Pompe Disease Drugs Market Size 2024-2028

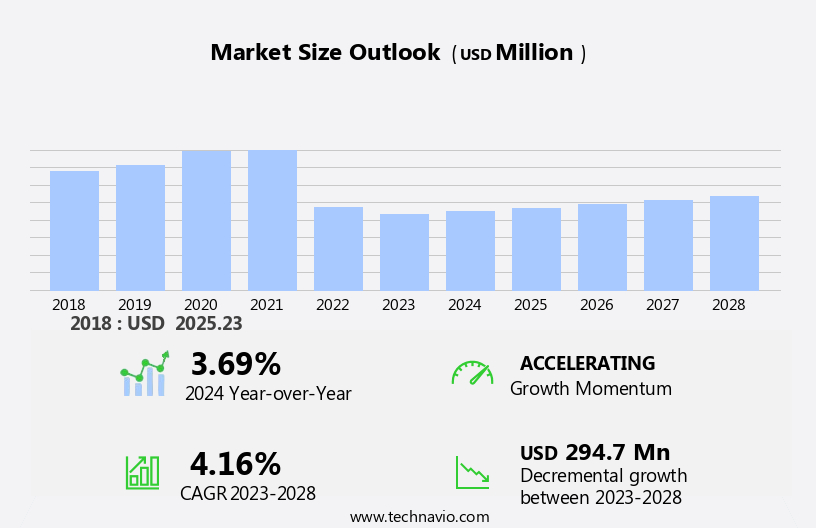

The pompe disease drugs market size is forecast to increase by USD 294.7 million at a CAGR of 4.16% between 2023 and 2028.

- Pompe disease, a genetic disorder marked by progressive muscle weakness and respiratory complications, is gaining attention due to the rising prevalence of its associated genetic mutation. The market is witnessing substantial growth, driven by advancements in treatment options, including the approval of Enzyme Replacement Therapy (ERT) with Acid Alpha-Glucosidase.

- However, the high treatment costs remain challenging for patients and healthcare systems. To address this, initiatives are underway to raise awareness about Pompe disease and its available treatments, aiming to improve patient access and outcomes. Healthcare analytical testing services and healthcare analytics are playing a crucial role in diagnosing and monitoring the disease more effectively. Despite these advancements, the high treatment costs associated with Pompe disease remain a significant challenge, necessitating ongoing efforts to improve patient access and affordability.

What will the Pompe Disease Drugs Market Size be during the forecast period?

- The incidence of Pompe disease, a rare genetic disorder caused by the deficiency of the lysosomal enzyme acid alpha-glucosidase, continues to impact the lives of numerous infants and individuals worldwide. This condition, characterized by the progressive deterioration of organs and tissues, primarily affects the heart and skeletal muscle. Medical advancements have been instrumental in the discovery of various treatment options for Pompe disease. Drug discovery efforts for treating Pompe disease focus on addressing genetic defects in the acid alpha glucosidase gene, which leads to the buildup of sugar in cells, contributing to cardiac abnormalities; with rising Pompe disease prevalence, treatments like Nexviazyme offer hope for managing this autosomal recessive inherited disorder. Two prominent approaches include enzyme replacement therapy (ERT) and gene therapy. ERT aims to replace the missing or deficient enzyme in the body, while gene therapy focuses on introducing a functional copy of the gene into the patient's cells.

- Hospitals and specialized clinics provide the necessary facilities for diagnosis, treatment, and long-term management of Pompe disease. In late onset Pompe disease, an enzyme deficit leads to the accumulation of sugar (glycogen) in muscles, resulting in a gradual loss of muscle strength. Gene therapy, another promising approach, is still under investigation for the treatment of Pompe disease. This innovative technology holds the potential to address the root cause of the condition by introducing a functional copy of the missing gene into the patient's cells. In conclusion, the market is witnessing significant advancements in the form of ERTs and gene therapy. These treatments, while not without challenges, offer hope for those affected by this debilitating condition. The regulatory framework, coupled with strong healthcare infrastructure, plays a crucial role in ensuring the successful implementation of these treatments.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

