohol), Application (Films, Coatings, Adhesives, and Others), End-user (Electronics, Consumer goods, Automotive, and Medical) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Surging adoption of electric vehicles and advanced electronics propelling demand, Persistent volatility in petrochemical feedstock costs and supply chain instability

-

-

Who are the major players in the Polar Polymers Market?

-

Arkema Group, Asahi Kasei Corp., BASF SE, Celanese Corp., Covestro AG, Dow Chemical Co., DuPont de Nemours Inc., Eastman Chemical Co., Evonik Industries AG, Formosa Plastics Corp., Huntsman International LLC, Lanxess AG, LG Chem Ltd., LyondellBasell Industries NV, Mitsubishi Chemical Grp., Saudi Basic Industries, Shin Etsu Chemical Co. Ltd., Solvay SA, Sumitomo Chemical Co. Ltd. and Toray Industries Inc.

-

Market Research Insights

- The market is shaped by a dynamic interplay between technological advancement and regulatory pressures. The push for e-mobility applications and environmental compliance is accelerating innovation, with structural adhesives enabling a component weight reduction of 25% compared to mechanical fasteners in some automotive components. This focus on performance is mirrored in advanced electronics, where new materials are essential.

- Concurrently, corporate ESG mandates and the need for circular supply chains are compelling manufacturers to adopt renewable feedstocks. In the coatings sector, the transition to waterborne systems has reduced VOC emissions by over 70% in certain facilities, aligning with stricter green building codes. This evolution creates opportunities for firms that can deliver high-performance materials through sustainable and compliant processes.

We can help! Our analysts can customize this polar polymers market research report to meet your requirements.

RIA -

RIA -