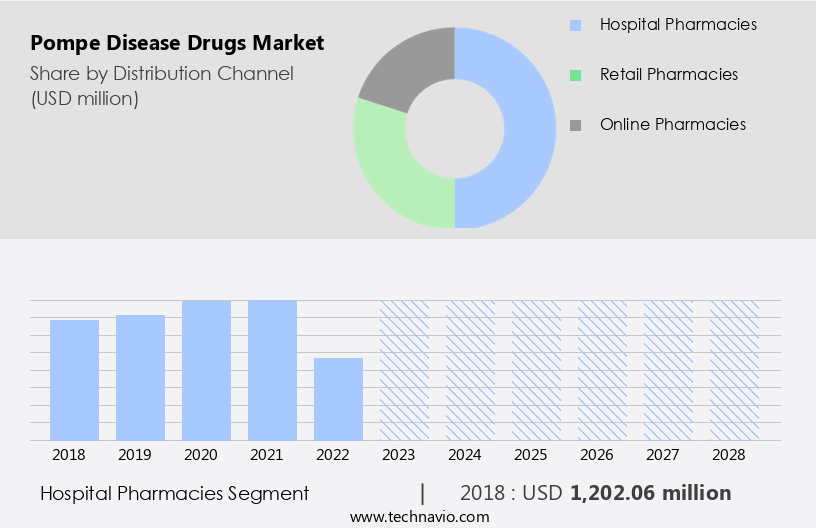

- Distribution Channel

- Hospital pharmacies

- Retail pharmacies

- Online pharmacies

- Therapy

- Enzyme replacement therapy

- Substrate reduction therapy

- Others

- Geography

- North America

- US

- Europe

- Germany

- UK

- Asia

- China

- Japan

- Rest of World (ROW)

- North America

By Distribution Channel Insights

- The hospital pharmacies segment is estimated to witness significant growth during the forecast period.

The hospital pharmacies hold a vital position in the healthcare system, facilitating the distribution and administration of medications for Pompe disease patients. These pharmacies are an essential component of hospitals, catering to inpatients and individuals receiving specialized care. Hospital pharmacies provide prompt access to medications during the acute stages of the disease or when close medical supervision is necessary. The collaboration between healthcare professionals and pharmacists in hospital settings is advantageous, ensuring effective communication and coordination for customized treatment plans. This partnership is crucial for monitoring patient progress, addressing any medication-related concerns, and managing immediate medication requirements during hospitalization. The integration of hospital pharmacies within the healthcare system enables efficient and timely medication management for Pompe disease patients.

Get a glance at the market report of share of various segments Request Free Sample

The hospital pharmacies segment was valued at USD 1.20 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

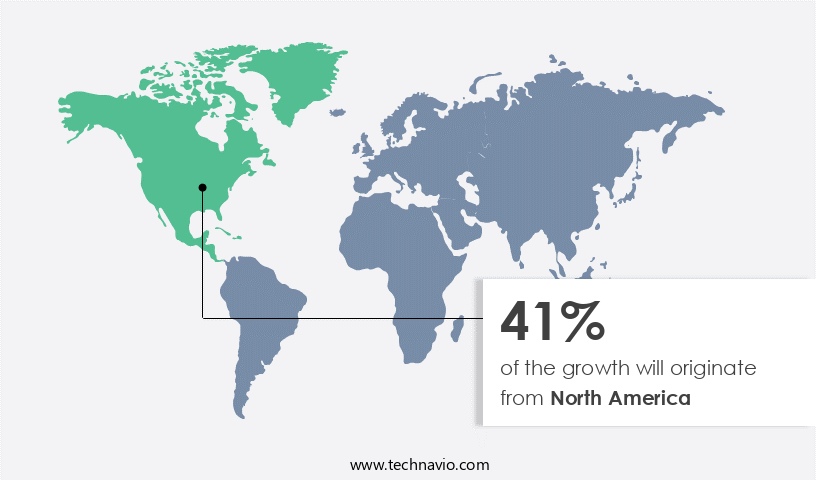

- North America is estimated to contribute 41% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

Pompe Disease, a genetic disorder causing lysosomal storage, primarily affects the heart and muscles. Hypertrophic cardiomyopathy, a common complication, can lead to heart failure. These treatments aim to restore the body's ability to break down glycogen. The US healthcare infrastructure plays a crucial role in ensuring access to these innovative therapies.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of the Pompe Disease Drugs Market?

Increasing efforts to raise awareness regarding Pompe disease is the key driver of the market.

- Pompe disease, a seldom-encountered genetic condition characterized by the absence of acid alpha-glucosidase, frequently escapes diagnosis due to its rarity and the diverse manifestation of symptoms. The significance of increasing awareness among healthcare specialists, such as physicians, genetic counselors, and pediatricians, cannot be overstated in facilitating early detection of this disease.

- Various educational initiatives, including workshops and medical conferences, are instrumental in expanding the expertise and diagnostic skills of healthcare providers regarding Pompe disease. Moreover, public awareness campaigns play a crucial role in enlightening the general populace about this condition. By raising awareness, individuals are empowered to identify potential symptoms and subsequently seek professional medical advice for an accurate diagnosis.

What are the market trends shaping the Pompe Disease Drugs Market?

Approval for new drugs for Pompe treatment is the upcoming trend in the market.

- The pharmaceutical sector in the United States has experienced an increase in research efforts toward the development of new medications for Pompe disease. This condition, characterized by a deficiency of the enzyme acid GAA, results in muscle weakness and weariness. One recent advancement came on September 28, 2023, with the FDA's approval of Amicus Therapeutics' dual-component therapy, Pombiliti (cipaglucosidase alfa-atga) + Opfolda (miglustat) 65mg capsules.

- This therapy, intended for adults with late-onset Pompe disease (LOPD) weighing over 40 kg, is particularly beneficial for those who have not experienced improvement with their existing enzyme replacement therapy (ERT). Late-onset Pompe disease is a severe lysosomal disorder that can significantly impact an individual's quality of life. The approval of this innovative treatment marks a significant step forward in managing this rare condition.

What challenges does the Pompe Disease Drugs Market face during its growth?

High treatment costs associated with Pompe disease is a key challenge affecting the market growth.

- Pompe disease, a genetic disorder causing breathing issues and muscle weakness, affects an estimated 1 in 40,000 people in the US. The disease is caused by a genetic mutation that impacts the production of acid alpha-glucosidase, an essential enzyme. This deficiency leads to a buildup of glycogen in the body's cells, causing various health complications. Enzyme replacement therapies (ERTs), such as alglucosidase alfa (Myozyme and Lumizyme), are the primary treatment option for Pompe disease.

- The financial burden of Pompe disease treatment is significant for healthcare systems and insurers, leading to complex decisions regarding drug reimbursement and coverage. The genetic prevalence of Pompe disease is relatively low, making it a challenge for pharmaceutical companies to justify the high investment required for research and development. The complex science behind developing therapeutic interventions for Pompe disease adds to the costs and complexity. However, ongoing research and advancements in biotechnology may lead to more cost-effective and accessible treatment options in the future. In conclusion, Pompe disease is a rare genetic disorder that requires expensive enzyme replacement therapies for treatment.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market. The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amicus Therapeutics Inc.

- Astellas Pharma Inc.

- AVROBIO Inc.

- Bayer AG

- EpiVax Inc.

- F. Hoffmann La Roche Ltd.

- JCR Pharmaceticals Co. Ltd.

- Johnson and Johnson

- Maze Therapeutics Inc.

- Sanofi SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Pompe disease, a rare genetic disorder caused by a deficiency of the enzyme acid alpha-glucosidase, affects the ability of the body to break down glycogen in organs and tissues, leading to the accumulation of glycogen in cells. The classic infantile form of Pompe disease is characterized by symptoms such as muscle weakness, hypotonia, respiratory insufficiency, and hypertrophic cardiomyopathy in infants. Medical advancements have led to significant progress in the discovery of drugs for Pompe disease. The regulatory framework for these drugs is stringently enforced to ensure safety and efficacy. Gene therapy and enzyme replacement medicines are two primary approaches used to treat Pompe disease.

Furthermore, the genetic defect responsible for Pompe disease is a mutation in the gene that codes for acid alpha-glucosidase. The carrier frequency and genetic prevalence of Pompe disease vary across populations. The pharmaceutical sector has experienced an increase in research efforts toward the development of new medications for Pompe disease, with growing reliance on pharmaceutical contract packaging and pharmaceutical contract research and manufacturing services to streamline production and enhance the efficiency of bringing these treatments to market The disease can affect various organs and tissues, including the heart, skeletal muscles, and respiratory tract. Symptoms of Pompe disease include muscle weakness, weariness, activity intolerance, and breathing issues. Treatment options include enzyme replacement therapy and new medications under development. The healthcare infrastructure plays a crucial role in the diagnosis and management of Pompe disease, with hospitals and specialized clinics providing essential services for patients.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

161 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.16% |

|

Market Growth 2024-2028 |

USD 294.7 million |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

3.69 |

|

Key countries |

US, Germany, UK, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -